Bitauto (BITA) is a heavily shorted, low float stock but there is far more to the bull case than a simple short squeeze. As with my long report on RH in the $80s, this report will attract vocal critics. But by the time BITA hits $100 I expect these critics will have long since gone quiet or found more suitable employment. My view that “BITA rises to $240” is not overly optimistic. In fact, it may prove to be too conservative. Read this report first and then simply decide for yourself if BITA could comfortably exceed $17 billion in market cap in the near future. To me, the answer is a very obvious “yes”.

Q2 hedge fund letters, conference, scoops etc

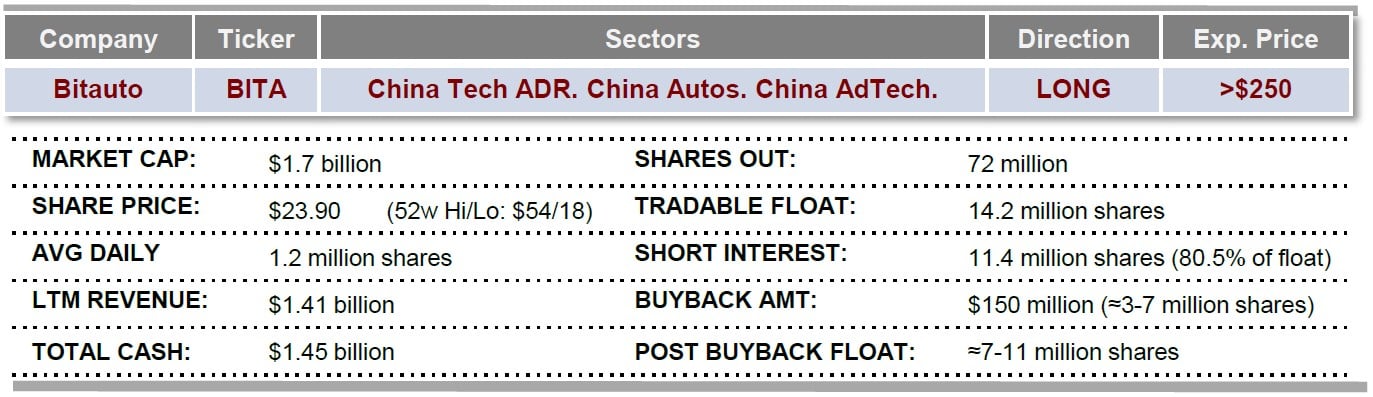

Short interest in Bitauto has quietly risen to 11.4 million shares. But because the float numbers are not pulling into Bloomberg, most hedge funds are unaware that this now amounts to 80.5% of the tradable float. BITA recently announced a $150 million share buyback which could now reduce the float to well below 11 million shares. The short interest would suddenly exceed 100% of float. BITA has $1.4 billion of cash sitting on its balance sheet to execute a mere $150 million buyback. The buyback was stated to be within the next eight (8) months.

Bitauto has deep backing from the biggest tech giants in China, including Tencent, Baidu and JD.com. Their familiar descriptors “The Facebook of China”, “The Google of China and “The Amazon of China” are well worn clichés but they are both accurate and highly relevant to BITA. Their ownership and involvement in both BITA and its largest subsidiary Yixin (HK 2858) is far larger and far more involved than the the market realizes. More than 80% of BITA’s tradable float is now gone and they already own roughly half of the Yixin subsidiary. The tech investors acted as a group, purchasing together via a large special purpose vehicle (“SPV”). They are insiders and their shares cannot be easily sold.

BITA’s founder and chairman William Bin Li also happens to be chairman and founder of electric vehicle maker NIO Motors. NIO is slated to come public on the NYSE within months in a $2 billon IPO which would value NIO at $15 billion. By 2020, NIO has stated that it will be selling electric cars in the US in direct competition with Tesla. More recently, Mr. Li was also appointed as chairman of Dida Chuxing AKA “The Uber of China”. Mr Li is currently owns over 10% of the outstanding shares of BITA. Mr. Li is very visibly employing the same tactics and technology approaches used by Apple and FB to conquer all market share in each of his multiple businesses.

