Dane Capital’s new idea Waitr, Dane sees 50%-100% upside to shares over the next 6-12 months.

First posted on HiddenValueStocks.com

Summary

- Waitr is a rapidly growing online restaurant delivery platform in 11 Southeastern States, trading substantially below peers, despite its faster growth. We see 50-100% upside over the next 12-18

- Waitr is going public through a merger with SPAC Landcadia Given the unconventional nature of SPACs, we believe many investors are unaware of this investment opportunity.

- Online restaurant ordering is still in its early stages in the US. GrubHub trades at 10.4x/8.1x 2018/19 EV/revenue vs. Waitr 7.4x/3.9x 2018/19 EV/revenue, despite over 2x GrubHub’s growth

- We expect continued industry consolidation. Acquisitions should put a floor on Waitr’s shares and could help generate a significantly higher multiple and stock

- Waitr’s position as a number 1 or 2 player in tier-2 and 3 cities (50,000-750,000 populations) insulates the company from competitors who are more focused on larger urban centers. Waitr has white-space to grow into several hundred cities over the next few

Q3 hedge fund letters, conference, scoops etc

Discussion

We believe Landcadia (LCA), which should complete its SPAC merger with Waitr during the 1st or 2nd week of November, represents a compelling, under the radar screen, opportunity for growth investors playing the offline to online restaurant delivery trend. We see 50%-100% upside to shares over the next 6-12 months. For those with a less bullish stance on the sector, valuations, or macro/broader economic concerns, we recommend a pair trade with far slower-growth (although high-growth), more highly valued, GrubHub (GRUB) which has both low short-interest and a low borrow-rate. Catalysts include: Closing of the SPAC merger in 1H November, 2018 guidance raise when company reports 3Q, sell-side coverage, and tender or warrant (LCAHW) exchange soon after transaction close.

The trend from offline to online has been relentless since the advent of the internet and mobile technology. We’ve seen it in shopping with Amazon and Alibaba, digital media with Facebook, Google, Netflix, and Spotify, Hospitality with Expedia, Priceline and Airbnb, and transportation with Lyft and Uber. Surprisingly, in the US, the trend towards online restaurant delivery is well behind these other industries, and relatively nascent at just 6% of off-premise restaurant revenue. Given its anticipated unabated high growth, market leader GrubHub has been awarded premium multiples, trading at 10.4x 2018 EV/revenue and 8.1x 2019 EV/revenue. Notably, GrubHub is concentrated in the Northeast, which comprises over 80% of the company’s sales. Given the attractiveness of the online restaurant market, large players including Uber (through the industry’s number 2 player, Uber Eats, and rumored to be looking to acquire Europe's Deliveroo), Amazon (which was also recently rumored to be in discussions to acquire Europe’s Deliveroo – valued in its most recent round at over $2bn) and Square which acquired Caviar in 2014, and more recently acquired OrderAhead and Entrees On-Trays, are all active in this segment. In addition, DoorDash and PostMates have also established themselves as serious players having raised $971.8mn and $578mn, respectively. We believe there is room for multiple winners.

In our view, Waitr, which is becoming a public company via merger with Landcadia, a SPAC sponsored by Tilman Fertitta, Chairman of Landry’s Inc. restaurants, and well connected across media (owner of the Houston Rockets, Station Casinos, etc.), and Richard Handler, CEO of Jefferies, has done an exceptional job growing, despite having raised just $26mn since inception. Waitr operates an online ordering and delivery platform that enables consumers to discover and order meals from local restaurants, powered by its team of delivery drivers. Waitr’s core expertise in second and third-tier cities has driven the explosive growth of the company since its founding in 2013. Even though Waitr has much higher projected growth rates of 125%+ and 90%+ respectively in 2018E and 2019E compared to industry median growth rates of 41% and 29% over the same period, Waitr only trades at 7.4x EV/ 2018 high-end of guided revenue, while the median of comps trade at ~9.7x EV/2018E revenue. Similarly, shares trade at just 3.9x EV/ 2019 high-end of guided revenue, versus comps at 7.2x and GrubHub at 8.1x. We note that comps, including Delivery Hero, Just Eat and Takeaway.com all compete in far more mature and saturated European markets. We also note that technology giants including Alibaba and Tencent have invested billions into money-losing Chinese on-line restaurant delivery companies such as Ele.me and recently public Meituan Dianping, which sports a ~$50 billion valuation, while Naspers and others have done the same in India in Swiggy. Softbank is the largest investor in Uber (parent of Uber Eats) and DoorDash, making the potential for foreign investment in the US online delivery business very real. We note that in China and India, deliveries are largely subsidized and money losing on a per transaction basis. Conversely, Waitr’s unit economics are compelling and increasingly efficient.

