Investing in mutual funds continues to be one of the primary avenues to wealth for many investors, even as they face competition from exchange-traded funds (ETFs). As of the second quarter, there were more than $22.6 trillion US assets invested in mutual funds, according to data from the St. Louis Federal Reserve.

In this guide, we’ll show you how to invest in mutual funds, what some of the best mutual funds in 2024 are, and cover some well-known mutual fund providers.

What are mutual funds?

Mutual funds are investment vehicles that pool money from multiple investors to purchase a diversified portfolio of securities, such as stocks, bonds, or other assets. They fall into different categories based on their investment objectives and the types of assets they hold.

The diversification in mutual funds helps spread risk and potentially increase returns. Mutual funds are managed by professional fund managers who research and select investments on behalf of the fund’s shareholders. There are also index mutual funds that track a benchmark index and require less input from a manager, making them a practical complement to other strategies like exploring different ways to invest in gold.

What are the typical returns of mutual funds?

Historically, stock mutual funds have generally outperformed other asset classes over the long term, but they also come with higher volatility. Over the past 15 years, mutual funds returned an average 7.94% a year across seven categories, ranging from short-term bond funds to US large-cap stock funds, according to investment research company Morningstar.

The returns on mutual funds can vary widely depending on several factors, including:

- Fund Type: Different types of mutual funds, like stock funds, bond funds, and balanced funds, have different risk and return profiles.

- Market Conditions: The overall performance of the stock market and bond market significantly impacts the returns of mutual funds.

- Fund Manager’s Skill: The skill and experience of the fund manager can influence the fund’s performance.

- Fees: Higher fees can eat into the fund’s returns.

How do mutual funds work?

Mutual funds pool money from multiple investors to invest in a diversified portfolio of securities. When you invest in a mutual fund, you indirectly own a portion of the underlying securities. For instance, if you invest in a tech-focused fund, you’re not directly buying shares of companies like Amazon or Microsoft. Instead, you’re buying shares of the fund itself.

The fund’s share price fluctuates based on its net asset value (NAV). The NAV is calculated by dividing the total value of the fund’s assets by the number of shares outstanding. As the value of the fund’s holdings changes, so does its NAV and, consequently, its share price.

What fees do mutual funds charge?

Before investing, it’s important to consider what fees each mutual fund charges as these will erode the returns. Here the main type of costs to look at:

Expense Ratio

Also known as the operating expense ratio (OER), this is the annual cost of owning the fund’s shares. The fund company charges this fee to cover operating costs like management, administrative, custodial, distribution (sometimes called 12b-1 fees) and marketing expenses. It’s expressed as a percentage of the fund’s net assets.

Example: If you have $5,000 invested in a fund with an expense ratio of 0.5%, you will pay $25 a year.

Shareholder expenses

Sales commissions and other transaction costs that occur when you buy or sell mutual fund shares. Note that different funds will have different pricing structures, and it’s important to get clarity about these expenses before investing.

Some of the typical shareholder cost items that can occur are:

- Sales load: This is a transaction fee that’s similar to the commission a brokerage would charge on purchases. It compensates the brokers the fund uses to buy assets.

- Redemption charge: It occurs when you redeem your shares in the mutual fund.

- Exchange fee: Some funds charge this when swapping your fund shares for the shares of a different fund within the same fund group.

- Account fee: Some funds may charge you for maintaining your accounts, sometimes when the account value is below a certain limit.

For a deeper dive into the various fees, we recommend reading this Investor Bulletin compiled by the US Securities and Exchange Commission (SEC).

Some of the world’s best-performing stock mutual funds this year

Let’s take a look at some of the best mutual funds for 2024. Investors tend to hold onto mutual funds for the long-term, so we took a wider view to measure each one. We’re focusing on funds with relatively low expense ratios of below 0.70% that have had a five-year total return of 25% or more, and which have returned 10% or more this year.

