Whitney Tilson’s email to investors discussing Tesla Inc (NASDAQ:TSLA)’s possible capital raise; The best Model 3 review to date; Bernstein: TSLA: Egad, those “other” regulatory credits… Fundamental Q1 automotive gross margins worse than first believed; Tesla getting into auto insurance; Tesla getting into the auto insurance biz???.

Possible Tesla capital raise

From a friend who tracks the flights of Musk’s jet:

Q1 hedge fund letters, conference, scoops etc

Landed just after Midnight:

GRACIAS! Tracking Update: After only one day in Chicago, back to the Left Coast. Departed MDW 10:00 PM PDT last night, arrived OAK 12:35 AM. $tslaQ $TSLA

— Machine Planet (@Paul91701736) April 29, 2019

All the signs are there that they are cobbling together some sort of a capital raise. Elon's plane was in town for a few hours on Friday evening, and then again amazingly enough on Saturday evening again. Who else is in the office on those times? No normal workers, that's for sure.

One does suspect that the company has found "an angel" who is willing to do some sort of a PIPE (call it strategic or not). Its impact on the market would clearly depend on the terms.

If it's a "clean" or "plain vanilla" stock issuance at or not materially below the prevailing market price, then there is the potential for it to be a positive event. For every $400 million raised, it would postpone a bankruptcy scenario by approximately one quarter. I assume that could take the stock up a few percent. Let's say 2 million shares at $250, those 2 million shares are a tiny fraction of the short interest.

However, if a raise has some preferential hair or equivalent on it, then it gets murkier. It may not be positive for the stock at that point. Depending on the terms, even lots of downside.

I really can't handicap these probabilities, but it does seem like all the signs are in the air that Tesla is trying to get something done on this front, and I assume the 10-Q was the last official hurdle to negotiate the final terms with the other parties. I imagine we will know very soon, possibly within days, if this does happen.

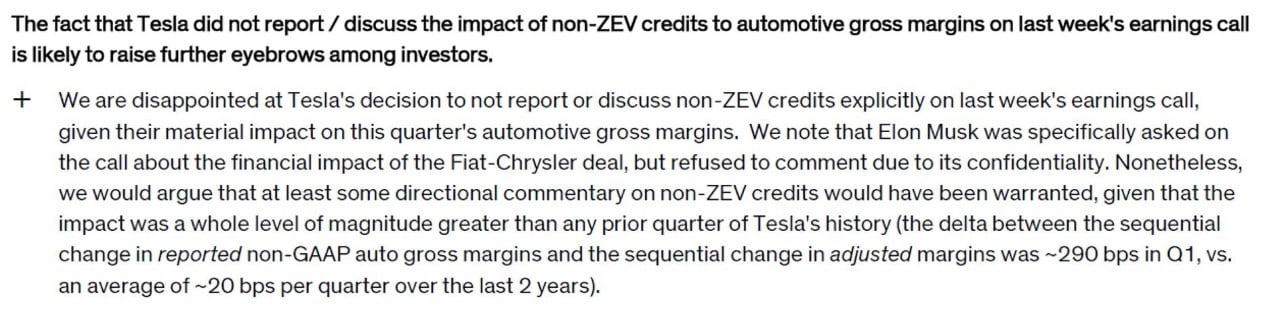

Bernstein: TSLA: Egad, those "other" regulatory credits... Fundamental Q1 automotive gross margins worse than first believed

I don’t think much of most Wall St. analysts, but Bernstein’s Toni Sacconaghi, whom I had the pleasure of meeting a couple of years ago when we were both on Tesla’s Gigafactory tour, is an exception. He does excellent work, as evidenced by today’s report on Tesla’s 10-Q, in which he reveals the extent and importance of Tesla’s deceit in hiding the non-ZEV credits.

You rarely see a Wall St. analyst so explicitly call management absolute total f**king liars as Toni does here:

The best Model 3 review to date

From a friend:

I know you have probably viewed and read more Model 3 reviews than you had ever planned, and are probably sick of them by now. I sure am.

However, I would like to call your attention to what I am certain is the very best one yet, and it's from Alex Dykes, who is generally regarded as one of the top 10 or so YouTube reviewers. I rank him as my #1 to-go car review channel, because it focuses on information and comparisons with competitors. Nobody else has his extreme focus on comparisons. Alex is also a walking encyclopedia of knowledge. Yes, almost all automotive journalists are experts of some sort, but Alex is in a different league altogether. I didn't think there was anything more I could learn from a Model 3 review. Alex gave me a laundry list of new knowledge. I can guarantee you will learn at least 20-30 new things about the Model 3, that you didn't know before.

It is a two-part review, starting with this one:

In this first part, Alex correctly identifies Tesla's self-claimed self-driving system as a lower level of autonomy compared to system in the Cadillac. You will hear this shortly after the 10:45 mark.

The second part is this:

It has comparisons to Hyundai Kona EV, BMW 3-series sedan, Honda Accord and Toyota Camry. Alex says that some of those comparisons make very little sense, but the reasoning behind them is that those are comparisons that his readers (viewers) requested -- so that alone can give you some insight into the consumer's mind.

