Mittleman Investment Management commentary for the first quarter edned March 31, 2018.

Mittleman Investment Management, LLC’s composite declined 11.3% net of fees in the first quarter of 2018, versus declines of 0.8% in the S&P 500 Total Return Index and 0.1% in the Russell 2000 Total Return Index. Longer-term results for our composite through 3/31/18 are presented below:

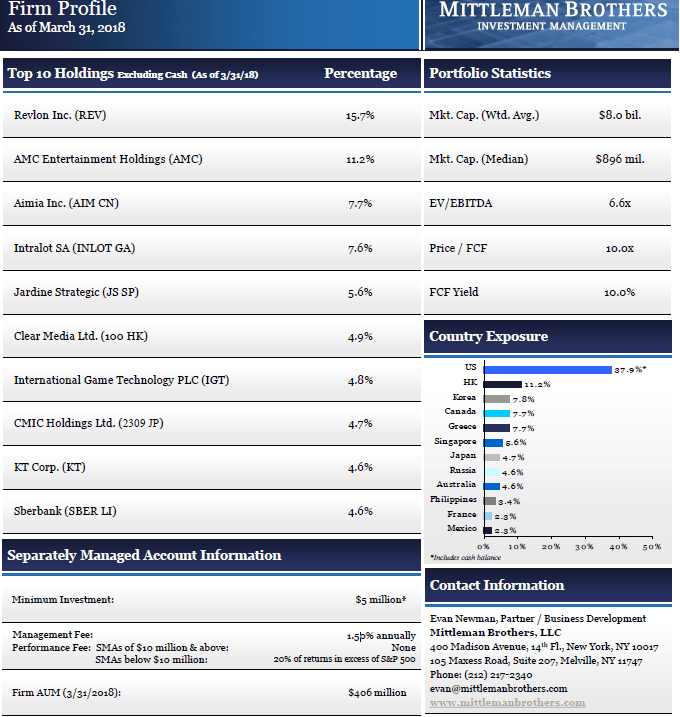

The top three contributors to our Q1 2018 performance were CMIC Holdings (2309 JP): $17.93 to $25.38 (+42%), Sberbank (SBRCY): $17.03 to $18.65 (+10%), and Intralot (INLOT GA): $1.36 to $1.41 (+4%).

CMIC’s stock price was awoken from its long slumber by news of new contracts, and strong earnings. As one of the largest CROs (Contract Research Organization) in Japan, CMIC benefits from the secular tail wind of increasingly outsourced R&D spending by pharmaceutical companies in Japan, catching up to their U.S peers in that regard. CMIC is also a testament to the benefit of patience, as the stock had languished in our portfolio for 5 years from 2012 to 2017, but more than doubled in the past year from $12.29 in April 2017 to as high as $28.37 recently. The founder and CEO, Kazuo Nakamura, still owns about 40% of the shares, and listening to the advice of some U.S. shareholders, he led the Board to initiate a stock buyback program last year while the stock was still abysmally cheap. We think fair value for CMIC is $31, about 22% higher than the quarter- end price, which would put this growing company at only 9x EBITDA, versus 15x EBITDA for PRA Health Sciences (PRAH) and 13.5x for IQVIA Holdings (IQV), both in the global CRO peer group.

Intralot was also the beneficiary of positive sales news, as it won a major new contract in February for $340M over 10 years ($34M per year) working with the U.K. lottery company, Camelot, on the Illinois state lotteries. Intralot’s U.S. business is their biggest and most profitable, providing about $60M in EBITDA annually, or about 40% of total company EBITDA on a proportionate (versus consolidated) basis. And yet because the company is domiciled and listed only in Greece, it suffers a significantly discounted valuation versus the major peers, despite getting 94% of its sales from outside of Greece. But I was very encouraged to hear on the company’s March 29th quarterly conference call that they were actively discussing with advisors the prospect of bringing their U.S. subsidiary public here, which we encourage, as it would certainly highlight the value of that division and hopefully of the company overall. Also, there is a huge lottery contract coming up for bid in late May for the Pennsylvania State Lotteries, a contract which has been with Scientific Games for the past 10 years. Intralot will bid and while the incumbent usually has an advantage, if Intralot did win it would likely be a game changer for Intralot, providing a massive increase in their earnings. Our other lottery company, International Game Tech (IGT), is also bidding for that PA lottery contract, but given their much larger size, it would be a more muted impact on their business, yet still a significant positive. The contract award will be announced in June. I estimate 121% upside potential for Intralot from quarter-end price of $1.41 to my fair value estimate of $3.11 (7x EBITDA), and that is not including the PA contract, should they win it.