We believe Waitr has provided guidance that is conservative. When they reported 2Q, they raised full-year 2018 revenue guidance from $60-$65 million to $62-$67 million. We expect them to further increase guidance when they report in early November, and we estimate they ultimately report at least $70 million for 2018. If they merely achieve their 2018 and 2019 guidance, we think the stock has meaningful upside, however, if their results reflect our checks, revenues and stock appreciation could prove far better than outlined. We provide Dane Capital’s revenue estimates later in this report. While our estimates are above the guidance provided by management in its de-SPACing investor presentation, they are well below at least one set of management’s figures calculated in April and presented to Jefferies as part of its analysis in May (see below).

"Jefferies reviewed the provided estimated 2018 revenue multiple for Waitr of 5.2x for the Waitr Management Case and 6.0x-6.5x for the Street Case, each of which was lower than the median for the selected companies. Estimated 2019 revenue multiple for Waitr was 2.4x in the Waitr Management Case and 3.0-3.2x in the Street Case, each of which was lower than the median for the selected companies.

In addition, Jefferies applied a revenue multiple range of 7.0x to 10.0x to Waitr’s Management Case revenue forecast of $297 million and Waitr’s Street Case revenue forecast of $210 million for 2020 and applied a discount rate of 12.3% to derive an implied value per share of $20.60 to $36.24.

In addition, Jefferies reviewed certain key points relating to Waitr’s financial summary, including that Waitr estimates it will become profitable in the second half of 2019 and estimates EBITDA margins of approximately 12% by 2021. In addition, Jefferies included in this review an extrapolation to Waitr’s forecasted financial results for 2022, 2023, 2024 and 2025."

Source: LCA Proxy, P128, bold added

Our sanguine view regarding Waitr’s opportunity is based on several factors:

- Since the total restaurant industry only has 6% off-premise, there are still significant white-space opportunities. Several sell-side research reports estimate total domestic online takeout sales to grow at a 20.0% CAGR over the next ten

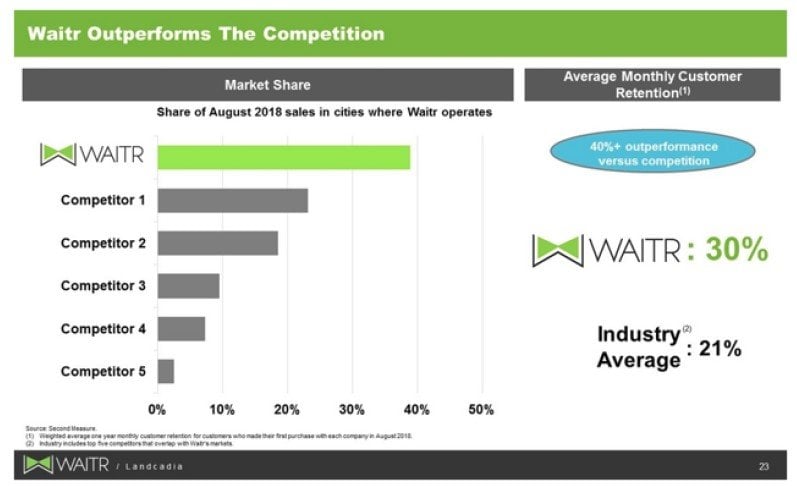

- By primarily focusing on under-served tier-two and three markets, Waitr is able to capture substantial market share of ~40%, with average monthly customer retention of 30% relative to industry average of 21% (per company's investor presentation)

- By employing a “hub-and-spoke” model for expansion into new cities, Waitr still has significant white-space growth opportunities of ~300 new markets in close proximity of their current footprint, despite significant growth in the last few years.

