Key Takeaways

- Investors will be closely watching this week’s CPI release and the impact it could have on interest rates and stocks.

- The good news for investors in love is that low overall inflation again carried over to common Valentine’s Day gifts in 2017, with prices rising at or below the average pace.

- Relatively costly items such as trips and jewelry saw smaller price gains than the more traditional gifts like a night at home or on the town.

Inflation and economic growth are key drivers of long-term rates, and rising rates can lead to higher borrowing costs for individuals and businesses, potentially impacting consumer spending and profit margins for businesses. Given the recent market volatility, the January Consumer Price Index (CPI) report, which will be released on Wednesday, February 14, could become a focal point for markets. Consensus forecasts expect that both headline and core CPI (which excludes volatile food and energy prices) may slow down on a year-over-year basis to 1.9% and 1.7%, respectively, but given the focus on rising rates and their potential impact for equity prices, any upside surprise in CPI could lead to additional volatility.

As a reminder to those of us who may have forgotten, February 14 is also an important day for another reason—it’s Valentine’s Day. Inflation’s impact on stock market performance is certainly an important topic, and markets will indeed scrutinize the January report to see what it means for stocks moving forward (we will post a blog about the CPI release on lplresearch.com on Wednesday as well). However, the fact that CPI will be released on one of the major gift-buying holidays of the year also provides a good opportunity to see how inflation can impact everyday life.

Recent Market Volatility

Rising inflation expectations and a corresponding rise in long-term interest rates have been a focal point for markets over the past week, and have been identified as at least one of the causes behind recent stock market weakness. Worries about the potential for rising wages to lead to increased inflation and a more aggressive Federal Reserve (Fed) caused interest rates to move higher. This, along with a spike in the VIX Volatility Index (commonly viewed as the market’s fear gauge), led to an unwinding of trades that had bet on a continuation of last year’s low volatility theme, resulting in the S&P 500 Index falling into correction territory (a drop of 10% or more from all-time highs) for the first time in two years. We discuss this chain of events, as well as where we think markets may go next, in this week’s Weekly Market Commentary, “Correction Perspectives”.

The Valentine’s Day Index

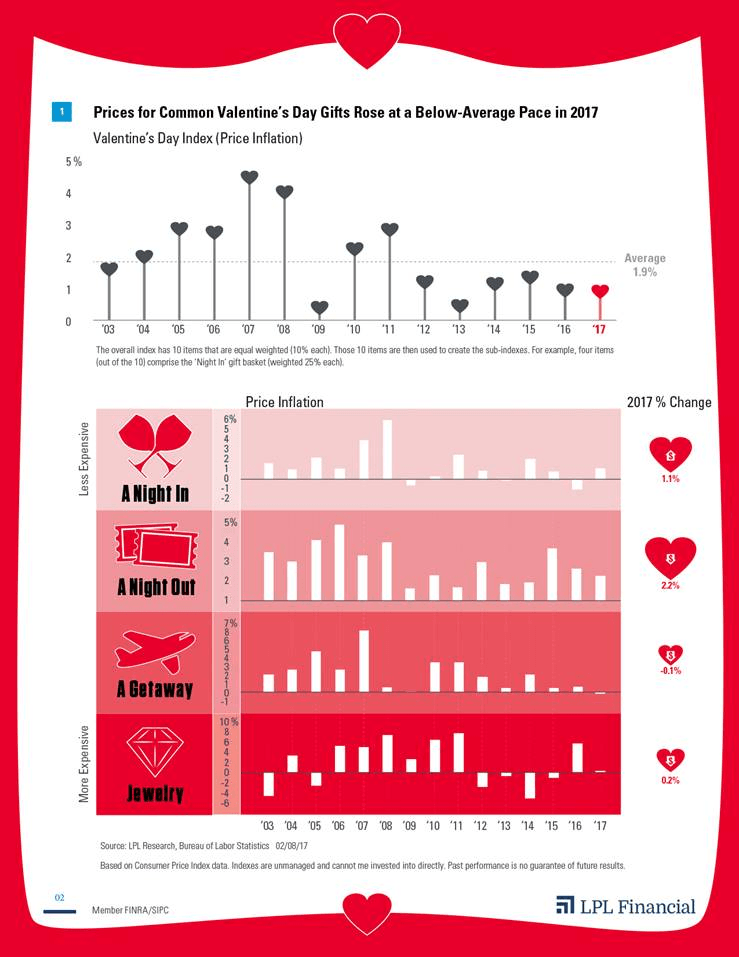

LPL Research’s annual Valentine’s Day Index tracks the cost of typical Valentine’s Day gift categories over time using CPI data. To get a clearer idea of price increases in individual gifts, we have separated the index into four common gift categories. Grouping all items together into the Valentine’s Day Index [Figure 1] shows that Valentine’s Day inflation increased by 0.9% over the previous year, slower than the 1.9% average for the previous 15 years, but in line with the 2016 increase. The rise was also slower than December 2017 readings for headline (2.1%) and core (1.8%) CPI.