After producing a 52.6% total return in 2017, Sberbank continued its ascent in Q1, rising 10%, propelled by strong earnings growth. Despite these gains, SBRCY still has significant upside potential to reach our conservative estimate of fair value, which is currently $25 per share, a P/E of 10x $2.50 in earnings per ADR. But, while this letter is a review of Q1 2018, I would be remiss not to at least comment briefly on the sharp drop that Sberbank’s stock has experienced in just the past few days due to a new round of sanctions levied by the U.S. on individuals and businesses in Russia, some of which Sberbank (which is not under sanctions itself), has lent money to. But those secured loans only amount to $9.75B, or 2.5% of Sberbank’s $390B in assets, and 16% of their $60B in shareholder equity, and less than one year’s worth of net income which is running at about $15B per year now. Again, the sanctions don't directly affect Sberbank, but as the biggest most liquid stock in Russia, it suffers as an easy source of funds. Sberbank’s CEO Herman Gref is a reformer, and runs the bank very well with enviable metrics, and I think he is recognized by the West as a man we could do business with in a post-Putin Russia, thus neither he nor the bank is targeted directly by these sanctions. Sberbank remains one of the largest banks in Europe with likely the highest ROE (23%+), a strong balance sheet (CET1= 11.4%), and lowest valuation. And it has vastly outperformed the likes of Bank of America (BAC) or Deutsche Bank (DB) from 12/31/07 until 03/31/18, with Sberbank up during that period, from $16.73 to $18.65 (plus significant dividends), while BAC is down from $41.26 to $30, and DB is down from

$101 to $14. So while Russia is perhaps hopelessly corrupt, they carry very little debt, at the sovereign level and at the household level, which leaves room for further penetration of basic financial services (credit cards, auto loans, mortgages, etc.) over the long term, and Sberbank, with nearly 40% of the country’s deposits, is practically a monopoly over there. So while we did sell some during Q1 in the $18 to $21 range to rebalance, with the stock suddenly back down here at $13 yesterday, a P/E of 5.2, with nearly 100% upside to fair value, we’ll hold on until the missiles stop flying. Also recall that it was not sanctions that put Russia into recession from late 2014 into early 2016, it was the price of oil, with the Brent oil price dropping from $115 in June 2014 to $27 in January 2016, a 77% drop. Brent oil is now $72 and trending up. So that should outweigh, fundamentally, any negative impact of the new sanctions.

The three most impactful detractors from our Q1 2018 performance were Aimia (AIM CN): $2.99 to $1.34 (-55%), Clear Media (100 HK): $1.00 to $0.76 (-24%), and Village Roadshow (VRL AU): $3.04 to $2.39 (-21%).

Aimia (AIM CN), based in Montreal and formerly known as Groupe Aeroplan Inc., is a holding company that owns as its primary asset 100% of Aimia Canada Inc., which operates the Aeroplan coalition loyalty program in Canada, with over 5M members (14.2% of the Canadian population, 34% of households), second in Canada only to Air Miles (owned by NYSE- listed Alliance Data Systems (ADS)) which has 10M members. While stand-alone loyalty programs are common in the U.S. (for example if you buy coffee at Starbucks regularly and join their loyalty program, you earn points redeemable for free coffee for doing so), in Canada, the U.K., Brazil, Mexico, and many other countries, multi-partner coalition loyalty programs, usually anchored by the frequent flier program of one major airline, are also very popular. The concept has never really caught on in the U.S., although American Express tried to launch one in 2015 with their “Plenti Card” program that partnered with Rite Aid, Macy’s, and other retailers; it failed to gain traction and was shut down in January 2018, which highlights the difficulty in building such a program to scale from scratch, even for a huge firm like AMEX. Frequent flier programs of most major airlines are the most cash generative businesses they have, in good and bad times. Aimia, anchored by Air Canada, was the first frequent flier/coalition loyalty program to come public as a stand-alone entity when it did so in 2005. A couple of other programs, listed in Brazil, have since followed: most recently Smiles SA (frequent flier program for Brazil’s Gol Airlines, went public in April 2013 and has seen its share price nearly quadruple since then, now trading at EV/EBITDA of 13x, mkt. cap/FCF of 20x) and Multiplus SA (frequent flier program for TAM airlines, IPO’d in 2010 and more than doubled since then, with 10% dividend yield at current price, trading at 8x EBITDA, 10x FCF).

