Peterson Investment Fund I annual commentary for the year ended December 2020.

Q4 2020 hedge fund letters, conferences and more

Dear Partner,

Investment Results

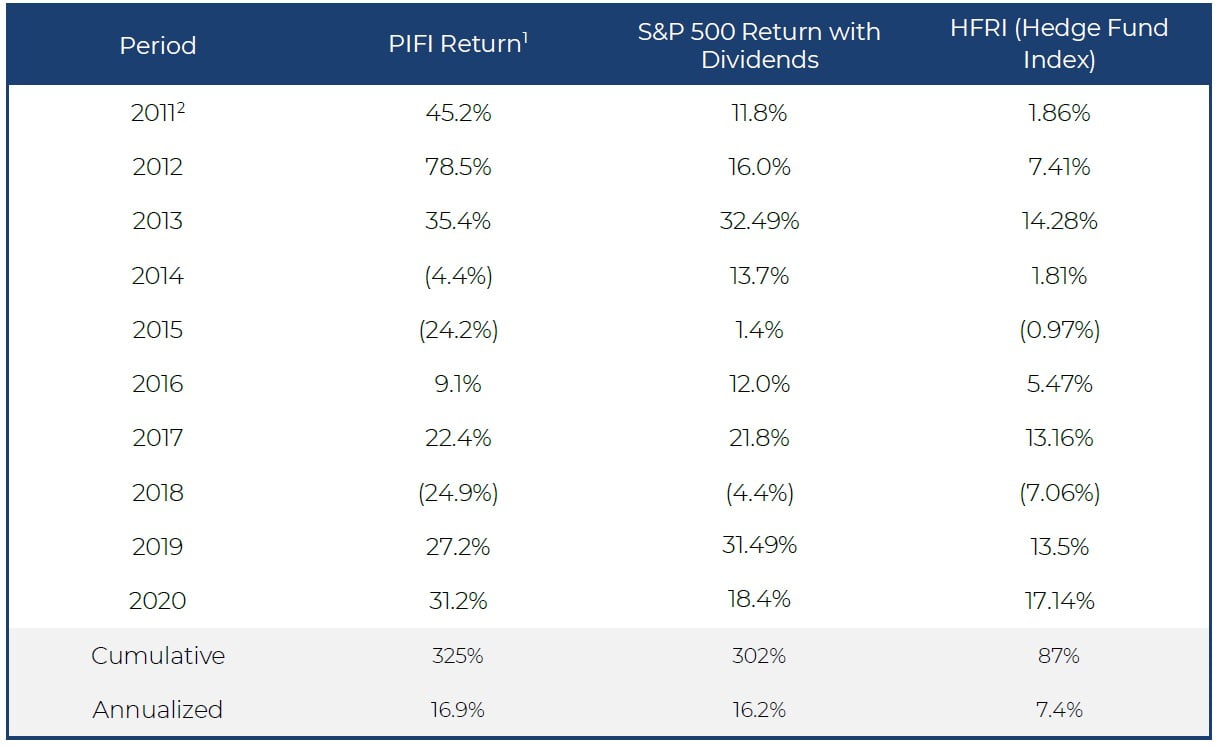

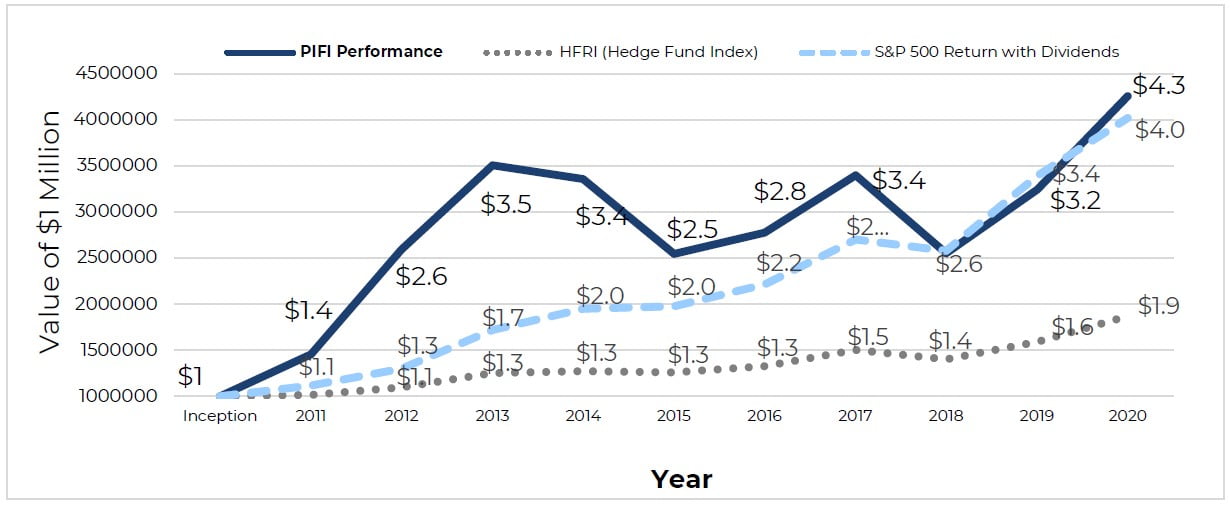

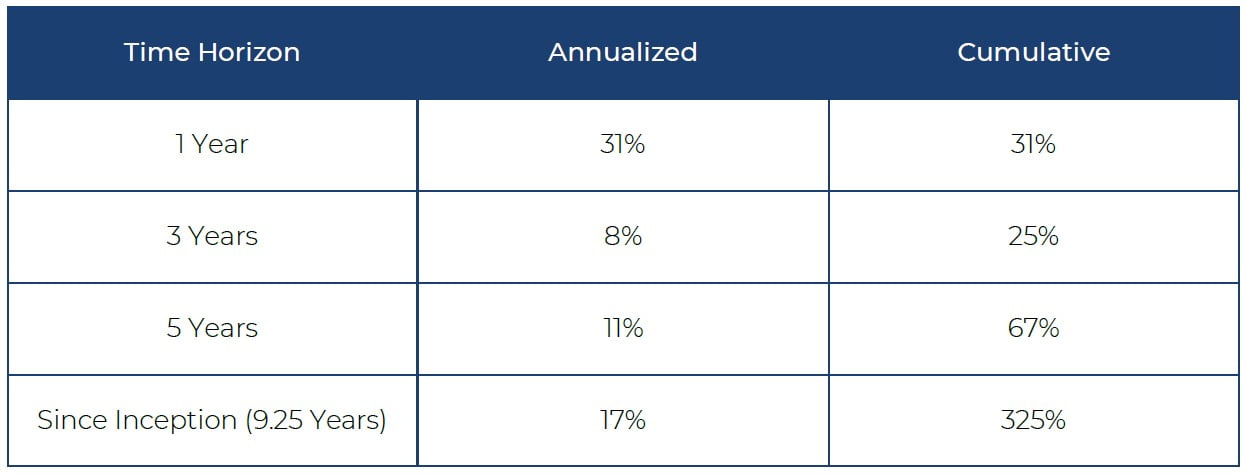

A $1 million investment in Peterson Investment Fund I (PIFI) at inception on October 1, 2011 grew to over $4.2 million on December 31, 2020. This amounts to a cumulative return of 325% in just over nine years.

Peterson Investment Fund I grew by 40% during the fourth quarter of 2020 and delivered a 31.23% return in 2020. In comparison, the S&P 500 completed the year up 18.4%. PIFI has generated annualized returns of 16.9% since inception.

This table presents a summary of our performance since inception and is just beginning to illustrate the underappreciated power of long-term compounding. We remain doggedly committed to our mission of providing a world-class capital appreciation vehicle that builds enormous wealth for our long-term partners.

Despite the explosive growth of the S&P 500 over the past decade, with some apparent levels of excess, the price of our portfolio remains far below its intrinsic value. In other words, our portfolio’s value continues to grow rapidly, while market prices are not keeping up. Despite price growth, the gap between price and intrinsic value has widened. As this gap closes, we expect our portfolio prices to rise considerably in the months and years ahead. The fund remains very concentrated, holding only our absolute best ideas with asymmetric expectations (an abundance of upside potential coupled with limited downside risk) for future performance.

