Qualivian Investment Partners commentary for the fourth quarter ended December 2020, discussing their holdings in quality compounders.

Q4 2020 hedge fund letters, conferences and more

I very frequently get the question: “What’s going to change in the next 10 years?’… I almost never get the question: ‘What’s not going to change in the next 10 years?’ And I submit to you that the second question is actually the more important of the two.” – Jeff Bezos

Introduction

2020 was a year that tried investors souls. Between Jan. 1 and Dec. 31, the S&P 500 returned 18% which was “good” by historical standards. However, “good”, in 2020’s case, conceals much. It reminds us of the statistician who had his lower half in an oven and the upper half in the freezer. Asked how he was feeling, he said, “on the average I feel good.”

The sharp selloff in the back half of February and March and equally rapid recovery ignited the powerful whiplash of greed and fear: “Do I really know this stock?”, “What if it goes down further?”, “Maybe I should lock in my gains?”, and “Should I increase my cash holding?” were likely some of the questions spooking investors who were suffering from Covid post-traumatic stress disorder.

The selloff in the first quarter may have caused some to panic and sell at or near the lows, since the end of the pandemic was uncertain. This would have hurt their performance since many investors likely did not re-enter the market prior to its snapback. This is exactly why short termism hurts investment performance: the market is very hard to predict in the short term. This is consistent with the observation that being out of the market even temporarily can substantially affect long-term returns. For example, being out of the market for the 30 best days out of the last 25 years would reduce annualized returns from 9% to 1.5%5.

