Our latest featured stock is a small cap investment company with some significant hidden expenses.

Last week, our analysts parsed 350 filings and collected 43,532 data points. In total, they made 7,185 adjustments with a dollar value of $460 billion. That breaks down into:

- 2,917 income statement adjustments with a total value of $35 billion

- 3,043 balance sheet adjustments with a total value of $210 billion

- 1,225 valuation adjustments with a total value of $214 billion

Figure 1: Filing Season Diligence

Sources: New Constructs, LLC and company filings.

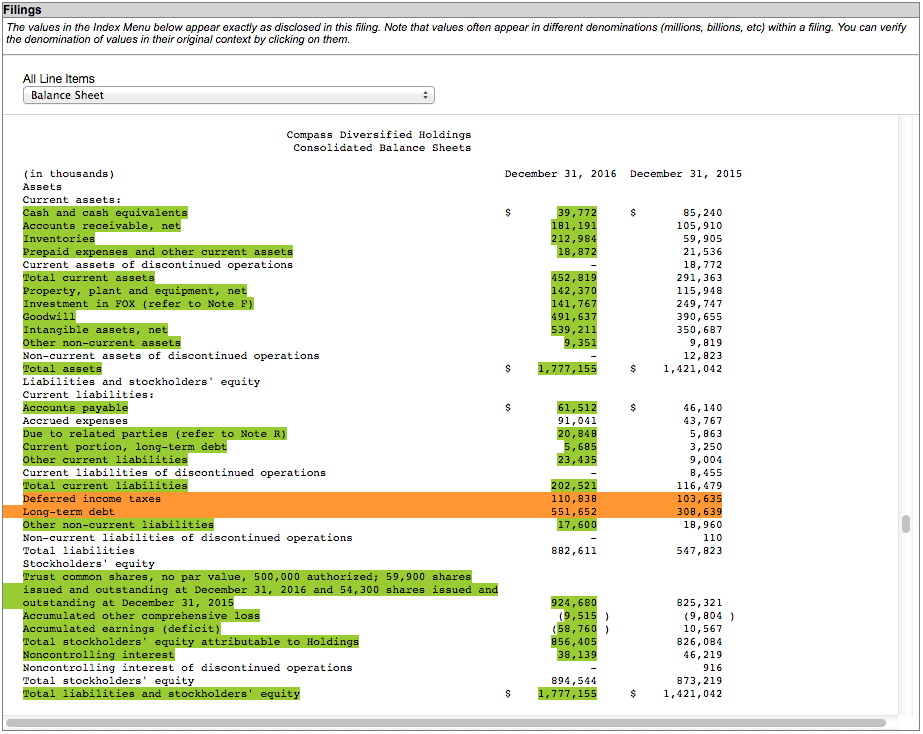

Compass Diversified Holdings

During the past week of filing season, we found a change in accounting policies from Manitowoc (MTW), a misleading ROIC calculation from Lincoln Electric (LECO), and an unusual tax benefit from Pzena Investment Management (PZN). Follow us on Twitter and check out the hashtag #filingseasonfinds for regular updates on our research.

Every year in this six-week stretch from mid-February through the end of March we parse and analyze roughly 2,000 10-Ks to update our models for companies with a 12/31 fiscal year end. This effort is made possible by the combination of expertly trained human analysts with what we call the “Robo-Analyst.” The Robo-Analyst uses machine learning and natural language processing to automate much of the parsing process.

A Fiduciary Level of Diligence

Our technology enables us to deliver fundamental diligence at a previously impossible scale. We believe that in time investors will come to demand this level of diligence when it comes to their investment advice.

Only by reading through the footnotes and making adjustments to reverse accounting distortions can advisors go beyond the suitability standard and provide a fiduciary level of diligence to their clients.

One Company To Watch In 2017

Based on our analysis of Compass Diversified Holdings’ (CODI) 10-K, we have upgraded the stock from Dangerous to Neutral.

Senior Analyst Lindsay Bohannon identified two significant hidden items that artificially depressed CODI’s reported GAAP net income in 2016.