1. State Street Small/Mid Cap Equity Index Portfolio (SSMHX)

The fund attempts to track the The Russell Small Cap Completeness Index, which measures the performance of Russell 3000 Index companies that are not in the S&P 500. The thought is there may be more growth with promising small-cap and mid-cap stocks.

The fund, which trades for $359.76 a share, has a five-year total return of 70.65% and a low expense ratio of only 0.02%. It delivers a yield of 1.06%.

Over the past year, the fund has had a total return of 18.35%. The diverse fund, which is weighted toward industrial, financial and technology stocks, currently holds 2,478 stocks with the largest being Spotify at only 1.36%.

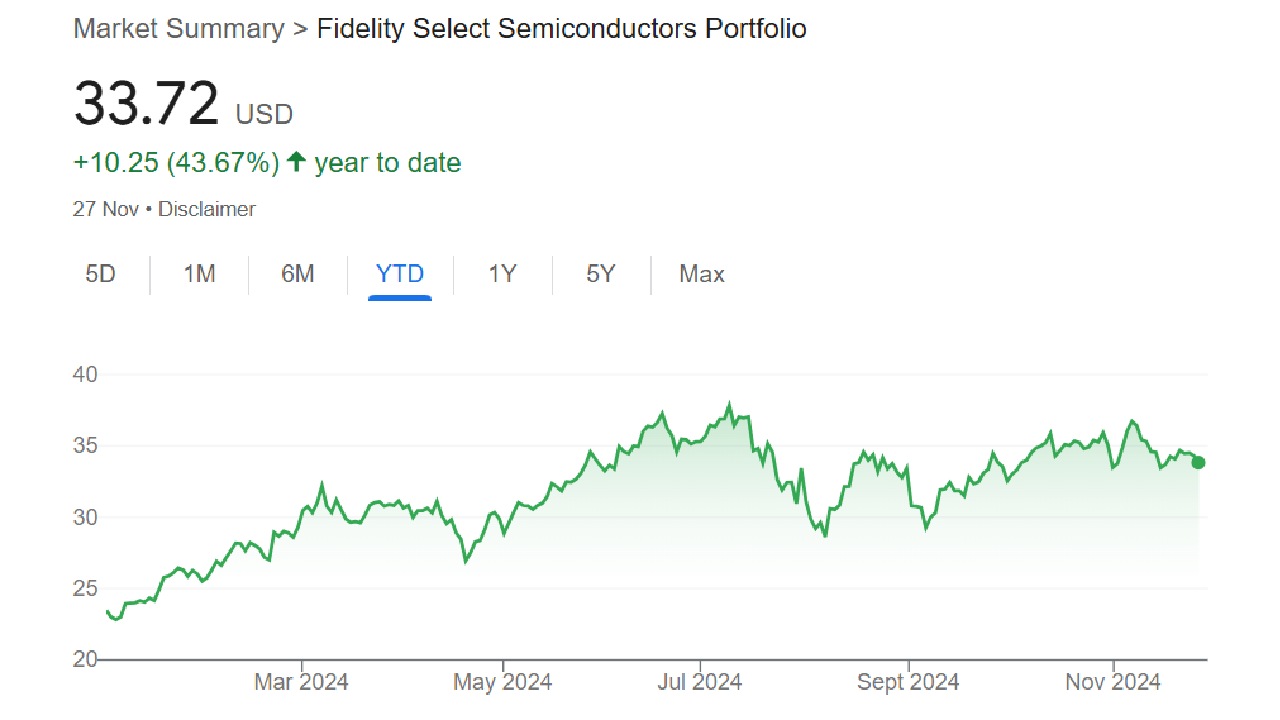

2. Fidelity Select Semiconductors Portfolio (FSELX)

The fund specializes in companies that design, manufacture, or sell electronic components (semiconductors, connectors, printed circuit boards and other components); equipment vendors to electronic component manufacturers; electronic component distributors; and electronic instruments and electronic systems vendors.

It has a 5-year total return of 342.7% and its total return is more than 38.17% over the past year.