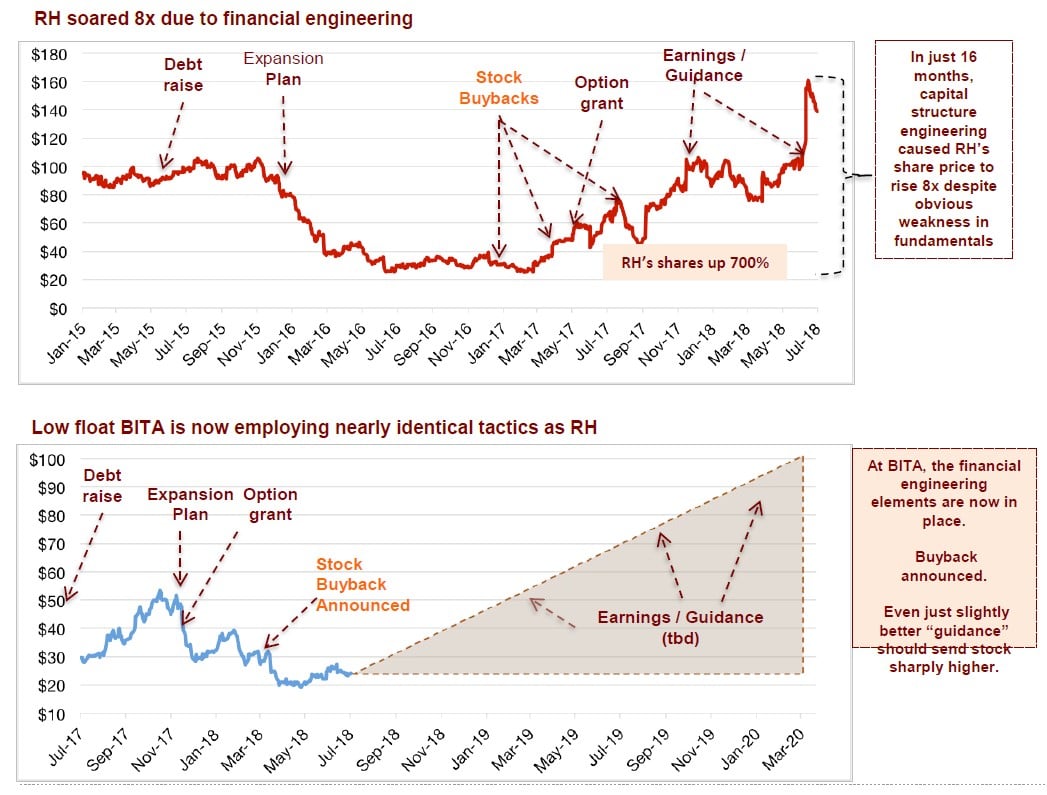

With RH, it was “capital structure engineering” that took the stock from $20 in 2017 to $160 in recent weeks. RH was an “8 bagger” from its lows despite its visibly weak fundamentals. The upside with Bitauto is vastly greater than what we saw with RH, for two reasons. First, the capital structure engineering is far more aggressive with BITA than it ever was with RH. This includes the same sequenced tactics seen at RH: leverage, float reduction, equity/option grants and a share buyback, all coupled with an announced expansion plan. Second, in contrast to RH’s weak fundamentals, the business prospects and cash generation for BITA are extremely strong. This can be clearly seen by comparing BITA to its competitor Autohome. BITA is now rapidly surpassing Autohome in revenues and growth. Yet Autohome is valued at over $12 billion. The only reason for BITA’s bottom line weakness is that it continues to spend aggressively to secure even more growth. This expensive land grab tactic is exactly what Facebook was doing at the time of its IPO in 2012, and its shares were similarly pummeled down to $17. FB currently trades at around $200.

