Lyrical Asset Management commentary for the year ended December 2020, titled, “EAFE Value Index.”

Q4 2020 hedge fund letters, conferences and more

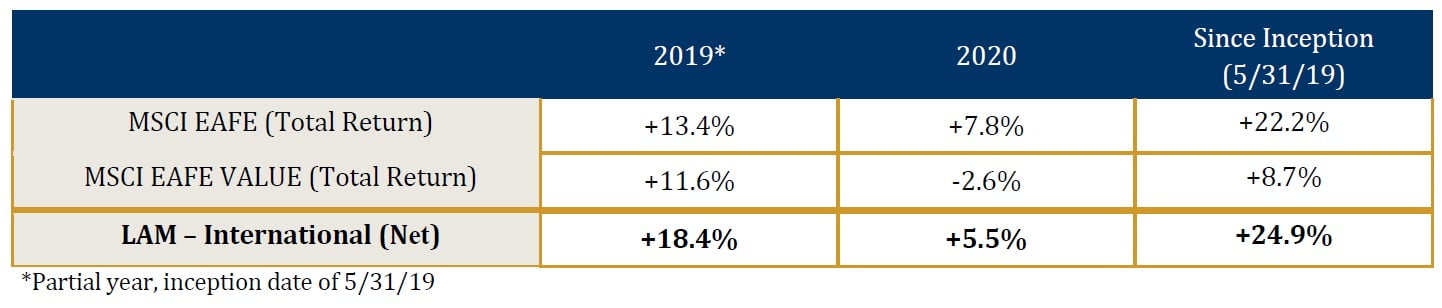

The pandemic tested our mettle, but our strategy and the companies in our portfolio navigated well through the volatile environment. We seek to own attractive businesses at attractive valuations, and this discipline helped us manage confidently through a challenging time. Despite a rocky start to 2020, our portfolio advanced 5.5% (net) for the year, outperforming our Foreign Large Value mutual fund category peers by 460bps.

After a bruising first quarter for international value stocks, it would have been hard to predict a solid gain in the portfolio this year. The cheapest stocks were hit especially hard at the onset of the pandemic, and the first quarter of 2020 marked the only quarter our strategy has underperformed the EAFE index since our inception in June of 2019. Most of the underperformance came during the first three weeks of March, before a sharp recovery. In the first quarter, we underperformed the EAFE by nine percentage points, but since then we outperformed by 15 percentage points, ending the year 230bps behind the EAFE, but 810bps ahead of our style benchmark, the EAFE Value.

While we managed through the year with a mid-single-digit return, value in general did not fare as well. We believe this unusual decline in cheap stocks has created an incredibly attractive opportunity set. Value stocks are now trading with historically wide spreads versus the market, which has typically led to sustained periods of outperformance. We have performed well in a difficult period, and we are looking forward to our results when the value winds are at our back.

Thrive And Survive

While the COVID virus created an economic crisis like no other, we had good reason to believe that, on average, there was no more risk from the pandemic in our portfolio than in the overall market. At Lyrical, we have three requirements for every investment – Value, Quality, and Analyzability, or in other words, Inexpensive, Good, and Simple. One of the reasons we want to buy quality / good businesses is because they are resilient and can adapt. When you own a stock for 7-8 years on average, as Lyrical has done historically, it is likely you will own it through a recession. This is why a key part of our due diligence entails understanding how a business will respond to a weak economic environment. We want to own businesses that can not only thrive when times are good but also easily survive when times are tough.

