GoodHaven Fund annual letter for the year ended December 31, 2017.

To Our Fellow Shareholders:

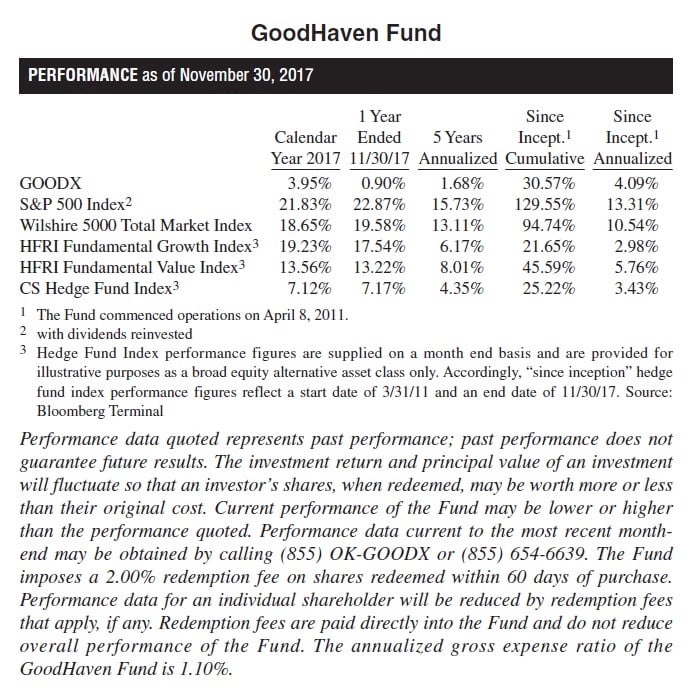

2017’s modest gains masked overall strong business results across our distinctively positioned portfolio, leaving us feeling well positioned going forward – especially compared to world where it appears that overvaluation reigns in almost all asset classes. To put the last two years’ returns into perspective, for the 24 calendar months ended December 31, 2017, the Fund gained approximately 25% compared to a gain of about 36% for the S&P 500 Index1, with most of the difference over that period attributable to our sizeable cash position compared to a zero cash position for the index. Notably, for this period, results were well above low risk, U.S. Treasury bills2 and typical hedge fund returns over the same period as measured by the HFRI Value and Growth indexes.

Similar to what we said at the beginning of that two-year period (in early 2016), we feel that this past year’s frustratingly modest gains are tomorrow’s opportunity. This year and despite positive business results, declines in our largest holdings overshadowed other upside performance in our concentrated portfolio, while a sizeable cash position, some modest hedges, and a collapse in volatility also helped to limit relative returns. These factors leave us both dissatisfied and optimistic, feeling frustrated about recent results yet positive about the Fund’s positions, especially compared to the stretched valuations of broader equity indexes. If the S&P 500 or NASDAQ 100 indexes were a single security, we would not own either today. By contrast, the Fund’s portfolio has many securities selling at a sizeable discount to our estimates of intrinsic value as well as typical index valuations. Moreover, we have cash while the indexes have none.

Imagine that a genie had appeared from a magic lamp a year ago and told us that by year end oil would rise to nearly $60 per barrel, OECD and U.S. oil inventories would decline meaningfully during the year, that WPX Energy Inc. (currently our largest investment) would grow oil production by almost 50% in 2017, monetize non-core assets, improve its balance sheet, forecast another 40% increase in 2018 oil production, and be less than one year from generating material free cash flow. With that knowledge, we would have expected the stock price of WPX to be much higher than where the year began rather than its recent quote of a double digit decline for the fiscal year.3 Instead, our energy holdings were our worst performers creating the backdrop for what we believe is an opportunity to capitalize on the inefficiency of markets. The two energy companies we own have talented managers with proven capital allocation records. While not depending on material commodity price increases, we expect a material catch-up in WPX’s stock price, which should follow business value over time. Adding to our confidence, oil supplies are down and prices are up. To paraphrase Ben Graham, in the short-run the market is a voting machine; in the long run, a weighing machine.

In 2017 gold rose about 14% and copper about 32%, yet our second largest investment, Barrick Gold also saw its stock price decline this year. Despite solid operating results, another year of significantly improved balance sheet strength, and excellent cost control, the company had to deal with two unexpected developments: a temporary halt at its Veladero mine (which was promptly resolved, followed by the mid-year sale of a one-half interest in Veladero to a leading gold producer in China); and a partial interruption in production by 63% owned Acacia Gold, a relatively high-cost African gold-miner, which appears to be on a path to resolution, though there are no guarantees.4

Despite the issues noted above, we note that Barrick’s financial strength is the best in years and the company generates significant free cash flow at current commodity prices. Moreover, Barrick has large and low-cost reserves, it has roughly $2 billion in liquidity and nearly $4 billion in borrowing capacity, corporate insiders have purchased shares at both significantly higher prices earlier this year and again just recently, and we believe the company is now positioned to play offense rather than defense.