These are high margin businesses that have unusually high free cash flow conversion relative to EBITDA, and where sales and EBITDA are much less relevant than gross billings (miles earned) and redemptions (miles redeemed) which is also known as the burn/earn ratio which rarely crosses above 100 (where cash burns) on a quarterly basis and never has on an annual basis since the plan was founded 1984. A very loose analogy for the burn/earn ratio might be the combined ratio of a property & casualty insurance underwriter. But, in this industry, unlike the insurance business, no regulator dictates how much capital reserves must be held against the deferred liabilities created, or how the float must be invested. And during recessions, while gross billings go down as people charge less on their credit cards, demand for travel also drops even more so, such that the spread between miles burned and miles earned and the resulting FCF is relatively unscathed.

Air Canada, the core partner for Aeroplan (which was wholly owned by Air Canada prior to its 2005 IPO) announced in May 2017 that they would not renew their contract with Aeroplan when it expires in mid-2020. The stock fell over 60% on the day of that announcement, and we started buying it a few weeks after. Then Aimia announced that it would suspend dividend payments, which we expected, and the stock fell further as an almost entirely dividend-oriented shareholder base evacuated, and we bought more. Our premise was and still is that Aeroplan should be able to supplement a less lucrative relationship with Air Canada post-2020 with multiple other airlines who would happily take the business. Aeroplan is by far the largest ticket buyer for Air Canada, so other Canadian airlines like Westjet or even U.S. airlines like Delta that fly similar routes should be willing to offer bulk ticket purchase discounts to have Aeroplan airline ticket buyers redirected to their seats. Such discounts for Aeroplan should be wide enough to make the business attractive, if not quite as attractive as the current deal with Air Canada, which will still remain a redemption partner for Aeroplan post-2020, but just not on such favorable terms. Another key facet of our investment thesis with Aimia is that there is plenty of value in other Aimia holdings to protect us should Aeroplan not survive. That subsidiary, Aimia Canada Inc., is distinct from the holding company, Aimia Inc., so liabilities from that segment shouldn’t destroy the value of the other assets held by the holding company, assets which include, for example, its 49% ownership of PLM Premier (5.3M member, fast growing coalition loyalty program anchored by Aeromexico, Mexico’s flagship airline). This is comparable to the Phillip Morris (MO) investment we made in 1999 as it dropped from our first purchase at $40 to $19 by year-end, as we believed the fear of Philip Morris USA going bankrupt was overdone given that the holding company also owned Kraft Foods, Miller Brewing, and other assets that wouldn’t be touched by Philip Morris USA’s potential bankruptcy, and the stock more than tripled over the next 5 years.

Aimia was our portfolio’s top contributor in 2017, but has started this year in the penalty box as its share price dropped in response to the company selling Nectar (their UK loyalty program) to Sainsbury’s, the UK grocery chain and Nectar’s largest customer, on Feb. 1, 2018 at what we believe was an unreasonably low price. In response, we reduced our estimate of Aimia’s fair value from US$9.00 to US$5.89, which still provides significant upside from Aimia’s current price of US$1.34 and our average cost of US$1.59. The terms of the Nectar transaction caused us to amend our filing status from passive to active, and we subsequently engaged in a constructive dialogue with the company. Our discussions resulted in the company granting us two seats on the Board of Directors for our nominees (Jeremy Rabe and Phil Mittleman), and Aimia added a third nominee (W. Brian Edwards), who we also know well from when he was Chairman of the Board of Directors of Miranda Technologies (MT:CA), another Canadian company that we bought in early 2012 at around $11 and sold at $17 just a few months later as the company was acquired by Belden Cable. The press release from Aimia discussing these board additions can be accessed through the following link: https://www.newswire.ca/.

