- Kwasi Kwarteng’s mini-budget was announced a year ago – on 23 September 2022.

- In the wake of the announcement, the market was alarmed that inflation would run riot, which caused government bonds to drop dramatically. This pushed interest rates on fixed mortgage through the roof, and made annuities and savings rates far more attractive.

- So where are we a year down the track?

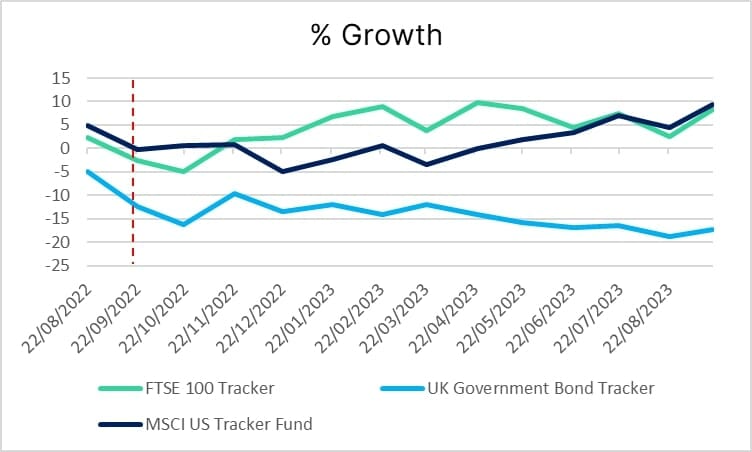

UK’s Economic Growth

Susannah Streeter, head of money and markets, Hargreaves Lansdown:

‘’The mini-budget sparked a wave of apprehension about the UK’s economic prospects, with investors baulking at the fast and loose plan for big tax cuts to stimulate spending at a time when inflation was running amok. Britain was compared to an emerging market, turning itself into a submerging market, so the price of gilts plummeted and yields jumped – reflecting the premium investors were demanding to hold UK government debt. The firestorm of uncertainty saw a further seeping away of confidence in companies listed on the FTSE 100, pushing the index below the psychologically important 7,000 mark.

U-turns, resignations of Kwarteng, then Truss and the appointment of a new Chancellor in Jeremy Hunt did help calm the turmoil and bit by bit more confidence was restored, helping bolster gilt prices and helping the FTSE 100 gain rapid ground. But the recent stubbornness of inflation, even without the Trussenomics tax cuts, has taken investors by surprise. This has caused another summer spike in pessimism about the UK’s prospects, putting fresh upwards pressure on gilt yields and stopping the FTSE 100 regaining the highs above 8000 reached in February 2023.

Liz Truss is still banging the tax cut drum from the back benches, but despite inflation creeping downwards it is still more than three times above the target, so her demands are likely to get short shrift. While stimulus may well be needed to boost a struggling economy, long-term investment to increase Britain’s infrastructure and competitiveness is more likely to help Britain regain its mojo.’’

Source: Hargreaves Lansdown

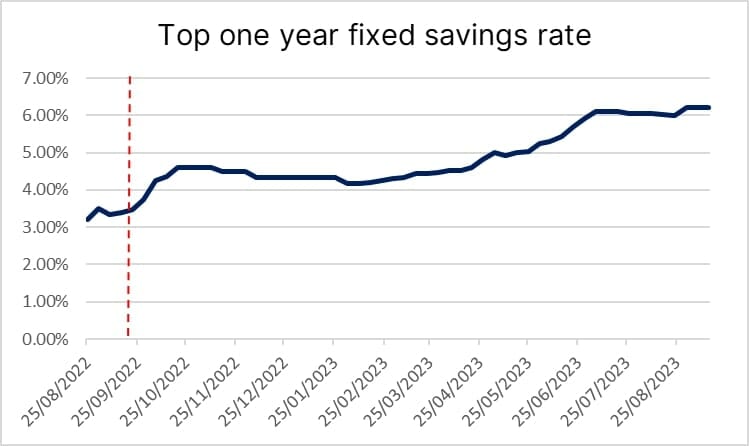

Rise In Savings Rates

Sarah Coles, head of personal finance, Hargreaves Lansdown:

“The mini-budget caused carnage in many areas of people’s finances, but for savers, it was another story entirely. Savings rates had been gradually rising with each Bank of England rate hike, but the announcement accelerated this process significantly. The market started to suspect that an awful lot more rate hikes would be needed in order to get inflation under control, so they started pricing more of them in.

