Forge First Asset Management commentary for the month ended July 31, 2018.

Q2 hedge fund letters, conference, scoops etc

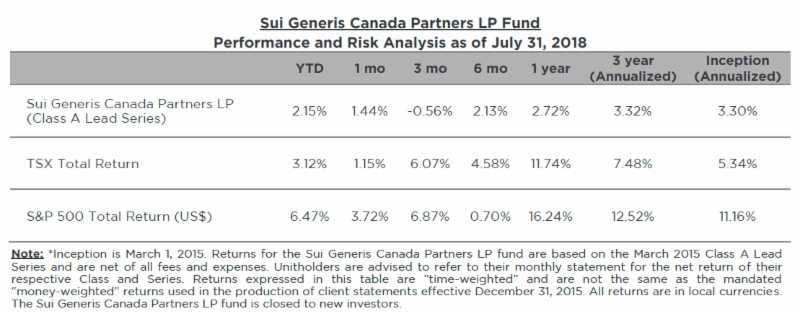

The Sui Generis Canada Partners LP fund was up 1.44% for the Class A Lead Series during July 2018, resulting in a year-to-date net return of 2.15% and since inception (March 1, 2015) cumulative net return of 11.75% (3.30% annualized).

July 2018 Commentary

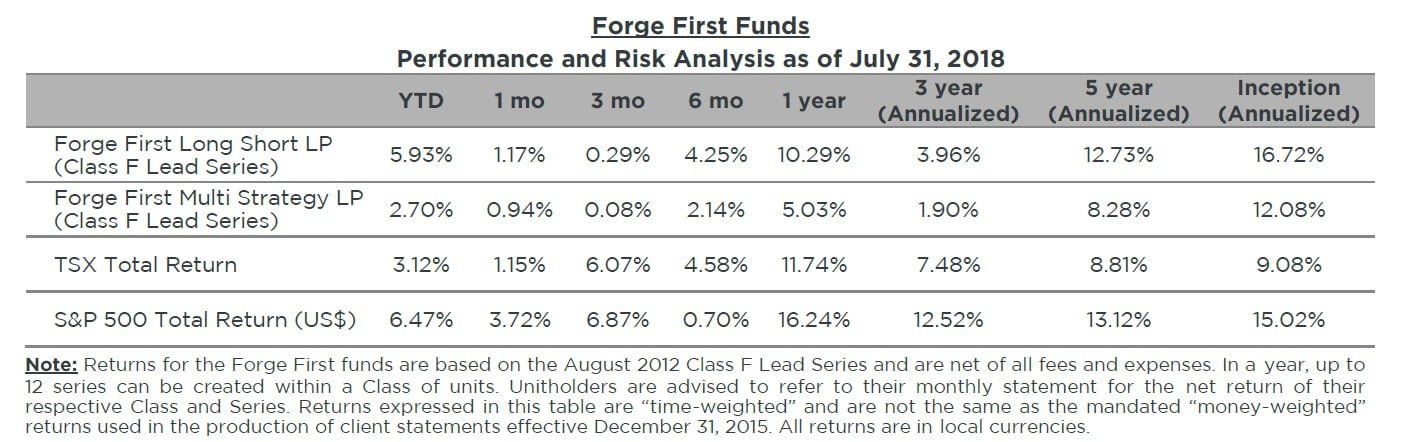

July saw a resumption of positive returns for Forge First Asset Management Inc. after an ever so brief hiatus. Given our strong focus on free cash flow and continuous bottom up analysis, we typically find that earnings season treats us reasonably well. It’s a quarterly reminder to the investing world that the companies we own have strong underlying fundamentals while those that we are short may be overvalued for any number of reasons; but again the presentation of financial statements leaves little room to hide. We were particularly encouraged by the broad based contributions to July’s performance, with the top ten made up of energy E&P longs (3) and shorts (1), technology longs (2), a REIT, a financial, an industrial and an energy marketer that seemed left for dead less than a year ago. Concerning the last stock in that list, we thought mid-year might be a decent time to lay out what has been our thesis for some time on one of our favourite names.

