Thus far, the year 2020 has been defined by “healthcare” and “digital”. The coronavirus pandemic has sent shockwaves through healthcare systems across the world. Public and private health systems quickly risked paralysis from the outbreak and were forced to confront the limitations and costs of their processes. This – and the need for social distancing – caused an accelerated shift to digital, speeding up the implementation of digital alternative processes such as apps, telehealth and web-based resources. In some cases, this shift was rapid – as with the UK NHS’s switch to remote physician consultations. In others, it was extended and troublesome – as with the implementation of the UK’s track-and-trace app, for instance.

Q2 2020 hedge fund letters, conferences and more

Overall, the shift to remote working and the stay-at-home imperative have pushed telemedicine to the forefront. A McKinsey survey conducted among 213 European physicians suggests that 55 to 58 percent of them believe that telemedicine will play a significantly greater role in the future.

In a similar vein, many pharmacy and prescription medication services now need to work online, too, as individuals continue to avoid pharmacies and medical practices for fear of the virus, subsequently enjoying new levels of convenience. We therefore expect to see more activity akin to Amazon’s 2018 acquisition of PillPack in a crossover between the digital commerce and healthtech spheres.

Furthermore, health IT services and BPO will grow more as healthcare providers will accelerate digitisation and reach the limits of in-house implementation and have no other choice but to outsource to specialised third-party firms. These are likely to reap the benefits of the crisis.

Meanwhile, the most prolific acquirers such as Philips, TabulaRasa or Varian are, so far, laying low this year, but we expect them to come back strong in 2H2020 and beyond once healthtech priorities become clearer and the global economy adjusts to a new set of realities.

M&A Summary

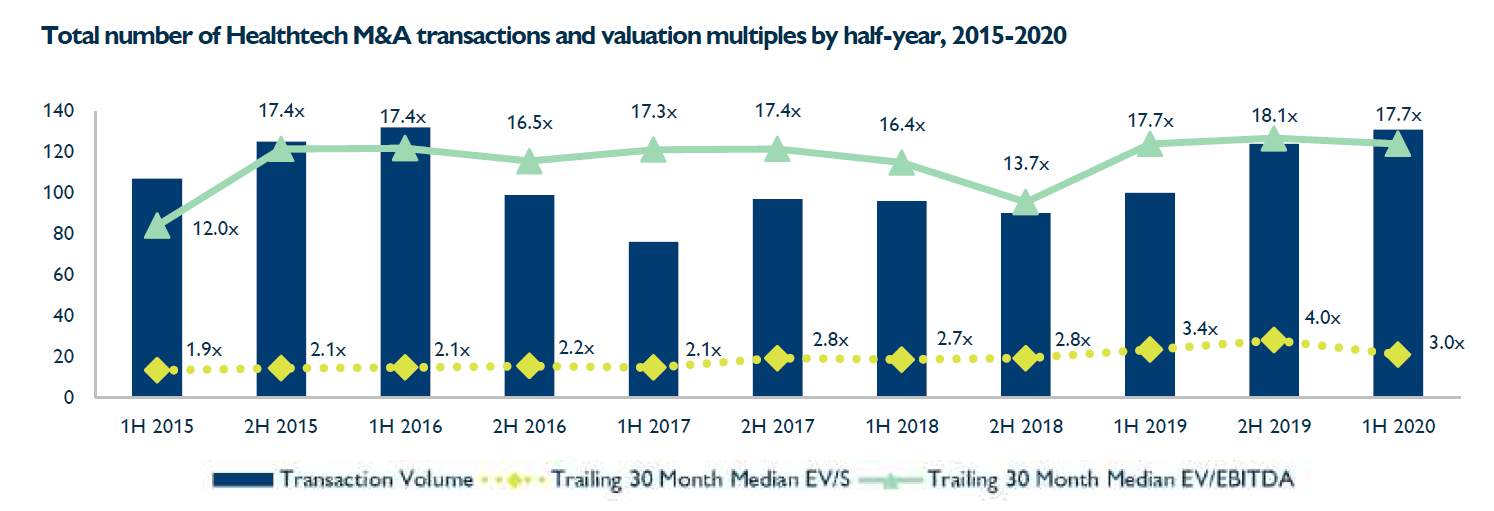

Valuations retain momentum Valuations in the healthtech space have been high for the best part of the last five years. In the first half of 2020, the trailing 30-month median EV/S multiple dipped slightly to 3x following a 4x peak in 2H2019. Despite previous volatility, EBITDA multiples are still very high, coming in at 17.7x in 1H2020. This growth has been driven particularly by high valuations in the Healthcare Vertical Software segment – the largest subsector covered in this report.