- Waitr has operated with a high growth business model built in a capital efficient manner relative to peers. Waitr has scaled rapidly, growing its Gross Food Sales by over 285% from 2016 to 2017 and net revenue by over 300%, all done with just $26mm in capital raised since founding (including a $10 million funding round led by future NFL Hall of Famer Drew Brees). With over $200mn of cash on its balance sheet post-merger with Landcadia (versus under $2mn as of June 30), we anticipate a meaningfully accelerated growth profile through increased marketing spend, greater resources to grow geographies at a faster rate, and tuck-in acquisitions of smaller players moving forward. In our conversations with management, we were given the impression that their 2019 and 2020 revenue forecasts presented in May were not predicated on a capital raise anywhere close to this size. Given the huge cash influx, we would not be surprised to see growth well ahead of guidance in 2019 and 2020.

- Recent consolidation in the online food delivery industry should prop up valuation. For example, GrubHub recently bought out on-campus food ordering platform Tapingo for $150mm, and com also acquired 10bis for €135 just this year. With Amazon and Uber rumored to express interest in buying out Deliveroo, we believe Waitr could potentially be a similar acquisition target given its unique position in tier two and three markets.

Business Overview

Waitr offers takeout and delivery services through both its Waitr App platform and the Waitr website. It differentiates its services through focusing on the three parts of the value chain:

- Waitr’s restaurants – Waitr has been successful in providing its restaurants with a new channel of profitable sales, which is demonstrated by Waitr’s inception-to-date restaurant retention rate of ~99%. Restaurants who have stayed with Waitr’s platform for four years have managed to obtain 4.0x more sales as compared to those who only had a year listing on Waitr.

- Waitr’s diners – Waitr provides the most restaurants relative to other online platforms in 32 of the 34 markets that Waitr currently serves (it actually now serves 45 markets, but 34 represents the last reported period for which data was provided). As a result, Waitr has strong consumer interest, with nearly half of its diners placing more than one order per month and with a 90% customer retention rate, measured on a quarterly

- Waitr’s delivery drivers – Waitr invests significant resources in its ~6,100 drivers, including background checks, in-person interviews, training, uniforms, peer reviews and scheduled working

Waitr primarily targets markets that fall within the top 51-500 markets in the U.S. based on population (50,000-750,000 people). These markets are often under-served and account for 35% of U.S. restaurants and 32% of the U.S. population according to the U.S. Bureau of Labor and Statistics and the U.S. Census Bureau.

In terms of pricing model, Waitr provides its restaurants with flexibility around price point, charging restaurants under two fee model: (1) with an initial setup and integration fee and partnership level pricing, and (2) with a higher fee rate and no upfront setup and integration fee. In charging an initial fee (typically $1,500), Waitr finds that it builds partnerships with its restaurants, ensuring buy-in and commitment to the platform from market launch.

More information on Waitr’s business can be found on its most recent investor presentation.

Contents:

- 3 Basic Questions

- Consolidation and Industry Investment

- Thesis / Key Base Case Drivers

- Management

- Valuation Analysis

- Risks

- Conclusion

1. Three Basic Questions

Before we dive into the analysis of this investment opportunity, there are 3 questions that we want to address. These are questions that inform our thinking when we look at any potential investment:

What is the reason for this mispricing (aka why should we be so lucky)?

What is our margin of safety (aka what protects us from a permanent loss of capital)?

What is the asymmetry of the opportunity (aka what are we playing for)?

What is the reason for this mispricing? First and foremost, we believe this opportunity exists because Waitr was only founded five years ago and is going public through a SPAC. As such, there is a limited institutional following and no research coverage (for now). SPACs lack the market price discovery of traditional IPOs, often creating stock prices disconnected from fundamentals, often generating compelling opportunities - recent example include BlueBird, Cision, Magnolia Oil & Gas, and WillScot. NRC Group (NRCG) and IEA (IEA) are two SPACs completed in 2018 that we purchased in 2018 still trading near their original $10 stock prices, which we believe offer 50%+ upside in coming quarters based on excellent, improving fundamentals, and valuations at dramatic discounts to peers, despite superior growth characteristics.