A Night In

A night at home—including candy, flowers, a home-cooked meal, and a bottle of wine or champagne—continues to be a good bet for value conscious consumers. However, the cost did increase by 1.1% in 2017. This is below the 1.4% average gain over the previous 15 years, but an increase from the 1.1% fall in prices in 2016.

A Night Out

The cost of dinner and a movie, a Valentine’s Day tradition for some, increased by 2.2% this year. Though this category saw the largest price increase of any of the four gift ideas this year, it was below its average increase of 3.0% over the previous 15 years, and also slightly lower than its gain of 2.6% in last year’s index. This gift idea includes dinner at a restaurant, movie tickets, and child care. The cost of child care has increased by 82% since 2001, the fastest increase over that time period of any item in the Valentine’s Day Index, though it took a breather in 2017, increasing by just 1.8%, compared with 2.3% for a meal at a full-service restaurant and 2.7% for movie tickets.

A Getaway

A trip may offer a decent value for those looking for a memorable Valentine’s Day experience in 2018. Though not the lowest cost gift in our index, it was the only one that experienced a drop in price, with the overall cost of the underlying items—dining out, lodging, and airline fares—decreasing by 0.1%. The decrease was driven by airline fares falling 4.0% (following a 4.7% drop in 2016), and hotel prices that that rose only 0.3% (versus 3.3% in 2016).

Jewelry

Jewelry saw the largest price gain in the 2016 Valentine’s Day Index (5.8%), but prices increased by just 0.2% for 2017, the second lowest rate of inflation of the four gift categories. Sticker shock could still be an issue for those choosing this gift in 2018, but shoppers can take at least some solace in jewelry becoming a better relative bargain.

Conclusion

Inflation has been, and could continue to be in the news over the near term, as markets try to determine if it is in fact moving higher, and what impact it may have on the Fed, and ultimately equity and fixed income markets. With the correction in stocks fresh in investors’ minds, the latest inflation reading from January’s CPI report, which will be released on Valentine’s Day, may be carefully scrutinized, and an upside surprise could lead to more market volatility in the short term. Despite the recent volatility in markets, we continue to believe that underlying fundamentals remain strong, and maintain our 2018 targets of gross domestic product growth of +3.0%, an S&P 500 fair value estimate of 2,850–2,900, and that the 10-year Treasury yield will end the year in the 2.75%–3.25% range.

In addition to market impacts, it can also be instructive to look at the impact of inflation on our individual lives. LPL Research’s Valentine’s Day Index can help last-minute shoppers (including perhaps a few here at LPL Research) determine which gift idea represents the best value this year. Big spenders may see more value in 2018, with the cost of a trip falling slightly, and jewelry prices increasing only marginally. A night at home and out on the town saw slightly larger increases, but both remained well below historic averages. The key takeaway for investors is that the higher inflation expectations that started in the second half of 2017 have yet to translate to significant actual inflation (in Valentine’s Day gifts or more broadly), though markets will be closely watching Wednesday’s CPI report to see if this trend continues.

As noted in Outlook 2018: Return of the Business Cycle: LPL Research projects real gross domestic product (GDP) growth of around 2.5% in 2018. This is in line with historical mid-cycle growth of the last 50 years. Economic growth is affected by changes to inputs such as business and consumer spending, housing, net exports, capital investments, and government spending. LPL Research’s S&P 500 Index total return forecast of 8 – 10% (including dividends), is supported by a largely stable price-to-earnings ratio (PE) of 19 and LPL Research’s earnings growth forecast of 8 – 10%. Earnings gains are supported by LPL Research’s expectations of better economic growth, with potential added benefit from lower corporate tax rates. LPL Research also expects the 10-year Treasury yield to end 2018 in the 2.75 – 3.25% range, based on its expectations for a modest pickup in growth and inflation.

Article by LPL Financial