Transaction volume continues to increase Transaction volume is on the rise, with 131 transactions recorded in 1H2020. This upward trend since a significant dip in 2H2016 and 1H2017 has taken us back to the peak levels observed five years ago. Meanwhile, 60 per cent of deals took place in Q1 and 40 per cent in Q2 – a split which alludes to the cautiousness of buyers after the markets crashed in March 2020 (though they have since made a healthy recovery).

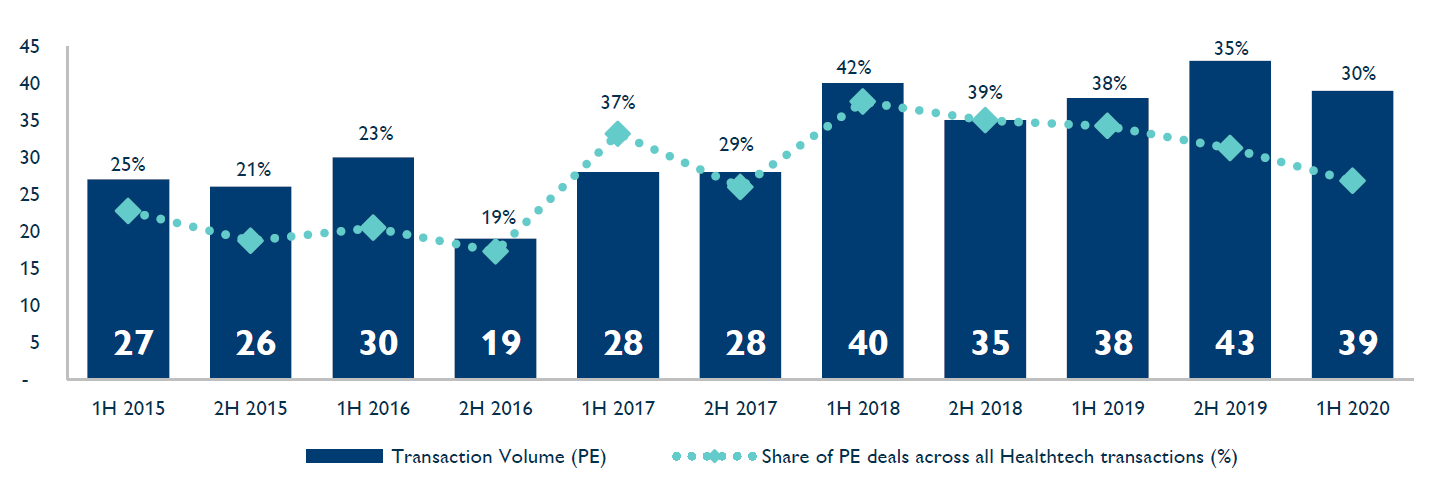

Private equity remains prominent buyer group Private equity firms became increasingly active in the healthtech space in the run-up to 2018; however, the market share of financial buyers has since decreased slightly. That said, financial buyers still constitute a substantial part of the buyer universe. Interest rates are not expected to rise soon, and access to cheap debt will continue to fuel these financial buyers’ acquisition activity.

Top Acquirers – PAST 30 MONTHS

Although it featured at the top of the acquisition table between 2017 and 2019, Philips has now been overtaken by other healthcare giants such as TabulaRasa or Mediware – despite the fact that neither of these companies made any purchases in 2020 either.

CGM made two acquisitions just before the coronavirus outbreak, picking up the German and Spanish assets of Cerner, and Italian telemedicine software provider H&S Qualità nel Software.

In addition, Elekta AB, a Swedish company that provides radiation therapy, radiosurgery and clinical management for cancer and brain disorder treatment, acquired Finnish firm Kaiku Health in February. Kaiku’s patient monitoring software and mobile application has modules for more than 25 types of cancer and is in use in over 40 European cancer clinics and hospitals

Trends, largest deals & subsector breakdown

- Regional deal-making sees European targets acquired by more local acquirers

- First signs of deals influenced by Covid-19, e.g. deals targeting respiratory disease detection software

- Telemedicine services continue to thrive as Covid-19 pushes everything online and people steer clear of in-person consultations

- Private equity and financial buyers continue to invest and acquire, accounting for almost a third of all transactions in the sector in the first half of 2020

- Health IT services and BPO thriving as healthcare providers reach the limits of their capabilities and look to third-party firms for assistance

- Pharmacy and prescription services firmly online in a new age driven by Amazon’s acquisition of PillPack in 2018

Geographical breakdown

Over the past 30 months, 63 per cent of European targets were bought by acquirers that were also European. This figure is a little lower for Q1 2020, before the coronavirus outbreak.

However, this number has jumped to 100 per cent if we look only at deals closed in Q2 2020, pointing to more regional dealmaking for 2020. This is likely to be due to travel restrictions and local lockdown measures strongly impacting the prospects for intercontinental M&A.

