Sven Carlin digs into GrafTech International Ltd (NYSE:EAF), it is a very interesting stock to buy but there are also concerns which is normal.

GrafTech International Stock Analysis – Possible PE ratio of 1 stock! Pabrai is Buying!

Q3 2019 hedge fund letters, conferences and more

Transcript

Good day fellow investors. It's always good to copy/mimic great investors and in this video I want to show you my analysis of GrafTech a company that Mohnish Pabrai famous for looking at price to earnings ratios of 1 companies, recently bought with a nice stake in his portfolio. So in this video will analyse GrafTech International and we'll see the risks and the rewards perhaps try to find why Mohnish bought that and then see whether this fits your portfolio or not.

There is one reason that I say okay, I might watch it, but I'm looking for a little bit better low lower risk investments. Mohnish has a good theory there, he'll probably do well within his portfolio but always keep in mind that when you look at these hedge funds or investment managers, they always put it in a portfolio perspective they might be long this if this works out. They do five times their money if it doesn't they'll do on something else we usually don't see the something else so let's start and analyze GrafTech.

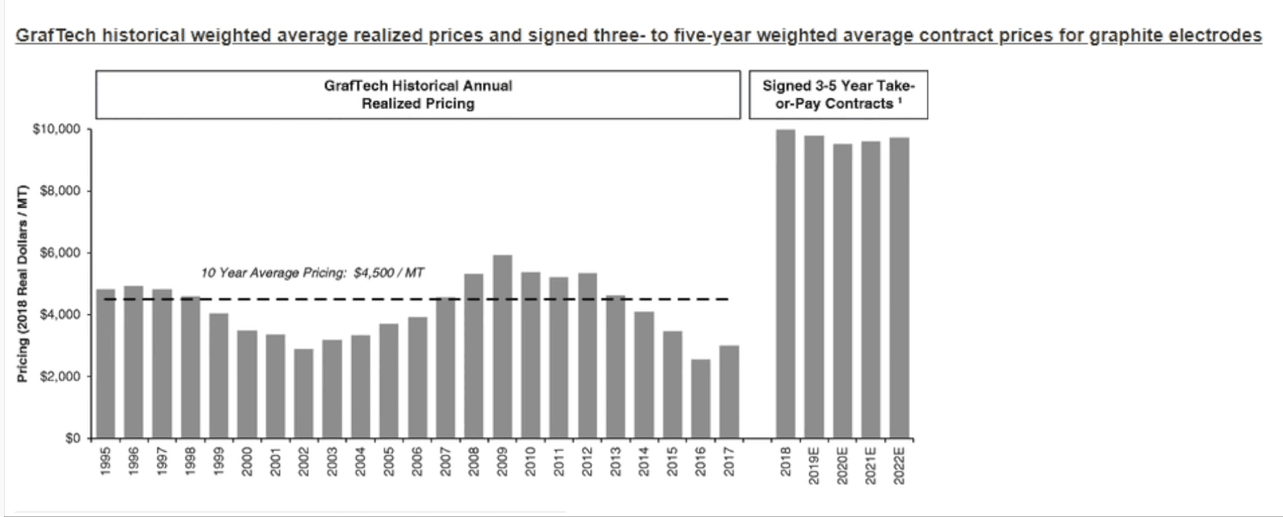

So, overview GrafTech International is a provider of high power graphite electrodes for the growing electric arc furnace steel market there is a blast furnace to make steel and electric arc. Electric arc needs graphite electrodes to produce very high temperatures to make that steel. The company is an integrated producer as it owns see drift coke which produces 75% of the needed petroleum needle coke to make graphite electrodes. Higher needle coke prices create instability in the sector, and therefore, it's good to be integrated.

Business model

The company practically went bust in 2015 when Brookfield acquired it for 1.2 billion. Graphite electrode prices were around 2600 per tonne in 2016. While those around are around 10,000 now. So what was the case in 2016 might happen again, and this is a big risk, because the market can change very quickly after all, this is a commodity.

So that's something to keep in mind. The management moved however very quickly and switch from mostly selling on spot to immediately making long term three to five year take or pay contracts to fix the high price and to create stability for on the company. So that's what Brookfield brings to you plus the cash to do things to improve production and everything

Now is GrafTech International's margin and a PE ratio of 1, really what do we have there? As they said they have the steak or pay agreements of high prices, which will lead to margins, good margins and good profits for the coming three years. Over the next three years they will have they have already contracted 4.5 billion in revenue and the high prices thus high margins you can expect that the cash flows per year will be around 750-800 million as those are now.

GrafTech International margin of safety

So, that is GrafTech's margin of safety. So, this is what Pabrai is practically buying his buying by being 3 billion now to buy 3 billion in free cash flows over the coming four years. Whatever graph that does, after year four will be free for Pabrai. However, if electrode prices go down, then there will be things will get very risky for GrafTech because, yes, they have good prices, good margins, good cash flows, but they also have a long term debt of 2 billion they intended to pay it down over the years. But you never know with igh debts and in such a volatile environment as graphite electrodes, anything can happen.

And hersuch he we come to Brookfield in their relation to GrafTech, they bought it financed it length, a lot of money to it, and now they want to get rid of it. When the stock price hit 19. They immediately sold the shares to GrafTech for a buyback. But that already tells you okay Brookfield wants to get rid of this.

So perhaps the upside is limited, perhaps the 20 the 1720. They'll say, Okay, get rid of it. So the upside is not five times on a price earnings ratio of one, the upside might be only 50-100%. So it's important to put things into perspective of the big owner, before selling before going public. They didn't have the money to issue a dividend. So they issued a loan in the form of a dividend to Brookfield and saying here is your dividend but we will pay you six months later when we get the money.