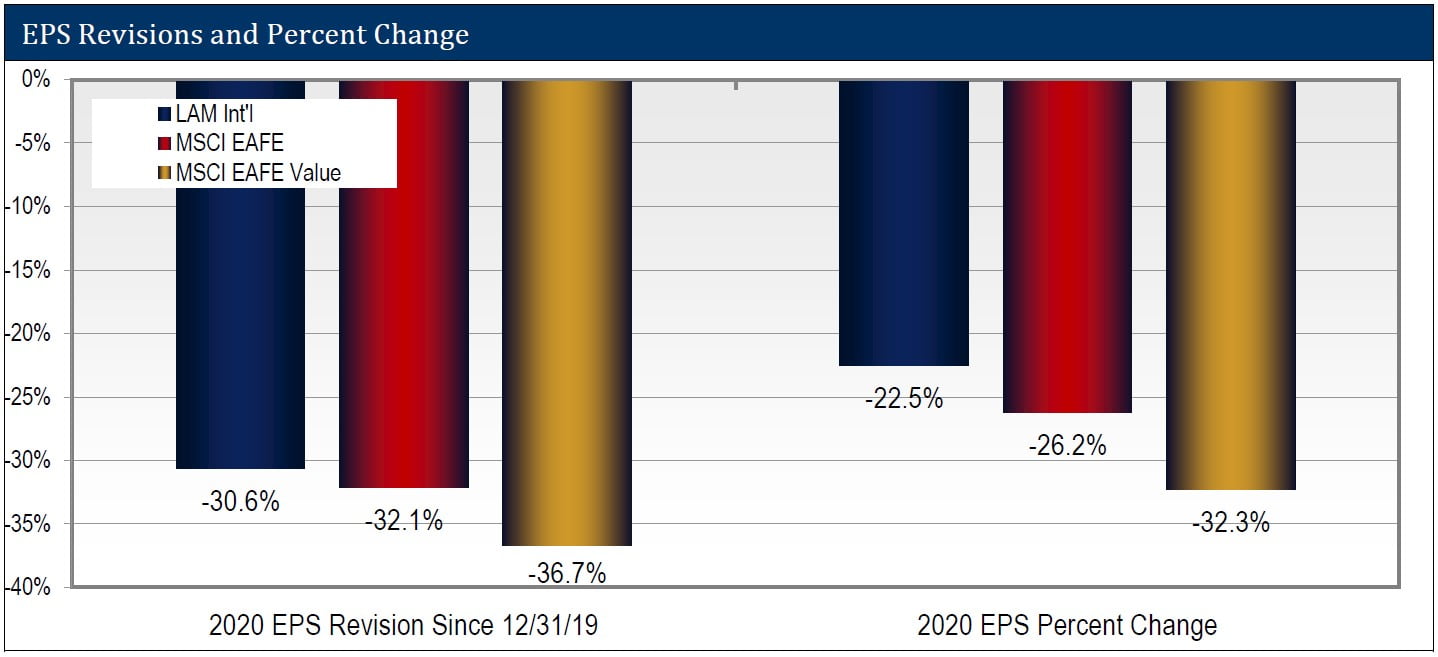

Our disciplined underwriting paid off in 2020, as our portfolio had better fundamentals, as indicated by earnings and earnings revisions, than the market and the value index. As shown below, 2020 EPS revisions and earnings for our portfolio declined less than both the EAFE and EAFE Value index. This did not surprise us. We invest in companies with durable competitive advantages, flexible cost structures, strong balance sheets, and healthy free cash flow. These qualities allow companies to persevere during economic setbacks. While we did not know what shape this particular crisis would take, we had already stress-tested our companies by analyzing their performance through extreme periods like the Global Financial Crisis, when our companies’ earnings also held up better than the market.

Despite the superior resiliency of the businesses we own, many of our stocks were punished worse than the market during the panic sell-off. As of March 18, 2020, 71% of our stocks were underperforming the MSCI EAFE Index, down an average of 40.5% year-to-date, compared to down 32% for the EAFE.

Given the outperformance of our portfolio’s fundamentals, we think the early sell-off in our stocks is yet another example of the market behaving emotionally. Falling stock prices can create a vicious cycle, as they scare more investors into selling, which then causes prices to fall more. Stock prices go from being an indication of a company’s worth to reflecting pure emotion. Of course, our companies were hurt by the pandemic, but, evidently, they were hurt less than the market. Furthermore, our businesses’ long-term earnings power has been mostly unaffected and, in some cases, has improved because of COVID-19.

