Key Points

- The demand for socially responsible investing strategies is growing as a means to manage environmental, social, and governance (ESG)–related risks—which can impact long-term returns—and as an opportunity to promote social and environmental issues, but much remains unknown about the performance potential of these strategies.

- Research identifies two ESG metrics linked to good corporate governance, which have the potential to drive performance: notably, financial discipline and diversity.

- Rebalancing positions using thoughtful smart-beta product design is a powerful market-tested return enhancer. Combined with the two forementioned performance-driving firm attributes, it is a proven way to construct an ESG strategy with strong long-term return potential.

Abstract

Socially responsible investing strategies, which use environmental, social, and governance (ESG) criteria to position portfolios, are increasingly popular around the world. Socially responsible goals are lauded by most investors, but questions remain about the investment merits of strategies that constrain the portfolio construction process. Thus, many ESG-oriented investors face an uncertain tradeoff between social responsibility and investment performance. A growing body of research, however, has identified a set of company characteristics directly aligned with the tenets of ESG investing and associated with superior financial outcomes. Two of these, financial discipline and corporate diversity, top the list of governance-related metrics with potential positive performance implications. Combining a tilt toward companies that display these characteristics with the return engine of a fundamentally weighted portfolio presents the opportunity to earn superior long-term risk-adjusted returns for ESG-minded investors.

“…we firmly believe that investors do not need to abandon investment performance to achieve their ESG objectives.”

Socially responsible investing (SRI), also called sustainable investing, is an approach that considers environmental, social, and governance (ESG) criteria in making portfolio construction decisions.1 Investors are attracted to SRI as a means to manage ESG-related risks—which can impact long-term returns—as well as an opportunity to promote social and environmental issues. As a result, demand is growing for attractive investment strategies that can satisfy the dual objectives of social responsibility and long-horizon outperformance.

We believe these dual objectives can be met by introducing two elements that go beyond the machinery of traditional ESG strategies. The first element is to supplement standard ESG metrics with performance-driving firm attributes directly linked to ESG principles; in particular, this is the degree to which a firm possesses the financial discipline to generate sustainable long-term performance for its shareholders rather than make decisions to benefit its managers in the short run—essentially, acting as a bedrock of good governance—as well as the level of diversity among a firm’s ranks (to date, most often measured by its diversity in terms of gender).

Although limited data availability makes it difficult for researchers to draw conclusions from standard econometric tests, and much remains unknown about the performance potential of traditional ESG metrics, we find considerable research support for both financial discipline and diversity, with financial discipline more obviously and more practically amenable to traditional empirical tests than diversity, at least to this point in the research.

The second element is to apply thoughtful smart-beta product design and implementation techniques to an ESG strategy. For example, using the market-tested smart-beta portfolio construction technique of fundamental weighting, which breaks the link between portfolio weights and stock prices, allows us to capture the return engine of systematically rebalancing back to stable anchor weights, and spreading out trading over a period of days to preserve that rebalancing return through low implementation costs.

In this article, we summarize our understanding of the research related to the investment implications of ESG investing and present a case for how investors can meet both their social responsibility and investment objectives with a thoughtfully designed investment strategy.

Growing Demand for ESG Investing

The ESG space has experienced tremendous growth over the last half-decade. Investors are not only voicing—at times very vocally—their views on the importance of environmental, social, and governance issues, they are also speaking with their wallets.

According to the Global Sustainable Investment Review 2016 (hereafter GSIR, 2016), which reported the results of market studies performed by members of the Global Sustainable Investment Alliance (GSIA),2 US$22.9 trillion of assets were being professionally managed at the start of 2016 under SRI strategies, 26% of total global assets under professional management. Since 2014, when the GSIA last reported this number, these assets have grown 25%, from US$18.3 trillion.

In 2016, the largest sustainable investing strategy globally, and the predominate strategy in Europe, was negative/exclusionary screening (US$15.0 trillion), followed by ESG integration (US$10.4 trillion),3 which was predominantly used, on an asset-weighted basis, in the United States, Canada, Australia/New Zealand, and Asia ex Japan. In 2014, investments in these two strategies totaled US$12.1 and US$7.5, respectively. Of the US$8.7 trillion in SRI assets invested in the United States, US$5.8 trillion were managed under an ESG integration strategy, defined in the GSIR (2016) as “the systematic and explicit inclusion by investment managers of ESG factors into financial analysis.”