Savings rates don’t tend to move as far and as fast as mortgage rates, because nobody wants to move too far ahead of the rest of the market and attract too much cash at too high a price. Instead, they take it in turns to nudge ahead of one another. It means we saw a month-long speed-shuffle.

It hasn’t been a smooth path upwards, as rate expectations have fluctuated and the market has responded. However, since the spring, every indication of sticky inflation has pushed the market ever-higher. As the rate rise hiking cycle looks to be coming to an end, we’re not expecting fixed rates to rise much further from here. However, the cumulative effect of the rises in the past year have been significant.

The best fixed rates are now around double what they were before Kwasi Kwarteng delivered his fateful speech. Someone fixing for a year just before the announcement might get 3.48% on £30,000, and earn £1,061 in interest. Someone fixing £30,000 for a year today, might get 6.2%, and earn £1,914 – £853 more.

It has had a striking impact on saver behaviour too, with a wave of people moving into fixed rate accounts in the final months of 2022, to take advantage of the mini-budget boost. Active Savings statistics show that last September, savings being fixed were up around 75% from a year earlier. This intensified in October and November, when money flooding into fixed rates more than tripled compared to a year earlier.

This was reflected across the wider savings market. Given that the most common period to fix for is a year, it means we’re expecting an awful lot of that to mature soon. There’s an estimated £32-35 billion maturing in the next six months, so savers will be hoping that rates hold near the top for as long as possible, to give them a chance to fix.”

Source: Moneyfacts

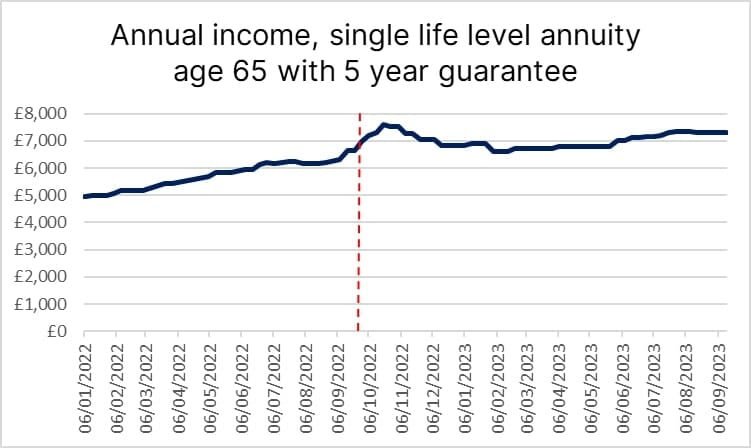

Annuity Rates Skyrocket

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown:

“After years in the doldrums annuity incomes had already been on an upward trend in the months leading up to the mini-budget, as the Bank of England began its interest rate hiking cycle. However, the chaos unleashed on the bond market in the immediate aftermath of the announcements sent annuity rates rocketing skyward.

In September a 65-year-old with a £100,000 pension could get up to £6,637 per year from an annuity* but by the end of October this had surged to £7,586 – levels not seen since before the Global Financial Crisis. As the market settled, rates did start to gently drift back down again with the same person now able to get up to £7,317 per year from their £100,000 pension proving to be a rare good news story in the current economic gloom.”

*Single life, level, five year guarantee

Source: Hargreaves Lansdown

Sarah Coles:

“The mini-budget drove a coach and horses through the fixed rate mortgage market. In the immediate aftermath, rate expectations were climbing so fast that lenders were finding it impossible to price mortgages, and they ended up having to pull them and wait for the dust to settle.

When they returned, they were at a much higher rate, and they continued to climb. Moneyfacts figures show some fluctuations, and in early 2023, they started to drop back. However, another surge in spring and summer this year took average rates over the level they hit in the wake of the mini–budget. There wasn’t anything like the same sense of panic around at the time, because the return to the peak had been more gradual, and there was no sense that it was out of control. However, it took a toll on buyer demand, and is likely to have hit house prices.

Today we’re seeing fixed rate mortgages start to drop back again, but the rise over this period has still been pretty horrible. On the date of the announcement, the average two-year fixed rate mortgage was at less than 5%, and today it’s over 6.5%.

The impact on homeowners will only be felt gradually, as people come to the end of their fixed period and face the horror of remortgaging. However, at that point, they’ll be reeling. The HL Savings & Resilience Barometer found that as higher rates feed through, over the next 12 months, 26% of mortgage holders will be at risk of arrears. Around 230,000 of those people have cash savings that cover less than three months of essential spending – so are classed as being at high risk; and 470,000 also have unsustainable spending, so are considered to be at critical risk.”