Some Clear Examples

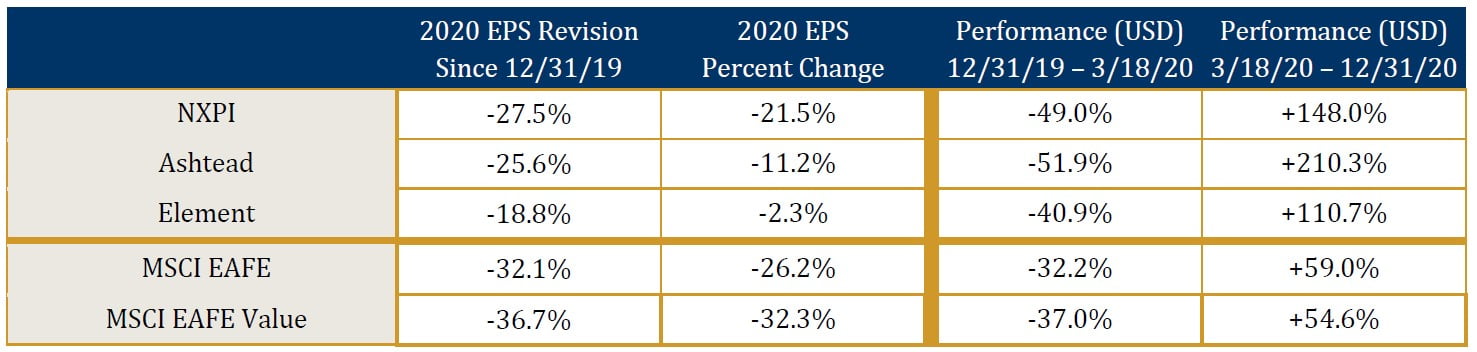

Let’s look beyond the aggregate portfolio data to examine a few stock examples that help show how the market overreacted (although, explaining why isn’t as easy). Below, we show the 2020 earnings estimate revisions and earnings change for three of our companies—NXPI, Ashtead, and Element—compared to the market. We also show that these stocks underperformed significantly through March 18th, only to rebound dramatically in the ensuing months.

NXPI is a semiconductor company with the #1 position in radar technology for auto collision avoidance and autonomous driving. For 2020, EPS is expected to decline 22%, due in large part to global auto production shutdowns that occurred during the spring. Longer-term, little has changed, and the current 2022 consensus EPS estimate is near where it was prior to the pandemic and 67% higher than 2020. Through March 18th, NXPI was down 49%, which we believe was driven by the company’s exposure to the then-struggling auto sector. At that point, it was hard to know when auto supply chains would start up again. Regardless of how long the shutdown endured, it was easy to see that NXPI would grow secularly over the long-haul as more vehicles employ NXPI chips for collision avoidance, battery management, and more. We capitalized on the opportunity and purchased the stock on March 16.

Ashtead, based in the U.K., is the #2 tool rental equipment company in North America and has been a position in our portfolio since inception. Early in the pandemic, there was a concern that demand would collapse, and the stock price dropped 53% in less than one month. We did not know exactly how far demand would fall, but we knew the business would benefit from countercyclical cashflows. Because of Ashtead’s scale as the #2 player, the company has negotiating leverage with suppliers. As a result, they can cut their new equipment orders with just 45-60 days notice. We saw the company cut capex by about 80% in the financial crisis, and we knew Ashtead could once again pull the same lever in an abrupt slowdown. This is exactly what happened. Even though EPS is expected to decline 11% in 2020, free cash flow is expected to increase 72%, to a record £1.1 billion. The stock initially sold off like other industrial cyclicals before the market realized Ashtead’s resiliency. From the bottom, the stock gained 210%, and it ended up 49% on the year. We were confident the company could survive a downturn, and now we once again should get the rewards from the company thriving in a rebound. Ashtead is a secular winner, benefitting from scale and technology advantages that allow it to consistently take share from the mom-and-pop businesses that still control most of the market.

Element is a leading global commercial vehicle fleet management business. The company manages mission-critical cars, vans, and trucks for a diverse set of customers, including Amazon, whose businesses are heavily dependent on their fleets. While Element provides many services for its customers—purchasing, repair, and fuel to name a few—it does not bear any residual risk for the vehicles it leases to them. This means that even a sharp downturn is unlikely to impair the business. In the financial crisis, credit losses peaked at around 10bps. The company’s relationships are sticky and revenues are recurring. Suffice it to say, we were surprised to see the stock down 41% in the early part of the year, and we took advantage of the dislocation to make our investment on April 7. With fewer corporate vans on the road, service revenue fell 8% year-over-year in the second quarter, but by the third quarter service revenue was already rebounding and was +2% compared to the prior year. For all of 2020, EPS fell only 2%, a commendable result although far less than original expectations for 20% EPS growth. While the stock has more than doubled off the bottom, we are still in the middle innings of a shift to outsourced vehicle management that we think will drive double-digit earnings growth for years to come.

