Mittleman Investment Management Chief Investment Officer commentary for the year ended December 31, 2017.

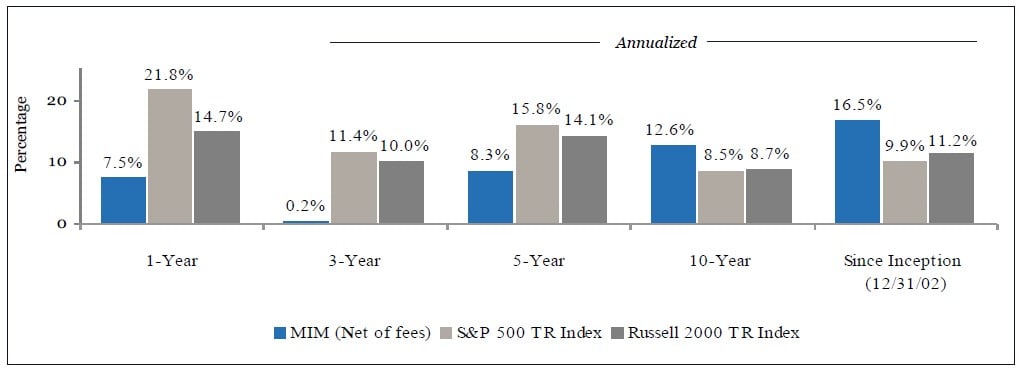

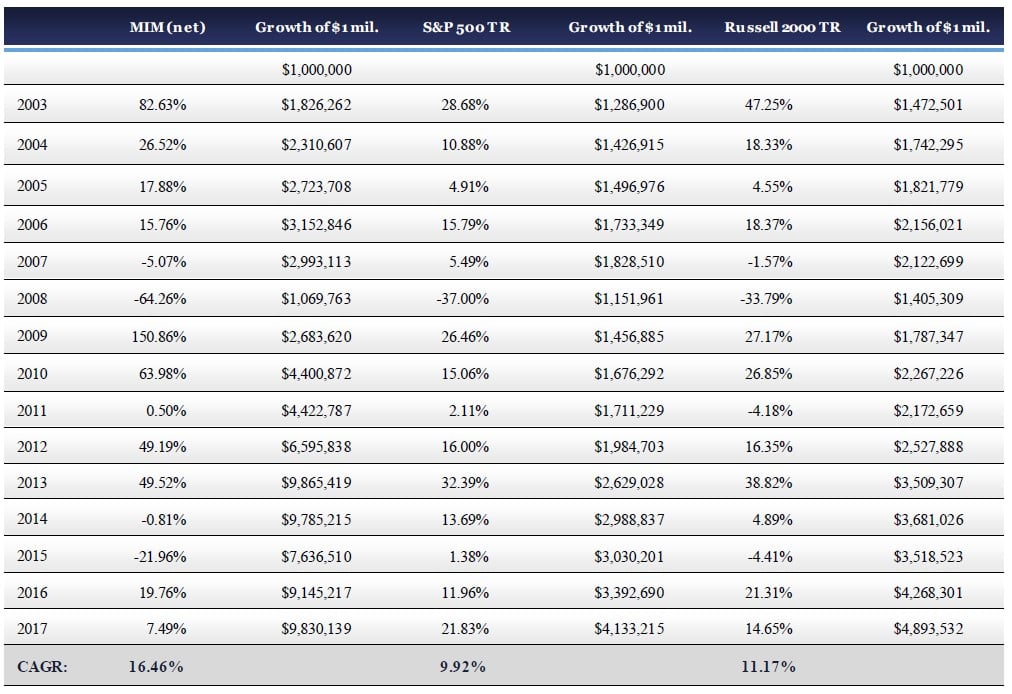

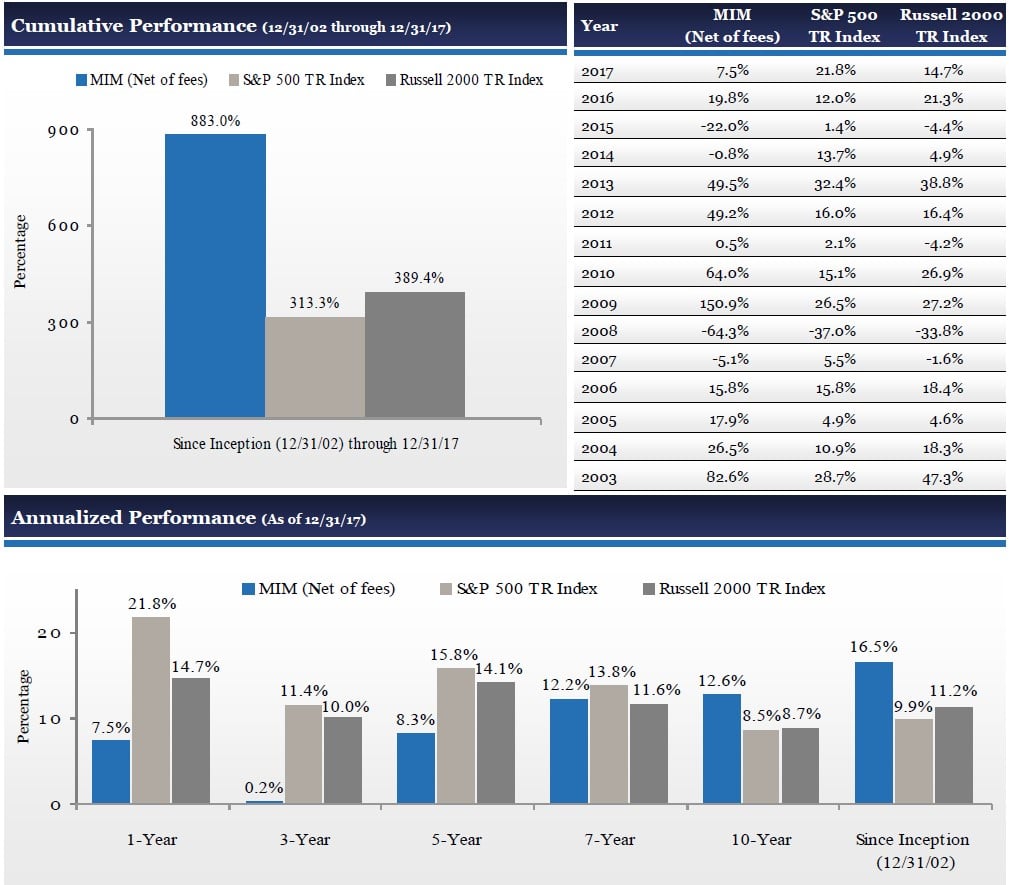

Mittleman Investment Management, LLC’s composite gained 4.4% net of fees in the fourth quarter of 2017, versus gains of 6.6% in the S&P 500 Total Return Index and 3.3% in the Russell 2000 Total Return Index. Longer-term results for our composite through 12/31/17 are presented below:

Building on strong 2016 performance, we made further progress in 2017 towards reclaiming our high water mark of August 2014, but at a frustratingly slow pace. Our composite was up 7.5% net of fees in 2017, versus a 21.8% gain in the S&P 500, and a 14.7% gain in the Russell 2000.

We have all heard how stocks labeled as “value’ in general have underperformed those categorized as “growth” stocks, both domestically and abroad, but we take little solace in that acknowledgement. We know a few value-oriented managers who out-performed significantly in 2017, so it clearly was not impossible to do so despite the adverse headwinds to the style in general. Those value-oriented managers who did out-perform in 2017 tended to own more highly cyclical businesses like automobile manufacturers, which we continue to avoid due to the significant cash burn they typically endure during recessions. In fact, consistent free cash flow generators (like most of our holdings) as a further subset of the “value” stocks group, have been unusually under-owned lately. From the Financial Times, 1-18-18, columnist John Authers:

“Growth investing may have done well last year, but over the last quarter-century it has failed miserably even to keep up with the main market indices, barring a brief illusion of great riches at the top of the dot com boom. Meanwhile, value has had a bad time of it of late. But if the various factors that generally indicate value (such as a low price/earnings or price/book, or a high dividend yield) are analysed separately, different factors of value have performed differently over time - and by far the most successful in the long term has been free cash flow yield. It is interesting (and a little worrying) that this latest rally has been the first time in a quarter of a century when the market has penalised companies for reliably throwing off a lot of free cash. With the brief exception of the dot com crash (not an encouraging precedent), companies have regularly outperformed if they have a high free cash flow yield.”

