Cost control is key to long-term investment success, but trading costs associated with portfolio rebalances add up over time, decreasing returns overall. This slippage is hard to measure, because it is never explicitly stated in annual reports. Yet market impact can be reconstructed, if you know where to look.

This article presents a deep dive into the forensic evidence of that slippage, generating a market impact estimate for a reconstitution trade in a sample ETF. A follow-up piece will offer a cost/benefit analysis that highlights winners and losers from these rebalance trades.

Complex indexes require frequent reconstitution and rebalancing in order to maintain their desired exposure. These updates take place at predictable intervals, as rebalance schedules are published in index methodology documents. ETF portfolio managers, charged with tracking these indexes, must shift their portfolios on the rebalance day in order to stick to their mandate.

These massive trades have attracted the attention of market makers, who stand to benefit from the trading activity. The evidence starts with massive fund flows that surround rebalance activity in many ETFs with complex indexes.

Portfolio data, fund flows, and the consolidated exchange tape round out the forensic toolset for assessing these hidden costs.

REGL Reconstitution Forensics

ProShares S&P MidCap 400 Dividend Aristocrats ETF (REGL-US) had an index reconstitution on January 31, 2018. REGL’s small portfolio size (52 stocks), proportionally large “heartbeat flows,” overall low level of creation/redemption activity, and low average portfolio security volume make it possible to identify many of the associated trades. Of course, REGL is but one of many ETFs that benefits from these heartbeat flows and the ability to redeem appreciated securities in-kind.

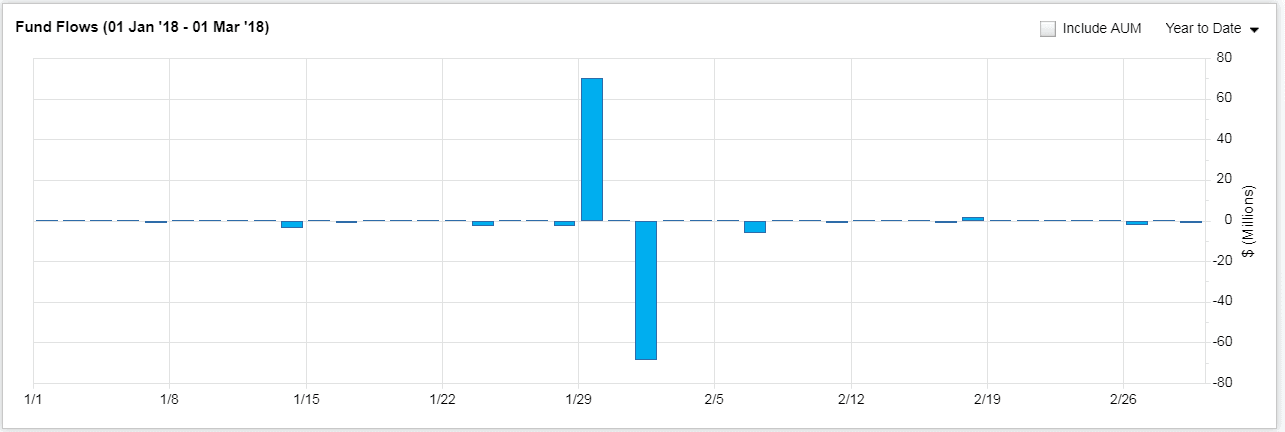

REGL’s underlying index, the S&P MidCap 400 Dividend Aristocrats reconstitutes annually after the close of the last business day of January. REGL’s portfolio must follow suit. The process begins a few days ahead of time, on January 29, with a massive inflow, which sets up an equally large outflow on January 31.

Here’s a close-up of January and February flows activity.

REGL gained and lost 1,250,000 shares during the final three days of January. That’s about 15.9% of starting AUM. In dollar terms, that’s $69.45 million in and $68.44 million out.

Portfolio data shows the inflows clearly. Every one of REGL’s 44 securities increased in share count by 15.91% between Friday, January 26 and Monday, January 29 in each of REGL’s 44 equity positions.

| Ticker | Share Count | Percent Change | |

| 1/26/2018 | 1/29/2018 | ||

| ATO | 110,968 | 128,624 | 15.91% |

| BRO | 193,684 | 224,500 | 15.91% |

| CDK | 142,969 | 165,719 | 15.91% |

The January 29 portfolio changes and flows match in dollars, as well as percent. These portfolio share count increases were worth $69.47 million at the day’s closing price, matching the $69.45 million net inflows number almost exactly.