“Money talks. If we can deploy capital and the power of financial markets, we can ensure [these] companies make the transition needed to cap global warming.”

—Anne Simpson, CalPERS (Rundell, 2017)

The interest in ESG investing can also be illustrated by the results of the Pensions & Investments annual money manager survey. Of the worldwide institutional assets managed by the largest 500 firms responding to the survey, as of year-end 2016, US$3.9 trillion was invested with an ESG focus compared to US$1.4 trillion invested in factor-based strategies, another increasingly popular strategy with investors (Diamond, 2017). A global survey of 461 asset owners and asset managers found that by 2019, 46% of responding asset owners plan to have 50% or more of their funds invested in ESG/RI,4 and 54% of asset managers plans to market 50% or more of their funds as ESG/RI (BNP Paribas, 2017). ESG investing is making strong and steady progress into the mainstream of investing.

This trend is likely to continue. The members of one of the largest generations, Millennials,5 are moving into prime decision-making time for aligning their investing beliefs with their values, and they are making substantial efforts to reshape corporate behavior and to have their voices heard through various forms of activism. As a result, public pension sponsors and other asset owners are facing a surge of mandates to use their investing heft to achieve social goals such as reducing the carbon footprint, improving gender diversity, and so on.

The preference for ESG investing comes despite widespread views that ESG investing might involve a performance penalty. For example, Riedl and Smeets (2017) found that investors are willing to sacrifice financial performance to invest in accordance with social preferences, and that both social preferences and social signaling play a dominant role in investors’ decisions to purchase and hold socially responsible mutual funds.6 Although the available research is so far inconclusive, we firmly believe that investors do not need to abandon investment performance to achieve their ESG objectives.

What ESG Research Is Telling Us

The empirical research results on the investment merits of ESG investing are mixed. Some analyses support the classic market-equilibrium view that excluding segments of the market, such as those having a poor ESG score or “sin stocks” of companies associated with alcohol, tobacco, and gambling, should lead to worse investment outcomes, whereas other studies suggest that excluding companies based on ESG considerations may have no negative impact on returns. Other research, however, shows that taking ESG factors into consideration when making investment decisions can improve long-term performance.

“We believe that an economically efficient, sustainable global financial system is a necessity for long-term value creation. Such a system will reward long-term, responsible investment and benefit the environment and society as a whole.”

—From mission statement of United Nations Principles for Responsible Investment, www.unpri.org

We can understand the perspective of those who conclude that constraining portfolios to meet ESG preferences should theoretically deliver lower expected returns. According to standard economic reasoning,7 sin stocks should offer a return premium over “virtuous stocks” because ESG-investor demand for sin stocks is suppressed by ethical standards superimposed on the investment process, while virtuous stocks are priced relatively higher, leading to a differential in required rates of return. Hong and Kacperczyk (2009), Brammer, Brooks, and Pavelin (2006), and Fabozzi, Ma, and Oliphant (2008) reported results supporting this position—that investors pay a price for virtue.8 In what may be viewed as a bit of a plot twist, the logic of this standard economic argument also leads to a reasonable expectation of a one-time windfall for ESG investors (which may be called an “ESG-preference dividend”) as prices adjust to reflect newly asserted and increasingly shared preferences, a process that may take years and possibly decades to fully play out.

Interestingly, recent research suggests that the historical return premium associated with sin stocks can be explained by exposures to well-recognized factors. Blitz and Fabozzi (2017), for example, find that the excess returns from sin stocks can be fully explained by the two relatively new quality factors of profitability and investment (Fama and French, 2015): sin-stock companies happen to be both profitable and not aggressively growing their businesses, attributes typically rewarded in the market. The findings of Blitz and Fabozzi are robust over time and across different markets. This new evidence sheds light on how sin stocks may be earning a premium and hints at the fact we can address the potential shortfall in performance from shunning sin stocks by intentionally selecting high-profitability and low-investment companies (i.e., financially disciplined companies) in the more virtuous segments of the market.

