In 2008, Warren Buffett made a bet that an index fund would do better than a quintet of hedge funds over 10 years when fees are accounted for. Buffett chose a low-cost Vanguard fund that tracked the performance of the S&P 500 index. That fund had a return of 125.8% over the duration of the bet. The returns of the five hedge funds, including fees, over the decade averaged about 36.6%.

Investors took notice, and late last year, passively managed funds passed actively managed ones for assets under management (AUM) for the first time. Sometime this decade, index funds are forecast to account for more than 70% of all funds under management. If you are considering jumping on this trend, and wondering how to invest in index funds, this guide will walk you through the process. We also cover some of the best-known index funds and the top brokerages offering these funds.

- Show Full Guide

What are index funds?

An index fund is a type of investment fund that tracks a specific market index, for instance a stock or a bond index.

The financial firms compiling the index funds use a passive investment strategy because they aim to replicate the performance of a specific index without active trading. This approach typically results in lower fees compared to actively managed funds, making it an appealing choice for those looking to balance their portfolio with other assets like gold investing for long-term stability.

What is a stock index?

A stock index is a statistical measure that tracks the performance of a group of stocks. It’s a snapshot of a particular market or sector. Indices are calculated using a specific formula that considers factors, such as the stock prices and market capitalization of the companies included in the index. The indices form the benchmarks of many financial products, including index funds.

How do index funds work?

Index funds are popular investment vehicles that track the performance of a specific market index, such as the S&P 500. Unlike actively managed funds, which rely on fund managers to pick individual stocks, index funds invest in a basket of securities that mirror the composition of an index. This passive investment approach reduces management fees and often results in better overall returns for investors.

Some of the world’s best-known index funds

Let’s take a look at some well-known and popular index funds, their main features, including costs, and recent performance:

1. Vanguard Total Stock Market Index (VTSAX)

The fund, created in 1992, currently holds 3,654 stocks of the 3,608 stocks in the CRSP Total Market Index. Created to give investors an overall exposure to the US market, VTSAX includes growth and value stocks across the spectrum of small-cap, mid-cap, and large-cap.

The benefit of the index is a broad diversification to the market. The fund will not purchase more than 10% of the voting securities of any one stock. It has $1.8 trillion in AUM, more than any other index fund. It has a price-to-earnings ratio (P/E) of 26.5.

Over the past decade, it has given an annual average total return of 12.38% compared to the benchmark’s 12.40% return. One downside to the fund for some investors is the minimum investment is $3,000. VTSAX. However, it’s also available as an exchange-traded fund (ETF), at a lower initial outlay.