2020 Performance Review

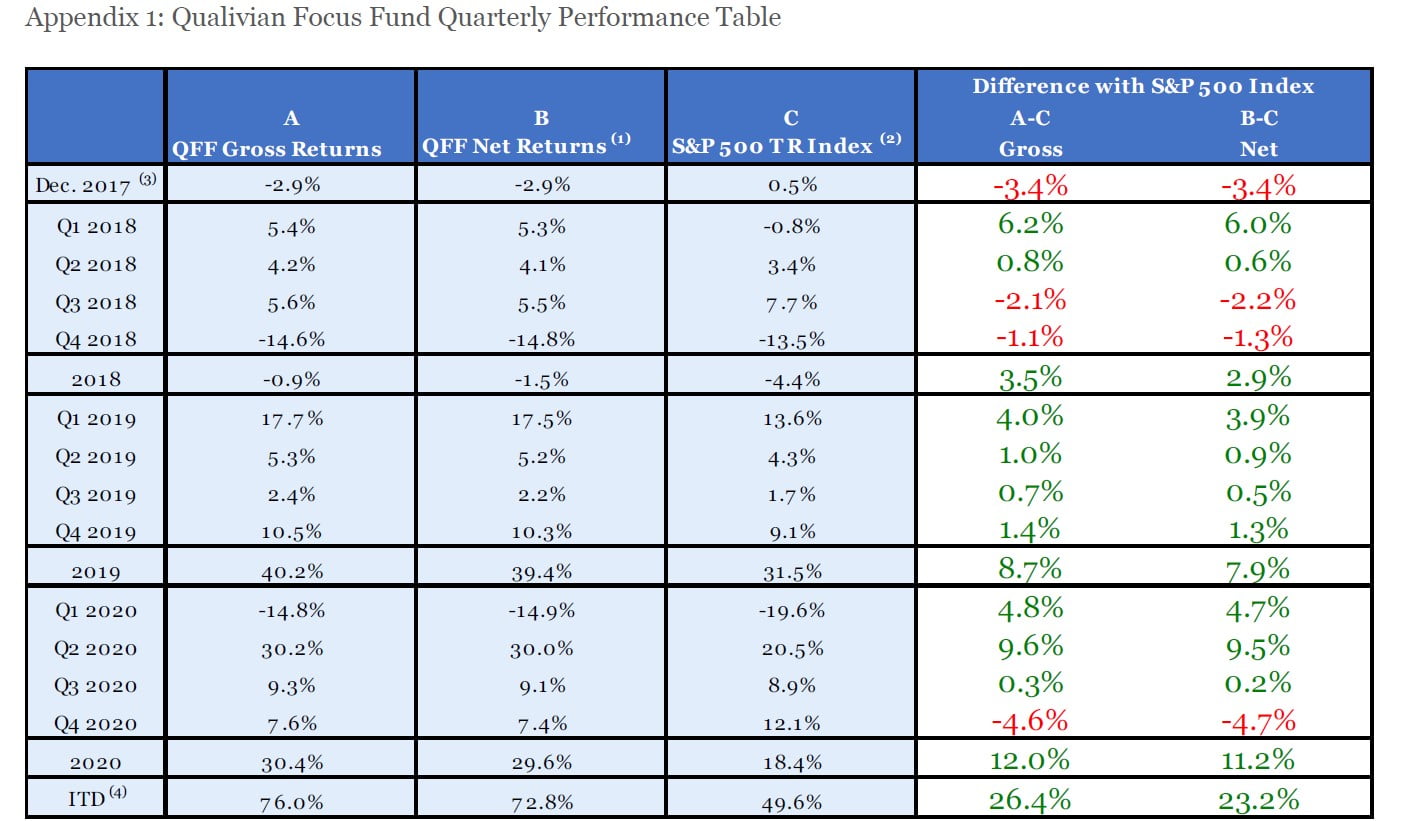

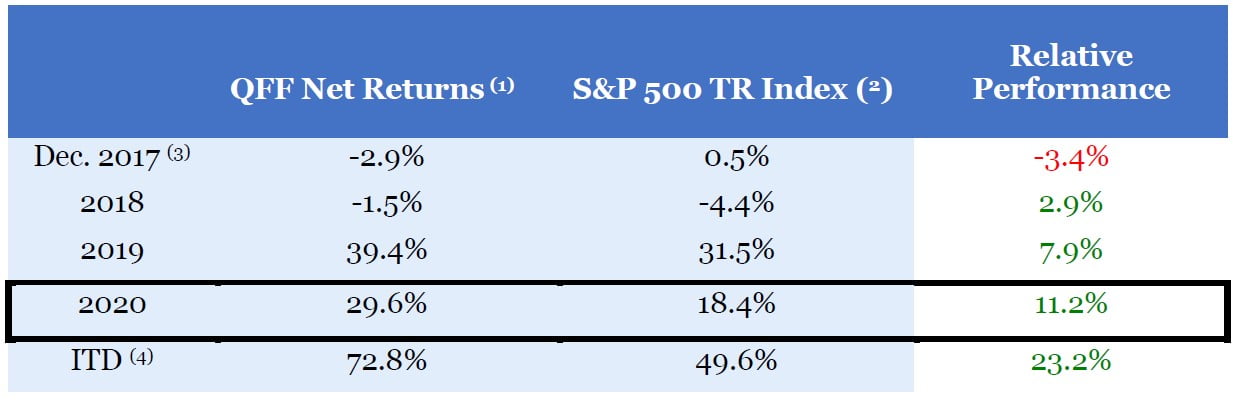

We outperformed the S&P 500 by 12.0% and 11.2% on a gross and net basis respectively during 2020. In the first three quarters our holdings in quality compounders, which included internet, ecommerce, and payment stocks helped us outperform by 15.6% and 15.1% on a gross and net basis, respectively. In the fourth quarter, as mentioned above, we underperformed by 4.6% and 4.7% due to our underweight to the cyclical energy, material, financial and “ground zero” cyclical stocks which did well this quarter.

Changes to the Portfolio in 2020

In the first quarter we sold our position in Wyndham Hotels (WH), given its sensitivity to travel and our inability to gauge the duration of the Covid epidemic, and Broadridge Financial (BR), because Microsoft, which was on our buy list, had corrected sufficiently to give us a better risk/reward than BR.

In April, we reduced our holding in Brookfield Asset Management (BAM) as the stock continued to underperform together with much of the credit sensitive financial sector as the uncertainty regarding the length and depth of the COVID slowdown increased in the quarter. Some of BAM’s subsidiary companies (BPY for instance) had substantial exposure to real estate and have higher than average levels of leverage. In an environment of potentially high credit impairments and economic uncertainty, we were less confident in our ability to forecast BAM’s growth runway. We replaced it with Adobe (ADBE), a dominant software leader that had been on our shopping list and which we had been tracking closely and that presented us with an attractive entry point.

We made no changes to the portfolio in the third quarter. Finally, in the fourth quarter, we sold the remaining position in BAM and used cash on hand to fund a new position in Watsco (WSO), which we had written about in prior letters, and which presented us with sufficient evidence in its second and third quarters that its financial performance was improving because of significant front-end and back-end technology investments it had been making over the past 3-4 years.