Parkland Fuel Corp (TSX: PKI) has been amongst the fund’s largest positions for the duration of 2018 and continues to be a core position today. To the uninitiated, Parkland is Canada’s largest independent marketer of fuel and petroleum products, and a leading convenience store operator, with 1,849 total dealer and company-owned retail fuel locations across its network. They operate branded retail sites that many consumers are familiar with such as Ultramar, Esso, Chevron and others. In 2017, Parkland also acquired a 55,000 barrel per day refinery based in Burnaby, British Columbia. At the time this was the source of great consternation amongst the investing community, but an opportunity for those who could see through the noise. As a result, the funds began to accumulate shares of Parkland when we believed the company was poised to create substantial value for shareholders and was mispriced and clearly misunderstood in the market. We continue to believe this is the case today. Our position in Parkland has largely been predicated on the following 4-point thesis:

- Long term earnings and free cash compounder: In 2017, Parkland completed two significant acquisitions – CST Brand’s Canadian fuel marketing assets, and Chevron’s BC-based assets. At the time of acquisition, PKI indicated that adjusted distributable cash flow per share (a reasonable proxy for free cash flow) would increase from $1.60 in 2016 to $2.80 following full integration of the acquired assets and related synergy capture. This represented an increase of 75%, yet Parkland’s shares finished 2017 ~4% below year-end 2016 levels. We believed the value creation would be substantial, and went to work to investigate the company’s claims. Our work not only supported the company’s guidance, but found near and medium-term opportunities for upside. For example, the company’s guide utilized overly conservative ten-year low margin estimates in deriving the earnings power of the Burnaby refinery and incorporated very little growth in the base business. Today, we believe Parkland continues to have many organic and inorganic opportunities to drive long-term compounded growth in earnings and free cash flow. With the success PKI has demonstrated following the two acquisitions in 2017, we believe investors are largely overlooking the potential to acquire over the next 3-5 years.

- Beat and raise story: At the beginning of 2018, analysts expected PKI to generate ~$565 million of 2018 EBITDA. Through our due diligence on their existing legacy network, acquired retail stores, and analysis on realistic refinery margins, we concluded that EBITDA would exceed consensus expectations by >20%. Meaning without any improvement in the market’s valuation, Parkland shares were undervalued based on earnings upside alone. The company has exceeded our expectations, and recently raised 2018 EBITDA guidance to $775 million. While further “beats” will be less prominent, we still see earnings upside.

- Investor Sentiment: It is no secret that electric vehicle (EV) adoption is negative for retail fuel consumption. The fear of EV’s on long-term fuel consumption led many investors to believe that retail fuel marketers we’re declining businesses. We believed this fear was apparent in Parkland’s share price in 2017, meaning the stock was overlooked and under-owned. Our work around EV adoption and its effect on fuel volume consumption suggested that the fear was overblown. While EV’s are negative, fuel marketers have the ability to consolidate a highly fragmented industry while realizing substantial supply-related synergies in fuel and merchandise products, leading to attractive growth and return on investment opportunities – even against a declining volume backdrop.

- Valuation: While Parkland’s shares have appreciated year-to-date, we don’t believe the valuation has changed dramatically from when we initiated the position due to improved performance relative to our expectations and increased synergy capture. We believe PKI shares are trading at an all-in 9% free cash flow (FCF) yield, which we view as attractive given the forecasted mid-teens FCF growth over the near-term. We would argue this is mispriced on an absolute basis and relative to peers.

Again, we don’t typically spend our commentary on single stock deep-dives, but some stories just beg to be told, and we believe that in spite of its recent strength, PKI is still well worth owning.

Please do not hesitate to reach out to us if you wish to learn more about how our strategies can complement and lower volatility in your investment portfolio. As always, we welcome any feedback, and for more information please visit our website at www.forgefirst.com.

Thank you,

Daniel Lloyd

Portfolio Manager

Andrew McCreath, CFA

President and CEO

{kind=link}