Our philosophy is not designed to eliminate volatility, but rather, to minimize the risks of a permanent loss of capital. For some, any level of volatility is too difficult to handle. However, our concentrated investment approach allows us to remain focused on reaching the best outcomes, without being weighed down by lower performing positions that might offer diversification but lower returns. We remain focused on obtaining strong downside protection by paying far less than fundamental business value. Over the long-term, this approach will continue to produce successful results for our partners.

Finally, our portfolio remains uncorrelated with the S&P 500, including a global set of businesses, some private exposure, and our structured value practices. Our portfolio companies are extraordinary businesses. While market prices may fluctuate, the businesses we own will continue to thrive when the US and global markets trade up, down or sideways.

Results Commentary

Peterson Investment Fund I, LP is a concentrated long-term, value-based hedge fund. Our objective is to compound capital at a rate that outperforms the S&P 500, including dividends, over the long run.

We are pleased to report another year of significant returns to partners and to outpace the formidable and rapidly increasing S&P 500 index. This year presented extraordinary challenges, including a devastating pandemic, a recession, social unrest, and political uncertainty. Millions of people were confined to their homes, many suffering unimaginable hardships. Most Americans have never experienced this level of extreme uncertainty.

This is the third crisis I have been investing through, professionally. During the dot com collapse and September 11 attacks, I was writing financial plans for clients of what is now Ameriprise. During the 2008 financial crisis, I was five years into a consulting career on Wall Street and was working with Goldman Sachs in London.

Amid the 2020 pandemic, similar to the previous two recessions and consistent with the past two and half centuries of American history, opportunities were available for those bold enough to take action. Wealth during these times is in some cases destroyed but, in most cases, it is transferred. It shifts from the impatient to the patient, from the unprepared to the prepared, and from the many to the few.

Many investors rationally understand to buy when others are fearful, yet it is often difficult to execute on this simple philosophy. In 2020, the VIX, commonly known as the fear index, broke its historical record, exploding from 12 to over 80 – reflecting a moment of unprecedented fear.

Those who took decisive action at critical moments were rewarded. As explained in subsequent sections, policymakers paved the way for rising prices, but fear is a deeply embedded human condition that is difficult to quantify. Since one is unlikely to escape such a subconscious emotional state, great fortitude is required to execute in the face of perceived danger.

“Be greedy when others are fearful and be fearful when others are greedy” is a well-known quip from Warren Buffett. But this simple statement demands immense discipline and courage to implement.

Phil Fisher reminded us many years ago, “Don’t be afraid of buying on a war scare” and Howard Marks wrote in April 2020, “It’s not easy to buy when the news is terrible, prices are collapsing and it’s impossible to have an idea where the bottom lies. But doing so should be the investor’s greatest aspiration.” These investors offer the same lessons for success from different perspectives. What one should do is not always easy to do, and that is why it is so rewarding.