4Q 2020 Performance Review

We underperformed the S&P 500 by 4.6% and 4.7% in the fourth quarter on a gross and net basis, respectively. This was due to a material underweight to cyclical stocks in the energy, material, and financial sectors. These stocks generally do not pass our qualitative nor our quantitative screens due to their lack of competitively advantaged and long-duration visible earnings. These stocks had underperformed during the Covid sell off and with the post vaccine economy in sight they snapped back, starting in June when the initial results on the Pfizer/BionTech and Moderna vaccines became public. They picked up steam starting in November as the rollout of vaccinations were announced to start towards the end of the calendar year.

As a reminder this was our third negative quarter out of the 12 full quarters since inception (the other two quarters were Q3 and Q4 of 2018). Appendix 1 has our quarterly performance data since inception.

Was Covid a Time Machine?

Crisis reveals character. Imagine a look into the future for the next five years. If a business had a hypothesized competitive advantage today, this would be even more apparent in five years, as it outperformed the competition. The same holds true for a business that seemed average or even competitively disadvantaged. Time separates the fragile from the robust (not impaired by stress) and the antifragile (improves under stress). If something is fragile, it will break or deteriorate over time. Now suppose you could compress the next five years in a few months. This would provide the stress test without having to wait five years.

Covid provided that stress test by accelerating certain key trends, like virtualization, digital payments, eCommerce, etc. It uncovered fragilities at two different levels.

First it uncovered fragilities within the business models of the portfolio holdings. As investment analysts we are constantly pressure testing the business models we own. Covid performed the stress test for us in the real world rather than in simulation mode.

Second, it uncovered the weaknesses in investment processes. As stocks collapsed, conviction in the portfolio holdings got tested. Shoddy research got exposed. The visibility of earnings diminished or even vanished. The bear case became the best case. Emotions got inflamed. The quality of decision-making declined. Many investors threw in the towel and fled to safe stocks. Many of them likely missed out on the snap back of the stocks they had sold which impaired their returns.

Which Businesses Won From Covid?

Those businesses that benefited from Covid fall into two buckets:

- Those businesses that have pulled forward demand, by borrowing from the future when it will have to be repaid. There has been no cumulative increase in the size of the addressable market. An example would be a lawn care retailer that got more orders because more people were staying at home and tending lawns during the epidemic. The long run growth rate for lawns has not changed so there has been no permanent increase in the company’s growth rate.

- Those businesses where the increase in demand enhanced their competitive advantage and their future growth rate. They do not have to pay back the current increase in demand. An example would be a two-sided platform that benefits from a flywheel effect. By gaining mind and market share, its platform has increased its competitive advantage and its long-term growth rate. Examples would be PayPal (PYPL), Square (SQ), or Etsy (ETSY).

How Our Portfolio Did During Covid

Overall, the performance of the underlying businesses in our portfolio met our expectations. Almost all our holdings are the number one or two players in their sector, are highly cash generative, and have minimal debt. Some of them are two sided platforms so their competitive advantage increased due to pulled forward demand that likely permanently enhanced their share of their addressable markets. From Jan. 1 to Sept. 30, 2020, we outperformed the SP500 by 15.6% and 15.1% on a gross and net basis, respectively.

Our investment process remained unchanged during the crisis. We underwrite our portfolio holdings to a three to five year holding period, fully cognizant of the slings and arrows of outrageous fortune that the market can shoot at businesses. During the crisis we did not rush into safe stocks (for example consumer staples, telecom services, or utilities) nor did we rush head-long into Covid boosted stocks that may have seen short-term boosts to their businesses but whose growth rates were likely to mean revert to a lower longer-term growth rate (for example Zoom (ZM) or Teladoc Health (TDOC)). We carefully revisited the investment thesis behind each holding and debated whether it still held to the same degree.

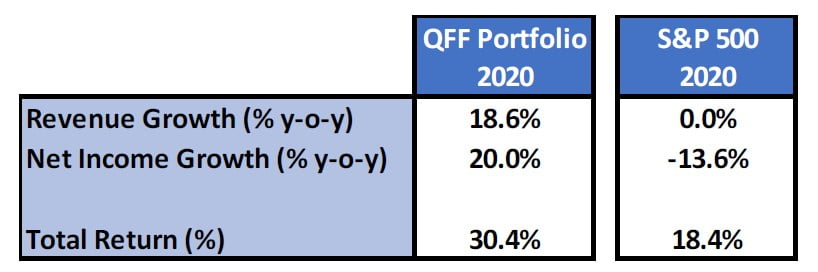

The following table illustrates the decline in annual revenue and net income of our portfolio vs its benchmark, the SP500:

- Whereas our portfolio’s revenue and earnings growth increased 18.6% and 20% in 2020 over 2019, respectively, the S&P 500’s revenue and earnings growth was flat and down 13.6% respectively, demonstrating our portfolio’s resilience during times of economic stress.