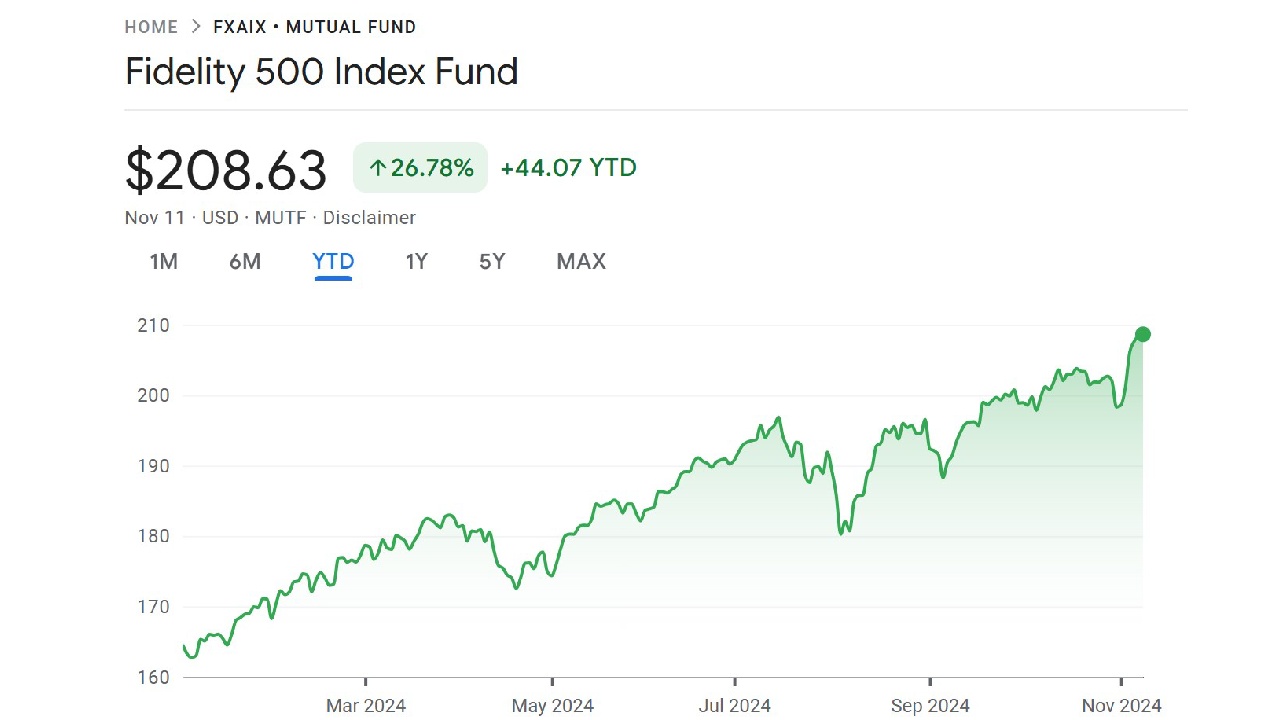

2. Fidelity 500 Index (FXAIX)

The fund, created in 1988, tracks the S&P 500 index, with at least 80% of its holdings in members of the benchmark that includes the 500 largest companies traded on US bourses. It’s mostly a blend of large-cap growth stocks. Over the past decade, it has produced an average annual total return of 12.99%.

The largest sector in the fund is information technology, representing 31.7% of its holdings. Its top holding is Apple at 7.27%.

The fund also delivers a quarterly dividend, with a yield of 1.27%. Its low-cost structure (0.15% expense ratio) makes it a popular choice. In addition, there’s no minimum investment requirement, which means it could be a good index fund for any investor.

3. Vanguard 500 Index (VFIAX)

It’s the granddaddy of all index funds, created in 2000. While it requires a $3,000 minimum investment, its balance and low fees makes it a core holding of many investors.

The fund holds 506 stocks and tracks the S&P 500. It trades at slightly higher than 27 times earnings and has a dividend yield of 1.24%.

Over the past decade, it has produced an average annual return of 12.96% compared to 13% for the S&P 500 Index. The fund is just as volatile as the S&P 500, which covers 75% of the total value of the US market, so that’s a concern for some investors.

4. Vanguard Total International Stock Index (VTIAX)

Created in 2010 as a diversified complement to US-based index funds, VTIAX seeks to track the performance of the FTSE Global All Cap ex US Index and has 8,688 holdings. The point of the fund is to provide a wide exposure in developed and emerging non-US equity markets. It includes a number of stocks from Japan, the UK, Canada, Australia, and France.

While the fund returned just 4.94% a year on average over the past decade, its total return so far this year has been 8.8%. It delivers a strong yielding dividend of 2.68%.

There’s no minimum investment requirement and its low expense ratio of 0.12% make it a good selection for investors seeking to broaden their portfolio. It focuses on large-cap and mid-cap international companies.

5. Vanguard Total Bond Market II Index (VTBIX)

The fund was established in 2009 and has 11,373 holdings. It tracks the Bloomberg US Aggregate Float Adjusted Index, which measures investment-grade, taxable, fixed-rate bonds in the US.

Its annual average return over the past decade is just 1.38%, but the point of the fund is to give investors exposure to US investment grade bonds and provide downside protection if the economy falters.

It’s best for investors with medium-term investment horizons (4 to 10 years) who are looking for income (it has a dividend yield of 3.68%) over growth and have a low tolerance for short-term price moves.

6. Schwab S&P 500 Index Fund (SWPPX)

This index fund, introduced in 1997, has outperformed most other similar funds. So far this year it is up 26.39%.

Whereas many similar portfolios have a turnover of 4% or more (turnover is the number of buying and selling of stocks within the fund), the SWPPX has had only 2% turnover and currently has 503 holdings. That shows more of a buy-and-hold approach that has paid off.

The fund doesn’t charge an investment minimum. It isn’t that diverse. More than 99% of its holdings are US companies and 46.8% of its stocks are large-cap companies with market caps of $10 billion or more.

