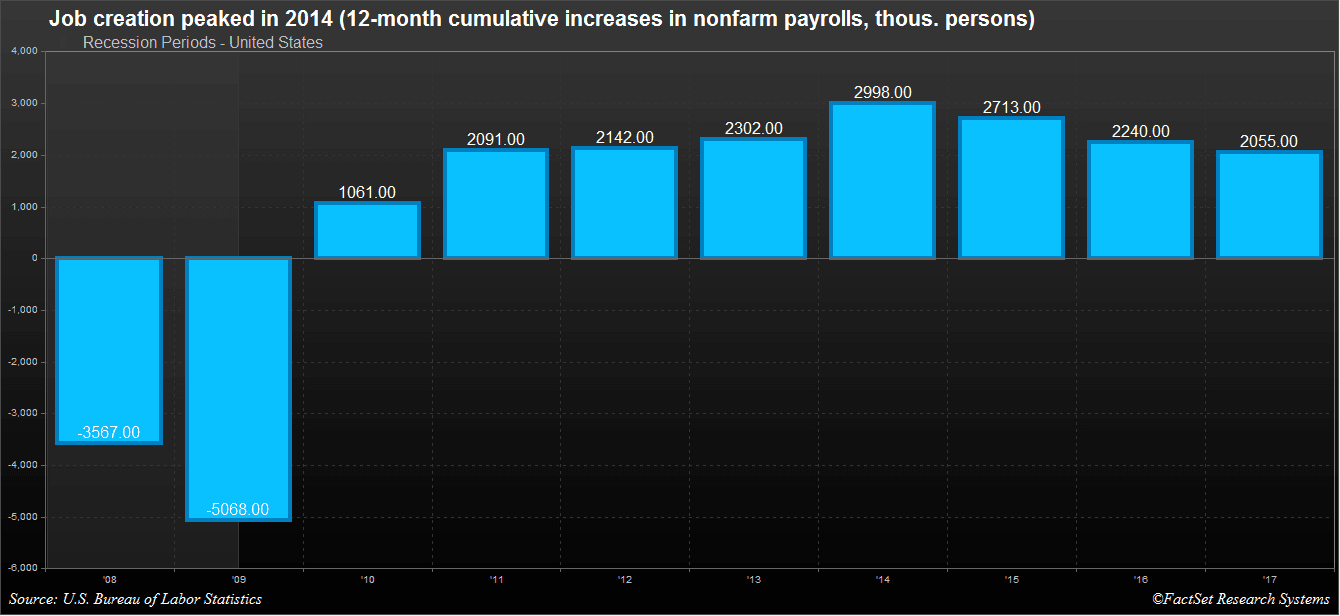

Last week’s December Employment Situation release showed continued job market strength as we ended 2017. However, the December increase in nonfarm payrolls disappointed, with just 148,000 jobs added during the month, below expectations for an 189,000 increase and the slowest gain since September’s hurricane-depressed 38,000. Still, December’s results marked 87 straight months of positive job gains.

[REITs]Throughout 2017, the job growth numbers continued to ease, not surprising for an expansion that is now 8.5 years old and with an unemployment rate at a 17-year low of 4.1%. While still respectable, the 12-month increase in nonfarm payrolls that we saw in 2017 was the slowest in seven years, with 2.1 million jobs added, a monthly average of 171,250. Digging into the numbers, what were the underlying factors defining the employment picture in this expansion, especially as we complete the ninth year of growth? Are there any signs that this expansion may be coming to an end?

Businesses Are Constrained by a Lack of Qualified Applicants

At this point in the current expansion, it’s not surprising that companies are having trouble filling open positions. According to the National Federation of Independent Business, the percentage of small businesses who are finding few or no qualified applicants for job openings hit an all-time high in December 2017 of 54% (data series starts in January 2004).

We also see this trend in the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS), a data set closely followed by the Federal Reserve, including Chair Janet Yellen. Several of the statistics from this release are part of Yellen’s “dashboard” of job market indicators, which she uses to gauge the strength of the economy.

Over most of the history of JOLTS (back to December 2000), the hires rate (ratio of hires to total employment) exceeds the job openings rate (ratio of job openings to total employment). However, in 2015 we began to see this pattern reverse. During 2017, the job openings rate was higher than the hires rate in 10 out of 11 months, and the two were identical in one month. This points to a growing skills mismatch in the labor force.