In a concentrated portfolio, results in any brief period can be heavily influenced by the short-term stock market performance of our largest holdings – as they have been in the past. As discussed in past letters, we urge our shareholders to avoid overweighting short-term results. Both of us have decades of investing experience, we are rational and disciplined, we have some non-consensus thoughts, and we remain optimistic about what we own today. We are among the largest individual investors in the Fund and added to holdings during the year. In addition, our minority partner Markel made a material new investment into the Fund mid-year. A reduction in the corporate income tax rate to 21% will likely benefit a number of our companies although those with tax-loss carryforwards will see negative but non-cash balance sheet adjustments. On average, S&P 500 corporations have been paying a little less than a 25% effective rate, well below the old 35% statutory rate. Large international tech companies tend to have lower than average tax rates, so Alphabet Inc., for example, should not see much benefit and may actually see a modest drag. However, companies like Verizon Communications, Berkshire Hathaway, Builders FirstSource and others with mostly domestic revenue will likely see tangible benefits in terms of after-tax cash flow.

While positive, the overall impact to the S&P 500 is likely to be somewhat muted given the lower effective rate prior to the change, and indications that companies will increase capex and raise wages rather than simply pass through the entire benefit to earnings. We believe the indexes have already priced in at least some of benefit to expected overall corporate results.

We own two energy companies comprising about 14% of our portfolio – WPX Energy and Birchcliff Energy – that have demonstrated exceptional management, solid assets, and the ability to grow production at low cost. Both of these companies should have low-cost growth ahead. We believe both are materially undervalued by the current market and both are negligible percentages of index funds.

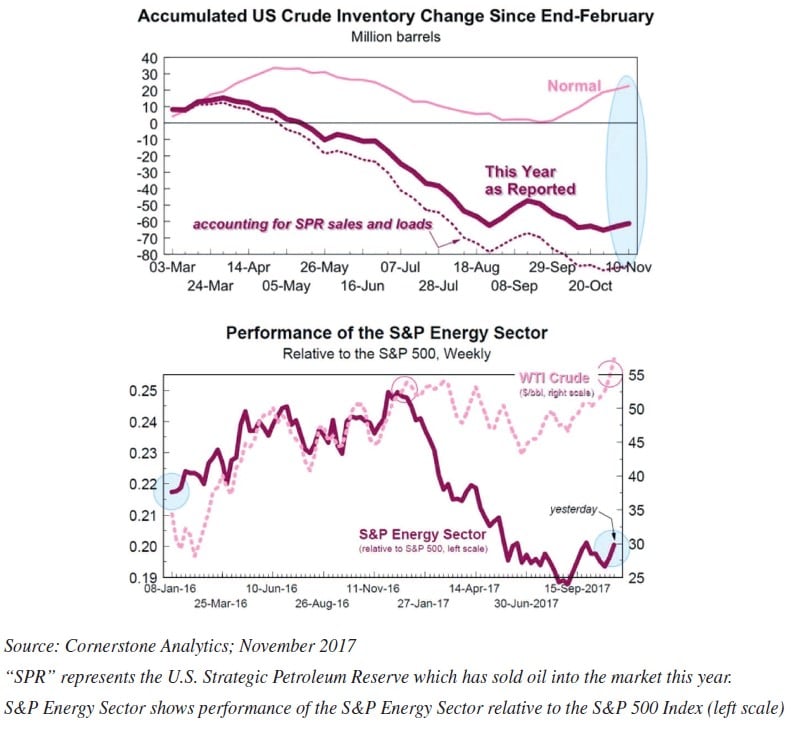

The fundamental industry backdrop continues to improve. As a percentage of the S&P 500, energy continues to bounce along forty-year lows, despite its necessity in everyday life. Yet since the oil price decline of 2014 and 2015, overall industry capital spending collapsed by at least $1 trillion and has not recovered. This is likely to constrain overall industry supply growth for years notwithstanding steady but still modest gains in hydrocarbon alternatives. Since February, both OECD and U.S. inventories have fallen sharply while the S&P energy sector underperformed the overall S&P 500 by a wide margin as shown below. In the short-run, this may simply reflect ETF cash flows, which now seem to be the tail wagging the fundamental dog.