Secondly, the online food delivery space has been dominated by large players such as GrubHub, Uber Eats, PostMates, etc. in densely populated city areas, leaving few investors cognizant of this fast-growing regional company. moreover, because Waitr has decided to focus on lower tier markets, it is not popular or well-known on a national scale as some of the bigger players, and thus under-followed.

What is our margin of safety? Investors who are worried that Waitr’s rapid expansion might slow down in the future should be comforted by the fact that Waitr has not failed its expansion into new markets, given its effective hub-and-spoke expansion model. On the contrary, Waitr has been continuously improving on launches in new markets – it took Waitr 76 days to reach 1,000 cumulative orders when it launched in Lake Charles in late 2014, and only 8 days to reach the same number of orders in February 2018 when it launched in Columbus. We also see the active consolidation dynamics in this space to provide a floor on valuation – at present, Waitr already trades at much lower than comps, at 7.4x EV/2018E high-end guidance of revenue as compared to an industry median of 9.7x, and an even more dramatic discount based on 2019 multiples. We believe more conservative investors or those concerned about absolute valuation in the industry can consider a pair trade by longing Waitr and going short GrubHub. Given that GrubHub trades at ~$114 while Waitr currently trades at just over $114, we think longing 10 shares of Waitr while shorting 1 share of GrubHub (one can be more precise) sets up as a fairly easy trade. We believe this is a useful hedging tool given the large disparity in trading multiples between GrubHub, which trades at 10.4x/8.1x EV/2018E/2019E Revenue, and Waitr. On a EV/2019E Revenue basis, the discrepancy becomes even more stark, with GrubHub trading at 10.3x EV/2019E Revenue, while Waitr trades at 4.3x EV/2019E Revenue.

What is the asymmetry of the opportunity? The central bet we are making here is that the industry will grow into its valuation through the white-space opportunities from the shift from offline to online off-premise food delivery. Given a capital efficient business model coupled with an injection of additional cash, we view Waitr as the best and cheapest player to invest the space.

2. Consolidation and Industry Investment

As we stated out the outset, the inexorable shift from offline to online has been seen throughout numerous industries, and online restaurant delivery in the United States is relatively nascent. Clearly, picking the right companies is of huge importance and being early and right can drive a multi-bagger return Whether shopping with Amazon, digital media with Facebook, Netflix or Spotify, Hospitality with Expedia or Priceline, and transportation with Lyft and Uber.

We believe that in 5 years it's unlikely that Waitr will be a standalone company. Based on our conversations with management, we think they have significant room to grow their business, but long-term will act to maximize shareholder value. The recent reports of both Amazon and Uber pursuing Europe's Deliveroo, which carries a multi-billion-dollar price tag, suggests both are serious about expansion. For that matter, following Amazon's acquisition of Whole Foods, if they wanted to pursue domestic market leadership in online restaurant delivery they could make a play for GrubHub, which would be relatively bite size, even at a 50% premium (approximately $15 billion) given Amazon's market cap. Then again, Uber could do the same. At this point, its unclear how serious Square is about the opportunity, but with a $30bn+ market cap, it certainly has currency to make additional acquisitions in the space.

Interestingly, Uber's largest shareholder is Softbank which has a Donald Trump approved $72 billion plan to invest in US companies. Softbank also recently led the financing round for DoorDash. It would not seem much of a stretch for an Uber/Softbank effort to consolidate and lead the US restaurant delivery industry.

While perhaps less likely to pursue US opportunities due to current Administration policy, both Alibaba and Tencent have strong interest in the sector as well, and have meaningful historic investments in the US. Alibaba is the largest investor in Chinese restaurant delivery company Ele.me, has a large investment in Swiggy in India, and has significant investments in US companies Lyft and SnapChat (not to mention Jet, which was acquired by

Walmart). Tencent was the largest investor in recently IPOd money-losing Chinese delivery service Meituan Dianping, which sports a near $50bn valuation, in addition to its investment in money-losing restaurant deliver company Zomato in India. Tencent also has large investment in Tesla and Snap.