As with at least four other journalists in the business, Alex bought this Tesla for himself. It is not a temporary review car provided by the manufacturer, as is customary. Unlike the other journalists, Alex also bought a version of the Model 3 that is as close to the base $35,000 as possible. The only option was $1,000 for the (blue) paint job, and the mandatory $1,200 delivery fee, for a total of $37,200.

Tesla getting into auto insurance -- I stand corrected

I stand corrected. Here are comments from two friends:

1) He’s been working on this for awhile.

The cars have high accident frequency (people enjoy the acceleration to excess) and high severity (there are no spare parts and they are expensive to fix and the service is so bad, that cars are often in the shop for months for small problems — and rental cars are needed). So, insurance companies are charging so much that it increases the cost of ownership. (Tesla advertises gas savings, but not higher insurance costs.)

Typical Musk: rather than fix the repair problem, he will take over the problem.

They have made a number of filings and have a “fronting company” (State National, part of Markel).

This will launch...and Tesla will probably undercharge...but more car sales now is better than some insurance losses down the line in the Tesla ethos.

2) Everything with Tesla that's old, is new again. Tesla announced the intent to offer an insurance product one year ago, May 2018:

https://electrek.co/2018/05/29/tesla-insuremytesla-insurance-model-s-most-expensive-car/

"Tesla is building up in-house insurance as Model S tops list of most expensive cars to insure"

And again in August 2016, "Tesla enters car insurance business as self-driving cars prepare to disrupt the industry"

The background to all of this, is that insurance companies (particularly in Europe, but also in the U.S.) are (1) Raising rates dramatically for insuring Teslas and (2) Some are outright refusing to insure Teslas anymore. Why? They're in accidents a lot more than other cars, and they are far more expensive to repair -- and take a lot longer to repair.

Here is an example from Roman and Tomas Mica, who live near Elon Musk's brother Kimbal in Boulder, CO, in terms of their repair experience with their brand new Model 3 -- just last week:

(start watching around the 10 minute mark, as that tells the beyond-insane insurance story, and then closer to the 16 minute mark when the insurance adjuster and body shop person explain how Teslas are far more expensive to repair than other cars, and take multiple times longer to fix)

Good thread comparing differences in the risk factors section between TSLA’s 2018 10-K and Q1 2019 10-Q

I finally had a chance to compare the latest 10-Q to the 10-K.

Following are some changes in the risk factors worth mentioning:- $TSLA admits that they had an issue with a supplier for M3. (p.34)

— bourcastle (@bourcastle) April 30, 2019

Tesla getting into the auto insurance biz???

As further evidence of Musk’s mendacity (insanity?), consider his reply to an analyst who noted during the Q1 conference call that “the insurance market is very unreliable for Tesla ownership right now.” Musk replied:

The answer is, yes, we are creating a Tesla insurance product and we hope to launch that in about a month. It will be much more compelling than anything else out there.

WHAAAAAT??? Because Tesla’s customers are complaining about how expensive it is to insure their cars, the company is going to get into the auto insurance business, a highly regulated, highly competitive industry in which a strong balance sheet and access to low-cost capital is critical? Musk thinks Tesla should try to compete against Berkshire Hathaway’s GEICO? And launch within a month?

This has to be one of the dumbest ideas I’ve ever heard.

For Tesla to make this happen, it would have to get regulatory approvals, raise capital, etc. So I searched the 10-Q for details and found…NOTHING! Not a single word about this bold new proposal.

I can only conclude that Musk just made up this idea on the spot. It’s nothing more than a figment of his imagination. Mark my words: Tesla will never insure a single car.

It would be hard to find a better example of Musk’s desperation and delusion…

A friend’s smart comments on the many emerging competitors to Tesla:

Reading almost all of the bullish reports on TSLA, it's clear that the analysts aren’t doing the detailed work on a multitude of levels. For example, are any of them aware that in this month -- April 2019 -- the Volkswagen eGolf (all-electric Golf) outsold the Tesla Model 3 in the most-developed EV market in Europe (Norway)? Or that the Audi eTron and Jaguar i-Pace outsold the Tesla Model S and X there by a combined factor of 6:1?

I would give the Tesla analysts a to-do list. Go out and test-drive these cars (as I’ve done):

- Audi eTron

- Jaguar i-Pace

- Hyundai Kona EV

- Kia Niro EV

- Kia Soul EV (238 mile edition)

- Nissan LEAF (226 mile edition)

- Chevrolet Bolt EV

If they did, they would learn that while the three Tesla models are indeed good products on a few impressive metrics, the other electric cars in the market are also very good -- not necessarily on all the same metrics -- and that some people may just prefer aspects such as basic quality and user interface issues such as doors that open/close every time, no glass roof cracks and water leaks, and Android Auto/Apple CarPlay, a car whose computer doesn’t regularly fail, requiring a tow to the service center, etc.

One more thing: Volkswagen will start taking reservations/deposits for the "ID" car -- a direct Tesla Model 3 competitor -- on May 8. It enters production this November, and the first deliveries will start realistically around January 1. They plan to make 150,000 units in 2020, all for European consumption (no exports to Asia or the Americas). Will it get more reservations than Tesla ever got from Europe? To be found out -- very soon. Next week.