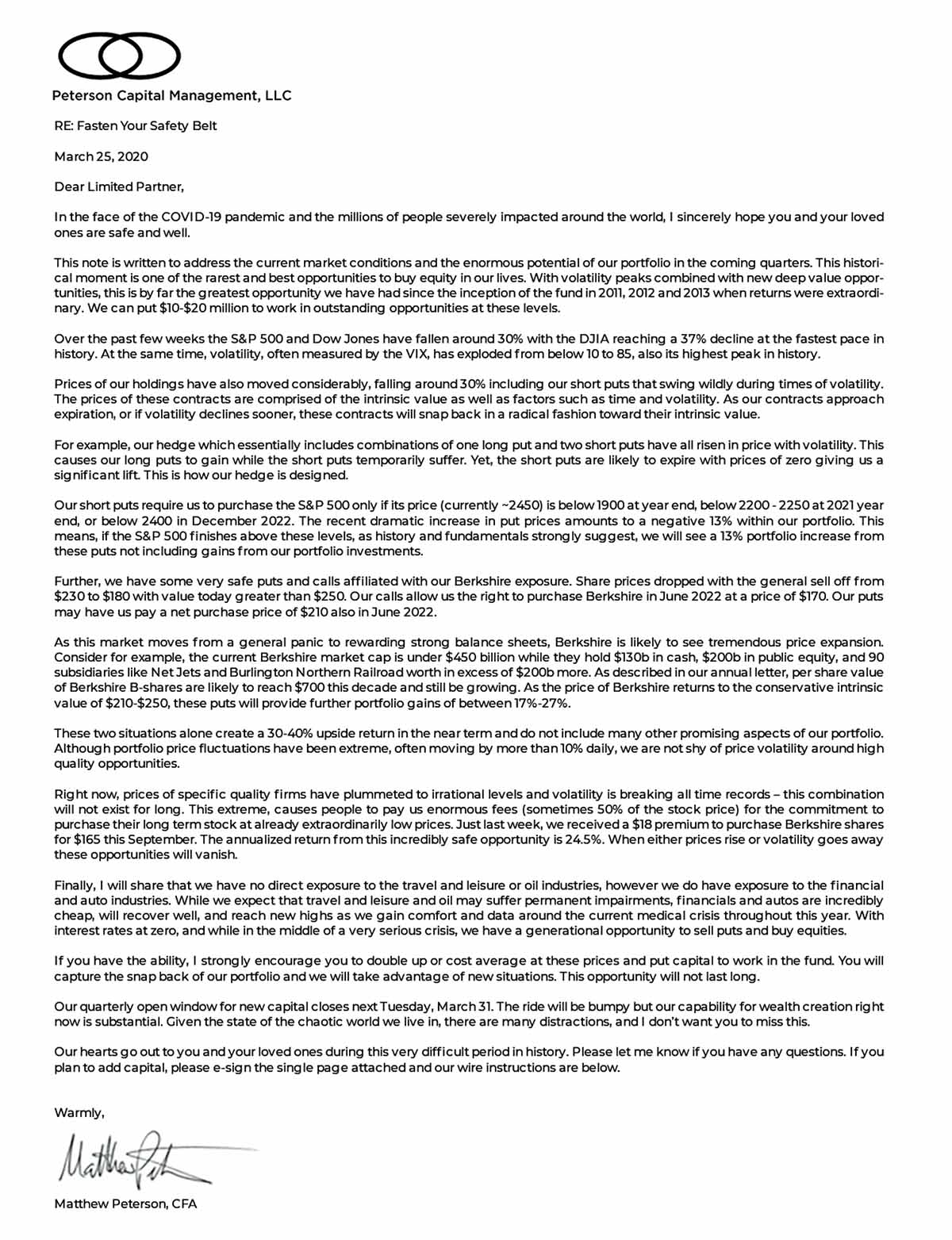

On March 25, at the bottom of the market, we provided our first mid-quarter memo to LPs in nine years titled, “Fasten Your Safety Belt.” It urged partners to rationally appreciate the significance of the opportunities available. That memo is reprinted on the following page.

In Q2 we wrote to partners, “This historical moment will be recognized as one of the rarest and most remarkable opportunities to buy equity in our lifetime. When the dust settles, our future selves will most certainly look back at the prices of today with envy. I strongly encourage you not to miss this opportunity. This is an exciting moment to be a value investor and our capability for wealth creation is substantial.” We then began our upward trajectory, gaining over 75% during the second half of 2020, lifting returns from -29% during the first half to +31% by year-end.

A multi-disciplinary understanding of business, economics, psychology and history were aiding forces driving our successful year. Coupled with decades of experience, we were able to act confidently. We took decisive action in April to not only position our portfolio well for the year ahead, but to increase the quality of our portfolio for the decade ahead. The subsequent sections describe how we were able to obtain this successful outcome and why this is only the beginning of many promising years.

Portfolio Commentary

We remain focused on compounding wealth over the long-term by applying our deep, value-based principles and our business owner mindset. Our winning formula includes focusing on the best business models, best management teams, and best value opportunities in the modern economy. Our willingness to concentrate the portfolio among a few exceptional holdings provides an advantage toward our objective of outperforming the S&P over the long run.