January 31 turned out to be a big turnover day for REGL. Comparing holdings between January 30 and 31, we find that REGL added eight new positions, increased the size of one existing position, and trimmed 43 positions. These trades netted out as a $68.44 million sale, including some balancing cash.

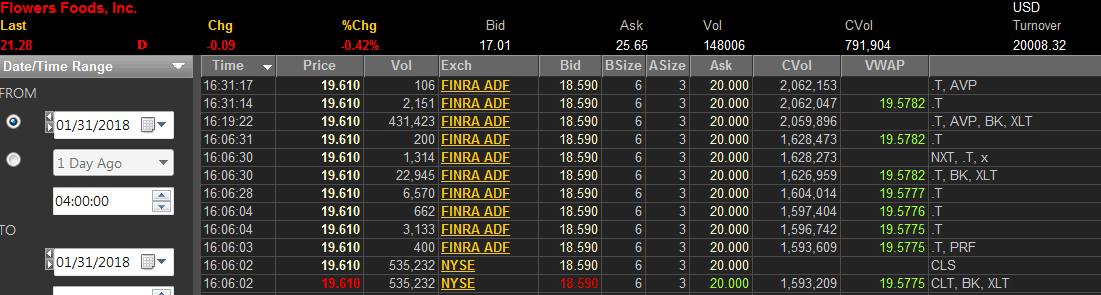

Two examples – one buy in Flowers Foods (FLO-US) and one sell of Nordson Corporation (NDSN-US) – offer a window into the mechanics and profitability of these trades.

Buying the New Positions

REGL initiated a position of 431,423 shares in Flowers Foods on January 31. FLO’s composite tape shows a trade of 431,423 FLO shares reported at 4:19:22 PM, using form T, which indicates a late report. It appears as a block trade (BK), reported via the FINRA alternative display facility. FINRA’s ADF is used for reporting transactions from dark pools.

The price was equal to the day’s closing price of 19.610, as you can see by looking at the 535,232 share print from the NYSE, marked “CLS” on in the right-hand column.

There’s additional information about this trade in the far right-hand column. The code “AVP” tells us that this was reported as an average price trade. According to FINRA’s Trade Reporting FAQ (A404.1), AVP flags the customer leg of an order that a dealer worked during the trading day. The broker/dealer selling to the REGL PM likely bought shares throughout the trading day and then sold them on the close, at a mark-up.

All eight new additions and the one position increase in REGL’s portfolio for January 31 are reflected on the tape the same way. All have time stamps at 16:19:22, with block trade and AVP flags and with prices that match the day’s official closing price.

These customer trade flags strongly suggest that REGL’s portfolio managers worked with a broker/dealer to execute the buy list. The fact that the trades were priced at the day’s closing price supports this assertion, as we know the portfolio managers want to minimize tracking error.

The Sell Side

Now to confirm sales and redemptions.

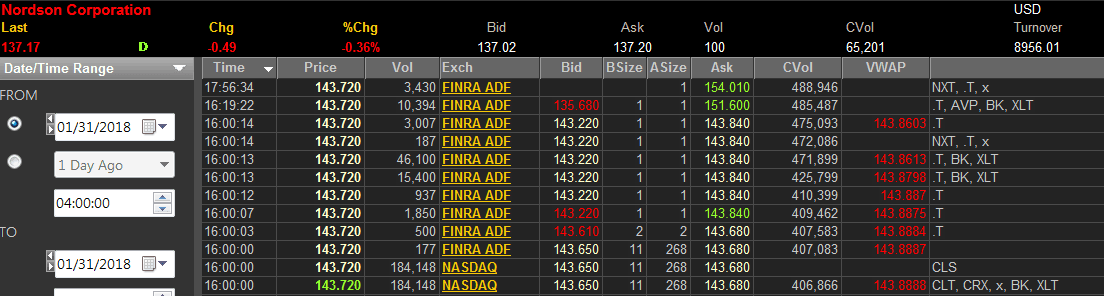

On January 31, REGL trimmed its position in Nordson by 31,644 shares. According to REGL’s daily holdings, the ETF held 88,353 shares of NDSN on January 30, but only 56,709 shares on January 31. We are looking for a trade of 31,644 shares.

