Spruce Point Capital Management, LLC today issued an 54-page report entitled “A Repellant Investment,” that outlines why shares of Magnite Inc (NASDAQ:MGNI) face up to 25%-50% downside risk.

Q3 2020 hedge fund letters, conferences and more

Spruce Point Capital Issues “Strong Sell” Opinion On Magnite, With Up To 25%-50% Downside Risk

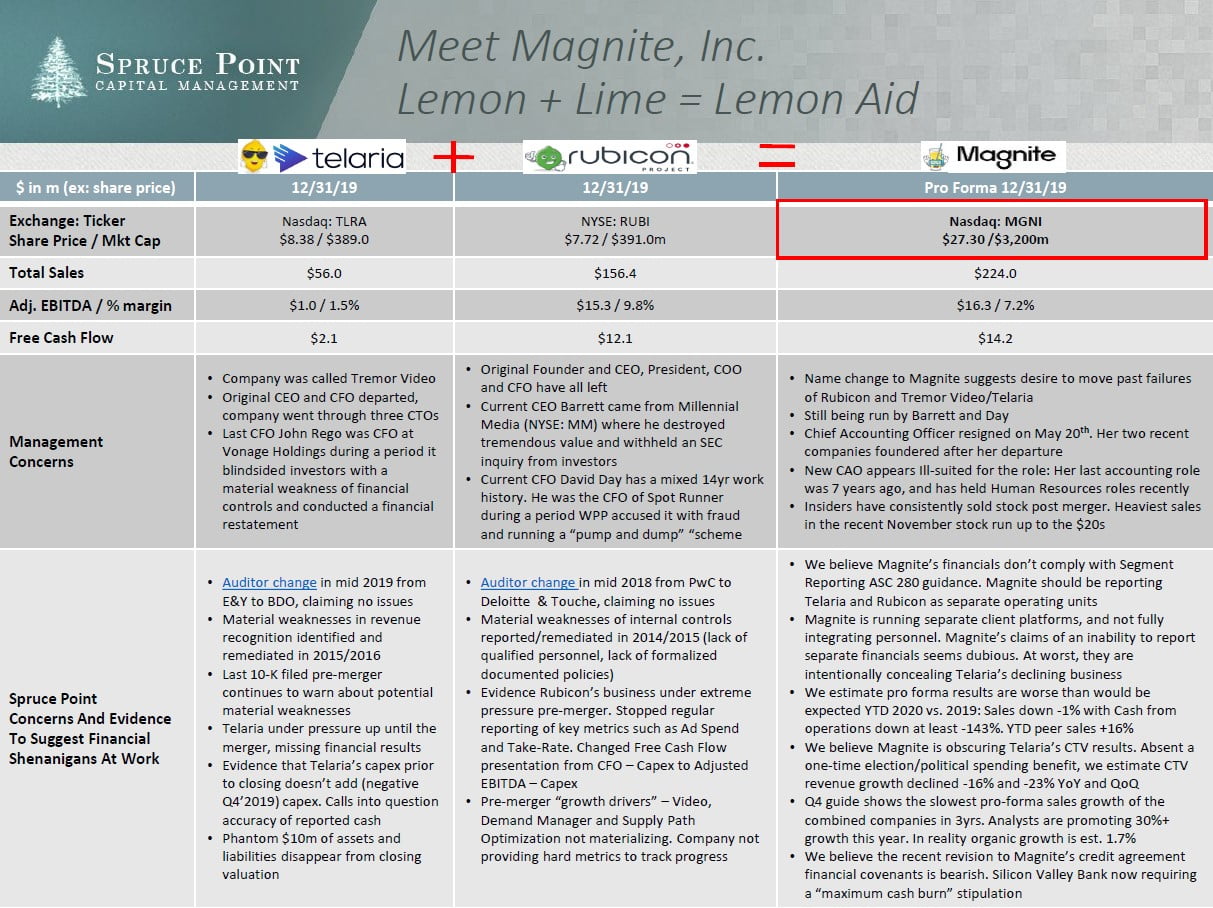

Magnite Inc (NASDAQ:MGNI) was formed in early 2020 by a merger of two advertising technology companies – Telaria (formerly Tremor Video) and Rubicon Project. The merger was predicated on cost, and not revenue synergies, and bringing a Connected TV (“CTV”) product to Rubicon that it couldn’t build alone. Spruce Point finds evidence to suggest that both companies were hampered with business and accounting struggles prior to the merger. We believe they have continued to mask challenges with inaccurate financial reporting. Magnite’s pro forma organic sales are down -1% YTD with peers +16%. Multiple customer interviews all tell us that Magnite does not have much quality CTV inventory to currently sell. A recent subtle change in Magnite’s financial covenant from “Adjusted EBITDA” to “Maximum Cash Burn” suggests further pressures could lie ahead. Adding to concerns, Rubicon’s CEO failed to promptly disclose an SEC inquiry at Millennial Media (NYSE: MM) where he was CEO, while Magnite’s CFO held the CFO role at Spot Runner, accused in a lawsuit of running a pump and dump scheme. Magnite is being promoted by an analyst with a FINRA citation and checkered past that includes hyping the AOL / Time Warner merger, a former tech media darling that settled SEC accounting fraud charges.

We believe investors are being misguided by Magnite’s growth prospects, and see 25%-50% downside.

Dubious Management

- Spruce Point finds evidence that Rubicon management exaggerated growth opportunities, and was failing to deliver on expecations prior to the merger. CEO Barrett destroyed tremendous value at his prior CEO role at Millennial Media, and for months failed to report an informal SEC inquiry into goodwill accounting. CFO Day held the CFO role at Spot Runner during a period WPP sued it and alleged it to be a pump and dump scheme. Telaria’s former CFO Rego blindsided investors with an accounting restatement earlier at Vonage Holdings