The auto market in China continues to be one of the largest, fasting growing and most profitable consumer segments in the world. This is why Bitauto continues to grow revenues at over 50% per year for the past five years, even while keeping gross margins steady at 60-80%. The partnerships with the Chinese tech giants goes both ways. Not only are they eager to secure a piece of BITA’s fast growing penetration into this market, but they are also actively sharing their own mass targeted data with BITA to fuel BITA’s growth even further.

BITA to $240. The long thesis.

The transformation of BITA. Bitauto (BITA) is an AdTech company located in Beijing which focuses on advertising, financing and technology driven services within the auto sector in China. BITA trades on the NYSE and has a market cap of $1.7 billion. BITA’s shares have recently fallen from $40 to around $25 as Wall Street has been concerned about rising expenses which have hit the bottom line. By contrast, BITA’s competitor Autohome has minimized current expenses to maximize current profits and is currently valued at over $12 billion. But because of the low spending, Autohome’s revenue growth has stagnated at just 4%. BITA continues to grow revenue at around 50% per year and its total revenues are now 52% greater than Autohome. (Link, Link)

What’s about to happen with BITA. Bitauto is now being quietly transformed into a Facebook-style data aggregation platform using Big Data and AI for targeted monetization into the largest and most profitable auto market in the world. The profit potential is staggering. This is why tech giants Tencent, JD.com and Baidu have been aggressively pouring new money into BITA (and not ATHM) in multiple rounds of successive financings. More than 80% of the float of BITA is now locked up. In addition, these tech giants have also been aggressively investing in BITA’s largest subsidiary, Yixin. They now also own roughly half of BITA’s largest subsidiary.

China’s digital gold rush. The digital gold rush in China is on a scale that has no true parallel in the West. In the US, there are now government enquiries into Facbook’s collection and use of targeted personal data. But in China, the tech giants have a much closer relationship with the government. Their ability to collect precision targeted data on China’s 1.5 billion people is actually highly encouraged rather than throttled . And there are far fewer limitations on monetizing this data. BITA is not the biggest player in the digital gold rush. But Bitauto and its chairman William Bin Li are now playing a critical role. The huge investments into BITA by Tencent, JD.com and Baidu are strategic investments being used to intertwine the volumes of data being aggregated by BITA (and other William Bin Li companies) into the mass collection by Tencent, JD and Baidu themselves.

BITA founder William Bin Li. Aside from founding BITA, Li is also the founder and Chairman of NIO Motors. (AKA “The Tesla of China”). NIO is slated to come public on the NYSE in a $2 billion IPO within a few months, which would value the company at $15 billion William Bin Li was also recently appointed Chairman of DiDa Chuxing (AKA “The Uber of China”). Mr. Li owns just over 10% of BITA.

Electric car start-up NIO prepares US$2b IPO in Tesla’s home turf (South China Morning Post, Feb 2018)

Chinese EV Startup NIO’s Founder Li Bin Joins Ride-Sharing Platform Dida Chuxing as Chairman (SCMP, Apr 2018)

Facebook. Big Data. AI. Facebook (FB) IPO’d in 2012 at $38. But Wall Street could only see that recent expenses were too high and current profits were too low. (Link). Wall Street failed to grasp the true value of Big Data and AI for collection and monetization of mass targeted data. They pummeled the stock straight down to $17. Facebook is now at nearly $200 and is one of the most valuable companies in the world. The commercial value of such micro targeted consumer data is now apparent to everyone. Zuckerberg knew it all along.

Monetization at BITA is much narrower than FB…but also far more concentrated than FB. BITA is not trying to be Facebook. This is obvious. Bitauto is entirely concentrated within the automotive sector in China. But in dollar terms, this narrow niche of “selling cars in China” also happens to be one of the the largest, fastest growing and most profitable consumer markets in the world. (See page 16)

Much of FB’s daily traffic consists of non-commercial personal activity which is not directly monetize-able . But with BITA, all of its traffic is inherently of much greater “value density”. Any time someone visits or searches on a BITA site or ad, they are revealing a specific interest in buying a very specific big ticket item. On top of that, they indirectly reveal volumes of demographic data such as location (wealthy vs. non wealthy) and other personal demographic data. This information is collected, aggregated, shared and deployed amongst and between BITA and its tech-giant partners (Tencent, JD, Baidu). As with Facebook, the monetization value of such detailed and targeted data is astounding, especially in a booming consumer segment like China’s auto market in China.