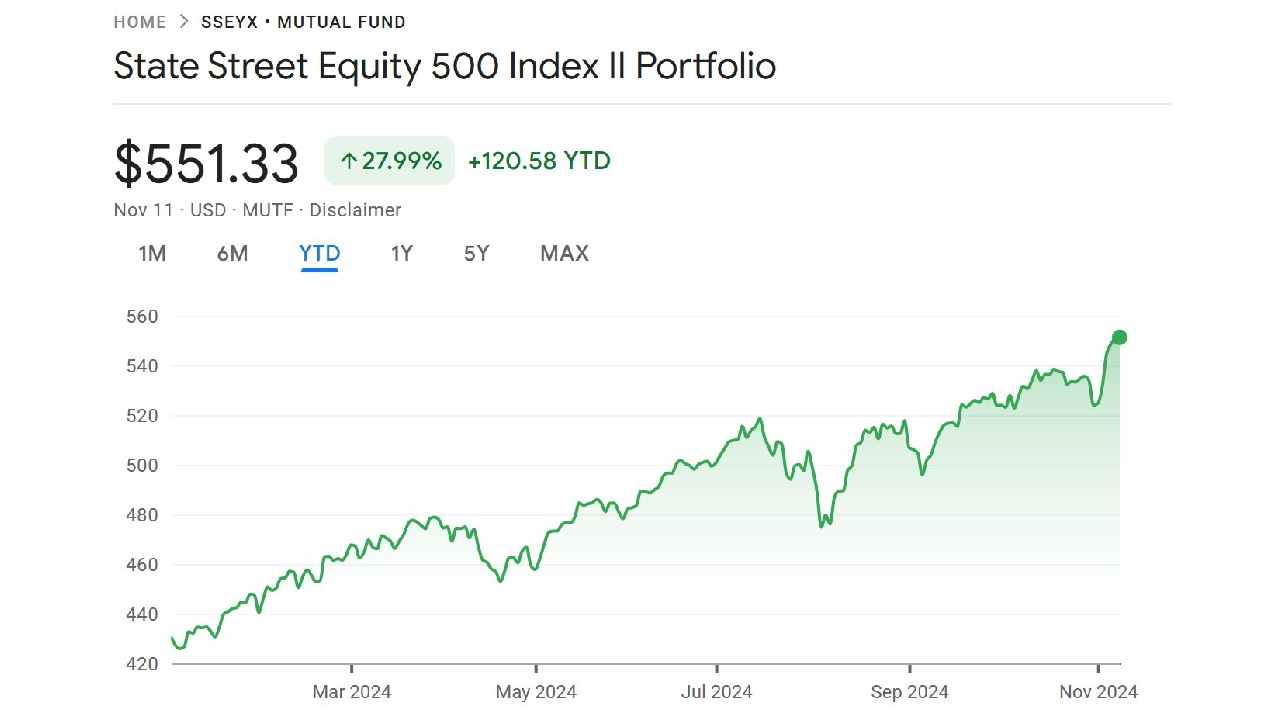

7. State Street Equity 500 Index II (SSEYX)

The fund, created in 2014, tracks the S&P 500 Index. Over the past decade, it has had an average annual return of 12.95%. Its primary sector is technology stocks at 32.07%, followed by healthcare at 11.29%.

So far this year, it has outperformed many S&P 500 index funds. It’s a fairly diversified fund that focuses on large-cap stocks in the S&P 500 and attempts to have the same weighting of the stocks the way they are in the S&P 500 Index. Its dividend yield is 1.2%.

Comparing these top index funds

Let’s compare the costs and returns of the largest and most popular index funds in the world that we highlighted above.

| Fund (ticker symbol) | Assets under management | Expense ratio | YTD return |

| Vanguard Total Stock Market Index (VTSAX) | $1.8 trillion | 0.04% | +26.17% |

| Fidelity 500 Index (FXAIX) | $592.7 billion | 0.015% | +26.78% |

| Vanguard 500 Index (VFIAX) | $552.77 billion | 0.04% | +26.71% |

| Vanguard Total International Stock Index (VTIAX) | $447.2 billion | 0.12% | +8.31% |

| Vanguard Total Bond Market II Index (VTBIX) | $147.1 billion | 0.65% | -0.60% |

| Schwab S&P 500 Index Fund (SWPPX) | $108.3 billion | 0.20% | +27.97% |

| State Street Equity 500 Index II (SSEYX) | $12.6 billion | 0.020% | +25.99% |

Why invest in an index fund?

There’s a reason why the six largest mutual funds in the world, based on assets under management, are index funds. Index funds have consistently done better than managed funds. It’s very hard to time the market or beat the market. Therefore, a simple, low-cost index fund is a good way to provide diversification and solid performance to your portfolio.

Why is diversification important in investing?