Over the last decade, the S&P has compounded at an extraordinary 16% annualized rate. However, Wharton Professor Jeremy Siegal has described in his book, Stocks for the Long Run, that, over 200 years, with much consistency over a decade or two, the compound rate of the S&P 500 is approximately 6.8% after inflation. Passive investing in an index fund is unlikely to sustain the heightened level of growth from the past decade.

We are not correlated with the S&P 500, but use this benchmark because it is the best alternative to our fund for most partners. Each year the S&P 500 outperforms about 80% of professionals and a much higher percentage of retail investors. Over multiple years, far fewer professional funds can continue to maintain this outperformance.

Our mentality is that of a business owner and we are passive advocates for the firms in which we invest. This approach is distinctly different from the short-term speculative transactions pursued by many. PIFI’s investment paradigm involves buying securities when shares are underpriced, based on fundamental analysis. The Peterson Investment Fund I investment objectives include capital preservation, long-term capital appreciation over the benchmark (S&P 500), and limitation of downside risk.

Using a method we have termed ‘structured value,’ the fund combines value investing principles with long-term equity anticipation securities (LEAPS), warrants and other products to obtain better prices when purchasing or selling securities. This is a departure from using these products for short-term trading, and it is an approach that allows us to provide a strong performance advantage to our partners.

Our portfolio includes impressive businesses that are growing in value faster than the stock market can sustain over the long-term. This bodes well for our portfolio performance relative to the S&P 500. Only a small number of these opportunities exist, which is why success requires a strict level of concentration. We have no use for the 20th best opportunity.

Today, over one-third of our portfolio is comprised of three rapidly compounding firms: Daily Journal Corporation, Berkshire Hathaway, and Dhandho Holdings. Our portfolio gains result from several distinct factors, including equity appreciation, dividends, and profits derived from structured products.

Conventional thinkers may question the Peterson Investment Fund I portfolio because of its unique attributes, including the unconventional level of concentration. Indeed, one-third of the portfolio is comprised of a micro-cap multi-asset government SaaS business, a mega-cap conglomerate, and an ownership stake in a private India-focused nano-cap hedge fund. Yet, the high-quality compounding nature of these businesses may allow us to own and profit from them for a decade or longer.

Our unmistakable concentration would be questioned by anyone who still believes in the efficient market hypothesis. However, independent thinkers will recognize that the unique nature of our portfolio is precisely what will allow its outperformance over the market.

While concentrating our portfolio leaves us susceptible to uneven short-term results, it is a key ingredient to yielding long-term returns that outperform the benchmark. Value investing remains the surest way of obtaining exceptional results.

The time horizon among some US investors is becoming shorter than ever before. Discount online brokers like Robinhood, Public and others offer zero-fee fractional shares and are aiding the adoption of high-frequency trading on Main Street. This is unlikely to have profitable or productive benefits for most investors or society. Passive investing has also gained favor with the proliferation of index funds, partly because of the unusually high returns experienced in recent years. However, in a zero-sum game, day traders often give up their gains to long-term investors and index investors are likely to match the ultimate trend of 6.8% plus inflation.

Our portfolio is made up of high-quality businesses trading at price discounts compared to their growing intrinsic value. We hold 15 positions across six sectors (communication services, consumer discretionary, financial, health care, real estate, and technology). Our companies are headquartered in four nations (United States, Canada, China, and Turkey), and they serve customers across the globe.

Our framework prioritizes opportunities with excellent business models, superior management quality, and extraordinary value. Further, the companies will perform very well in the years to come making any possibility of a long-term permanent loss in capital extraordinarily small. This asymmetry in risk-reward is rare.

This simple co-priorities framework illustrates why such conviction is warranted. It is hard to go wrong when we get this right:

Superior business models deliver more cash flow to be allocated by management. Thus, a primary skill required by high quality management is strong capital allocation capability.

Management must choose from internal investments, external acquisitions, dividends, debt repayment or share buybacks. Optimizing cash flow allocation decisions will have a profound impact that creates value for the firm. Many CEOs and executive teams fail at this task because rising professionally at a firm does not typically require success in capital allocation.