Our point in all this is that there is a ton of money in this space. The funds are being invested by giants, frequently in unprofitable companies based on promise. We believe Waitr has lots of white-space for growth in geographies that are of relatively limited interest to larger players versus major urban areas. We don't believe that will remain the case indefinitely. However, we think there are 3 things working in Waitr's favor. First, they have first mover advantage in many of the geographies that they are pursuing. Second, their newly cash-infused balance sheet will allow them to dramatically accelerate their growth from previous plans. Last, when competitors eventually are interested in Waitr's territories, we believe the buy versus build decision will be an easy one - it will be far less expensive, time-consuming, and distracting for these cash and currency rich companies to buy versus build.

We believe in several years, Waitr will be a very sought-after asset.

3. Thesis/Key Base Case Drivers

Large, under-penetrated and growing TAM creates meaningful LT opportunity

According to research by Raymond James, the total takeout food sales (both chain and independent) is expected to be $269bn in 2018E, increasing to $367bn by 2028E (a 3.2% CAGR). Within the takeout food space, total online takeout market is expected to by $18bn in 2018E (6.7% penetration) and this is expected to increase to $111bn by 2028E (30% penetration), amounting to a 20% CAGR. Moreover, online sales through 3P providers such as Waitr and GrubHub is expected to be $2.4bn in 2018E, (14.2% commission rate ex delivery fees) increasing to $12.2bn by 2028 (13.5% commission), growing at a 17.7% CAGR.

Source: Raymond James, Oct 5, 2018 GrubHub Research Report

Moreover, if we were to compare the penetration of home delivery options in the U.S. as compared to that of the U.K., there is still a huge potential in the U.S. for consumers focused on convenience to get food delivered. Based on research from Euromonitor, home delivery is was at 3.8% of total restaurant sales in 2016 in the U.S., as compared to 7.6% in the U.K., providing huge runway for growth in terms of the shift from offline to online food delivery.

In addition, according to research by U.S. Census, Euromonitor, L.E.K Research and NPD, food is an under-penetrated category online vs. other categories such as sporting goods or electronics, representing a huge runway for growth:

Source: U.S. Census, Euromonitor, L.E.K Research, NPD

First mover advantage in under-penetrated tier-2 and 3 cities offers strong existing growth opportunities

As mentioned, Waitr targets primarily markets ~51 to 500 in size (populations of 50,000-750,000).

Source: DEFA 14A, Slide 11

Because of its core expertise operating in a relatively unsaturated market, Waitr has significantly outperformed competitors both in terms of market share and retention rates.

Source: DEFA 14A, Slide 22

Source: DEFA 14A, Slide 23

By hosting more restaurants on its platform than any of its competitors, Waitr has been able to grow orders by 139% YoY in 2018 and allowed restaurants which have utilized its platform for four years to generate 4x more sales than those restaurants which used Waitr only for a year.

Moreover, with tier-2 and 3 cities growing at a much faster pace than tier-1 cities which are saturated, we see that Waitr’s market cohorts are continuously increasing since launch. While there isn’t exact statistics on the difference in growth across different tiers of cities, according to a research report by Jefferies on GrubHub, in 2016 tier-2 cities were generally growing at 2x the rate of tier-1 cities.

By employing a “hub-and-spoke” model for expansion into new cities, Waitr still has significant white-space growth opportunities of ~200 new markets in close proximity of their current footprint, despite significant growth in the last few years.

Waitr has been pursuing a “hub-and-spoke” strategy to expand into new cities, a model that is highly scalable and increasingly effective as Waitr continues to deploy it. For example, Waitr initially built a strong platform within Louisiana – with leading market share in terms of number of restaurants in its home markets of Lake Charles, New Orleans, Lafayette and Baton Rouge – and has since then expanded into new hub markets in nearby cities and states such as Columbus, Georgia and Montgomery, Alabama, among many others. Even with the rapid expansion, Waitr has identified 200 new markets in proximity that it has the ability to expand into given its current footprint. The replicability of this expansion model can be seen from the number of days to reach 1,000 cumulative orders decreasing from 76 in late 2014 to 8 in February 2018.

