Euclidean letter for the third quarter ended September 30, 2017; titled, “Has Value Investing Lost Its Shine?”

Coming out of the financial crisis, Euclidean delivered strong returns to our investors. During that time, one of the more insightful—and, at the time, theoretical—questions we received from current and potential investors came in a form resembling:

“How well will you adhere to your model when you have your first period of extended underperformance?”

This was an important question because it honed in on the fact that it is easy to adhere to an approach when everything is going well, and it is human nature to contemplate trying something new following recent difficulty. In recent years, this question has become timely, as our returns and the returns of many value strategies have materially lagged the market.

Q3 hedge fund letters, conference, scoops etc

Answering this question requires us to have a thoughtful perspective on whether the investment principles underlying our approach are in decay or will persist across time, even if they ebb and flow with market cycles.

On the side of abandon, it seems worth pondering whether there can be any persistent investment principles whatsoever. After all, industries evolve; companies emerge, mature, and go away; market structure adjusts; and accounting standards change over time. Thus, many of the conditions that could lead to a particular style doing well at one time may not exist in future periods. Moreover, even if a particular approach proved resilient in the face of those types of changes, investing is a competitive business, and you might expect such an approach to be rapidly adopted, such that good opportunities would be competed away. Thus, there is some reason we might not expect what worked in the past to be an adequate guide for future endeavors.

| Wall Street Journal, August 2017 | J.K. Galbraith, A Short History of Financial |

And yet, on the side of adherence, Galbraith's quote suggests another angle. His words describe how investors’ short memories cause them to over-optimize for present conditions and underappreciate Mr. Market’s cyclical nature. Indeed, if past investment experience has any value whatsoever, then it must be because there are some persistent patterns that transcend industry, accounting, and market structure changes and that lead to fruitful long-term results. Perhaps these patterns can be resilient to competitive pressures if they occur over a time frame that stretches beyond the average investor’s working memory and time horizon.

So, this is the task at hand. Long-term investors must determine which of history’s lessons to hold and which ones to discard. And, in the context of our recent performance, you must determine if our results are a sign of secular changes that have broken whatever previously fruitful cause-and-effect relationships were behind previous returns, or if the results reflect temporary, cyclical conditions such that you may be well-rewarded by staying the course.

The foundation in question

So, let’s review the foundation of our investment process. After selling our previous business, we wanted an investment strategy geared to tax-efficient compounding over the remaining 40–50 years of our investment lifetimes. To this end, we use machine learning to look for ways of investing in public companies that have performed well across very long periods of time.

This involves building systems to evaluate today’s companies in the context of firms from the past that resemble them. By evaluating how similarly situated companies from the past evolved both operationally and from a market value perspective, our process attempts to form an empirical, historically grounded context for selecting investments. In this effort, we look across decades at what occurred in different interest rate environments and market cycles. We examine industries that have emerged and declined, and a diverse set of companies providing a wide variety of products and services.

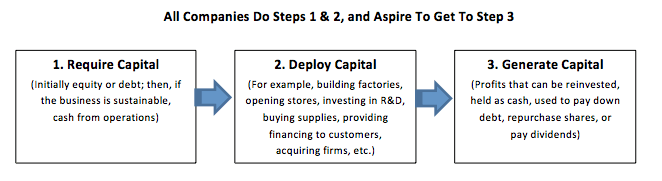

Despite these differences, our research found that we can normalize and compare companies based on how well they create wealth for their owners. That is, regardless of industry, maturity, or growth profile, all companies require, deploy, and (in some cases, but not all) generate capital that enhances the wealth of their shareholders.

Euclidean examines the character and consistency of this process for today’s companies, in the context of their capital structures and enterprise values, to rank them on what appears to have been generally fruitful in the past.

And, from our perspective, what appears to have been fruitful feels like common sense. For example, we found validation for statements such as:

- Companies that have consistently generated a lot of cash for their shareholders in relation to the capital invested in their businesses, tend, all else being equal, to be worth more than those companies that generate little or no cash, or that have a volatile history of cash generation.

- Companies undergoing a lot of changes to their capital structures, or that are overly reliant on debt or equity issuance to fund operations, tend to be less reliable investments.

- And, most importantly, companies that possess a favorable combination of these kinds of qualities tend to perform best as investments when they are priced at very low prices.

We adhere to principles like these because we believe that they increase the probability of building an equity portfolio that performs well over the long term. Our belief emerged through our own research and was bolstered by the vast body of work showing the merits of adhering to even very simple value strategies over long periods.

For example, there is extensive evidence shared by others and in our previous letters, showing that by paying very low prices in relation to any one of a number of different intrinsic measures (earnings, book value, sales, etc.), investors would have done well across long periods.

How could this have ever been true? And, as it appears to have been true across the past 50+ years, could it now cease to be?

The Value Advantage, Gone For Good?