Meanwhile, across global M&A activity, North American targets have maintained their majority share of deals, accounting for 84 per cent of all deals in Q1 2020 and 76 per cent in Q2 2020.

Healthcare Vertical Software

Sub-sector overview

Already the largest subsector within the healthcare space, in 1H2020 the Healthcare Vertical Software segment saw the most transaction volume on record with 88 deals – a 20 per cent increase on the last reporting period. In fact, transaction volume has grown consistently since 2017.

On the valuation side, so far 2019 has not been beaten. In 1H2020, the trailing 30-month median revenue multiple came in at 3.6x, while the EBITDA multiple reached a high 17.3x.

It is also worth noting that, while previous EBITDA multiples on the below graph were very high, they included a handful of exceptional deals which closed at high EBITDA multiples (>50x). Thus, it is safe to say that the current median is more representative of valuation trends in the Healthcare Vertical Software segment.

Respiratory illness stays front of mind

Given the concern over respiratory illnesses as a result of Covid-19, this deal came as no surprise. AireHealth, an American provider of respiratory care management through a mobile app, acquired BreathResearch, a respiratory healthcare firm that detects fluctuations in respiratory health. Its VitalBreath virtual care software helps patients, caregivers and clinicians to be more informed in respiratory care, enabling faster response to exacerbations and translating to fewer emergencies and fewer hospitalisations.

Through the deal, AireHealth adds to its capabilities all of BreathResearch’s assets including employees, intellectual property, research and published works. AireHealth also gains all patents related to respiratory drug delivery, medication adherence and analysis of breathing sounds using machine learning and artificial intelligence.

Invitae targets pharmacogenetics

In March, Invitae, the publicly-listed medical genetics company, purchased YouScript, a clinical decision support and analytics platform, for $79 million; and Genelex, a pharmacogenetic testing company, for $20 million.

According to the acquirer, despite its broad utility, the incorporation of pharmacogenetic information into routine medical care has been slow. Combining Genelex testing with clinical decision support using YouScript software allows clinicians to easily navigate this information when making prescription choices at the point of care.

YouScript’s software pairs a patient’s pharmacogenetic profile with published drug and gene interaction information to assess the risk for adverse drug events and possible side effects. Health systems can also use YouScript at population scale to identify patient populations at highest risk for adverse events.

Genelex offers pharmacogenetic testing that analyses the genes that are important for understanding variation in how people metabolise and respond differently to prescription medications. The testing process includes pharmacist review, patient- and clinician-facing reports, as well as access to clinical decision support for the treating provider.

The use of YouScript in combination with Genelex has been shown to reduce adverse events, costs and hospital readmissions.

Health IT Services & BPO

Sub-sector overview

After a strong rebound in 2H2019, transaction volume in this segment declined again in 1H2020, with 15 deals recorded. However, the trailing 30-month revenue multiple remained stable, coming in at 2.4x. There were not enough disclosed EBITDA multiples to warrant a reliable trailing 30-month median EBITDA multiple.

Almost all the transactions in this segment were carried out between a north American buyer and north American seller.

Segment sees largest deal

The Health IT Services & BPO segment saw the largest deal in 1H2020. In March, private equity firm Veritas spent $5 billion on the health and human services business of DXC Technology, i.e. the assets which provide health software consulting and integration for Medicaid hospitals and healthcare providers in the US. For instance, DXC HHS enables users to manage patient health records, monitor quality of care in real-time, and manage bookings and admissions, laboratory information, electronic medication, pharmacy and mortuary processes. DXC said it would use the proceeds from this sale of the Medicaid services business to pay down debt.

This is not the first time Veritas Capital and DXC h. ave worked together. In 2018, components of Veritas’ business, Vencore and KeyPoint, along with DXC’s federal business, were folded together to create the DXC spinoff Perspecta.

Cerner divests underperforming RCM unit EHR giant Cerner shed its German and Spanish assets to CGM in February and followed with the sale of its underperforming RevWorks business to R1 RCM in June for $30 million. With the deal, Chicago-based R1 gains access to RevWorks’ commercial, non-federal client relationship. Cerner will also extend R1’s EHRagnostic revenue cycle capabilities to its clients and new prospects.

According to Healthcare Dive, the multi-billion-dollar revenue cycle management (RCM) sector has few players but is expected to grow as hospitals struggling with suboptimal collections rates and weakening margins look to outsource back-end functions.

Acquirer R1 has remained largely unaffected by the pandemic, reporting a revenue spike of more than 16 per cent year over year in the first quarter. The 17-year-old RCM player has embarked on a campaign of inorganic growth this year to solidify its position in the unsaturated market, also snapping up patient engagement player SCI Solutions in April.