Diversification helps investors manage their risk by spreading their investments across different asset classes, such as stocks, bonds and cash and across sectors. It’s one of the best ways to weather market ups and downs and maintain the potential for growth. By diversifying, investors reduce the chance of a negative event wiping out their portfolio because they had too much invested in one stock, one sector, or one type of investment.

What are some of the risks involved in buying index funds?

Over the long haul, index funds have had a strong performance, but by only investing in index funds, investors could miss out on huge growth stocks, such as Nvidia or Amazon that have a history of outperforming the market. Also, one of the biggest concerns with index funds is they don’t really protect you during a general market downturn in the way, say, a portfolio that has a healthy dose of bonds might.

Summary of the benefits and drawbacks of index funds

Index funds are suitable for most investors’ portfolios. However, they do have some advantages and disadvantages to consider:

Pros

- Diversification: By investing in a single index fund, you gain exposure to a wide range of securities, reducing risk compared to investing in individual stocks.

- Low Costs: Index funds typically have lower expense ratios than actively managed funds, allowing more of your investment to work for you over time.

- Transparency: Index funds are straightforward, with clearly defined holdings. This transparency contrasts with the often opaque strategies of actively managed funds.

- Tax Efficiency: Lower turnover rates in index funds generally result in fewer taxable events, especially for mutual fund investments held in taxable accounts.

- Simplicity: Index funds offer a simple and accessible investment approach, requiring less research and analysis compared to actively managed funds.

Cons:

- No Outsized Returns: While index funds provide diversification, they tend to deliver average market returns. This means they may not offer significant outperformance compared to broader market benchmarks.

- Risk of Dividend Cuts: In times of economic downturn or financial distress, companies may reduce or eliminate dividends.

- Limited Upside Potential: Index funds are designed to track a specific index, limiting their ability to capitalize on short-term market opportunities. Investors seeking quick, substantial gains may find index funds less suitable.

- Exposure to Market Downturns: Index funds are susceptible to market fluctuations. During periods of market decline, index funds will generally experience losses, offering little downside protection.

Investing in index funds: a 3-step guide

To invest in index funds, you can open a brokerage account and purchase shares directly. Many online brokerages offer a variety of low-cost index funds, making it easy to build a diversified portfolio.

Step 1: Research index funds that fit your goals

With a multitude of index funds available, careful selection is key to optimizing your investment portfolio. To gain a clearer understanding of your investment, carefully examine the underlying holdings of the index fund. This will provide insights into the specific companies and sectors in which your money is invested. Remember, the fund’s label may not always accurately reflect its true composition.

Consider these essential factors:

- Expense Ratio: As index funds are passively managed, their expense ratios, or annual fees, should be minimal. Given the often-similar performance of index funds, even small fee differences can significantly impact long-term returns.

- Minimum Investment: Ensure the fund’s minimum investment requirement aligns with your initial investment and subsequent contribution plans, both for taxable and tax-advantaged accounts.

- Dividend Yield: For investors seeking income, dividend yield is a crucial metric. Compare dividend yields across funds to identify those that can potentially boost overall returns, even in challenging market conditions.

- Inception Date: A longer track record can provide valuable insights into a fund’s historical performance, including its ability to navigate both bull and bear markets.

- Geographic Focus: Funds like the ones tracking the S&P 500 and Nasdaq-100 invest in US companies. Other funds may concentrate on specific regions, such as France or the Asia-Pacific region.

- Sector-Specific: Some funds specialize in particular industries, such as pharmaceuticals or technology and track a sectoral index.

- Income-Oriented: Funds may prioritize high-dividend-paying stocks.

- Growth-Oriented: Other funds may focus on companies with high growth potential.

Step 2: Make your choice

Once you’ve identified potential index funds, consider these other factors to make the most informed decision:

- Tax Implications: Mutual funds often distribute capital gains, which can lead to higher tax bills.

- Accessibility: Mutual funds may require substantial initial investments, while ETFs often have lower minimums or even allow fractional share purchases.

Step 3: Buy your index fund

This is usually the easiest step, assuming you’ve already funded your account. If your broker carries the particular index funds you’re interested in, you can buy them from your broker. Remember, though, that each broker often has their own index funds and it may ultimately be most cost effective to buy an index fund that your broker sponsors, after all the fees are factored in. Index funds often incur two types of fees: sales loads and expense ratios.

Sales Loads: These are commissions charged when buying or selling a fund. To avoid these fees, consider investing through investor-friendly companies like Vanguard, Charles Schwab, or Fidelity.