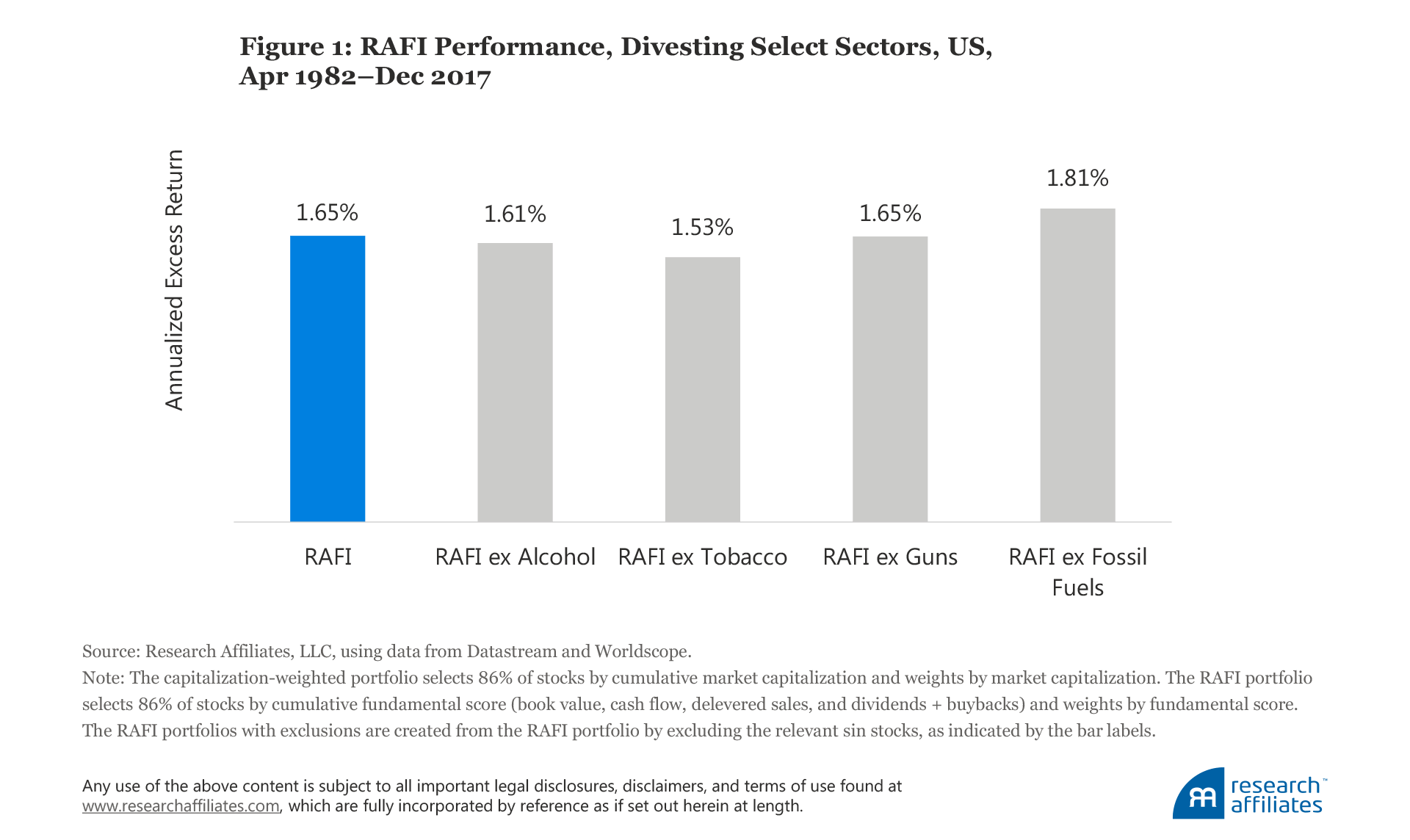

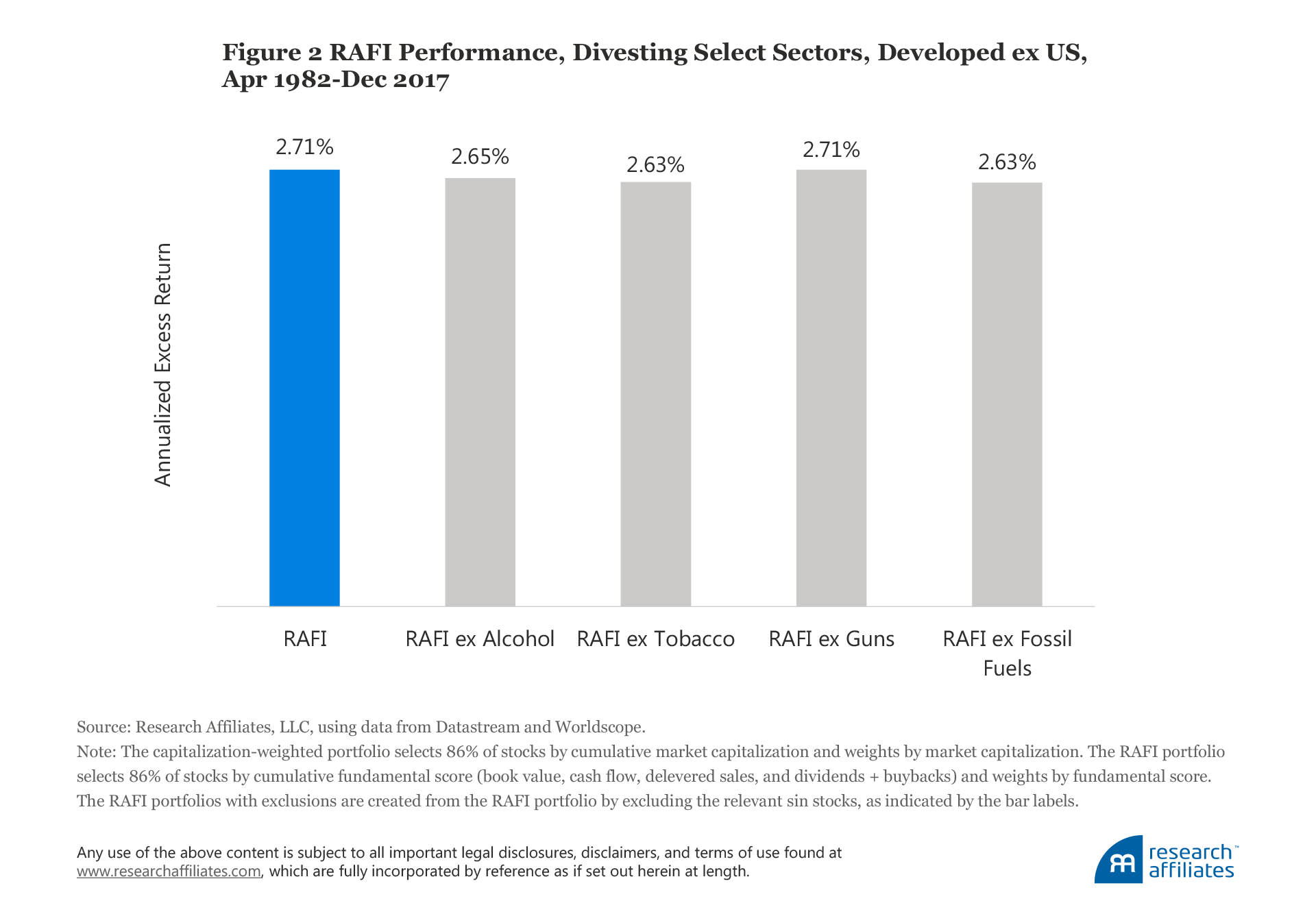

Recently, Jeremy Grantham and his colleagues at GMO (Huebscher, 2017) ran a simple but illuminating study to test the received wisdom that negative screens on subsets of companies and sectors—such as those involved in screening out sin stocks or divesting from fossil fuels—should be expected to hurt performance. Their conclusion was stark: yes, you can divest from oil, or anything else, without much consequence, busting one of the great myths against ESG investing. The GMO analysis removed one sector at a time from the S&P 500 Index and measured the performance of each resulting index over three periods beginning in 1925, 1957, and 1989, with each ending at Q3 2017. In each of the three periods, the worst performing index returned just 16, 21, and 27 basis points (bps) or less, respectively, than the S&P 500 over the same period.

