Alluvial Capital Management commentary for the second quarter ended June 30, 2021.

Q2 2021 hedge fund letters, conferences and more

Dear Partners,

Alluvial Fund, LP continues to enjoy a good year, returning 7.0% in the second quarter. Returns for the quarter, year-to-date, and since inception periods comfortably exceed all relevant benchmarks.

Since the quarter’s end, markets have re-discovered the concept of risk, with indexes declining high single digit percentages before staging a partial recovery. Turns out, the economy is complex and a rapid return to pre-pandemic conditions is not guaranteed. The COVID-19 Delta variant may or may not slow the re-opening process, and high and persistent inflation is either a looming menace or just a blip, depending on whom one asks. I don’t lose sleep over it. Anyone who does lay awake, heart racing, dreading any particular scenario, has invested aggressively and without understanding what he or she actually owns. My goal with Alluvial Fund is to generate the highest possible returns for partners—of which I am one!—but this pursuit cannot come at the expense of proper risk controls.

The simplest path to easy returns over the last several years has been to purchase the flashiest, most speculative, least profitable companies and ride investor euphoria “to the moon.” One shining example is AppHarvest, which produces tomatoes in high-tech greenhouses in Kentucky. The enterprise value of the company is $1 billion. That’s $16.7 million for each acre of tomatoes the company expects to harvest in 2021. Maybe these new greenhouses really are more productive and efficient, but I doubt they are worth literally 3,800x the price of Kentucky cropland. Additionally, the farmers working this cropland make money on average; for its part, AppHarvest expects to experience cash burn of $733,000 per each of these extraordinary acres before growth investment this year. AppHarvest is far from the only company for which investors have willingly suspended all logic and critical thought. I admit to feeling frustrated at times as investors relentlessly bid up the prices of these hugely speculative companies while ignoring our less “hypeable” holdings. Then again, I like knowing the values of our holdings are backed by solid cash flows and assets. Hopes and dreams alone are a poor foundation for stock valuations. And when companies like AppHarvest fall just a little short of their holders’ wildest fantasies, look out below. AppHarvest shares are down >70% since February as investors realize that for $1 billion, it might be better to buy 227,000 acres of Kentucky cropland than 60 acres of tomatoes.

A New Idea and Portfolio Review

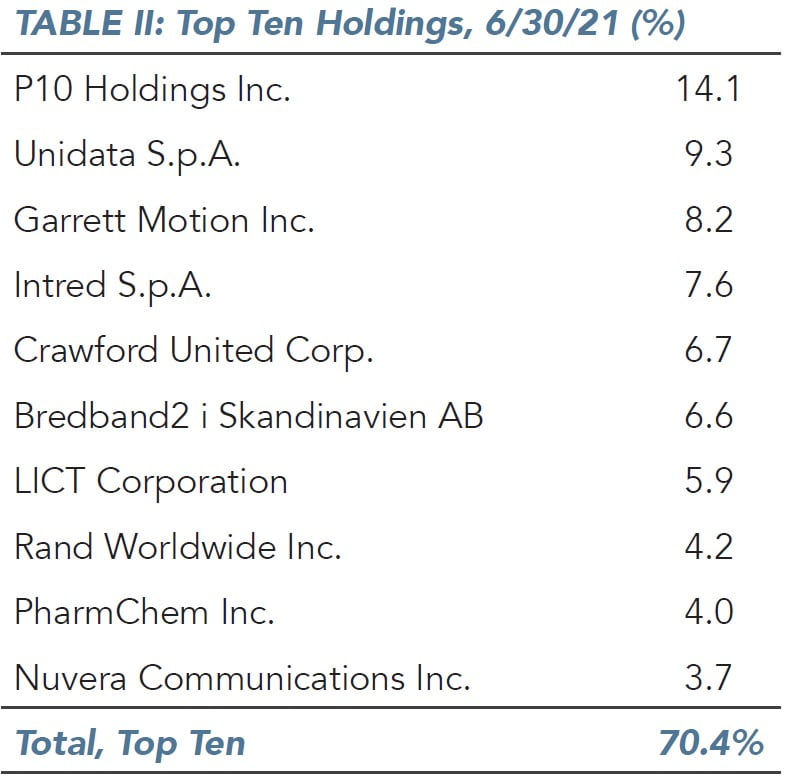

Garrett Motion

We owe a large portion of this quarter’s gains to a new investment in Garrett Motion Inc. We participated in the company’s post-bankruptcy recapitalization through our purchase of Garrett Motion preferred shares.