Frustrating as it is to be so out of sync with a raging bull market, we remain confident that we are where we should be. And although the schedule or timing by which our holdings will manifest renewed outperformance remains unknowable, it remains highly probable. Simply put, the popular stocks remain expensive; the unpopular stocks we own remain very cheap. At some point, this incongruity should resolve in our favor, as it has in the past.

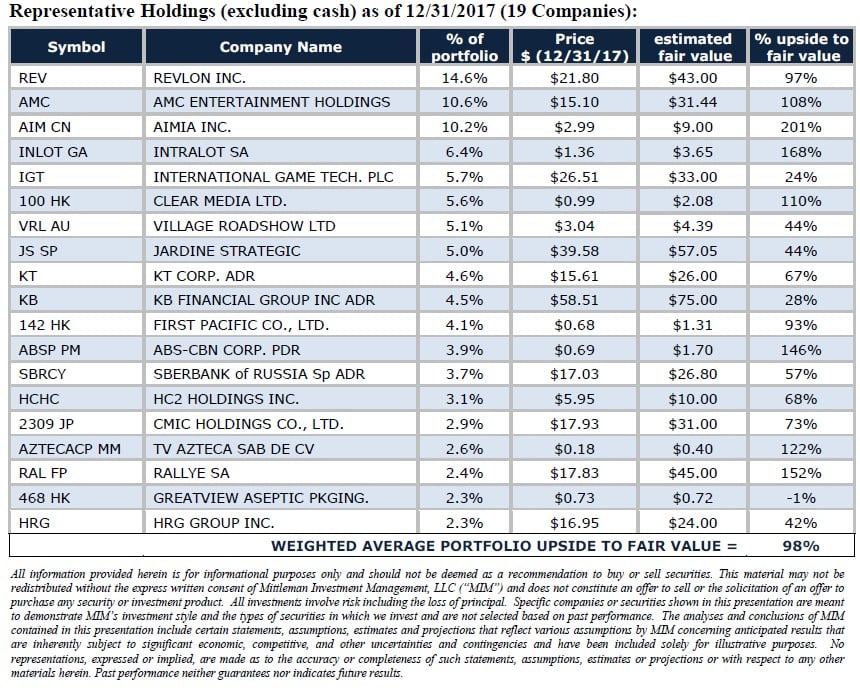

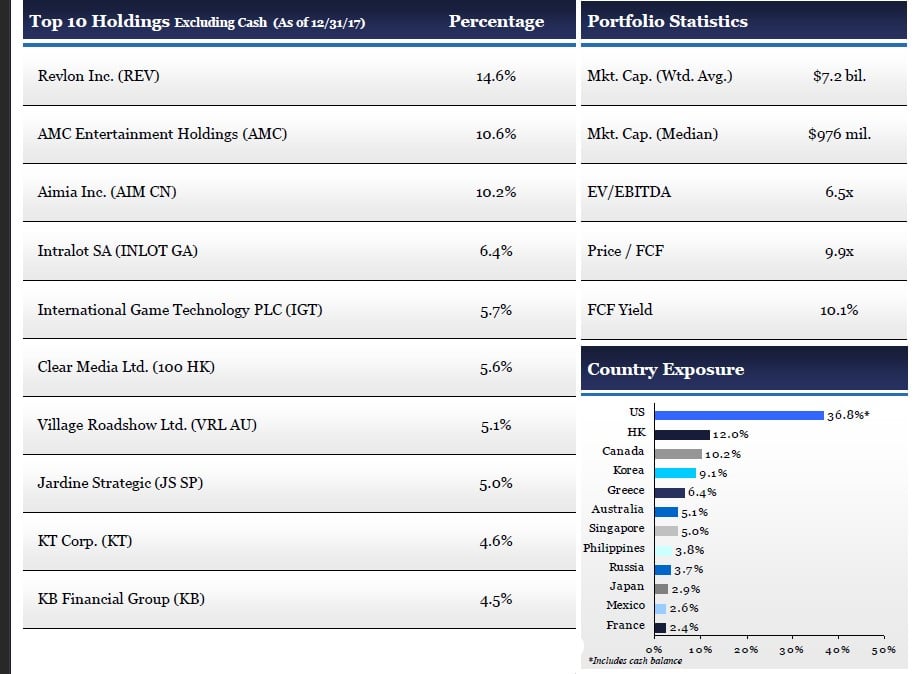

Our top three contributors to performance in 2017 were KB Financial Group (KB) +66%, Aimia Inc. (AIM CN) +62%, and Sberbank of Russia (SBRCY) +47%. Our most impactful detractors from performance were AMC Entertainment Holdings (AMC) -55%, Revlon Inc. (REV) -25%, and ABS-CBN Holdings PDR (ABSP PM) -23%.

Also sent out today was an updated version of our “What We Own, and Why” document, which provides one page summaries of the investment thesis underpinning each of our 19 holdings. For those who won’t find time to peruse that admittedly lengthy report, I think the excerpt below from the cover page is worth considering. The implied upside potential is as high as we’ve seen in our portfolio since the Great Recession. In fact, the implied upside potential was approaching this level in late 2011, just before we experienced two back to back years of 49%+ annual returns. Obviously, past performance doesn’t guarantee future results, but we find that encouraging nonetheless. To see how we arrive at those fair value appraisals, please review that WWOAW report.

But how long to wait? Michelangelo said, “Genius is eternal patience.” Goethe wrote, “Genius is knowing when to stop.” Yet George Jackson reminds us that “Patience has its limits. Take it too far, and it’s cowardice.” So, how long is long enough?

That question may have crossed the mind of an investor in Warren Buffet’s Berkshire Hathaway (BRKA) who paid $42 per share at year-end 1969 had a $38 stock at year-end 1975, six years later, while the Dow Jones Industrial Average was +36% over that same six year period. What happened next makes it obvious that extending patience there made sense. But that choice probably wasn’t so clear in December 1975.