We found similar results when we compared the performance of the simulated RAFI™ US Index and RAFI Developed ex US Index with their respective market’s cap-weighted index as well as simulated indices of each on the basis of ex alcohol stocks, ex tobacco stocks, ex gun stocks, and ex fossil fuel stocks.9 The comparative performance shows that, over the 35-year study period ending December 31, 2017, excluding a sector such as fossil fuels did not have a material impact on performance. For instance, the RAFI ex fossil fuels portfolio added 16 bps in performance versus RAFI US, while the RAFI Developed ex US ex fossil fuels underperformed 8 bps versus RAFI Developed ex US. In other words, the outperformance of each of these RAFI indices relative to the cap-weighted indices, on a simulated basis, was left economically intact when fossil fuel stocks were removed. We found similar results when stocks of alcohol, tobacco, or guns were removed. We thus conclude that the impact of excluding these controversial sectors from a portfolio is too small to be economically meaningful.

To this point, we have reviewed findings of ESG strategies based on negative screening, that is, the exclusion of certain stocks or sectors. But ESG investing strategies increasingly encompass approaches, such as positive/best-in-class screening, ESG integration, and sustainability-themed investing (GSIR, 2016), that tilt toward companies with attractive ESG attributes. In this context, Statman and Glushkov (2009) showed that tilting portfolios toward companies with high scores on social responsibility characteristics can actually improve performance. They do not resolve the origin of this performance advantage, however. One possibility we propose is that the different approaches to SRI and the varying definitions of the associated ESG criteria are leading to a slower-than-usual price discovery process as capital is reallocated according to a broad array of ESG preferences.

A survey by Amel-Zadeh and Serafeim (forthcoming) showed that the majority of responding investors believe ESG considerations are financially material to portfolio performance and that full ESG integration is the SRI strategy with the highest performance potential. The recent BNP Paribas (2017) survey showed nearly three quarters of respondents believe ESG can enhance investment returns over the long term.

Supplementing ESG Metrics with Closely Linked Performance Drivers

Among the corporate attributes directly aligned with ESG considerations and more reliably linked to positive financial performance in the academic literature, both financial discipline and diversity are natural sets of metrics that affect company performance positively and can be expected to improve investment returns. In the next two sections we summarize the research findings that support our conclusion.

“In a few short months, a substantial community of institutional investors have coalesced around this [the Climate Action 100+] initiative because they want to send an unequivocal signal—directly to companies— that they will be holding them accountable in order to secure nothing less than bold corporate action to improve governance, curb emissions, and increase disclosure to swiftly address the greatest challenge of our time.”9

—Andrew Gray, AustralianSuper (Rundell, 2017)

Financial Discipline

Good governance should, by definition, lead to better corporate financial performance. The extensive corporate financial data available have allowed considerable research into the connection between firm management, corporate outcomes, and investment results. In terms of ESG investing, the most immediately compelling body of research is a subset of what is referred to as quality investing, particularly financial discipline. To state the obvious, ill-governed companies that prioritize short-term gains for the benefit of management over the long-term wealth of shareholders fail to align with the good-governance intentions of ESG criteria and instead chip away at shareholder value. This can happen in small, legal, and not readily observable ways, sometimes culminating in dramatic fashion, as was the case of the Enron and WorldCom accounting fraud scandals nearly 20 years ago.