- In aggregate, our portfolio’s revenue growth performance was aided by the lockdowns as many of our names are in the forefront of eCommerce, digital payments, software, and online advertising, all of which had accelerating trends through the course of the year.

- In some instances, there were clear hits to revenue and earnings, especially our traditional specialty retail names (ORLY, TJX), whereas other names had company-specific improvements. For instance, Moody’s benefitted as more Financial Services clients signed on to added Analytics modules as their employees worked from home, as well as benefitting from a robust fixed income issuance environment as Investment Grade companies took advantage of historically low yields, and high yield and asset-backed issuers sought to strengthen their balance sheets during times of stress.

Our Three-Year Anniversary

We reached our three-year anniversary on December 14, 2020. One quarter of performance is mostly noise. However, 12 quarters of performance is more statistically relevant in disentangling investment luck from investment skill. Some reflections over the last three years:

Our Mistakes – Forced and Unforced

“Take chances. Make mistakes. That how you grow.” – Mary Tyler Moore

Mistakes teach you more than successes. Mistakes broadly fall into two categories:

- Mistakes of omission: stocks we did not buy but which outperformed. When you purchase a stock, the maximum loss is limited to the purchase price. When you do not buy a stock, the opportunity loss is potentially unlimited since the stock can go much, much higher. Mistakes of omission are less visible and do not always have to be “explained” to investors, since the stock was never in the portfolio, but we think it is important to analyze and highlight these misses in the spirit of continuous improvement.

- Mistakes of commission: stocks we purchased that underperformed either because (1) we should not have bought them or (2) we sold them too soon or too late.

Most investors focus on mistakes of commission because they are currently owned or were owned, and so are more visible. However, mistakes of omission tend to be far more costly.

Some Mistakes of Omission

“You miss 100% of the shots you didn’t take.” – Wayne Gretzky

These were names that passed our qualitative and quantitative screens and met the criteria of quality compounders. In hindsight, not purchasing them was either a forced or unforced error. We cannot do much about forced errors, but we should be held responsible for unforced errors.

- Nike (NKE): initially screened well on our investment criteria. It possessed a well-known global consumer brand and had built a fast-cycle logistics/supply chain capability from product design to order fulfillment. This allowed it to outcompete Adidas globally, as well as smaller competitors such as Under Armour, Puma, Asics, Reebok, etc. It possessed scale and scope economies across its value chain, allowing it to out-invest the competition. However, when we first looked at Nike in 2017 and early part of 2018, Adidas had been outperforming Nike having hit a sweet spot in its marketing campaigns and portfolio of athletic shoes and apparel offerings that resonated with the consumer. For us, that reminded us that there is a faddish element to apparel designers/retailers that we are not necessarily expert at getting right each time. However since, then Nike has regained its competitive edge, especially in the past 12-18 months and has handily outperformed Adidas and the markets overall, reminding us that a company like Nike with lasting brand dominance, as well as innovation/design and logistics advantages, is a good candidate for our portfolio. We continue to monitor it and look for an opportunistic entry point. An unforced error.

- Netflix (NFLX): NFLX fulfills most of our criteria: it has the dominant and growing share in the video streaming space, has good and improving returns on capital, and benefits from a flywheel effect. But it has to spend an increasing amount to acquire or create its content for streaming. It relied on the capital markets to fund its cash deficit, only becoming free cash flow positive in 2020. We had two big concerns. First, what if it made wrong choices on content? Those viewing assets would then be stranded and be written down. Second, what if the capital markets choked as they did in 2008? NFLX would have to make a dilutive equity offering or substantially lever up (which we are not fans of). These concerns kept us away. A forced error.

- Salesforce: (CRM): This clearly met some of our criteria: the premier salesforce automation product platform with high market share and a huge and growing market. It was led by a talented founder. They leveraged the optionality of the platform by making acquisitions like Tableau which enhanced their product set. We passed on it because of the large grants of options which reduced their economic earnings substantially and caused CRM to be trading at an excessive valuation. We always require a reasonable margin of safety in valuation. Furthermore, unlike most of our other holdings in the technology sector which are levered to the consumer, CRM’s business is driven by large and mid-sized companies’ technology spending trends which tend to be more cyclical. A forced error.