We believe the resulting board, if ratified by the shareholder vote on April 27th, will put us in a strong position to influence capital allocation and strategy in general for the company going forward, and adds significant loyalty and marketing experience to the board. As part of this agreement, we entered into a standstill with Aimia through June 2019. This standstill has no bearing on the Aimia position within our portfolio; rather it assures the company that we will not take any further actions against Aimia with respect to soliciting proxies, calling a special meeting, or proposing the removal of board members, etc. With the stock price at C$1.73/US$1.34 today, that is a market capitalization of US$204M, only 2.7x the US$75M in after-tax free cash flow we expect the business to produce in 2018. At 10x FCF the stock would have to rise more than 3.5x from current price of US$1.34 to US$5.00 per share, so we are very confident that this investment will prove to be a success. Even if Aeroplan were to implode on a tidal wave of redemptions due to the fear that Air Canada flight options would not be replaced by comparable seats on other airlines flying similar routes, then the other assets Aimia owns appear to be worth no less than US$1.60 (C$2.00), net of debt and preferred stock, which is 19% higher than the current price of US$1.34. But we think Aeroplan will be able to put together an attractive enough group of alternative flight options to keep card holders engaged post Air Canada’s highly discounted seats going away after 2020, and should likely be able to renegotiate a decent post-2020 deal with Air Canada as well, given the obvious mutual benefits of doing so. Aimia has said previously that they would be revealing their game plan for renovating Aeroplan for the post-2020 period when they announce Q1 2018 results on April 26, one day before the April 27 annual meeting, so we are looking forward to hearing more details on their strategy then.

Clear Media (100 HK), one of the largest outdoor advertising firms in China, had a good fundamental performance in 2017, with sales and EBITDA both up 6% for the year, just a little off their 7% CAGR over the past 10 years during which both figures doubled. But the stock fell 24% during the quarter since announcing on Jan. 2nd that they had discovered HKD 77M (USD 10M) in cash had been stolen from the company’s bank accounts. Two employees are under arrest for the crime, which mostly took place in 2010. The company established a special committee to investigate the matter, and their largest (50.4%) shareholder, Clear Channel Outdoor (CCO), has representation on that committee, which is using an independent external law firm and accounting firm to assist. The company retains ample net cash on the balance sheet of USD 52M (and no debt), and generates annual free cash flow of between $25M to $50M, most of which they distribute as dividends. We’ve owned the stock since it was HKD 4.00 (USD 0.52) in November 2012, and while it has dropped from HKD 7.77 (USD 1.00) to HKD 6.00 (USD 0.76) in Q1 2018, it has paid out dividends totaling $211.3M ($0.39 per share) over the past 5 years that we’ve owned it, averaging about $42.25M ($0.078 per share) per year, a greater than 10% yield versus the current market cap. of $414M. So while the theft is disconcerting, and clearly requires a significant change in their internal controls which they are undertaking, it doesn’t debase the overall high quality of the business and our optimism over its prospects. But the deficiency in their internal controls prevented them from getting a clean opinion from their auditor on their year-end final statement released March 29th, this led the Hong Kong Stock Exchange to suspend trading in the shares on April 4th, pending their own review of the company’s response to this issue. We think the company has responded adequately and thus the trading halt should be lifted soon.

We have experienced a couple of situations like this before. In November 1999, while I was working at PaineWebber/UBS with the clients who later became the foundation of Mittleman Brothers, and I was then (as now) severely under-performing a raging bull market, to make matters worse just before Christmas a stock I had bought one year earlier, Plains All American Pipeline LP (PAA), dropped from a split-adjusted $10 to $5 in one day on news that a rogue employee had gambled away $162M on authorized speculations in the oil futures markets which he was supposed to be using for hedging purposes only. That was a much bigger problem given the larger amount involved, and that the company already had a highly leveraged balance sheet. Still, I understood it to be a one-time event which didn’t diminish the long-term cash generating capacity of the company’s pipelines, so we bought more near the lows that very same day, and sold the entire position a couple of years later at nearly triple those prices. Also with Tyco International (TYC), we bought it in the summer of 2002 when the CEO, Dennis Kozlowski had just been fired after being caught stealing $81M in unauthorized bonuses among other transgressions. I thought the business should be unimpaired, despite the one-time hit, so we started buying the stock at $15 (before splits and spin-offs), thinking it was worth $25 to $35. It went almost immediately to $7 as front-page news speculated about a potential bankruptcy looming for Tyco due to technical default triggers in their bank credit lines relating to goodwill write-downs. We bought more near $7, and ultimate sold largely between $25 and $35 over the ensuing few years. And even beyond or own experience, Warren Buffett bought a huge position in American Express in 1964 after the stock was cut in half on news of “The Salad Oil Scandal” which was a fraud that cost AMEX dearly ($58M back then, versus total market cap. of about $300M) but didn’t diminish the long-term cash-generating capacity of the business. So Buffett tripled his money in Amex before selling it a few years later. My point is that if the business is good, the durability of that economic advantage should survive even much greater problems than that which Clear Media is enduring now. And therein lies the opportunity. We think Clear Media is worth nearly triple its currently depressed price, and with many years of growth ahead of it, so once the stock opens again, we’d expect to be buying more. One last point, Clear Media mentioned in their most recent presentation that they now get over 50% of their ad sales from e-commerce and tech related businesses (like Alibaba, Tencent, etc) which have displaced food, beverage, and autos from their former dominance. So if you believe that China will continue to shift to a more consumer-led form of GDP growth, while you could certainly buy Alibaba and/or Tencent, you would have to pay 26x EBITDA for either of those behemoths today. Whereas paying current price for Clear Media, a likely continued beneficiary of that growth, costs only 3.4x EBITDA.