Insight/2018/1.2018/1.11.2018_Econ/The%20job%20opening%20rate%20exceeds%20the%20percentage%20of%20new%20hires%20in%202018.png?t=1515695871397 "The job opening rate exceeds the percentage of new hires in 2018")

Job Gains in Services Dominate, with a Trend Toward Temp Workers

However, despite the lack of qualified applicants for many job openings, we still haven’t seen a resultant increase in wages, especially considering we are in the ninth year of an expansion. In 2010, early in the expansion, private average hourly earnings rose by 1.86%; annual earnings growth in 2016 and 2017 averaged just 2.6%.

As we discussed back in April 2017, the persistent mediocre wage growth can largely be explained by looking at the mix of jobs created during this expansion. Over the last 8.5 years (since the official end of the last recession in June 2009), the U.S. added 16.4 million jobs to nonfarm payrolls, a 12.5% increase. Jobs in goods-producing industries only accounted for 1.8 million of those jobs, while private services made up the bulk of the increase, with 14.8 million jobs added. With the biggest job gains registered in the service sector, largely in lower-wage sectors, it’s not a surprise that overall wage growth has been subdued.

| Employment by Industry – Changes During Current Expansion | ||||

| (Thousands of Persons) | ||||

| Dec 2017 | Jun 2009 | Change | % Change | |

| Total Nonfarm | 147,380 | 131,021 | 16,359 | 12.5% |

| Total Private | 125,039 | 108,445 | 16,594 | 15.3% |

| Goods-Producing | 20,259 | 18,422 | 1,837 | 10.0% |

| Mining & Logging | 727 | 686 | 41 | 6.0% |

| Construction | 6,993 | 6,010 | 983 | 16.4% |

| Manufacturing | 12,539 | 11,726 | 813 | 6.9% |

| Private Service-Providing | 104,780 | 90,023 | 14,757 | 16.4% |

| Trade, Transportation and Utilities | 27,448 | 24,908 | 2,540 | 10.2% |

| Information | 2,722 | 2,796 | -74 | -2.6% |

| Financial Activities | 8,498 | 7,821 | 677 | 8.7% |

| Professional and Business Services | 20,943 | 16,436 | 4,507 | 27.4% |

| Education and Health Services | 23,309 | 19,614 | 3,695 | 18.8% |

| Leisure and Hospitality | 16,050 | 13,076 | 2,974 | 22.7% |

| Other Services | 5,810 | 5,372 | 438 | 8.2% |

| Government | 22,341 | 22,576 | -235 | -1.0% |

Digging into the payroll numbers a bit more, the fastest growing services sector has been Professional and Business Services, with employment growth of 27.4% growth during this expansion. This highlights an interesting trend. The largest and fastest growing sub-component of these services is Temporary Help Services; over the last 8.5 years, this category has soared from 1.75 million jobs to 3.1 million jobs, a 76.8% increase.

The temporary help services industry is made up of businesses that supply workers to client companies, usually for limited periods of time. Temporary help services employment is at an all-time high, which would appear to represent a significant shift in company hiring patterns. One explanation is that businesses are moving away from hiring employees directly and toward using contract employment agencies in order to boost profits and shareholder value. This allows them to save money on employee benefits and gives them more staffing flexibility. When business slows, it is much easier and cheaper to drop workers when hiring through an employment agency. Employees of these temp employment agencies earn a lower wage than other industries. In November 2017, the average hourly earnings for temporary help services was $17.69, compared to $26.26 for all service jobs.

Because of the flexible staffing arrangements that these temp agencies provide, it makes sense that hiring temp employees enables companies to quickly adapt during economic downturns and recoveries. In fact, employment in this category appears to be a good leading indicator for the U.S. economy as shown in the chart below. Since we only have this data back to January 1990, we only have two recessions to study, but before both the 2001 and 2008-2009 downturns, these temporary jobs flattened and then declined. Temporary help services jobs were up 4.6% on a year-over-year basis in December, so it looks we still have a way to go in this expansion, at least according to this indicator.

Insight/2018/1.2018/1.11.2018_Econ/Employment%20at%20Temporary%20Help%20Services%20Continues%20to%20grow%20in%202018.png?t=1515695871397 "Employment at Temporary Help Services Continues to grow in 2018")

Despite continued weak wage growth, the good news throughout this expansion has been that inflation has remained benign, hovering at or below 2% for the last six years. This creates a conundrum for the Federal Reserve in pursuing its dual mandate to “foster economic conditions that achieve both stable prices and maximum sustainable employment.” The FOMC instituted three 25 basis point rate hikes in 2017, and the Federal Reserve is expected to raise rates at least three times in 2018. As we enter 2018, the jobs picture will be a key area of focus for policymakers and will likely determine future actions.

Article by Sara Potter, FactSet