The examples above illustrate how owning resilient businesses, supported by detailed fundamental analysis, can make it easier to maintain our conviction even in a panic-driven market. A list of all of our recommendations is available upon request.

EAFE Value Index: The Reports Of Value’s Demise Are Greatly Exagerrated

While our portfolio has fared well relative to the MSCI EAFE, the MSCI EAFE Value Index has significantly underperformed. In fact, the EAFE Value Index has been underperforming for so long that we are frequently asked if value investing is broken. We can understand the question. Since 2017, the EAFE Value Index has underperformed the EAFE by 25 percentage points. Furthermore, the EAFE Value Index has underperformed the EAFE in 10 of the past 14 years.

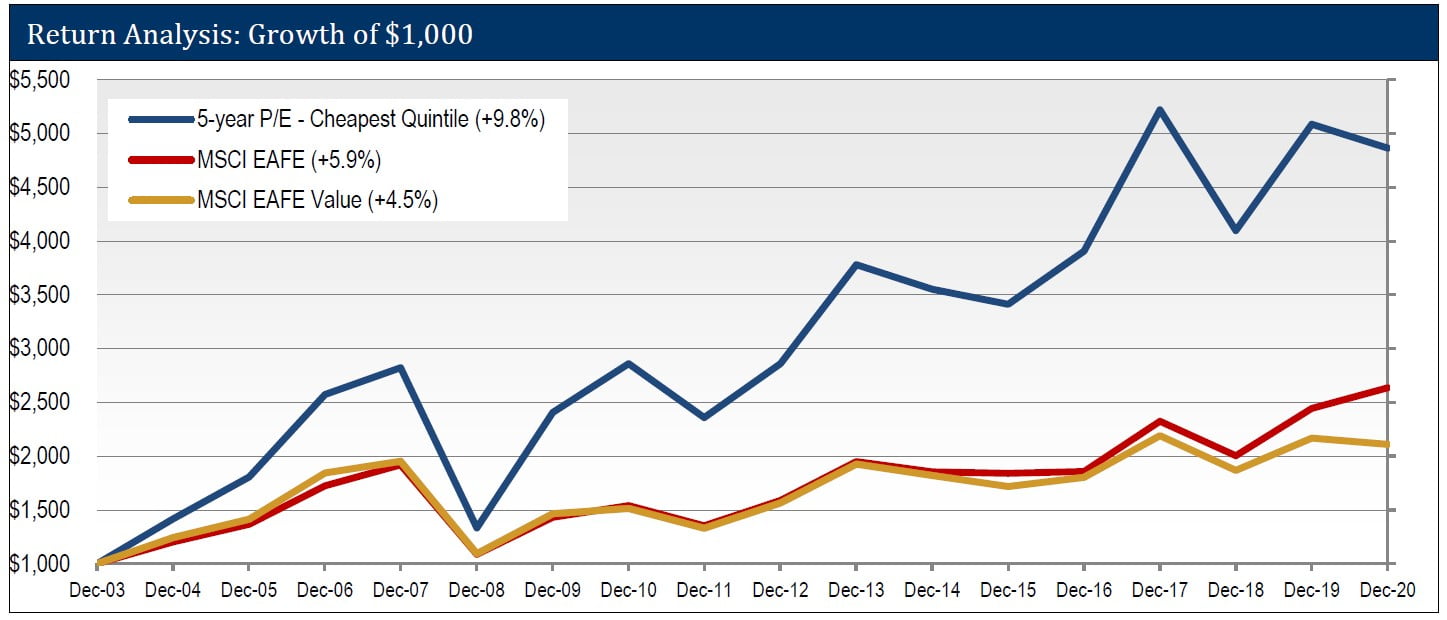

It is our view, though, that it is the value index that may be broken, but not value investing. Instead of looking at the performance of the MSCI EAFE Value Index, if you look at the performance of the cheapest stocks in the non-U.S. developed markets, you see a very different picture emerge. The cheapest stocks have outperformed the MSCI EAFE Value in 10 of the past 15 years. As you can see above, the cheapest quintile of our international universe has outperformed the MSCI EAFE and EAFE Value indices by 390bps and 530bps, respectively per annum, going back to 2004 which is as far back as we have reliable data.

Read the full commentary here.