EHR & Information Services

Sub-sector overview

Several successive reporting periods since 2016 were characterised by volatility and an overall decline in transaction volume. However, off the back of renewed momentum in 2018, deal volume climbed back to higher levels in 1H2020.

EV/S multiples have seen some volatility over the years but remain resilient overall, as the trailing 30-month median remains just below 3x.

Harris invests in EHR

In February, software giant Harris acquired Doc-Tor.com. An American firm based in New Jersey, Doc-Tor.com provides easy-to-use, cloud-based practice management systems for physician offices, allowing for efficient workflow and scheduling through collections and analytics. The Doc-Tor.com transaction also included the acquisition by Harris of New Ultimate Billing LLC, a full-service revenue cycle management (RCM) provider with 20 years of combined administrative leadership and medical billing experience. Doc-Tor.com will operate within Harris’s Amazing Charts business unit, and Ultimate Billing will be a stand-alone business unit within the Harris healthcare suite of solutions.

UKsees rare deal in the space

In May, public company Induction Healthcare Group acquired Zesty for $15 million. Zesty provides patient medical records management SaaS in the UK, allowing patients to consult their clinical record, manage appointments, read correspondence, provide feedback and attend remote consultations. Through the acquisition of Zesty, the Induction Group will be able to coalesce platforms that integrate patients, .clinicians and healthcare information sources across multiple sites and EPRs. By pooling their resources, the new group hope to develop their products faster and improve their growth opportunities.

Online Health Services

Sub-sector overview

In 1H2020, transaction volume in this segment has returned to healthier levels. Revenue multiples have also remained stable, as the trailing median 30-month EV/S multiple came in at 3.8x – lower than 2017 or 2018 but higher than the multiples seen five years ago.

Emergency response software garners interest In March, Central Research Inc (CRI), a provider of customised management and financial service solutions for the public and private sectors, acquired Global Emergency Response (GER) for an undisclosed amount. Founded in 2004 and headquartered in Georgia, GER provides web- and mobile-based software for emergency status tracking and situational awareness information, for healthcare, emergency response and governmental organisations in the US. The software includes features for patient tracking, incident coordination, resource tracking and .family reunification. The

events of 2020 such as the coronavirus pandemic or the Californian wildfires have no doubt reiterated the need for adequate digital solutions in case of emergencies.

Edtech and healthcare collide in 2020 In May, private equity firm LLR Partners acquired TrueLearn, a subscription-based online medical exam preparation service, for an undisclosed amount. TrueLearn was previously owned by Kian Capital.

According to PE Wire, e-learning solutions such as those offered by TrueLearn are in high demand as institutions adjust to asynchronous and remote classroom environments. In recent months, TrueLearn has expanded its offerings beyond physician education to adjacent healthcare markets including pharmacy and allied health. This shift has helped meet rising needs of .medical schools, residency programs and allied healthcare programs, which seek to train learners in remote settings, while continuing to address the problem of healthcare workforce shortages.

Conclusion & Contacts

In the six months since the publication of Hampleton Partners’ last healthtech report, the pressure on health systems has reached unprecedented levels as the Covid-19 pandemic has extended its grip globally.

Forced to ration services and cancel treatments, and with a vaccine still some way off, healthcare providers are having to turn to new technologies if they have any hope of maintaining, let alone enhancing, future healthcare services for patients adjusting to digitally-enabled new lifestyles in a changed global economy. This has continued to drive both M&A volumes and values across healthtech. Already the largest subsector within the healthcare space, in 1H2020 the Healthcare Vertical Software segment saw the most transaction volume on record with 88 deals – a 20 per cent increase on the last reporting period and a continuous trend since 2017.

Covid-19 has also currently changed the nature of deal making in the sector. Travel restrictions and local lockdown measures have strongly impacted intercontinental M&A with Health Services and BPO transactions, so far, in 2020 becoming exclusively intra-North American and European healthtech targets becoming solely the preserve of European acquirers.

Jonathan Simnett

Director

Jo Goodson

Managing Partner

About Hampleton Partners

Hampleton Partners is at the forefront of international mergers and acquisitions advisory for companies with technology at their core.

Hampleton’s experienced deal makers have built, bought and sold over 100 fast-growing tech businesses and provide hands-on expertise and unrivalled international advice to tech entrepreneurs and the companies who are looking to accelerate growth and maximise value.

With offices in London, Frankfurt, Stockholm and San Francisco, Hampleton offers a global perspective with sector expertise in: Automotive Tech, IoT, AI, Fintech, Insurtech, Cybersecurity, VR/AR, Healthtech, Digital Marketing, Enterprise Software, IT Services, SaaS & Cloud and E-Commerce.

See the full report here.