But no 31,644 block of NDSN traded on January 31.

At 16:19:22, there was a FINRA ADF trade for 10,394 shares of NDSN, reported with codes T and AVP, same as we saw with FLO. This was a late trade, average price trade, just like FINRA specifies for customer legs of a dealer’s worked order. The price was equal to the day’s official closing price, like the buys we just saw.

It looked like this:

The 10,394 trade was almost certainly executed by broker/dealers, as one of the trades on the PM’s sale list. Yet this trade accounted for only about one-third of the position change. We must still account for the other 21,250 shares.

But again, there was no print of 21,250 shares, so we must look harder.

Reverse Engineering the Redemption Basket

REGL’s portfolio managers likely split the position reductions between the sale list and the redemption basket, placing the lowest-basis stocks in the redemption basket, and perhaps realizing capital losses by selling high-basis stocks outright. The 21,250 shares could easily have gone in the redemption basket.

While we cannot find the 21,250 share trade on the tape, we can account for it nonetheless.

The total value of all position reductions should equal the broker/dealer net sales plus total outflows. If so, then the shares not traded in dark pools at 16:19:22 PM constitute the redemption basket.

We can see trades in all 43 REGL stocks with January 31 share reductions with timestamps at 16:19:22 on January 31. All had FINRA ADF trades with the form T and AVP flags, same as the buys. The total dollar volume traded was $67.23 million.

The total value of positions trimmed in REGL on January 31 was $135.18 million. $135.42 million - $67.23 million = $68.19 million. Add back the cash and that number becomes $68.44 million. $68.44 million is the value of REGL’s outflows on January 31.

Thus we can confirm that the balance of position reductions not sold via broker/dealers went in the redemption basket. We can determine each position’s split between broker/dealer and basket trades by subtracting the size of the FINRA ADF trade from the overall position reduction.

Market Maker Activity

During regular trading hours (excluding the opening and closing auctions), the median NDSN trade was a mere 50 shares. The largest non-customer trade was only 2,567 shares. The 21,250 must be scattered among the tiny trades that comprise the bulk of NDSN’s activity. We will not be able to discern which of the tiny trades to attribute to the market maker. The best we can do is to assume that the market maker traded at approximately the day’s volume-weighted average price, also known as the VWAP.

Adding it All Up

Now that we have the prices and quantities for all the rebalance trades, we can figure out how each of the players—the PM, the broker/dealer, and the market maker—benefits.

Our example positions, FLO and NDSN, help illustrate the situation.

The portfolio managers bought FLO from the broker/dealer paying the closing price of $19.61. VWAP—our assumed B/D execution price—in FLO was $19.57823. Profit equals $0.031766 per share, or $13,704.58 for the trade.

The PMs sold NDSN to the market maker at $143.72. NDSN’s VWAP was $143.8603. That’s a $0.14029 per share profit, totaling $4,439.37.

The buy and sell list trades were profitable. The difference between selling at VWAP and buying the shares back at the closing price, multiplied by the number of shares traded, summed up over each position, comes to $96,700.21 for the sell list and $44,866.01 on the purchases, based on buying at VWAP and selling at the closing price.

The market maker did well, too. The difference between selling short at VWAP and buying back shares on the close, for the 41 positions in the redemption process, was $121,553.04.

All told, the broker/dealer and the market maker’s net profit came to $263,119.26, or 0.06% of the AUM on January 31.

For most fund-holders in taxable accounts, the capital gains avoidance is almost certainly worth more than the slippage from adding market makers and broker/dealers to the mix. The capital gains could have run in the hundreds of basis points, while the capital markets slippage from the redemption trade amounted to only 0.03% of the January 26 AUM.

The broker/dealer gains cost another 0.03% of AUM. It’s entirely possible that this is a reasonable price to pay for removing execution risk and for keeping tracking tight.

Perhaps the biggest take-away from this exploration is that rebalances are not free. ETF strategies that require frequent or significant rebalancing or reconstituting bring with them the risk that the potential outperformance of the strategies gets eaten up by front-running on the trading floor. If the 0.06% slippage from REGL’s January reconstitution recurs in the quarterly rebalances, REGL would earn approximately 0.24% less than it would if index tracking and tax avoidance were not at issue. That’s a real consideration in a world where even 0.10% of alpha is increasingly hard to come by.

Article by Elisabeth Kashner, FactSet