Gold has been bouncing around, struggling to stay above $1,700 an ounce, and some may question whether it’s an effective hedge during this time of coronavirus-driven uncertainty. The World Gold Council looked at gold as a hedge and compared it to other common portfolio hedges during the current downturn.

Gold is the most optimal hedge

Some tail risk hedge funds posted quadruple-digit returns during the March downturn, but many tail risk strategies are technically complex and can be expensive to hold for a long period of time. Historically, gold hasn’t been a very strong hedge during tail risk events because prices don’t rise as quickly, according to the World Gold Council. However, gold has maintained its safe haven status by improving risk-adjusted returns and adding liquidity during the COVID-19 crisis.

To compare gold’s effectiveness as a hedge, the organization compared it to other well-known hedges, including volatility, credit hedges and real assets like other precious metals. The council adjusted the amount of each hedge in various portfolios based on their risk exposure.

The organization’s analysis indicates that any hedge is better than a diversified hypothetical portfolio with no hedge. Further, while each of the hedges have merit in certain market conditions, the analysis suggests that gold is the best hedge in the long run when considering various attributes.

Hedging tail events

Gold’s status as a safe-haven investment during risk-off scenarios is well-known, especially system events affecting multiple regions and industries. When stock markets plunge suddenly, correlation in risk assets can sometimes increase.

As a result, portfolios that were once diversified could see unexpected drawdowns, forcing margin calls and low funding ratios.

Many investors sell gold and other liquid assets during such events, which also happened during the coronavirus selloff. Correlation for gold and most major asset classes increased during the recent selloff, although gold’s correlation to the stock market was still flat to slightly negative.

As systemic events like the COVID-19 crisis unfold, gold prices tend to outperform, they added. Historically, the more the stock market has pulled back, the more negatively correlated gold prices become with the rest of the market, which is why it works as an effective hedge during such events.

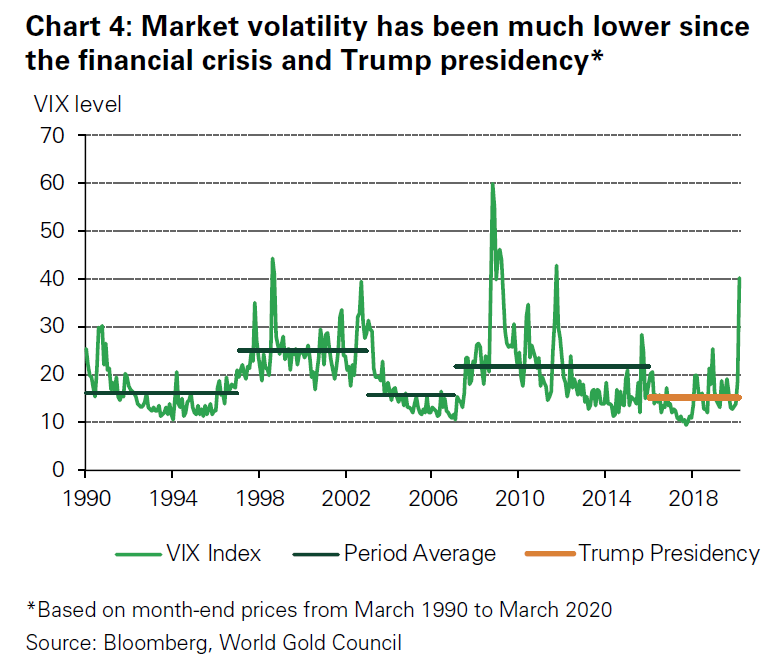

Volatility hedges are expensive but can work well

The World Gold Council notes that while it’s important to analyze tail hedges like the recent coronavirus selloff, systemic events don’t always remain contained within a small window. For example, some crashes occur in short spurts and hardly register in weekly returns. Others drag out like the 2008 financial crisis, lasting months with frequent selloffs. Thus, a tail risk hedge may need to perform beyond the window that initially defined the event.

The organization explained that VIX futures and other volatility-related hedges have historically mean reverted. That means that if the selloff is only an isolated event, then the hedge’s value will likely come crashing down toward the average very quickly after the selloff.

Thus, volatility-related hedges like VIX futures with portfolio insurance like put options can work well during tail risk events, but only with the proper timing. In fact, during the coronavirus selloff in March, the VIX was trading at or close to record highs. However, when VIX futures are implemented systematically, they tend to erode portfolio performance over time. VIX short-term futures can erode performance by almost 2% per year. This has been more significant over the last four years.

The organization adds that all of the hedges in their analysis except short-term VIX futures improved risk-adjusted returns compared to a portfolio with no hedges over the last 20 years. Interestingly, VIX futures significantly reduced portfolio drawdown, but they were very expensive.

Credit hedges have been the best since 2008

The World Gold Council said liquid indices on credit default swaps offer an easier way to be bearish on corporate bonds than actually shorting the bonds. Such holdings can hurt cumulative returns in the long term due to the high premiums, but many of the most recent tail events were credit related. As a result, such positions have positively contributed to portfolio performance since the 2008 financial crisis.

The organization found that fixed income hedges behaved more like risk assets during tail risk events. They said although Treasuries initially move higher when a crisis is just beginning, Treasuries have been somewhat positively correlated to the S&P 500 over the last 20 and 30 years. Treasuries only provide diversification during non-tail events.

Gold and other precious metals as an effective hedge

They also note that most investors want diversification only when markets are selling off. Most risk assets do provide diversification when prices are rising, but they become strongly correlated during a selloff. Further, hedges that diversify the portfolio on the way up can also erode performance while prices are rising.

They found that gold is one of a very few hedges that is positively correlated during risk-on periods. It becomes more and more negatively correlated with other assets during risk-off periods and has been for almost 50 years.