- NVIDIA (NVDA): Historically NVDIA’s business has been highly cyclical and tethered to the PC-gaming and console markets with its GPU chips. NVDIA did not particularly screen well on our quantitative screens, and we were not confident in being able to time its traditional chip cycles. From a valuation perspective, NVIDIA has perennially looked expensive to us and at this point does not present us with our required margin of safety to initiate a position in the company. A forced error.

Our Mistakes of Commission

- Altria (MO): we bought this at an average cost of $58 in the first year of the fund and sold it at an average cost of $54 in the first quarter of 2019. We were attracted by its oligopoly position, its high returns on capital, its low capex, and its long-term capital allocation strategy of repurchasing its own shares given its prodigious cash flow. We did not correctly judge how strongly the investing environment had turned to ESG values, of which Altria was a serious violator and made it a toxic stock for most portfolios, depressing its price. Furthermore, its capital allocation also disappointed us when they purchased 35% of Juul for $12.8bn (valuing the company at $38 billion) and had to write down its value by over $9 billion. Its CEO was replaced. We should not have bought it. An unforced error.

- JD.com (JD): we purchased this at an average cost of $39 and sold it at an average cost of $24. We sold it after the CEO was implicated in a sexual harassment case. The alleged incident occurred while he was visiting the United States. We lost confidence in his integrity. It is now trading at $94, and we would have done well holding it. However, we have no regrets. Integrity of management is not negotiable. A forced error.

- Alibaba (BABA): we purchased this stock at an average cost of $208 and sold it at an average cost of $177. Had we held on to it we would have done well. We usually do not focus on non-US businesses but BABA fit perfectly into the types of business models we go for: oligopolistic, capital light, a platform with lots of optionality but we sold it because: (1) the deteriorating relationship between the US and China made the long term future for US investors less certain and difficult to dimension, (2) we became increasingly uncomfortable about the security structure as a structured investment vehicle (SIV), which did not give its owners rights that were more limited than ADR’s, and (3) the non-expensing of significant option grants which diluted its economic earnings. Arguably (2) and (3) could have been anticipated to some extent but (1) was determinative. We do not like businesses where the political/regulatory risk is highly uncertain. Probably a forced error.

- Verisign (VRSN): A dominant provider of internet domain names. A monopoly with high returns on capital, low capex, and consistent predictable growth. We bought and sold it at an average cost of $114. We sold it because we believed it did not have the reinvestment opportunities and attendant growth that we were seeking. This turned out to be a mistake as it demonstrated good growth and the occasional targeted acquisition. It has handily outperformed the market. An unforced error.

What Have We learned about investing?

Pareto Principle

The Pareto Principle: the majority of the market’s return will come from a minority of available investments6. Our strategy of buying a limited number of outstanding quality compounders is premised on this.

The last three years have validated the Pareto principle as digitization has entrenched winners, business concentration has increased, and platform businesses with optionality have become more dominant.

Optionality

Conventional valuation approaches do not fully capture the value of optionality and intangible assets. Qualitative factors explain more of the variation in returns than in the past. Mean reversion is less effective in these instances but still applies for average businesses.

High Degree of Difficulty? Not for Us

Many investors avoid well known stocks because they feel they are efficiently priced, so they invest in illiquid, small cap, esoteric, or complicated investments which are sexy but have a high degree of difficulty. They make investing more difficult than it should be because (1) they believe they have the skill to deal with complex situations or (2) they want to impress their investors with their exotic picks. That is not our approach. We prefer low degree of difficulty situations. Our chances of outperformance increase when there are a small number of interacting variables in the investment thesis.

Don’t Overlook the Obvious

Sometimes the best stocks are sitting in front of your nose. Many well-known stocks can get inefficiently priced for extended durations because the market is applying wrong valuation models or because stocks prices fluctuate more than their fundamentals. For instance, some quality compounders were inefficiently priced when we purchased them three years ago even though they were well known names and they looked optically expensive on one-year out earnings.