Dubious Financial Reporting

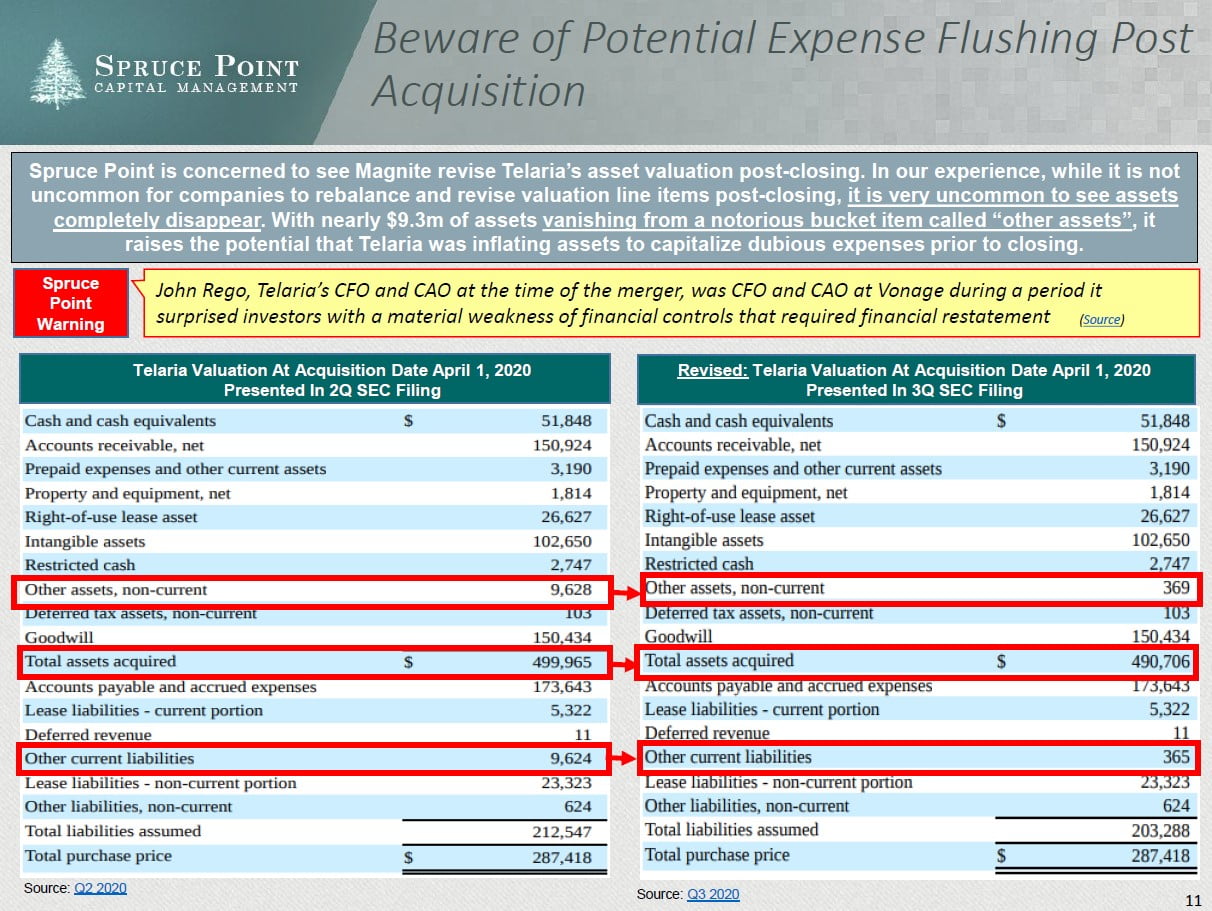

- We find evidence that Telaria’s capex reporting was mathematically impossible prior to its merger, and it made nearly $10m of assets inexplicably disappear at closing. Rubicon has reduced KPIs and resorted to a more aggressive interpretation of Free Cash Flow. Post-merger, evidence shows Magnite is running two separate businesses, yet only reporting one operating segment, allowing it to bury clarity into its struggles in our opinion.

Dubious Accounting And Leadership

- Both Telaria and Rubicon had prior material weaknesses of internal controls they claim were remediated, yet each recently had dismissed their auditors. Magnite’s Chief Accounting Officer (CAO) resigned in less than 2 months post close. Her departure from her two previous companies foreshadowed significant equity value decline. Magnite’s new CAO appears ill-equipped for the role. Her last accounting role was 7 years ago.

Dubious Stock Promotion

- Magnite’s shares are heavily promoted by Needham and Co, who blessed the merger with a fairness opinion. Needham’s analyst compares Magnite to an early Trade Desk, despite their business performance going in opposite directions. Analyst Martin has a FINRA citation, and was named in lawsuits related to the promotion of AOL before it collapsed and its successor was charged with fraud by the SEC and paid a $300m penalty

Excessive Valuation: Poor Risk / Reward

- Magnite is currently trading 20% over the average sell-side analyst consensus price of $21.70/sh. The market miscalculates Magnite’s true 2020 organic revenue growth of just 1.7%, and rewards it with a premium valuation of 14x sales, despite one-quarter of revenue “upside” driven by one-off benefits from the political election cycle. Absent this benefit, we estimate Q3 2020 CTV revenues declined -16% and -23% YoY an QoQ, respectively. At 6.5x-8.5x NTM sales, closer to peer multiples, Magnite would have 25%-50% downside risk ($14.75 – $20.00/sh)

Telaria Concerns Pre-Merger