BITA is employing textbook tactics in capital structure engineering

The tactics that took RH up 8x since last year. The driving factor which took RH from $20 in 2017 to $160 in recent weeks was textbook capital structure engineering. My report from November 3rd, 2017 explained how the process would unfold. The CEOs posturing in 2017 was transparent and the initial move on RH occurred on the exact day I had predicted. Starting on November 16th, RH shot up by 30% to as high as $107. It bounced up and down for the next few months, but then more recently it shot above $160. As I explained in my report, the explicit target for the CEO was precisely $150. This can be clearly seen from the strike prices on his recent and very massive option grant. This $150 threshold is then re-confirmed by looking at the strike prices of the “call spreads” which RH purchased against its convertible bonds. The low strike was $117 and the high strike was $180. Anyone who found themselves surprised by the move to $160 (right in the middle of those strikes) should stop shorting stocks until they figure this out. As I have said before, RH’s CEO has all the tools he needs to manifest the $150 going forward so that he can realize his nine figure pay day.

Long $RH – $RH Will Spike Much, Much Higher Very, Very Soon (MoxReports, Nov 3, 2017)

Increasing use of capital structure engineering. This wealth generation through capital structure engineering is a theme being copied by billionaires around the globe to generate staggering returns. But the cookie cutter formula being used by William Bin Li with Bitauto is even more aggressive than what we have seen from billionaires like Oprah Winfrey and Carl Icahn in the US.

Oprah’s Weight Watchers Stake Worth Half a Billion (Investopedia, June 2018)

Carl Icahn Claims $1 Billion Profit From Reduced Herbalife Stake (24/7 Wall St, May 2018)

Once BITA’s float was locked down, Bitauto began aggressively levering up, issuing debt to embark on an aggressive expansion strategy. Just as debt surged on the balance sheet, the income statement also saw a spike in SG&A expense. The resulting share price weakness should have been entirely predictable. Even as BITA’s share price fell, the company then suddenly incurred a staggering $179 million in “share based compensation” (stock and options grants, including BITA and Yixin). In previous years the company had incurred less than $15 million of stock based compensation expense.

With the float rapidly disappearing, increasing short interest quietly ended up amounting to over 80% of the remaining float. But because float numbers are not pulling in to Bloomberg, many investors have been unaware of this 80% short vs. float.

BITA announces share buyback. With the stock testing multi year lows and with option grants now in place, BITA then announced a $150 million share buyback. In fact, even a fraction of this buyback would cause the short interest to rise above 100% of the remaining float. The press release states that the buyback is for the 12 months from March 2018, so there only are eight months left. And even before any buyback, once the market figure outs that short interest is above 80%, there could be upside volatility just for this reason alone.

Bitauto Board of Directors Approves $150 Million Share Repurchase Program (Press release)

Here is the kicker. We have now seen the same phenomenon repeatedly. With “engineered” stocks like RH and Weight Watchers (WTW), the only thing necessary to send the stock up by a quick 5-10x was the release of earnings (or even mere “guidance”) that was just “slightly less awful than expected”. The same has been true for many other “billionaire stocks” such as Herbalife (HLF), Hertz (HTZ) and Dillard’s (DDS).

But with Bitauto, there is actually vastly more upside than many of these earlier engineered stock plays. This is because the fundamental prospects for BITA’s actual business are far stronger than what the market comprehends. BITA’s newly emerging Big Data/AI/Aggregation/Targeting model is being entirely missed. When BITA announces strong numbers in a Facebook-like surprise, the upward move will be greatly amplified by the engineered combination of low float + high short + heavy upside leverage.

Article by Mox Reports

See the full PDF below.

{kind=link}