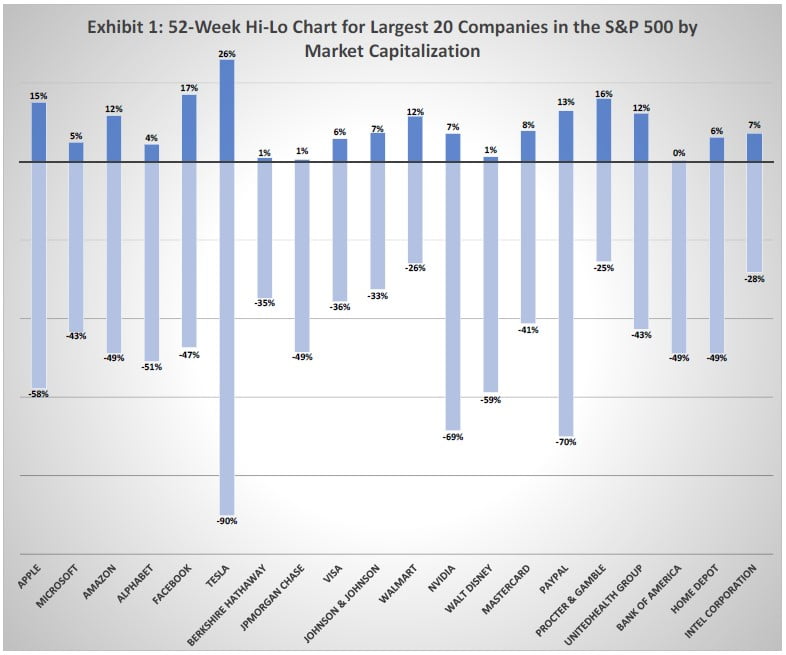

As an illustration, in the past 52-weeks, four of the five largest companies in the S&P 500, as well as ten of the largest twenty companies, had a greater than 50% swing in their stock price in the past 52-weeks. These are the largest and most widely followed companies. We are certain that in most of these cases, the underlying intrinsic value of the companies did not change by more than 50%. Yet, the stock prices certainly did, enabling disciplined investors to accumulate new positions at attractive valuation levels. Certainly, this period includes the time when stocks declined precipitously, last year due to the economic lockdowns due to Covid but similar results can be found in prior years (refer to our H1 2018 letter for a similar analysis we did back then). While anecdotal in nature, this certainly illustrates the fallacy behind (at least the “strong” form of) “efficient market theory” and the attendant notion that quality compounders are always fully valued because investors readily appreciate the superiority of their business models.

Dealing with the Future

We do not spend time trying to figure out what will happen to the market in the future. However, there are ways we can reduce the degree of difficulty in understanding how the future can affect the individual stocks in our portfolio to manageable proportions. Let us start with some things we cannot predict:

- the performance of the overall market or other macro variables,

- black swans like epidemics, depressions, wars; and

- other unknown unknowns.

Now let us get to known unknown’s we can partially predict:

- the future of individual businesses.

We can then make better predictions if:

- the business has an enduring competitive advantage which reduces the prospects of its rivals eroding its business model.

The predictive success gets even better if:

management is talented and shareholder-oriented, often founder-led. Talented management can create positive optionality and can find a way through business adversity.

And better yet if:

- The business has strong secular growth opportunities independent of the economic cycle. This enables you to focus on whether you are correct about the business and not which phase of the economic cycle you are in, which is hard to predict anyway.

Ultimately:

- You purchase it at a reasonable discount to your estimate of its economic worth. Just in case you are wrong.

And that really sums it up. You cannot predict the unknown unknowns of the future, but you can mitigate the negative effect of known unknowns.

What Have We Learned About The Business Of Running A Boutique?

To win you must first survive. The reason most investment boutiques fail is not just because of investment performance but also because they do not manage their business properly. A good investor is not necessarily a good business manager. When many boutiques do not reach their AUM goals within a few years, they exhaust their budgets and shut down. We are fully cognizant of this. We have kept our costs low and expect to keep going for the foreseeable future regardless of our AUM.

What Have We Learned About Ourselves?What Have We Learned About Ourselves?

Be Yourself

Our focus on quality compounders enables us to funnel the entire opportunity set (large and mid-cap stocks) into a smaller subset of names where our experience and skill set gives us an edge. Investing in quality compounders is but one way of investing, but it is one which leverages our skill sets and is consistent with our emotional tolerances.

There are other investment approaches. However, they fall outside our skill set and comfort zone. It is easy to be tempted to stray from one’s capability set and follow the winds of fashion or “what is working.” However, each investor must choose an approach that enables them to be their authentic selves. Remember, everyone else is taken.

Ending Thoughts

We look forward to continuing to share our thoughts on our investment approach, and to keep you abreast of our performance and changes to the portfolio. In the meantime, if you have any questions, please feel free to reach out to us at the links below.

With best wishes,

Aamer Khan

Co-founder

Cyril Malak

Co-founder

www.qualivian.com