Source: DEFA 14A, Slide 1

Source: DEFA 14A, Slide 21

Waitr has operated with a high growth business model built in a capital efficient manner relative to peers. Waitr has scaled rapidly, growing its Gross Food Sales by over 285% from 2016 to 2017 and net revenue by over 300%, all done with just $26mn in capital raised at founding. With the new capital raised from the merger with Landcadia, we see an accelerated growth profile through tuck-in acquisitions of smaller players moving forward.

As compared to competitors such as Postmates and DoorDash that have raised extraordinary amounts of funding to grow, Waitr has managed its phenomenal growth with only $26mn of capital. Waitr has been able to achieve this growth primarily due to its high value proposition to customers – Waitr’s customer return on investment yields over 10x lifetime value (LTV) as compared to its customer acquisition cost, providing a huge runway for growth moving forward. With the new infusion of cash through capital from Landcadia and additional funds from Luxor Capital, we expect Waitr to grow more rapidly than management’s guided numbers, since the projected management case growth in 2018 and 2019 respectively reflects the growth that could have been achieved on the existing $26mn capital base. Interestingly, in speaking with Waitr management, they suggested they could be break-even today. However, with this additional funding they will be more aggressive, although still judicious. We are confident management won't spend recklessly and will have thoughtful growth, we believe this $200mn of new capital will provide rocket fuel to the company's growth trajectory. It will also provide funds for bolt-on acquisitions, which management has commented to us, will be accretive.

Recent consolidation in the online food delivery industry should prop up valuation.

Consolidation plays in the online food delivery industry include GrubHub recently buying out on-campus food ordering platform Tapingo for $150mm, and Takeaway.com acquiring 10bis for €135 just this year. As mentioned earlier assuming Waitr executes, it is a likely acquisition target in a few years. With Waitr’s unique and dominant presence in tier-2 and 3 cities, it seems to be an optimal target. This would naturally prop up the valuation even more significantly versus comparables' trading multiple, although we did not factor this into account for our upside calculations. It is worth noting that this consolidation dynamic works in Waitr’s favor as well – based on our meetings with management, they mentioned several live opportunities for accretive M&A and actionable tuck-in opportunities in the near-term (over the next couple of quarters), all of which we did not take into account in our calculations.

4. Management Discussion

The management team and Board of Directors comprise individuals with a strong track record of accretive acquisitions and excellent financial acumen. Tilman J. Fertitta, the CEO of Landry's, will remain on the board after the business combination, bringing significant amounts of restaurant and media experience to the table. We believe he will use his significant strategic industry relationships to further accelerate the company's growth, expand the company's geographic reach and take the company to new height.

Richard Handler, Chairman and CEO of Jefferies, is a co-sponsor of SPAC leading the business combination (although he will not serve on the Board of Waitr post combination). We suspect Jefferies will provide valuable banking and financing services to the company. In addition, we believe the various parties have strong relationships across Wall Street and expect the company to get a good deal of sell-side attention, often a challenge for companies with a SPAC heritage.

5. Valuation

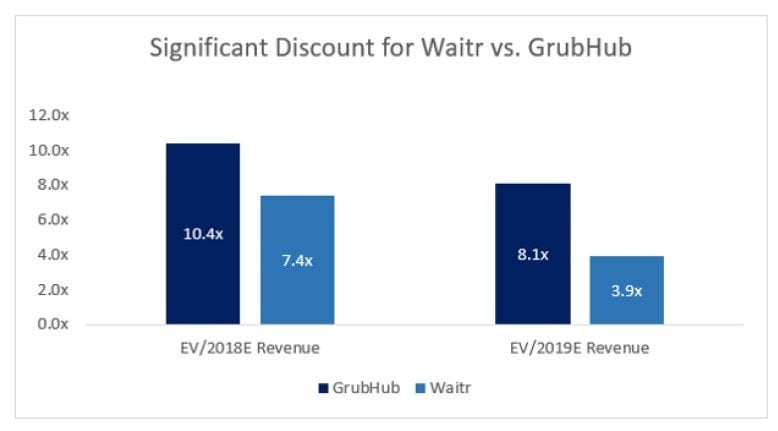

We believe the most relevant metric on which to value Waitr is on an EV/revenue basis. Based on an EV/2018E Revenue and EV/2019E Revenue, Waitr trades at deep discounts to peers at 8.1x and 3.9x, respectively (this is inclusive of the impact of warrants. This compares to comps which trade at a median of 9.7x and 7.2x EV/2018E revenue and EV/2019E revenue respectively.