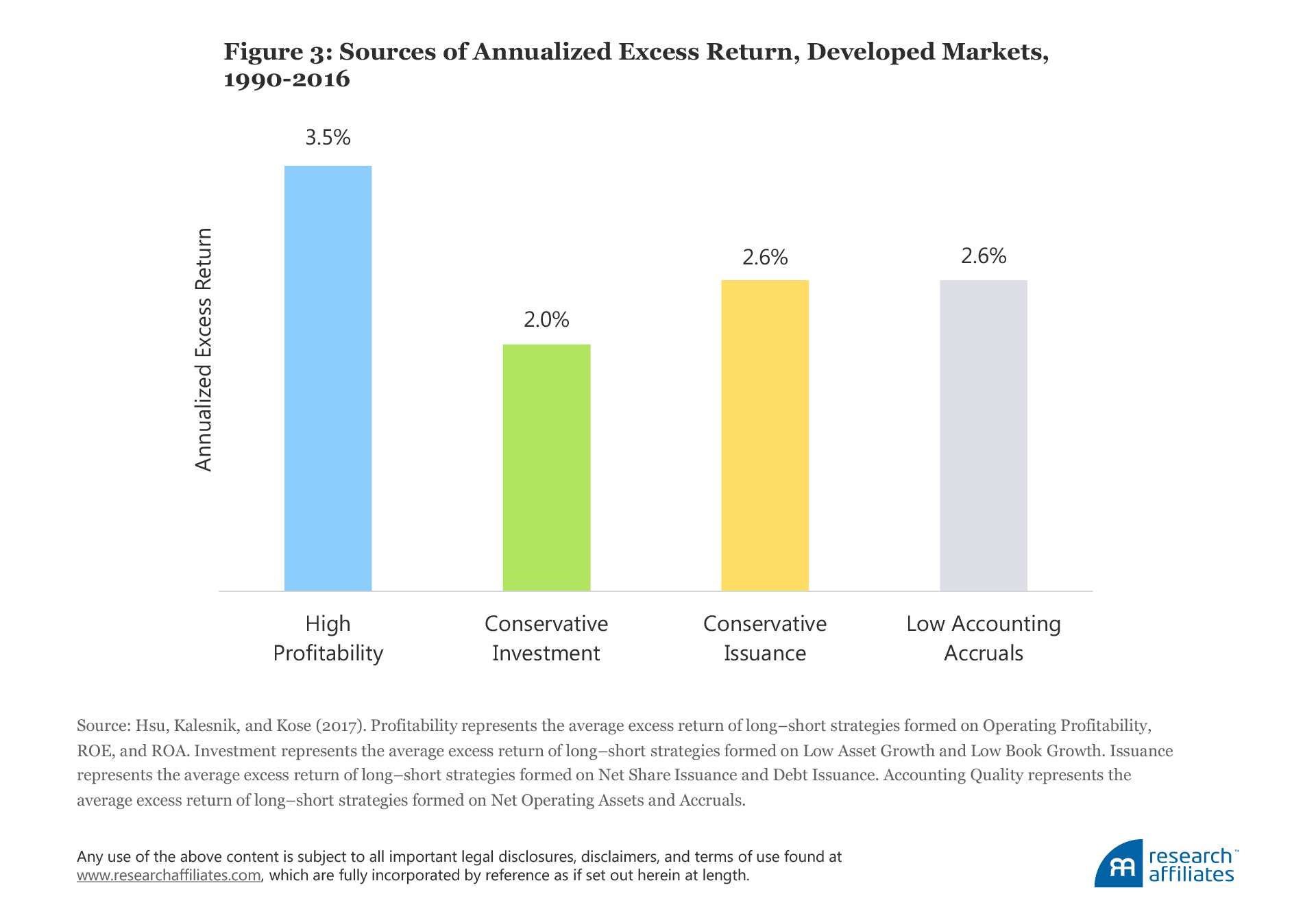

We are able to introduce a robust return driver based on metrics that indicate the presence of a financial discipline necessary to put long-term value ahead of short-term management comfort and support the investment merits of ESG investment strategies. In their recent survey of quality investing, Hsu, Kalesnik, and Kose (2017) identified four robust and complementary sources of return after adjusting for risk that directly speak to the preferred governance positioning of ESG investors: high profitability, low investment, low net issuance (or dilution), and low accruals.

High Profitability. Extensive research details a return premium associated with corporate profitability, measured by metrics such as operating profitability, return on equity, and return on assets.10 Novy-Marx (2013) suggested that the so-called profitability anomaly (labeled as such because it defies the efficient market hypothesis) results from investors’ limited attention, a form of cognitive and behavioral bias.