The fund has a relatively high expense ratio of 0.62% and a dividend yield of 0.53%. It does carry some risk as it has only 54 holdings and more than 26% of its fund is invested with Nvidia (NASDAQ: NVDA), so its balance is lacking.

3. State Street Equity 500 Index II (SSEYX)

The 10-year-old fund has a five-year total return of 114.4% and its total return is up more than 18% over the past year. It tracks the S&P 500 Index and keeps its expense ratio low at 0.02%. It tilts toward technology stocks at 35.65%, followed by financials at 13.19% and consumer cyclical at 10.68%.

So far this year, it has outperformed many S&P 500 index funds. It is a fairly diversified fund with 503 large-cap stocks among its 506 holdings. It strives to have the same weighing of the stocks in the S&P 500 Index.

Its dividend yield is 1.27%. There’s no minimum investment requirement, but it currently trades at more than $619 a share.

4. State Street Global All Cap Equity ex-US Index Portfolio (SSGVX)

The fund looks to find growth in international stocks. It tracks the MSCI ACWI ex-USA Investable Market Index (IMI), which focuses on small-cap, mid-cap and large-cap stocks in 22 of 23 developed markets, excluding the US, as well as focusing on 24 emerging markets.

Japanese companies are responsible for the largest portion of the fund at 15.13% while UK companies are responsible for 8.69% of the fund.

Over the past five years, it has had a total return of 44.41% and over the past year, its total return is more than 23%. Its expense ratio is relatively high at 0.04%, but it also has a dividend yield of 2.44%.

5. Fidelity Blue Chip Growth Fund (FSBDX)

The fund invests in large- and mid-cap growth stocks that have strong prospects, and it has a strong focus on information-technology stocks at 49.15% of its holdings, followed by consumer cyclical stocks at 18.30%.

It has an ultra-low expense ratio of 0.01% and its total return is more than 25% over the past year. Its dividend yield is a modest 0.43%. Its five-year total return is 130.3%.

The passively managed fund looks to invest at least 80% of assets in blue chip companies that are well-known, well-established and well-capitalized that show above-average growth potential.

One concern is the fund has a relatively high turnover rate of 50%, meaning greater potential tax implications as more frequent trading can trigger capital gains taxes for investors, especially in taxable accounts.

6. Vanguard Russell 1000 Growth Index Fund (VRGWX)

The fund tracks the Russell 1000 Growth Index, an unmanaged benchmark representing US large-capitalization growth stocks. The fund has a total return of more than 25% over the past year, and over the past five years, it has a total return of 126%.

Its expense ratio is only 0.07%. It is passively managed and has 394 holdings. Its dividend yield is 0.59% and its turnover rate is 11%. It is heavily weighted toward technology stocks at 53.66%, with consumer cyclical being the next highest sector represented at 13.22%.

Despite its strong performance, the fund has a big negative in that the minimum investment is $5 million, so it isn’t for the everyday investor.

These top-performing mutual funds compared

Here’s a snapshot of our selection of the best-performing mutual funds in the world:

| Fund (ticker symbol) | Expense ratio | 5-year total return | 1-year total return |

| State Street Small/Mid Cap Equity Index Fund (SSMHX) | 0.02% | 70.65% | 18.35% |

| Fidelity Select Semiconductors (FSELX) | 0.62% | 342.7% | 38.17% |

| State Street Equity 500 Index II (SSEYX) | 0.02% | 114.4% | 18.39% |

| State Street Global All Cap Equity ex-US Index Portfolio (SSGVX) | 0.4% | 44.41% | 23.67% |

| Fidelity Blue Chip Growth (FSBDX) | 0.1% | 130.3% | 25.08% |

| Vanguard Russell 1000 Growth Index Fund (VRGWX) | 0.07% | 126% | 25.20% |

Where can you invest in mutual funds?

Here are some of the best brokers and mutual fund companies for investing in mutual funds:

Interactive Brokers: Ideal for active traders and sophisticated investors, offering access to more than 50,000 mutual funds, including more than 20,000 funds with no transaction fees. It has no proprietary funds, so its offerings are from other brokers.