Expense Ratios: These are ongoing fees charged by the fund company based on the assets held within the fund. These fees are typically deducted daily and are often less noticeable.

Where can you invest in index funds?

Here are some of the best brokers and mutual fund companies for investing in index funds:

Vanguard: Vanguard is a pioneer in index funds and it offers more than 100 index funds, plus nearly as many ETFs that track indices. The US broker’s index funds start with a minimum investment of $3,000 and can run as high as a minimum investment of $100 million for its Short-Term Bond Index Fund Institutional Plus (VBIPX), for example.

A big advantage for Vanguard is you can trade ETFs and mutual funds commission-free, even those from other companies. While some mutual funds may have load and redemption fees, Vanguard offers many fee-free options. Additionally, Vanguard provides low margin rates, suitable for index investors, and a wealth of educational resources to assist with retirement planning.

Fidelity: The US broker offers more than 30 of its own index mutual funds, including many that have no investment minimums. It also carries other brokers’ index mutual funds.

The best thing about Fidelity is that it charges no commissions on any trade, whether it be an index fund or a stock. It even has an index fund, the Fidelity ZERO Total Market Index Fund (FZROX), which has an expense ratio of 0.

BlackRock: The US broker, like Vanguard, is an index fund pioneer and was among the first to offer a wide array of passive products and much of its revenue comes from its more than 106 index mutual funds. Most of its index funds require a minimum investment of $1,000, with its iShares S&P 500 Index K requiring a minimum investment of $5 million. However, it does have an Automatic Investment Plan (AIP) that allows investors to invest in their BlackRock funds on a periodic basis for a minimum of $50 per fund. Founded in 1985 by former Lehman Brothers executives, it serves institutional and individual investors. It began by focusing on fixed-income investments such as bonds and mortgage-backed securities and has branched out. It also owns and manages the iShares line of ETFs.

State Street: The US broker has more than 137 ETF index funds, but only 21 index mutual funds. It has a global presence, with offices in more than 28 countries. Its funds focus mainly on on S&P indices, but its expense ratios run slightly higher than some of its competitors. One of its top performing index funds is the State Street US Core Equity Fund (SSAQX), which is up more than 27% so far this year and has an expense ratio of only 0.14%.

Charles Schwab: The US company’s Schwab Asset Management arm is the third-largest provider of index mutual funds behind Vanguard and Fidelity and features more than 3,000 index funds.

One plus is it offers index mutual funds that require no minimum investment with no loads or transaction fees.

Interactive Investors: The UK-based broker offers 40,000 investments to choose from, including shares, investment trusts and exchange-traded funds (ETFs), and a wide assortment of index funds, many of them from Vanguard or Fidelity.

It specializes in flat-fee investing, with a minimum charge of £4.99 per month, plus £3 per trade, so it could be a good choice for more active investors.

The difference between an index fund and a mutual fund

Index funds can often offer lower expense ratios and potential tax advantages than other types of mutual funds. Index funds may be a good choice for investors who prefer a more hands-off approach and don’t need the intraday trading flexibility. Ultimately, the best choice depends on individual investment goals and preferences. Of course, index funds are a subset of mutual funds. There are some key the differences, though, to consider between index funds and actively managed mutual funds:

- Passive vs. active management: Index funds track a specific index, thus, their composition is fixed, only determined by the make-up of the index they aim to match. Therefore, they are passive investments. Mutual funds are managed by a professional portfolio manager or a team who set the fund’s investment strategy and handpick the securities to include.

- Objective: The manager of the index fund aims to match the performance of the benchmark index the fund tracks, while the manager of an actively managed mutual fund seeks to beat the benchmark.

- Lower fees: Index funds generally have lower expense ratios than other mutual funds. An index fund manager oversees the fund, but not doing stock research just mirroring the benchmark. Those lower fees often mean better returns for investors over the long term. Most of the fund options in workplace 401(k) plans are index funds, but you can also own them in an individual retirement account or a taxable brokerage account.

- Tax advantages: Index funds are generally more tax-efficient than actively managed mutual funds due to their lower turnover rates. However, the specific tax implications can vary depending on the fund’s strategy, the investor’s tax bracket, and the type of account in which the fund is held.

How much does it cost to invest in index funds?

The minimum needed depends on the fund and your broker’s policies. If your broker allows you to buy fractional shares of stock, you may be able to invest in an index fund with as little as $1. If not, your minimum investment will be the cost of one share of the fund.

There are other costs that can be associated with investing in index funds, such as expense ratio and loads, in some cases, but those come into play after you buy an index fund.