Garrett Motion is a manufacturer of automotive turbochargers that was spun off from Honeywell in 2018. Honeywell gave Garrett Motion a parting gift of hundreds of millions in asbestos-related liabilities, which ultimately proved unmanageable and led to the company’s bankruptcy in late 2020. The resolution of the bankruptcy process allowed Garrett to shed many of its liabilities and to recapitalize the company with new debt and preferred stock. Shareholders were granted the right to subscribe for new Series A convertible preferred stock.

The rights offering bore all the classic signs of an attractive “special situation” investment. I believed the offering price of the preferred shares, $5.25, was significantly below their market value based on any reasonable estimate of Garrett Motion’s post-emergence performance. What really got me excited about these preferreds was the behavior of the large hedge funds backstopping the rights offering. These funds had the right to acquire all the preferred shares not purchased by holders of Garrett Motion common stock, and the subscription process was designed to be quite difficult for smaller, less sophisticated shareholders. Vague, confusing paperwork; attorney attestations; proof of financial status—clearly, these backstopping funds didn’t want anyone else to get their hands on these preferreds. And if these large, sophisticated funds with their deep involvement in the bankruptcy proceedings thought these preferreds were so great, well…that was not enough for me to say “I’m all in!”, but it did suggest taking a much closer look.

We subscribed for a healthy number of Garrett Motion preferreds, and our investment has been a good one to date. The preferreds trade nearly 50% over our subscription price. Nice to see, but I think the best is yet to come. Following the bankruptcy, Garrett Motion is a small company with a confusing capital structure (term debt, Series A preferreds, Series B preferreds, common stock), no analyst coverage, and no guidance from management. On top of that, Garrett’s business model faces long-term challenges as the internal combustion engine gives way to electric. It’s no wonder the market values Garrett at distressed levels. But Garrett will generate hundreds upon hundreds of millions in free cash flow each year for the next several years, which will allow the company to deleverage and simplify its balance sheet, invest in next-generation products, and reward shareholders. I fully expect the preferreds we hold to be valued at 2-3x the current price in just a few years’ time.

LICT Corporation

On the telecom front, it was a quiet quarter. Shares of our various telecom-related companies have performed well, and I have reduced our holdings somewhat as the discount to fair value has narrowed. LICT Corporation continues to buy back shares and will soon announce the results of its strategic review. The company is evaluating various alternatives to increase shareholder value, including a potential SPAC, spin-off, or dividend recapitalization. Any of these would boost the value of LICT shares, though I would prefer the spin-off or dividend.

Nuvera Communications

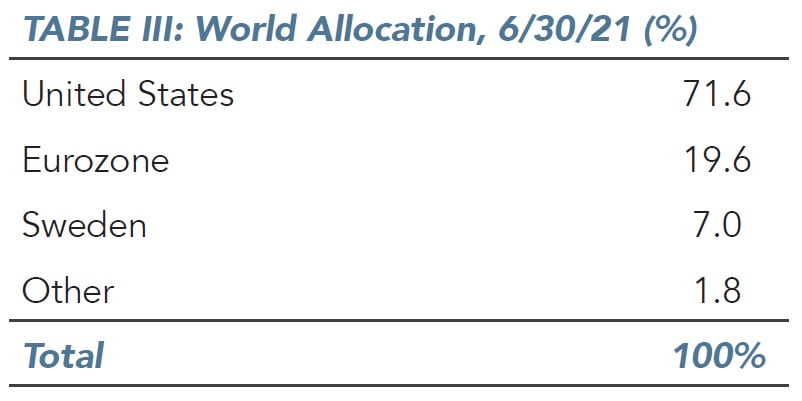

The ever-cautious Nuvera Communications hiked its dividend by 7.7%. The company’s cash balance is unusually high, and trading volume is unusually high as well. Could somebody be anticipating a move by the company, or some serious federal cash heading Nuvera’s way? Our trio of European fiber and broadband providers, Intred, Unidata, and Bredband2 i Skandinavien, benefited from continued customer additions and good operating leverage, resulting in excellent cash flow.

P10 Holdings

P10 Holdings remains our largest position, though I reduced our holdings this quarter to manage our exposure and to build cash for other opportunities. It has been a quiet year for P10 compared to the fireworks of 2020, but the company continues working to build a diversified alternative investments manager. I was pleased to attend the company’s shareholder meeting in Dallas in June. P10 is focused on completing additional acquisitions, though it will be extremely selective. Up-listing to a major exchange remains a priority, though the company will not allow the process to distract from the acquisition hunt, as acquisitions will provide shareholders with much more value in the long run. The company projects fee-paying assets under management of $16 billion by year-end, which should provide around 45 cents per share in free cash flow. Shares remain very attractively priced and will move on any acquisition or up-listing announcement.