Low Investment. Discipline to avoid superfluous corporate investments—particularly by profitable companies—is a key attribute from the perspective of good governance, one associated with superior performance. For instance, Brightman, Clements, and Kalesnik (2017) studied “sustainable” businesses, those companies with the discipline to return earnings to investors in the absence of attractive NPV projects. In contrast, “unsustainable” companies, such as Compaq and Yahoo in recent decades, tend to fuel aggressive investments with excessive stock and debt issuance at the height of their profitability and to expand in ways that damage their competitive advantage in fields they had previously dominated.11 Eventually such companies’ bottom lines suffer from ill-conceived investments and expansions, and their shareholders pay the price.

Low Issuance. Empirical studies consistently document a negative relationship between net issuance and subsequent stock performance.12 The exact causality has not been isolated in the extant literature, although experience suggests firms that are issuing extra shares may either possess private information about their stock price’s near-term overvaluation or, as just described, are issuing shares and debt to finance poor-NPV projects.

Low Accounting Accruals. Finally, poor governance can manifest itself in the form of high accruals, an indicator that “short-termist” earnings management may be occurring. Specifically, a number of studies have found that differences between reported and actual profits, as indicated by net operating assets and accruals, predict lower subsequent returns.13

Corporate Diversity

In addition to the rapidly growing recognition of the social benefits of diversity and inclusion,14 a large and expanding body of research shows that a broad range of benefits—including better financial outcomes—accrue to companies who build and nurture diverse and inclusive teams. The business case for diversity is grounded in research showing that teams whose members represent a mix of gender, ethnicity, experience, age, and culture, among other traits, and who purposely cultivate inclusiveness, tend to make better decisions because they are able to achieve a higher level of Collective Intelligence (CI).15 High-CI teams do not just happen: assembling a group of people, all individually highly intelligent, does not automatically create a “smart” team; the goal is to create teams who represent diversity in reasoning and whose members respect and value the perspectives of others on the team.

Rock and Grant (2016) reported that more diverse groups recall facts more precisely and produce more accurate results, because they are “are more likely to constantly reexamine facts and remain objective” and ultimately “may outperform homogeneous [groups] in decision making because they process information more carefully.” Engel et al. (2014) found that equal contribution, frequent communication, and strong complex emotional perception are top predictors of a smart team. They also state that women, who on average score better than men in terms of social perceptiveness, contribute positively to a team’s CI (Woolley et al., 2010).

Research shows that diversity has a positive impact on business outcomes—in particular, improved financial strength, higher net margins, higher compound annual growth rates, higher valuations, more frequent product innovation, and fewer instances of governance-related controversies.16 Gender diversity has been more closely studied than other forms of diversity because of greater data availability.

While a number of studies have found that corporations benefit from greater gender equality,17 a handful have found an inconclusive or ambiguous relationship between a firm’s financial performance and the presence of women in leadership roles.18 These latter findings are not surprising given that research into CI shows diversity alone is insufficient to unlock the performance potential in team decision making. While it is not possible (yet) to directly measure the CI of a firm, the existing body of research provides substantial support for our conclusion that firms scoring well on existing measures of diversity, starting with gender diversity, are likely best positioned to produce the strongest long-run financial results.

“We also will continue to emphasize the importance of a diverse board. Boards with a diverse mix of genders, ethnicities, career experiences, and ways of thinking have, as a result, a more diverse and aware mindset. They are less likely to succumb to groupthink or miss new threats to a company’s business model. And they are better able to identify opportunities that promote long-term growth.”

— Larry Fink, CEO, Blackrock 2018 Letter to CEOs

The majority of the research on diversity points to stronger bottom lines, measured by higher earnings before interest and taxes (EBIT),19 for example, rather than to higher long-run stock returns. Unlike financial outcomes, which can be studied in the cross-section of companies, a robust study of investment returns requires a long time-series; therefore, the shorter historical samples on which researchers have studied the connection between diversity and investment returns can only be suggestive at best.20 That being said, the links among corporate management, financial outcomes, and long-run investment returns are well researched, as previously discussed in relation to financial discipline. Given that the literature on diversity points to better corporate outcomes, we can view diversity as a natural complement to the empirically studied return drivers associated with financial discipline.