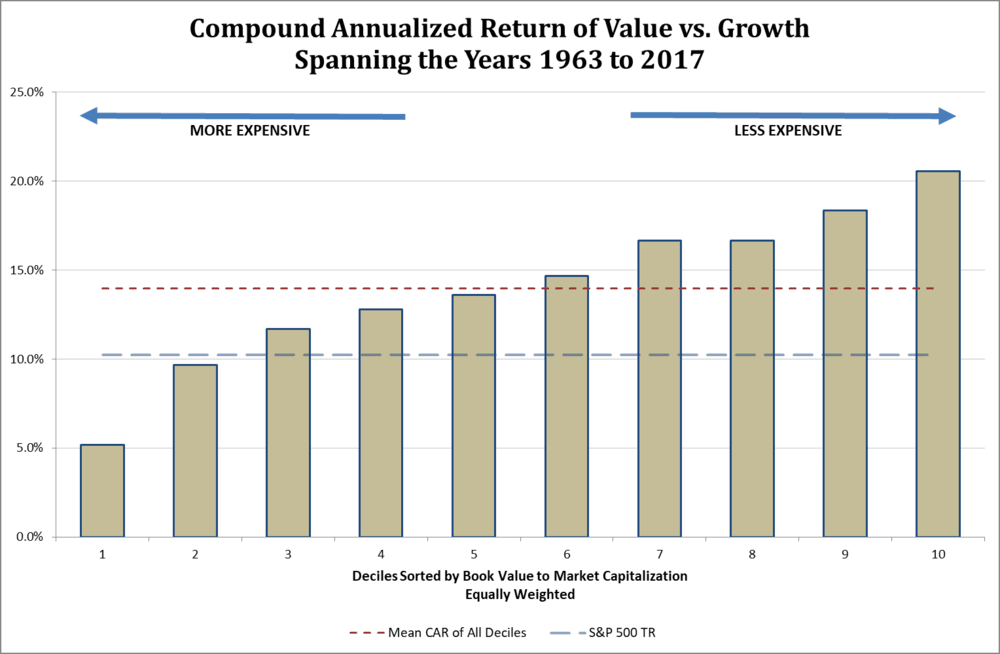

For long-term investors, value strategies have previously demonstrated a major advantage versus indexed or growth strategies. The chart below shows one dimension of this advantage by plotting the returns of companies based on how cheap or expensive they were as measured by price-to-book. We share results by decile, and we use price-to-book because it is the most widely studied of the value factors. Earnings-based measures, such as price-to-earnings or EBIT-to-Enterprise Value, appear to show an even more significant value advantage than what is presented here [1].

Thus, a value orientation has been a major advantage over these past 50+ years, and it has been evident across most rolling five-year periods, as you can see here.

We believe that this value advantage is caused by powerful human biases that impact investors’ evaluations of companies’ future prospects. It is well-documented that people fear losses more than they value gains. It is also well-documented that, when people make decisions, they have a tendency to give more weight to recent experiences than to experiences from the more distant past.

Perhaps this is why, when investors identify exciting companies, they seem to imagine them growing to the sky. We believe this is why investors perpetually overpay for growth companies, making them (as a group) poor investments. Likewise, with companies facing some sort of difficulty, investors seem to assume that because things have gotten worse, they can only get worse. Investors appear to extrapolate current difficulties to such extremes that value stocks became priced low enough to provide (as a group) better-than-market returns.

These investor tendencies seem systemic and provide a good model for understanding the cause of the historical value advantage.

Today, however, value strategies seem stuck in a rut, providing their weakest returns relative to the market in quite some time. Have investors evolved such that they have overcome the biases on which the value advantage depends?

That seems unlikely. If investors’ tendencies to take equity prices to extremes were in decline, we would expect to see tighter than normal spreads in how companies are valued. That is, we would expect to see growth investors being a little more careful with price paid, and we would also expect struggling companies to no longer sell at the very large discounts that enabled good value returns in the past. But the opposite is occurring. Recent valuation spreads appear wider than at any point in the past 50 years, except for during the peak of the dot-com bubble. [2]

Instead of the value advantage being in decay, we believe we are simply in the midst of one of those times required for the value advantage to persist over the long term. Look at the cycles between value and growth investing, which we have described in great detail in prior letters. There have been six distinct periods since WWII when growth outperformed value on a trailing five-year compounded return basis, and we are currently in one of these periods. During each of these times, value investing appeared dead.

There is no question that it is very difficult to adhere to value-minded principles during periods such as these. But it has to be this way. If value strategies delivered good results all the time, everyone would embrace them, and perhaps then, the value advantage could be arbitraged away.

But, at least for now, that time seems far off. Because the value advantage delivers over a time frame that apparently stretches beyond the average investor’s working memory and time horizon, we think very few investors are able to maintain the necessary long-term commitment it requires. And, as they deviate, running off after the incredible wonders of the present, our view is that investors are unwittingly creating the conditions for another fruitful period for value-conscious investors.

Best regards,

John & Mike

The opinions expressed herein are those of Euclidean Technologies Management, LLC (“Euclidean”) and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Euclidean reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Euclidean Technologies Management, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Euclidean including our investment strategies, fees and objectives can be found in our ADV Part 2, which is available upon request.

{kind=link}