Any further improvement in industry fundamentals should result in renewed demand for the securities of a limited number of high quality and low cost energy businesses. Alternatively, we expect corporate acquirers to start to find better value in the market than at the end of a drill bit.5 Our other commodity related holding is Barrick Gold, as discussed above. During the year, both gold and copper – the two principal commodities produced by Barrick – rose modestly in price while remaining well below the highs of five years ago. As we noted six-months ago, gold supplies have barely increased compared to a massive expansion of central bank liquidity in recent years.

Over the last two years, Chairman John Thornton has focused on restoring balance sheet strength, rebuilding the production pipeline, increasing the company’s depth of talent in management, digitizing and finding other ways to make operations more efficient, and making sure that capital is allocated efficiently and on behalf of shareholders. We strongly suggest you read his last few letters to shareholders in quarterly and annual reports – we believe he is on the way to creating an exceptional company, not just an exceptional gold miner.6

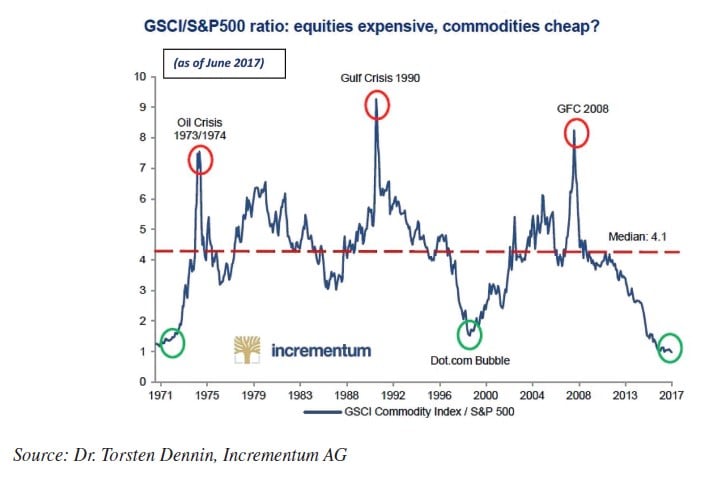

As a footnote to our investments in well-run businesses with commodity exposure, we note that commodities generally remain terribly depressed when compared to most financial assets. As the chart below suggests, the relative value spread between equities and the Goldman Sachs Commodity Index has rarely been as wide as it is now:

Our investments in commodity producers or distributors are not premised on commodity price jumps and there is no guarantee that commodities will behave as an offset to equity weakness. Nevertheless, many commodities are poorly correlated to large-cap equities historically; that is, they tend to zig when equities zag, particularly when inflation appears.

Among our other large holdings, most of which are well above our cost, we have further reasons to be optimistic. Alphabet is the only large software stock we own currently and, while no longer cheap, the company is growing fast and is more rationally priced than many of the companies with which it is often lumped together. Alphabet continues to hold and produce a prodigious amount of cash (its balance sheet shows roughly $140 per share in cash with little debt), has invested heavily in rapidly growing software for artificial intelligence, and retains huge optionality in its technology and medical venture portfolio. During the year, we scaled back our position modestly below current prices. Alphabet also approved a stock repurchase program which has yet to be implemented in a material way.

Despite large gains from our cost, HP Inc., which kept the computer and printer business after old Hewlett-Packard split into two businesses, continues to sell at about a 40% discount to the S&P 500 price-to-earnings multiple despite a rise in the stock price last year (price per share divided by earnings per share). Although cyclical and mature, the personal computer business appears to have entered an update cycle and HP is expanding into new printer markets, including the nascent, but potentially huge 3D printing business. While maintaining a sound balance sheet, the company has gained market share, and generated large free cash flows, which have been used to return billions of dollars to shareholders through buybacks and increasing dividends. At inception of our investment, we thought that if the company were stabilized, we would make good money and if it could grow (even modestly) we would earn more. Although our view was almost universally scorned then, it provided an opportunity that still continues. In this case, following the cash has proven rewarding.

Other material holdings include Spectrum Brands, Federated Investors, Verizon Communications, and Berkshire Hathaway. Shortly before this letter was written, Spectrum Brands became the subject of a merger proposal with HRG Group Inc., which owns a majority interest in Spectrum. This combination makes perfect sense at an appropriate price and conversion ratio. A merger will give Spectrum access to HRG’s material tax loss carryforwards. Spectrum is a leading consumer products company that expects to generate close to a 10% free cash flow yield in 2018.

