Knoll Inc. (KNL: $18/share) – Maintaining Long Position – Down 24% vs. S&P +3%

Knoll Inc. was selected as a Long Idea on 4/24/17. At the time of the report, the stock received a Very Attractive rating. KNL was downgraded to Neutral by our rating system on 8/10/17 due to lower profitability in its most recent 10-Q. Specifically, NOPAT margin declined to 7% (TTM) from 8% and return on invested capital (ROIC) fell to 10% TTM from 11% in fiscal year 2016.

Also read:

- Q2/H1 Hedge Fund Letters – Letters, Conferences, Calls, And More

- Hedge Fund of funds Business Keeps Dying Every Year

- Baupost Letter Points To Concern Over Risk Parity, Systematic Strategies During Crisis

- AI Hedge Fund Robots Beating Their Human Masters

Despite the rating change, we are maintaining our long position due to an improved 2H17 outlook, the firm’s profit diversification relative to competitors, and the stock’s low valuation. The current 0.9 price-to-economic book value ratio (PEBV) means KNL is priced for a permanent 10% decline in after-tax profits (NOPAT).

The stock’s recent underperformance can be attributed to disappointing earnings across the industry. Knoll (KNL), Corporation (HNI) and Steelcase (SCS) all fell short of earnings expectations in the most recent quarter and have seen their stocks underperform year-to-date. Both KNL and SCS noted that uncertainty surrounding economic and tax policies were delaying planned corporate investments and building pent up demand.

While our original thesis has proven too optimistic in the short run due to the industry slowdown, we believe KNL remains best positioned to benefit from the expected improvement in 2H17 industry trends.

Per Figure 1, KNL’s return on invested capital (ROIC) and NOPAT margins remain above the competition following recent earnings reports. Additionally, KNL’s Studio segment, which has higher operating margins than its Office segment, helps diversify its business across different markets.

Figure 1: KNL’s Top Profitability Among Competition

Sources: New Constructs, LLC and company filings.

KNL management expects efficiency improvement efforts to pay off in 2H17. Clarification on tax policies could also open the flood gates for pent up demand. KNL remains positioned to profit from expanded corporate investments and has a competitive advantage over market participants.

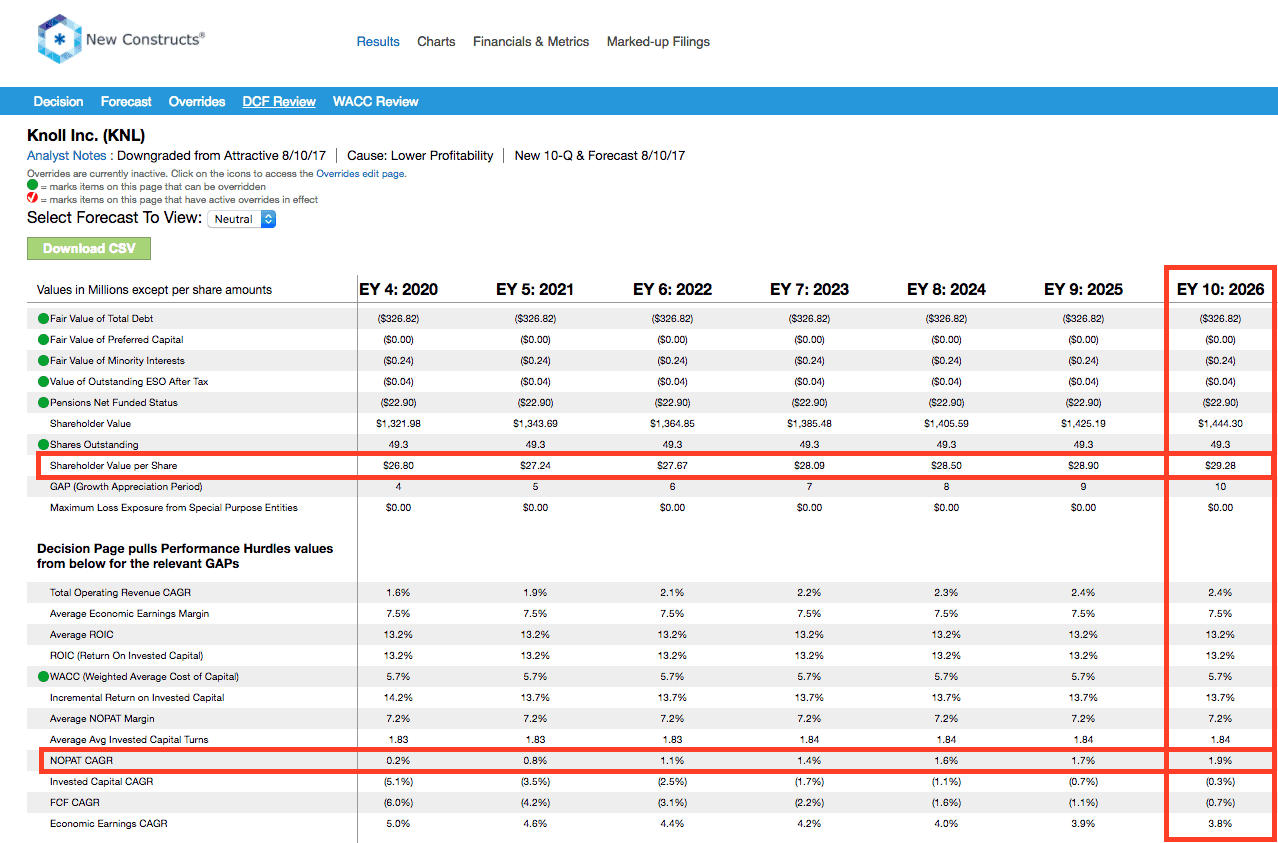

Further, the low valuation combined with industry leading fundamentals continues to present an attractive risk/reward trade-off for investors. As such, the recent pullback represents an opportunity to buy a quality stock in a beaten down industry. If KNL can maintain TTM NOPAT margins (7%) and grow NOPAT by just 2% compounded annually over the next decade, the stock is worth $29/share today – a 61% upside.

Figure 2: KNL Stock Price and Risk/Reward Rating History

Sources: New Constructs, LLC and company filings

This article originally published on August 31, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, style, or theme.

Article by Kyle Guske II, New Constructs

{kind=link}

{kind=link}