Most diversity studies focus on the potential benefits of greater diversity, but evidence of a possible link between tolerance for bias, harassment, and discrimination—which has been called the “flip side” of diversity and inclusion—and more general corporate misbehavior, ranging from controversies to fraud,21 is beginning to emerge. Given that fraud negatively impacts investment returns in the long run, prudent investors may choose to tilt portfolios away from firms with poor diversity scores as a risk-mitigation measure.22

Finally, the public statements and admonishments (a combination of carrots and sticks) that have recently been delivered by prominent pension fund sponsors and major global asset managers lead us to believe that the ESG-preference dividend is most acutely applicable to the issue of diversity, and gender diversity in particular. As a result, investors may anticipate a transition path over which higher returns accrue to higher-diversity companies and all companies rationally seek greater diversity among their ranks.23 Investors may benefit from embracing diversity metrics in ESG strategies in the pursuit of superior investment returns through this additional channel.

Putting Smart Beta to Work in ESG Portfolios

In addition to enhancing traditional ESG metrics with return drivers closely linked to corporate governance, such as those associated with financial discipline and diversity, the use of smart-beta portfolio methods—which start, we believe, with breaking the link between price and portfolio weight—can generate an additional source of outperformance in the form of a rebalancing return. In our view, the largest and most persistent active investment opportunity arises from long-horizon mean reversion (Brightman, Treussard, and Masturzo, 2014), and the systematic rebalancing of portfolio positions to stable anchor weights, which do not move in unison with stock prices, is the mechanism through which investors are able to benefit from this opportunity.24 Breaking the link between portfolio weights and stock prices protects portfolios from the approximate 200-basis-point return drag associated with the tendency of capitalization-weighted indices to overweight expensive companies (after price run-ups) and underweight inexpensive companies (after price declines) (Arnott, Hsu, and Moore, 2005).

This rebalancing mechanism can be constructed a number of ways, but Brightman (2013) showed that thoughtful design allows investors to capture the rebalancing return without incurring unnecessary risks or predictably costly portfolio turnover, which is not the case with more naïve portfolio construction approaches. For example, equally weighting index constituents creates higher allocations to smaller firms, which tend to be riskier and more expensive to trade. In the extreme, the entirety of the rebalancing premium can be dissipated by poor portfolio construction and the resulting trading costs. Li and Shepherd (2018) classified the craftsmanship of product design into four dimensions: 1) universe coverage and weighting mechanism, 2) signal definition, 3) measurement period, and 4) rebalancing frequency. Seeking the optimal tradeoff between implementation cost and strategy effectiveness in acquiring the desired exposure is a central design element governing all of the products Research Affiliates offers investors.

For over 10 years, Research Affiliates has used accounting metrics—in particular, cash flow, dividends, book value, and sales—to fundamentally weight index portfolios, turning the return drag of cap-weighted benchmarks into a return advantage for our RAFI indices, while retaining the benefits of allocating more capital to larger, and therefore easier to trade, companies. In addition, these four accounting metrics are simple, transparent, and consistent with accounting standards around the globe.25 The key smart-beta design elements characteristic of Research Affiliates’ strategies are applicable to an ESG strategy that relies on fundamental weights as the baseline for portfolio construction.

Conclusion

As investors continue to embrace ESG investing, we believe it is possible to successfully combine the responsible investing preferences of investors with the imperative of portfolio outperformance. If done thoughtfully, we believe the performance potential of ESG investing is strong. Our approach identifies ESG-aligned companies by supplementing traditional ESG metrics with two expected return drivers linked to good corporate governance—financial discipline and diversity—and investing in those companies using the market-tested principles of smart-beta portfolio construction, thus efficiently capturing the rebalancing premium available by breaking the link between portfolio weights and stock prices.

Article by Jonathan Treussard, Feifei Li, Katy Sherrerd - Research Affiliates