We (me, my brothers, and the clients who became the foundation of Mittleman Brothers LLC), held Carl Icahn’s investment vehicle, Icahn Enterprises (IEP), from $9 per share in 1996 (when it was called American Real Estate Partners LP) to $8 per share in 2002, six years later. We waited just over four more years and sold the last of our shares as high as $88 in 2007.

Patience doesn’t always pay off, and obviously there has to be a well-reasoned argument to be made for the extent of it. But when applied in copious amounts to a valid and time-proven investment discipline, the outcome is usually satisfying.

Chris Mittleman

See the full PDF below.

Firm & Investment Strategy Overview

Mittleman Investment Management, LLC (“MIM”) is an SEC-registered investment adviser that provides discretionary portfolio management to institutional investors and high-net-worth individuals. MIM pursues superior returns through long-term investments in what it deems to be severely undervalued securities, while maintaining its focus on limiting risk. MIM seeks to mitigate risk, which it defines as the probability of the long-term loss of capital, by investing in businesses that are proven franchises with durable economic advantages, evidenced by a wellestablished track record of substantial free cash flow generation over complete business cycles, and only when the very low valuation at which the investment is made provides a significant margin of safety. MIM employs a concentrated, long-term investment approach, typically holding between 10 and 20 positions. Investments are made globally, with the historical average of foreign holdings representing approximately 40% of the strategy. Unconstrained by capitalization parameters, MIM gravitates towards smaller market cap companies where the firm has identified the greatest disparities between market price and its proprietary estimate of fair value. Large cap companies are also considered, but only when priced attractively enough to warrant inclusion in the strategy. MIM believes its ability to go wherever the best risk/reward ratios appear to be available, in companies small and large, domestic and international, is a distinct advantage over other investment managers which operate within a more restrictive investment universe.

See the full PDF below.