We do not rely on potential catalysts when identifying holdings in which to invest, but we recognize this long period of underperformance has caused our clients to raise the question of catalysts and timing. So, we think it’s worth quickly highlighting an example of why one of our largest holdings’ stock price dropped, and why we expect it to recover in the not too distant future.

AMC Entertainment (AMC) fell from $35 in January of 2017 to approximately $11 in November 2017, and we significantly added to the position that we had received in December 2016 as partial compensation for the takeover of Carmike Cinemas, and brought our average cost down to $19.79. We believe the stock dropped for five primary reasons: 1) U.S. box office receipts declined 2.7% in 2017 and the summer was particularly weak, which brought out the almost perennial “Is the box office dying?” critics, 2) there was a fear that Premium Video on Demand (“PVOD”) was imminently going to be offered by studios, further damaging the theatrical window for exhibitors, 3) the emergence and hype behind MoviePass which created a fear that their artificially low subscription pricing structure would eventually lead to pressure on general movie ticket prices, 4) fears that AMC’s majority owner, Wanda, would somehow cause damage to AMC due to its highly publicized leverage issues and 5) integration issues with its Carmike purchase that further depressed EBITDA.

Since AMC’s stock hit its low, the box office has seen a major resurgence, with many now calling for a record year in 2018, PVOD has been declared dead (for now), MoviePass has found itself cutting prices further in what appears to be an urgent need for cash as its seemingly unsustainable business model appears to be showing signs of stress, Wanda announced significant asset sales (while reaffirming its commitment to AMC via the addition of a new, Wanda-appointed Chairman of the Board), and the Carmike integration issues appear to have been resolved. In addition, the Company sold over $300 million of non-core assets and sale-leasebacks to reduce leverage, on top of a $640M secondary they completed at $31.50 in February 2017. More recently AMC indicated they would likely pursue an IPO of its European operations, at a rumored valuation of over $2 billion. Regal Entertainment (RGC) agreed to sell itself for $23/share in December 2017, a 53% premium to its November 2017 low of about $15, and a 9x EBITDA multiple. AMC at that same valuation would be $26.35, but we’re using a target multiple of 9.5x because AMC is much further along in the cap-ex intensive process of converting theaters to the new, attendance-boosting recliner seats, and AMC gets 20% of sales from Europe, where attendance trends have been stronger than in the U.S. and growth potential and valuations for theater stocks over there are generally much higher, so we think AMC is worth 9.5x EBITDA, putting it into the low $30s. In spite of all these positive course corrections, as well as a stock buyback and insider buying throughout the decline at significantly higher prices, and the planned IPO of its European operations, AMC ended Q1 2018 at $14.05, barely above its lows achieved as those many fears were peaking, and far below our current minimum fair value target of $32. Why did the stock act so quickly and decisively in reacting to these fears, but not rebound as those fears appeared to be either unfounded, or otherwise resolved?

It’s also worth noting that legendary value investor Seth Klarman (Baupost Group) bought 3.6M shares of AMC in Q3 2017 and another 1.4M shares in Q4 2017 for a 9.9% stake in those class A shares (MIM held 6% of class A shares as of 12/31/17), so we’re not completely alone in our contrarian stance on this one. We believe AMC’s upcoming quarters will be a positive surprise and that the market will soon be reminded of how operating leverage also works to the upside in high fixed cost businesses such as AMC’s.

General commentary:

Our highly concentrated, value-oriented and contrarian approach can be, as it has been recently, woefully out of sync with a protracted bull market, but just as often it can be wonderfully out of sync with a protracted bear market as well. And even when we’ve sharply under-performed, like during the Global Financial Crisis of 2008 when our Composite dropped -64% vs. -37% for the S&P 500 that same year, over the 5-year period from 12/31/07 to 12/31/12 our composite gained 120% versus just 9% for the S&P 500.