Fidelity: The broker offers more than 10,000 mutual funds, including Fidelity funds and funds from other providers.

SoFi Technologies: It delivers more than 6,000 different mutual funds to members on the SoFi Invest platform. It doesn’t charge commissions on mutual fund trades and offers fractional share trading.

E*Trade: It sells more than 6,000 mutual funds, including many no-load and no-transaction fee funds.

Vanguard: Vanguard is a pioneer in mutual funds and it offers 267 funds worldwide, including 210 in the US It also has more than 131 index mutual funds. Most of its funds have no fees for buying and selling.

State Street: It has 74 of its own mutual funds, including 21 index mutual funds. The international company focuses on S&P indices.

Charles Schwab: The US broker offers more than 7,000 index mutual funds, including its own Schwab funds and those of other providers.

The types of mutual funds

Now, let’s see some common types of mutual funds, broken down by asset management style, and the assets they invest in:

Actively managed vs. passively managed mutual funds

Active funds are managed by professional teams who aim to outperform market benchmarks like the S&P 500 by carefully selecting individual stocks. However, this active management comes at a higher cost due to the resources required for analysis and research.

Conversely, passive funds, such as index funds, simply track a specific market index. They don’t attempt to outperform the benchmark but aim to replicate its performance. This strategy is less costly, as it involves minimal active management.

Importantly, many active funds not only fail to outperform their benchmarks but often underperform, especially after considering fees. This highlights the potential advantage of passive investing.

Mutual funds by assets class

Stock Funds

Invest primarily in stocks, offering the potential for higher returns but also higher risk. They include growth funds, which focus on stocks of companies with high growth potential, and value funds, which look for undervalued stocks with good fundamentals.

Bond funds

They invest primarily in bonds, offering lower risk and lower potential returns compared to stock funds and fall into sub-categories based on factors like maturity, credit quality, and interest rate sensitivity.

Money Market Funds

Invest in short-term, low-risk securities such as Treasury bills and commercial paper. They offer stable returns and low volatility, making them suitable for short-term savings goals.

Index funds

Index funds can invest in a variety of assets, including stocks, bonds, or a combination of both. They seek to replicate the performance of a specific market index, such as the S&P 500.

Unlike actively managed funds, which aim to outperform the market through stock picking and market timing, index funds take a passive approach. This minimizes management fees, making them a cost-effective investment option.

The difference between a mutual fund and an ETF

There are several differences between mutual funds and ETFs, including in how they are managed, how they are purchased and how much they cost.

Many mutual funds are actively managed, which means higher fees than ETFs, which are mainly passive investments. Investors can only buy mutual funds only be bought directly from the company that provides them, so their prices are set after the markets close, once a day.

ETFs, on the other hand, are traded much in the same way that stocks are traded, directly on an exchange, and their price varies throughout the day.

Another key difference between the two is the initial investment for a mutual fund may be $3,000 or more, while ETFs can be purchased for the price of one share of the ETF, or as little as $1 if your broker allows fractional trading.

If you’re interested in ETF investing, read our guide on the best ETFs.

Why is diversification important in investing?

One of the biggest advantages of investing in mutual funds is the diversification they offer. Diversification means owning a variety of assets that perform differently over time, but not too much of any one investment or type.

A diversified portfolio not only contains stocks from different sectors, but other assets, including funds, bonds, real estate and even saving accounts. The point is each type of asset performs differently as an economy grows or shrinks, but they offset each other, keeping returns relatively steady over the long haul.

The advantage of a diversified portfolio is it can reduce risk without sacrificing overall returns. Investments that move in opposite directions, depending on what is happening in the economy, provide the greatest protection against the impact of hard times.

What are some of the risks involved in buying mutual funds?

While mutual funds are a great way to provide a diversified background to your portfolio, like any investment, they represent some risks. The first is the high cost of entering some mutual funds, which can be more than $3,000 for an initial investment. That means that more of your investment cash will be tied up in one investment.