Source: FactSet, LCA presentations, Dane Capital estimates

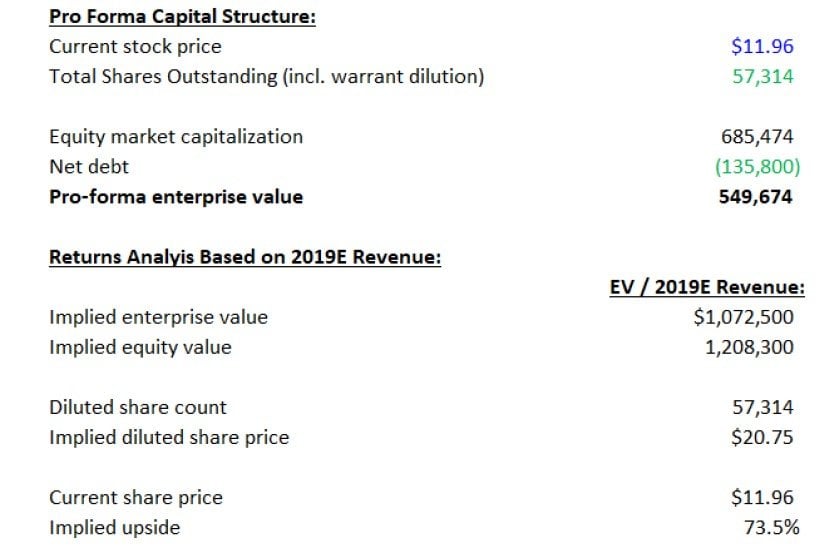

Applying GrubHub's 2019 revenue multiple to Waitr, suggests a fair value of $20.75, or 73.5% upside to Waitr's current price.

Source: FactSet, LCA presentations, Dane Capital estimates

In particular, as compared to GrubHub, Waitr shows a huge discount on EV/2018E revenue and EV/2019E revenue of 3.0x and 4.2x respectively. For investors who are worried about a possible bubble in the online food delivery space, we would recommend doing a pair trade by shorting GrubHub since GrubHub is not heavily and is not expensive to borrow. We believe this is a sensible strategy for more conservative investors.

Source: FactSet, LCA presentations, Dane Capital estimates

Below are Dane Capital's revenue estimates, the high-end of guidance from Waitr's presentation, and the "Waitr Management" numbers from page 128 of their proxy:

Source: FactSet, LCA presentations, Dane Capital estimates

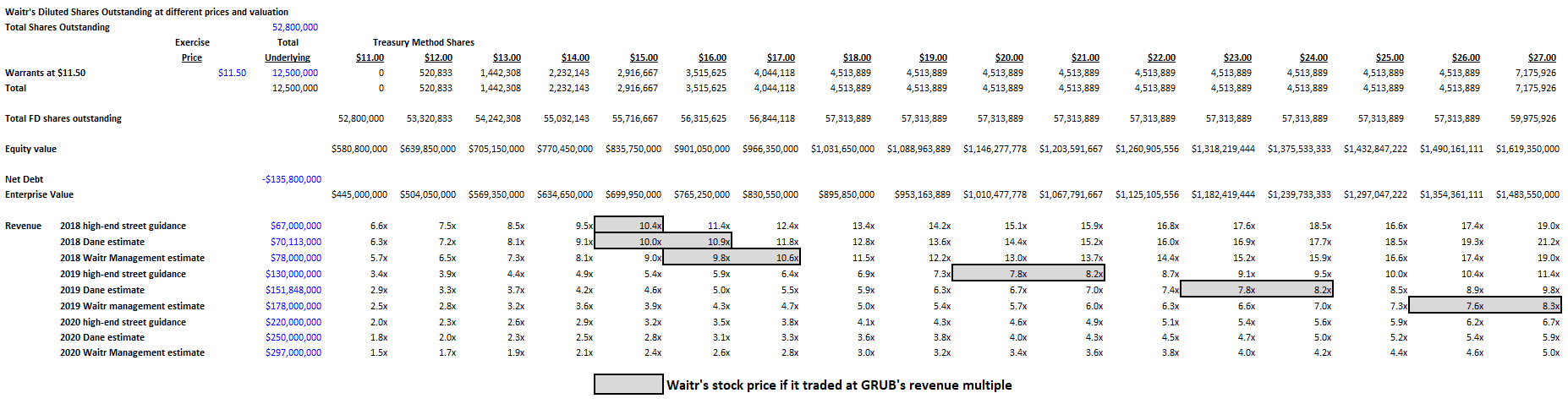

Finally, below we provide potential EV/revenue multiples based on different revenue scenarios accounting for the impact of warrants. It is worth stating that management has mentioned to us that they will act expeditiously to tender for the warrants (LCAHW) or to exchange them for a stock at premium to current prices, thus limiting their dilutive impact. We think this is sensible given our belief that management is extremely bullish and optimistic about where its stock is headed. In any event, the warrants can also be exchanged on a cashless basis if shares trade above $18 for 20 of 30 trading days, and therefore our valuation does not include the dilutive impact additional shares using the treasury method at prices higher than $18.

Source: Waitr filings, company presentations, Dane Capital estimates

6. Risk Factors

Execution - Waitr is growing in excess of 100% annually. We are optimistic that it has the personnel in place to execute on its growth plan and with its additional capital should have greater resources to successfully identify and enter new geographies.

Competition - We believe that Waitr's strategy of pursuing tier-2 and tier-3 cities in areas near its Southeastern base should help ensure that it has a top 1 or 2 position in the new geographies it enters. In our view, the larger industry players are focused on tier-1 cities with larger populations.

However, it's possible that competition will be faster or more intense than we anticipate. We believe that larger players are better served buying than building should they wish to enter Waitr's geographies.

Slower than anticipated shift to online - We expect the shift from offline to online restaurant delivery to be strong for years to come, just as it has been in virtually every other industry. Should an unexpected force disrupt this shift, Waitr, and the industry's growth may be less than anticipated

7. Conclusion

With the explosive growth in the online food delivery space, we think that Waitr is the cheapest and most attractive opportunity to in the sector. We believe it is likely to be a considerably larger company in several years with a commensurately greater valuation. Waitr not only provides a differentiated approach of focusing on tier 2 and 3 cities, it has managed to achieve much higher growth rates as compared to peers due to its hub-and-spoke model, despite trading at lower multiples than comparables. With the new injection of capital through the business combination, we believe Waitr will continue to display high rates of growth going forward. We are optimistic that looking out several quarters, shares will be 50-100% higher than current prices. We are also confident that management will act expeditiously to eliminate warrants (via tender or exchange for shares) which could offer a hefty premium from current prices, likely before year-end.

Disclaimer: This article was provided for informational purposes only. Nothing contained herein should be construed as an offer, solicitation, or recommendation to buy or sell any investment or security, or to provide you with an investment strategy, mentioned herein. Nor is this intended to be relied upon as the basis for making any purchase, sale or investment decision regarding any security. Rather, this merely expresses Dane's opinion, which is based on information obtained from sources believed to be accurate and reliable and has included references where practical and available. However, such information is presented "as is," without warrant of any kind, whether express or implied. Dane makes no representation as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use should anything be taken as a recommendation for any security, portfolio of securities, or an investment strategy that may be suitable for you.

Dane Capital Management, LLC (including its members, partners, affiliates, employees, and/or consultants) (collectively, "Dane") along with its clients and/or investors may transact in the securities covered herein and may be long, short, or neutral at any time hereafter regardless of the initial recommendation. All expressions of opinion are subject to change without notice, and Dane does not undertake to update or supplement this report or any of the information contained herein. Dane is not a broker/dealer or investment advisor registered with the SEC, Financial Industry Regulatory Authority, Inc. ("FINRA") or with any state securities regulatory authority. Before making any investment decision, you should conduct thorough personal research and due diligence, including, but not limited to, the suitability of any transaction to your risk tolerance and investment objectives and you should consult your own tax, financial and legal experts as warranted.