Federated is an established money-management firm managing bond and equity funds, along with a large money-market fund business – a division that has struggled in past years due to ultra-low interest rates. As short-term rates have risen, the company has recouped money-fund fee waivers (increasing earnings) and it may start to see asset inflows if rates continue to rise – further bolstering earnings. Over time, Federated has been an excellent steward of capital, rewarding shareholders with sensible dividends and share repurchases. The company should be a beneficiary of higher interest rates.

Verizon is a company operating in a competitive oligopoly. We were attracted to Verizon by the essential nature of its services, its large customer base, a limited number of competitors, the “undisputed leader” for overall network coverage and reliability (as measured by RootMetrics), and a valuation far below that of the market as a whole. While there has been much promotional activity in the last year or two from clever marketer T-Mobile and weaker competitor Sprint, industry headwinds may be lessening as providers gear up to provide faster speeds through 5G technology. Speed is important to both cell and internet customers and 5G will give Verizon an opportunity to challenge some cable operators in providing basic Internet service as well as cell service.7

After a year or two of stagnation (which created the opportunity), we think Verizon will begin to grow again as it offers new services and is able to slowly increase prices. As a bonus, changes to net neutrality rules and a lower corporate tax rate should add materially to earnings while net worth will increase due to a large one-time benefit from a reduction of deferred tax liability. Although Verizon’s debt load is material, the company generates large cash flows, easily covers interest expense and recent capital spending, and pays a material dividend. Verizon’s shares trade at a large discount to the earnings multiple of the S&P 500.

Berkshire Hathaway has appreciated significantly since our purchase some years ago. The company today has over $90 billion in cash and investments despite having made some major purchases along the way. While Berkshire is getting closer to our estimate of fair value, we believe the company to be a very-well run business with clever capital allocators. Although Warren Buffett is now 87 years young, he has recruited a large stable of demonstrated talent both on the investment side as well as within the operating businesses. Using its strong cash flow and existing cash hoard to make sensible deals, Berkshire should continue to outperform many other large companies over a multi-year period.

During the year, we also added some new names. Unfortunately, two of them ran up fairly quickly and we erred by not moving faster to make larger investments. Earlier in the year, we bought Builders FirstSource, a supplier to the housing construction markets that has been consolidating the wholesale supplier market. The company’s earnings have been better than expected, acquisition debt has been paid down faster than expected, and the stock price has moved up. Housing markets remain relatively tight, as inventories are lean, mortgage rates still relatively low, and single family construction remains well below pre-crisis averages.

Late in the year, we added a position in Macy’s amid widespread general fear about retailers and a collapse in that company’s stock price. Although recent earnings have been pressured and we recognize the industry is changing, the company generates significant free cash flow, has a smaller and rapidly growing cosmetics division, has growing on-line sales, and is focused on expanding on-line talent. Moreover, the company owns extensive real estate assets that are not mallbased and which are worth a large portion of the company’s public market value based on recent comparable transactions.8

Unfortunately, the stock spiked up after reported Q3 results and we own only a modest position. However, with earnings expected to approach $3 per share, a significant dividend yield, some signs of stabilization, and efforts to monetize unmortgaged property, we believe a share price in the high teens represented opportunity. In any industry where competitive dynamics are changing, there is both danger and opportunity. Accordingly, we expect to react faster and be quick to change our mind if the facts on the ground change.

We also recently made an initial purchase of Oaktree Capital, a money manager with a wonderful long-term record that specializes in distressed investing. We believe Oaktree is worth more than its current market price and could be worth a lot more, particularly as its business would seem inversely correlated to elevated equity indexes.9 Managed by founders Howard Marks, Bruce Karsh and CEO Jay Wintrob, Oaktree has created tremendous value for its owners and clients over time, has a history of paying out cash earnings, and has a franchise that should be able to grow.

During the year, we sold or eliminated some smaller positions and scaled back some others. These included, but were not limited to, our disposition of Staples Inc., which was taken private at a price that yielded us just a modest profit; the buyer got a bargain. Despite having eliminated our remaining position in Walter Investment Management earlier in the year, it still was a drag on performance for the period. At mid-year, we disclosed a position in New York REIT, a real estate investment trust that had approved a plan of liquidation. We bought after its stock price fell sharply in response to a lower estimate of realizable value by new management. Based on a property by property analysis, we expected that the liquidation proceeds would offer reasonable return to the newly lowered stock price with little or no correlation to broader indexes. However, after the company sold two properties for somewhat less than our original estimates, we sold the entire position at a modest loss amounting to less than 1/10 of 1% of the portfolio. In this case, we believe that capable CEO Wendy Silverstein did all she could to cleverly maximize property value, however, it appears that the commercial market in New York has weakened perceptibly since the liquidation was announced.

See the full PDF below.