A Texas Windfall and Other Thoughts on Excess Cash

We took advantage of another fast-moving opportunity this quarter in Crossroads Systems. Given the fund’s large investment in P10 Holdings, I am obviously a fan of Robert Alpert and Clark Webb at 210 Capital. Crossroads Systems is another 210-controlled entity. Prior to this year, Crossroads’ sole line of business was an alternative housing lending business in Texas. Solid, profitable, and growing, but perhaps not the most exciting. But with the expansion of the Paycheck Protection Program, Crossroads saw a major opportunity to earn fee revenue by partnering with a financial technology firm to provide PPP loans to small business operators and sole proprietors. When the dust settled, Crossroads Systems subsidiary Capital First Financial had provided billions through >470,000 individual loans and received an astonishing windfall from the associated fees. In the space of a few months, Crossroads used up its net operating losses completely and earned more than $50 per share, net of tax. The company will likely earn another ~$3 per share from net interest income before these loans are forgiven.

We were able to acquire shares of Crossroads Systems at prices ranging from $40 to $50, prices which I believed provided an acceptable discount to fair value and a high likelihood of an attractive return once the company revealed its bumper profits to the market. Last month, the company reported results for the quarter ended April 30, which included net loan fees for 200,000 of the total PPP loans. Some investors were disappointed by the margins Crossroads earned after processing costs and the fee split with the fintech loan originator, but the report confirmed the windfall profit. While the magnitude of the company’s one-time earnings bonanza was now known to investors, an important question remained. What would the company choose to do with all the excess cash? After all, the PPP program was over and done, and existing operations could not absorb this much incremental capital.

Last week, Crossroads Systems announced it would pay out most of its earnings as a $40 per share special dividend, retaining $20 per share in liquidity to support the growth of existing operations. The market reacted positively, sending shares to $60. Whether or not Crossroads Systems has a continuing place in our portfolio depends on where shares settle following the dividend payout, and on the strategy the company pursues going forward. I have a lot of confidence in the company’s team. Members of the 210 Capital complex continually find creative ways to make money. If Crossroads Systems trades at or below pro forma book value following the dividend payout, the risk/reward tradeoff may be too good to pass up.

A pet peeve of mine is small companies that hold onto cash far, far beyond their conceivable needs. Sure, businesses should keep adequate cash to fund operations through ups and downs, and a “rainy day” cash stash is never a bad idea. But when companies hoard cash sufficient to cover years upon years of losses in the most adverse scenarios, shareholders are being deprived. It usually comes down to incentives. If management does not own a meaningful percentage of the company, what does it benefit them to return excess cash to shareholders? Sure, the principalagent issues at hand can be ameliorated with well-designed compensation structures, but most small companies have nothing like that. So more and more, I avoid small companies with large non-operating cash holdings in the absence of a specific strategic rationale. I simply don’t trust management to use the cash well or return it in a timely fashion.

I never have to worry about idle cash with Peter Kamin-controlled companies Rand Worldwide and Calloway’s Nursery. Each has been generous this year. Calloway’s Nursery is earning record profits as Texans spruce up their homes and gardens with flowers and greenery. The company has paid out $1.25 per share in special dividends year-to-date and will likely pay at least $0.50 more, while funding its growth initiatives. Rand Worldwide is riding high on continued demand for its software solutions and a recent re-financing and has paid out $1.75 per share this year.

Smaller Holding Spotlight and Closing Thoughts

In my last letter I profiled Logan Clay Products. This time around, allow me to discuss another thinly-traded jewel, Tower Properties Company. Tower is a real estate company that owns over 3.5 million square feet of commercial space and multi-family dwellings in the Kansas City metro area. The company is run by savvy real estate operators. They maintain their properties well, finance them appropriately, and generally are content to enjoy the rewards of long-term growth in rents and real estate values. At the last trade of $19,500 per share, the market values Tower Properties at a capitalization rate of over 9%, corporate overhead included. If Tower Properties were to sell its portfolio today, I estimate it would collect at least $45,000 per share, pre-tax and net of debt. I doubt Tower will sell, but that’s all right. Management has substantial skin in the game, and they prove it by investing in property improvements and new properties when they see opportunities and paying special dividends when they do not. Tower paid a whopping $5,000 per share in late 2020. Though Tower Properties will probably not ever be our top performer, I am very happy to hold the company for the long term given its growing asset value, quality management, and discount to net asset value.

Once again, thank you for reading and thank you for the privilege of managing capital for you. I hope that you and your families are happy and healthy. We have enjoyed a good year thus far and I will do everything I can to identify the next set of opportunities. I will again be adding personal capital to the fund for August 1. You could say I am excited about this earnings season and beyond! Be on the look-out for details on our biannual webinar. As always, I am available to discuss the portfolio. I look forward to hearing from you.

Best Regards,

Dave Waters, CFA

Alluvial Capital Management, LLC