The market averages, and the most popular names in particular, appear very expensive to us and the dichotomy present today between the popular and unpopular in terms of valuation reminds us very much of 1999. In 1999, while the internet stocks were going up incessantly and we (on behalf clients who became the foundation of Mittleman Brothers LLC a few years later) held boring old companies like Phillip Morris, some clients got so impatient watching their friends making seemingly easy money in AOL, Cisco, JDS Uniphase, and many others that they couldn’t help but take some money out to buy those stocks, against my strongest admonitions not to do so. Over the ensuing 3 years (2000-2002) those “must own” stocks dropped 80%, while the boring, out of favor stocks that comprised the portfolio then gained 20% on average (Phillip Morris tripled during that time frame).

We see a similar set-up taking shape now. Given the immense size of some of the most popular names today, like Amazon, I wonder if anyone has considered the possibility that such huge entities might not escape the cyclical effects of a recession, and what much slower growth, or even an outright decline in sales for a year or two might mean in terms of valuation compression. In the year 2000, Amazon’s sales growth slowed from 169% in the year prior to 68%, and then to 13% in 2001, during that relatively mild recession of 2001. So even though the business never stopped growing, by merely slowing down the rate of growth Amazon’s stock dropped from a high of $113 in 1999 to a low of $5.51 in 2001, a 95% decline, while our “boring” stocks made very satisfying gains in that same time period.

We also look back to 2011 for additional perspective because that’s when our portfolio’s upside potential to reach our minimum appraisal of fair value last matched what we calculate it to be today. The 2011 valuation trough in our portfolio was followed by a 49.2% (net) Composite gain in 2012 and a 49.5% (net) gain in 2013. We were not frightened by the scary headlines in 2011 when the world was supposedly ending because Greece was in flames and the Euro was disintegrating, and we are not drinking the Kool-Aid currently with consumer confidence at levels not seen since 2000, and money so easy to make you can literally invent your own crypto currency. But our portfolio is very much as it was in 2011, significantly cheaper in valuation than the market indices, with a more resilient/less cyclical business profile overall.

Finally, we have always done our best to ensure clients understand the temperament and patience required to invest in a long- term oriented strategy like ours. And we believe that our client retention rate, which remains over 95% since inception, is a testament to the type of investors we have partnered with. We recognize that clients who have been with us for five years or less have not had a rewarding experience to date, but history has shown us that withdrawing money during downdrafts in our portfolio has proven to be destructive to long-term returns. The rational reflex, as difficult as it feels to act on, should be to add capital during such periods, and it has been encouraging to see that some our most sophisticated investors have taken notice of the opportunity set in our portfolio and have done just that. We truly appreciate your patience and we know how frustrating it is to endure periods like this. While we have been left out of the recent party, much like in 1999, we expect our abstinence from will be vindicated in the end, and your patience will be rewarded.

In arguably the best book on Warren Buffett, “The Snowball” by Alice Schroeder, on page 358 she describes how Buffett’s good friend Henry Brandt, a stock broker from New York that he’d known for over 15 years at that point, panicked and sold half of his Berkshire Hathaway shares at just over $40 in 1975, after they had fallen from as high as $93 just a couple of years prior.

Charlie Munger describes a rough 6-year period from the end of 1969 when Buffett closed his partnership and distributed Berkshire Hathaway stock to his LPs. It closed at $42 on 12/31/69, and 6 years later on 12/31/75 it was $38. While the Dow Jones had risen +36% in those same 6 years. The book quotes Munger, “It looked like not much was happening favorably for a long, long time. And that was not the way our partners, by and large, had previously experienced things. The paper record looked terrible, yet the future, what you might call the intrinsic record, the real business momentum, was gaining all the while.”

So these are the lessons of history, and even the greatest investors of all time were made to learn them. Yes, it has been a long 3.6 years since we hit out high water mark in performance on Aug. 31, 2014, but not so long that we are in any way dissuaded or discouraged as to the merits and validity of the long-term value-oriented investment discipline to which we continue to adhere. We continue to be “all-in” on the strategy with our personal funds, and recognize that many of our longer term individual clients are similarly situated. It is an honor and a responsibility that inspires and energizes us every day to constantly inquire, to expand and deepen our understanding of the businesses we own and those against which they compete, to question even our most certain of premises such that we take nothing for granted, and to leave no stone unturned in our relentless search for new opportunities.

Sincerely,

Christopher P. Mittleman

Chief Investment Officer - Managing Partner