New Stocks On Exec Comp & ROIC Model Portfolio: August 2016 by Kyle Guske II

Two new stocks make our Linking Exec Comp to ROIC Model Portfolio this month. August’s Linking Exec Comp To ROIC Model Portfolio was made available to members on August 16, 2016.

Recap from July’s Picks

Our Linking Exec Comp To ROIC Model Portfolio (+3.1%) outperformed the S&P 500 (+1.3%) last month. The best performing stock in the portfolio was Outerwall (OUTR), which was up nearly 19%. Overall, eight out of the 15 Exec Comp To ROIC Stocks outperformed the S&P 500 in July and 10 had positive returns.

The successes of the Linking Exec Comp to ROIC Model Portfolio stocks highlight the value of our forensic accounting as featured in Barron’s. Return on invested capital (ROIC) is the primary driver of shareholder value creation. By analyzing key details in SEC filings, we are able to calculate an accurate and comparable ROIC for 3000+ companies under coverage.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and tie executive compensation to improving ROIC. We think this combination provides a uniquely well-screened list of long ideas.

Greenbrier Companies (GBX), railroad freight car manufacturer, is one of the additions to our Linking Exec Comp to ROIC Model Portfolio in August, and is also on August’s Most Attractive Stocks list.

Since 2010, Greenbrier has grown after-tax profit (NOPAT) by 65% compounded annually to $271 million in 2015 and $320 million over the last twelve months (TTM), per Figure 1. Over the past decade, NOPAT has grown 20% compounded annually. The company’s NOPAT margins have improved from 3% in 2010 to 11% TTM.

Figure 1: GBX’s Consistent Growth In NOPAT

Sources: New Constructs, LLC and company filings

Improving ROIC is directly correlated with creating shareholder value. ROIC was added to Greenbrier’s executive compensation plan in 2014 and the company’s ROIC has improved from 12% in 2014 to 22% over the last twelve months. Longer term, ROIC improved from 2% in 2010 to 22% TTM, per Figure 2.

Figure 2: Improving ROIC Tied To Exec Compensation

Sources: New Constructs, LLC and company filings

In 2015, Greenbrier’s short-term incentive plan was based on corporate wide performance goals and business unit goals. While the breakdowns vary by executive, ROIC represented 25% of performance goals for the company’s CEO, CFO, and CCO. While other metrics do include adjusted EBITDA and region specific goals, the one fourth weighting of ROIC makes GBX’s compensation plan much improved than those that only include non-GAAP metrics.

Investors can reduce their risk by investing in company’s where the executive compensation plan aligns executives with shareholders while also incentivizing shareholder value creation, as GBX’s does.

When GBX reported fiscal 3Q16 results, and guidance came in below consensus estimates, the stock fell 9%. Longer term, the stock has fallen 50% over the past two years, as investors have questioned railcar demand across the globe. However, a near collapse in GBX’s business is now priced in, despite management still expecting fiscal 2016 diluted EPS to only fall 2% year-over-year, at the low-end of estimates. At its current price of $34/share, GBX has a price-to-economic book value (PEBV) ratio of 0.4. This ratio means the market expects Greenbrier’s NOPAT to permanently decline by 60%, which would appear to be an overly pessimistic expectation, even if consensus estimates are correct.

However, if Greenbrier can grow NOPAT by just 1% compounded annually for the next decade, the stock is worth $49/share today – a 44% upside. This scenario also assumes that Greenbrier’s spending on working capital and fixed assets will be 6% of revenue, which is the average change in invested capital as a percent of revenue over the past five years.

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Greenbrier’s 2015 10-K:

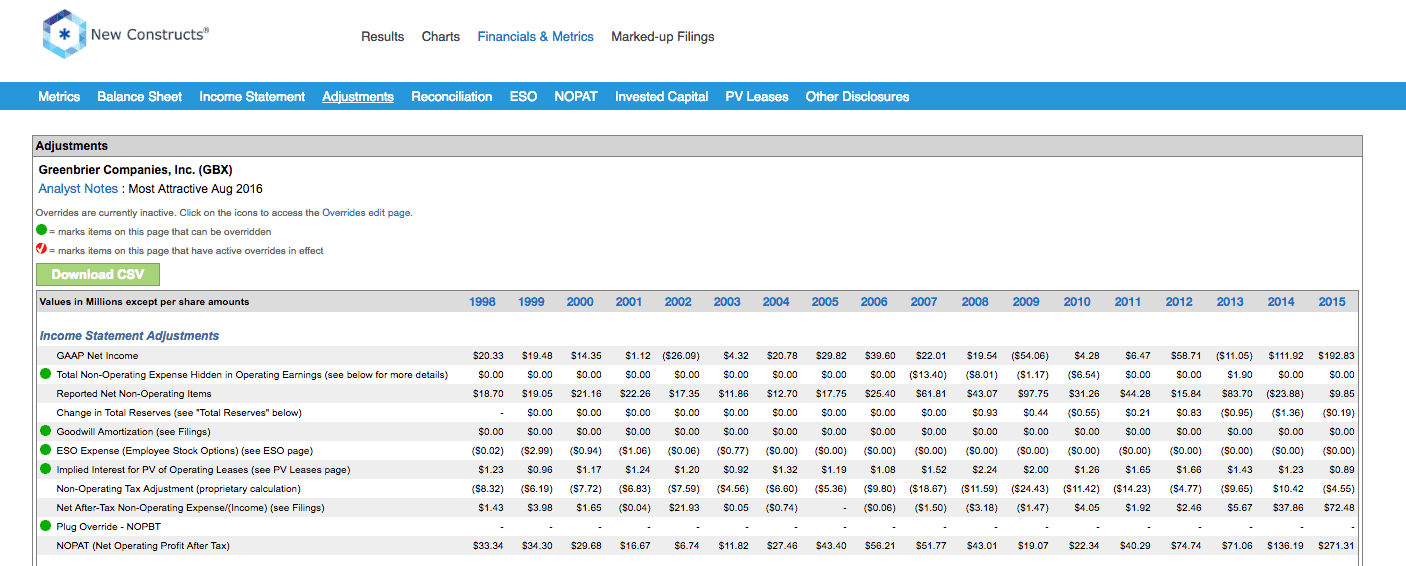

Income Statement: we made $106 million of adjustments with a net effect of removing $78 million in non-operating expenses (3% of revenue). We removed $92 million related to non-operating expenses and $14 million related to non-operating income. See all adjustments made to GBX’s income statement here.

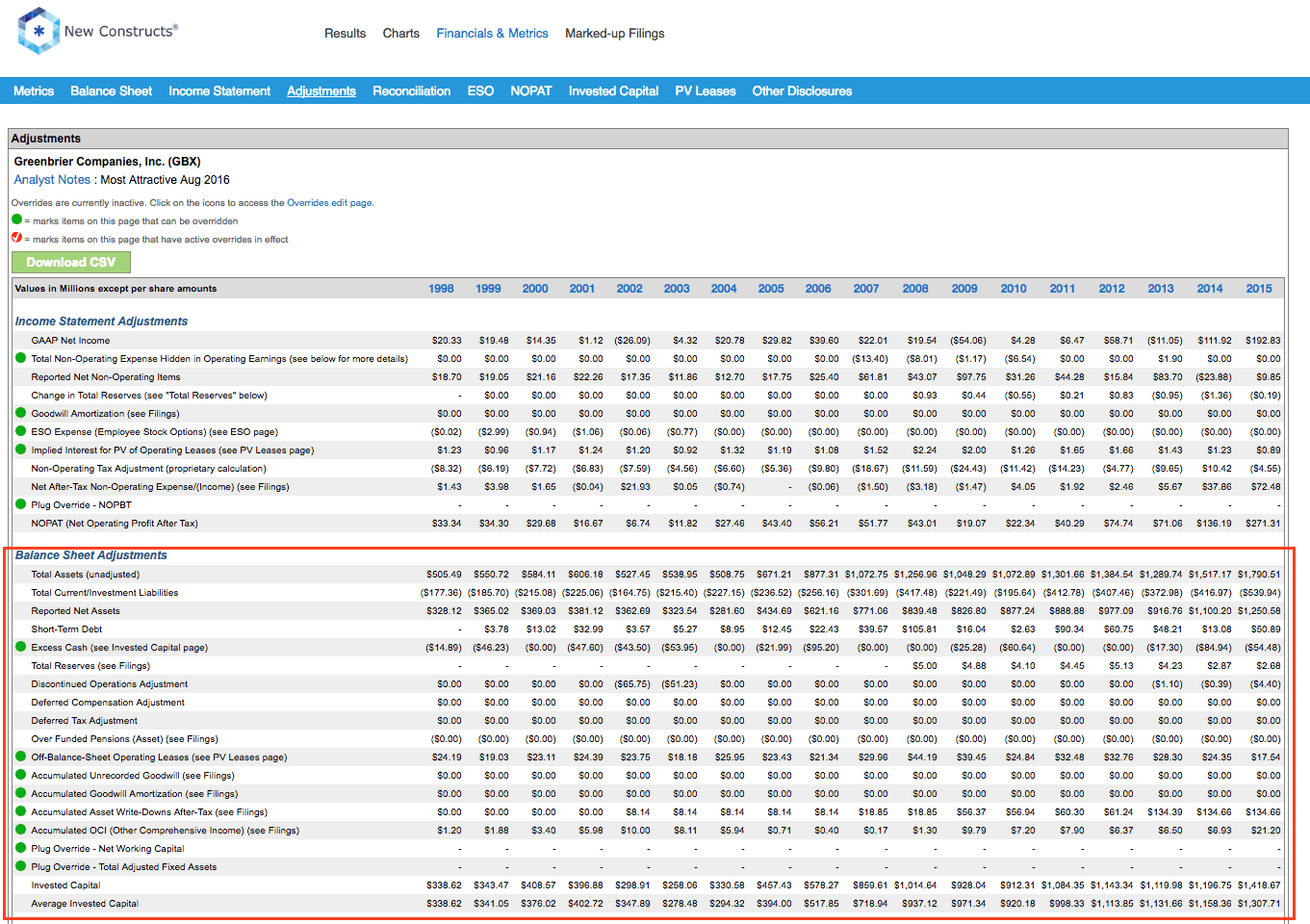

Balance Sheet: we made $397 million of adjustments to calculate invested capital with a net increase of $57 million. The most notable adjustment was $135 million (11% of net assets) related to asset write-downs. See all adjustments to GBX’s balance sheet here.

Valuation: we made $597 million of adjustments with a net effect of decreasing shareholder value by $453 million. One notable adjustment to shareholder value was the removal of $150 million related to minority interests. This adjustment represents 16% of GBX’s market cap. Despite this decrease in shareholder value, GBX remains undervalued.

This article originally published here on August 23, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

{kind=link}

{kind=link}

{kind=link}

{kind=link}