Evidence Telaria’s Business Has Been Under Pressure Pre-Merger

Spruce Point observes that Telaria’s revenue and, especially its EBITDA, continued to disappoint up until the deal closed in Q1 2020.

Pre-Deal Telaria, Q3 2019, Nov 5, 2019

“I’d like to finish our call this morning with our expectations for the remainder of 2019. We’re tightening our guidance range for the full year with revenue between $69 million and $71 million and adjusted EBITDA between $2 million and $4 million.”

Source: Q3 2019 Conf Call

Jan 30, 2020 Update

“2019 revenue is expected to be approximately $68 million, up 23% from 2018, with CTV revenue of approximately $30 million, up nearly 100% from 2018. Q4 2019 revenue is expected to be approximately $20 million, flat to the same period last year, with CTV revenue of approximately $10 million, up 55% year over year. Adjusted EBITDA for Q4 and full year 2019 are expected to be positive, with full year Adjusted EBITDA representing a significant improvement over the same period last ”

Source: Rubicon Project and Telaria File Joint Proxy Statement/Prospectus

Telaria Actual 2019 Results And Q1 2020 Outlook, March 10, 2020

Fourth Quarter 2019 Highlights:

- Revenue of $19.6 million

- CTV revenue of $10.1 million

- Adjusted EBITDA(1) of $2.7 million

Full Year 2019 Highlights

- Revenue of $68.0 million

- CTV revenue of $29.7 million

- Adjusted EBITDA(1) of $1.0 million

Q1 2020 Outlook

- Q1 2020 revenue of $15.0 -$16.0m

- CTV revenue to represent $8.5-$9.5m

Source: Q4 2019 Earnings Release

2019 Spruce Point Observations

- Revenue of $68m well below the $69-$71m Pre-Deal Guidance

- Adj. EBITDA of $1.0m well below the $2 -$4m Pre-Deal Guidance

- CTV revenue of $29.7m fell short of the approximately $30m guidance showing no strong upside

Q1 2020 Spruce PointObservations

- Revenue came in at the low end of $15.1m

- CTV came in at $9.1m in the middle of range

- No Q1 Adj. EBITDA guidance was provided

Source: Q1 2020 Results

Read the full report here by Spruce Point Capital Management