Our core holdings include teams that exhibit a high level of integrity, act rationally and display owner mindsets (typically through large ownership). We seek out firms focused on invariant strategies, such as deferred gratification, trust, and win-win. Despite the proven success of these methods and the likely failure of management focused on the inverse, Charlie Munger has exclaimed they simply, “can’t teach the old tricks to the new dogs.”

The stock market is a pari-mutuel market system where buying stocks pushes up prices, which will alter the risk-return profile and odds. Given that markets are mostly efficient, well-known business models and top management tend to cost top dollar. This causes us to look in unusual corners for firms with hidden value. When we find a high-quality firm with exceptional management at a cheap price, we will be aggressive.

This is a period of incredible opportunity and remains a unique period for both existing partners and those committing new capital to the fund.

Over the past several years, we incorporated a multi-year portfolio hedge. The following section describes profits from our 2020 hedge, followed by updates on three core compounding holdings. Despite a climate of volatile market prices, we expect these three positions to deliver significant gains well into the future.

Portfolio Hedge:

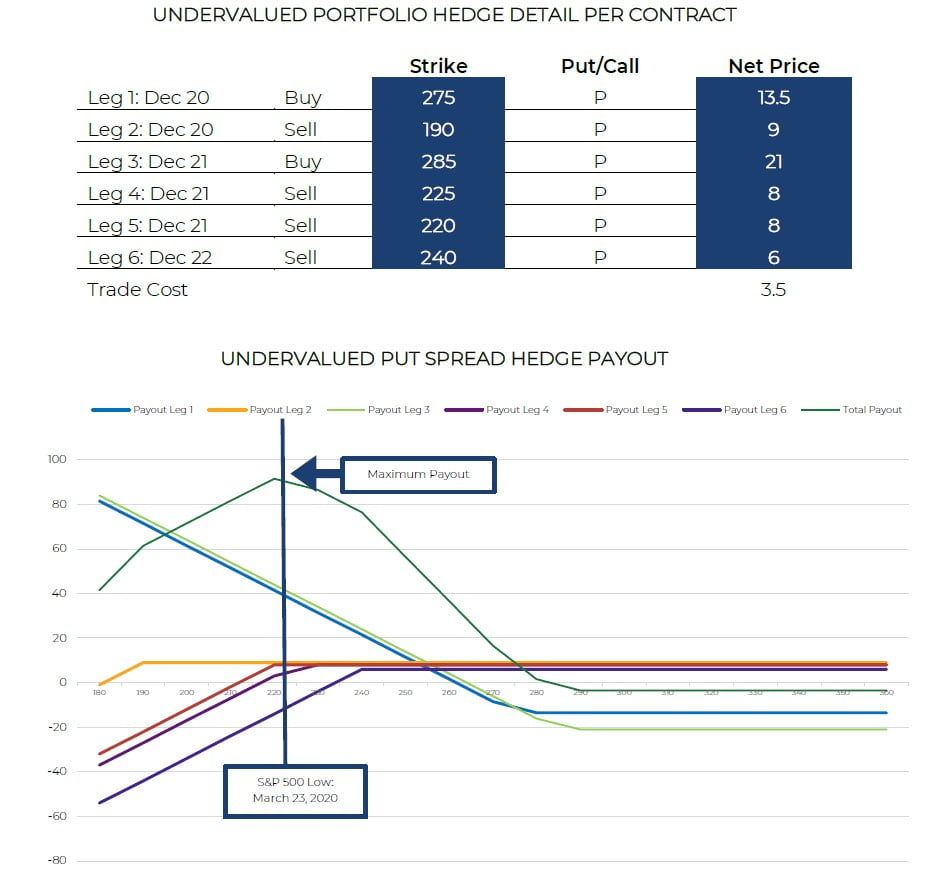

For years, we have provided details on the complex multi-year dynamic hedge constructed within our fund. In 2020 the hedge delivered a 5.5x or 550% return on the 2% position in our portfolio. This created more than a 10% gain for our entire portfolio. This growth occurred during the second half of the year, based on July asset values, as our contracts approached year end expiration. While the results were remarkable, the nature of this crisis, particularly its quick rebound, required us to take decisive action at the depths of the market meltdown.