Be careful of mutual funds with high expense ratios that can eat into your returns. Also, some mutual funds charge commissions, known as loads, that can erode your gains.

Mutual funds aren’t always completely transparent, making it harder to know what exactly is in them. That’s not good news for ESG-oriented investors or those who want to avoid certain types of sectors, such as oil and gas or commodities.

Summary of the pros and cons of mutual funds

Pros

- Easy diversification

- Professional management

- Potential for low-cost investing

- Dividends can be reinvested for compounding growth

Cons:

- They often require higher initial investment

- Some funds can have high fees

- Limited trading flexibility

How to choose a mutual fund: A 5-step guide

Here are five steps to follow when you are ready to invest in mutual funds and to continue investing in them:

Step 1: Determine your financial goals

The type of investments you choose depends on what you are trying to achieve. For example, someone about to retire will likely have a different asset allocation than someone who’s just out of college. So, always let your financial objectives drive your decision-making.

Younger investors who are saving for a long-term goal such as retirement will likely focus their investments on riskier assets like stocks, while an investor who’s near retirement age might shift their portfolio toward safer choices such as bonds or money-market funds.

Step 2: Research mutual funds

When you’re ready to invest in mutual funds, you’ll want to spend some time researching different fund options. Make sure to review if there are minimum initial investment requirements, the expense ratio, the transaction fees you’ll pay and any clauses related to pulling money out. These can include an early redemption fee, or deferred load fee. In the long run, fees are an essential consideration for investors, as they reduce your returns.

All the information you need about a specific fund is available in the fund’s prospectus. Take the time to review it in detail, and make sure you are comfortable with all the conditions.

Step 3: Outline your asset mix

Before investing in a new mutual fund, it can be helpful to assess your current portfolio to get a picture of how your money is allocated. Most portfolios are typically made up of a combination of stocks and bonds.

Allocate your money based on your risk tolerance. Those with low risk tolerance tend to hold a greater portion of their portfolio in bonds and fixed-income investments, while those with high risk tolerance may be more comfortable holding a large portion of stocks.

As with most investments, mutual funds are susceptible to losses. The magnitude of potential losses is tied to the level of risk contained in the portfolio. So, a fund that invests heavily in riskier assets like emerging technologies will have a very different risk profile from a fund that invests in established, tried-and-true names, bonds or money market instruments.

Step 4: Buy mutual fund shares

When you’re ready to purchase shares in a mutual fund, you generally have two choices: buy the shares directly from the fund company itself or purchase them through your online broker.

If you don’t already have a brokerage account, setting one up is relatively simple. Focus on the costs associated with a broker, the number of mutual funds available and the research tools before you decide which broker to go with. Charles Schwab and Fidelity scored well in Bankrate’s 2022 Awards.

You can also hold mutual fund shares in your 401(k) or another workplace retirement plan. These investments are typically automatic and made each time you’re paid by your employer.

Step 5: Keep track of your investments

By periodically reviewing your investments, you can take charge of your finances and make any adjustments needed. Utilize any free resources from your broker, like meeting with a financial planner, and always ask questions.

Ultimately, there’s no such thing as a hands-off investment, but few investments need to be monitored daily. If you’re investing for a goal that is still decades away, such as retirement, then checking in on your investments monthly or quarterly should be enough to make sure you’re on track.

Mutual fund investing FAQs

Are mutual funds a good investment?

Are mutual funds safe?

Should a beginner invest in a mutual fund?

Can you lose money in mutual funds?

How much do I need to start investing in mutual funds?

Do mutual funds pay dividends?

How much does it cost to invest in mutual funds?

Are mutual funds good for retirement?

References

- Data on mutual funds from the St. Louis Federal Reserve

- State Street Small/Mid Cap Equity Index Fund (SSMKX)

- Fidelity Select Semiconductors Portfolio (FSELX)

- State Street Equity 500 Index II fact sheet

- State Street Global All Cap Equity ex-U.S. Index Portfolio

- Fidelity Blue Chip Growth fund

- Vanguard Russell 1000 Growth Index Fund