Our hedge included a multi-year series of put combinations. Over the past three years, when volatility and prices were hitting record lows, we purchased slightly out of the money puts, while selling twice as many far out of the money puts to pay for some of the transactions. These contracts lasted approximately three years each and details on constructing this position are available in past annual letters.

In our 2019 annual report, we explained, “Our hedge will cause an approximate 1% annual loss during a flat or rising market, but will provide gains on our entire portfolio of perhaps 10% or more during a prolonged recession or market downturn of 20-30% or more.” This is precisely what happened – with one important detail: The enormous level of consumer-focused stimulus and prolonged zero interest rates were pushing markets up with great force. During Q2 we, fortunately, recognized that this had the potential to destroy our gains before contract expiration.

In a rational mindset, while analyzing historical crises, holding the contracts until expiration to capture gains seemed appropriate. This is, however, not always viable. We experienced such a rapid rebound that shrewd actions were needed to capture our gains and repurpose some longer-term exposure into shorter duration contracts.

The chart below illustrates our Index-based hedge going into March 2020.

Our strategy included two purchased puts that would increase in price if the S&P 500 fell below 2,850 and 2,750, and we wrote (sold) four additional puts much further down that would also increase in price as markets fell. Importantly, the set of four puts would likely expire at zero, allowing us to keep the cash earned from selling these puts. If purchases were required, these far out-of-the money puts offered considerable value. Our commitment was to purchase the index only at highly attractive prices like 1,900 in December 2020. For reference, the S&P traded above 3,700, nearly twice our committed price at expiration.

In April, the unpredictable state of the world was alarming. As a result of volatility, put premiums had risen to such record-breaking levels that the portfolio value of our purchased puts reached their maximum height. Further, if left through expiration in Dec 2020, 2021 and 2022, the puts we purchased would decline in price.

Ex-ante, our thesis of declining put prices was further justified as it appeared that the coordinated stimulus measures would cause stock market prices to rebound. Between rising markets and a decline in the VIX, our profitable hedge threatened to lose its intended value. Fortunately, as prices began a rapid rise, we were already considering the situation and had the foresight to act very quickly.

The challenge we found was that closing out only the profitable contracts left us considerably vulnerable to the downside for several years until the puts we wrote expired. However, inaction was not an option. Any delay would have our hedge moving against our fund performance in the coming months and all the benefits of our purchased puts would be lost.

Instead of leaving us exposed to all 500 firms in the S&P, we carefully designed a basket of a dozen firms with solid financials where we could repurpose this exposure with confidence. Specifically, we sought holdings with strong balance sheets, lots of cash, a long-term profitable enterprise and some big volatility spikes.

The firms included in our new basket included: BERY, BLDR, DIS, DXC, IRM, JPM, LSXMA, MKL, SBUX, SRG, VAIC, WFC.

This shift allowed us to unwind purchased puts at a large profit, while unwinding the four puts we wrote at a momentary loss. We then recaptured the forgone premiums by repurposing our exposure to a portfolio of strong firms with even higher momentary local volatility and shorter contract durations. These transactions reduced our total downside exposure, reduced the duration to expiration (2.75 years declined to 9 months) and increased the IRR or gains from the hedge.

Our newly constructed exposure required only nine months to capture our gains. As discussed in past letters, as the crash occurred, the hedge did not minimize our volatility. Our hedge was not designed to provide immediate gains, but to deliver them as our contracts expired. Within three quarters, contracts expired, and these gains had arrived.

The most difficult decision was choosing the right moment to unwind our profitable puts. We are not traders and have argued for years against timing the markets. Yet, suddenly, and by our design, we needed to time some crucial decisions.

Through a combination of factors including experience, analysis and fortuity, our actions proved to be successful. And lessons were learned. If a hedge like this becomes appropriate again, instead of selling two long-dated far out of the money contracts, we will repeatedly sell shorter duration far out of the money puts to increase our flexibility to take profits at the proper time.

Speaking with Ed Thorp on this topic would greatly aid our future decision making in this space.

See the full report here.