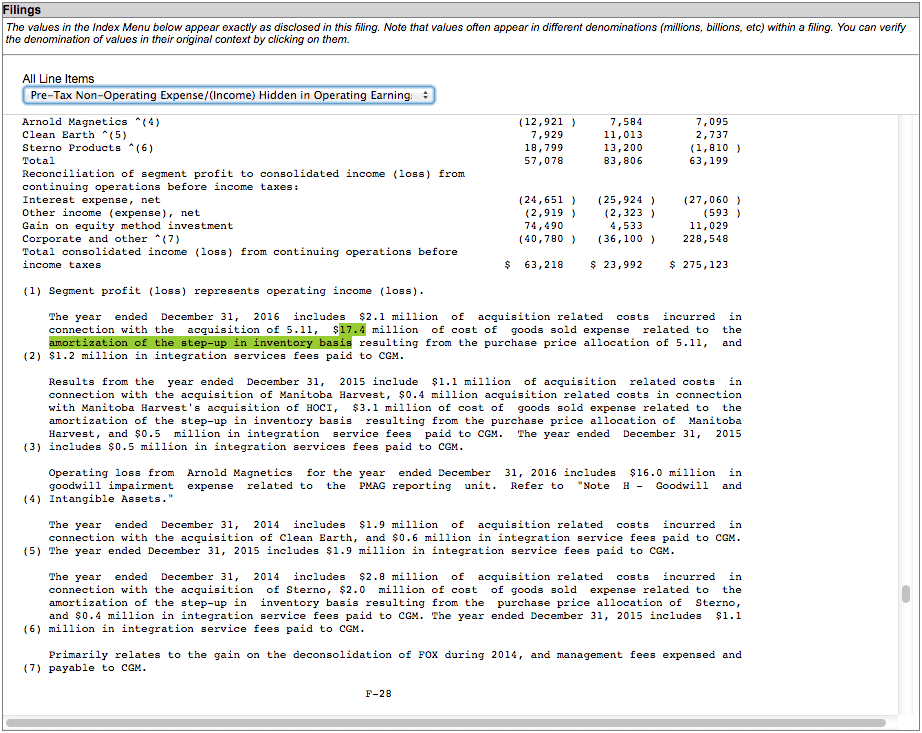

First, CODI reported a non-recurring, non-cash charge of $17.4 million due to the amortization of the step-up in inventory basis from its acquisition of tactical clothing brand 5.11. This charge was found on page 28 of the footnotes, page 157 overall.

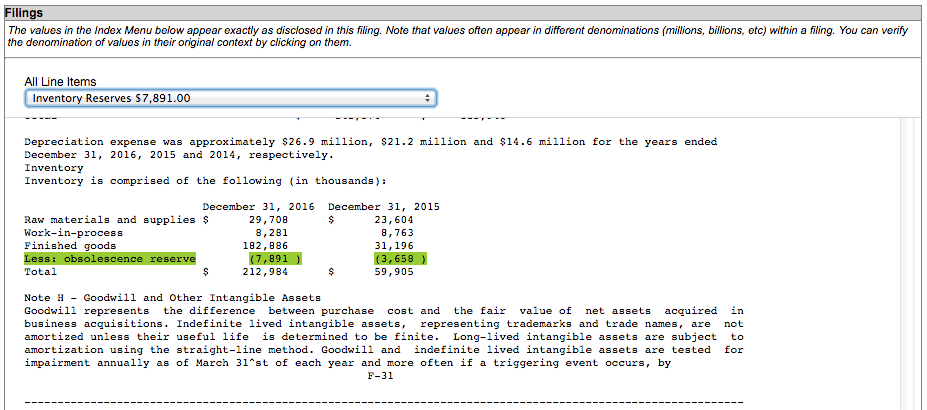

Second, CODI increased its inventory reserve by $4.2 million. This change was found on page 31 of the footnotes, page 160 overall.

In addition to these hidden items, we made several adjustments for items found directly in the financial statements, including:

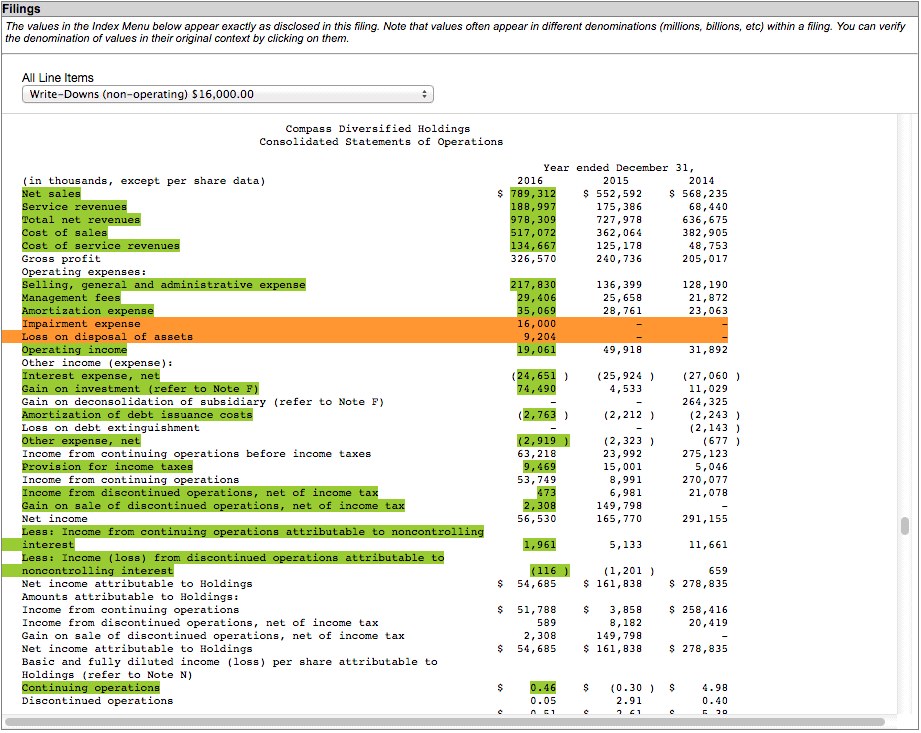

- Adding back $25 million in write-downs to both NOPAT and invested capital

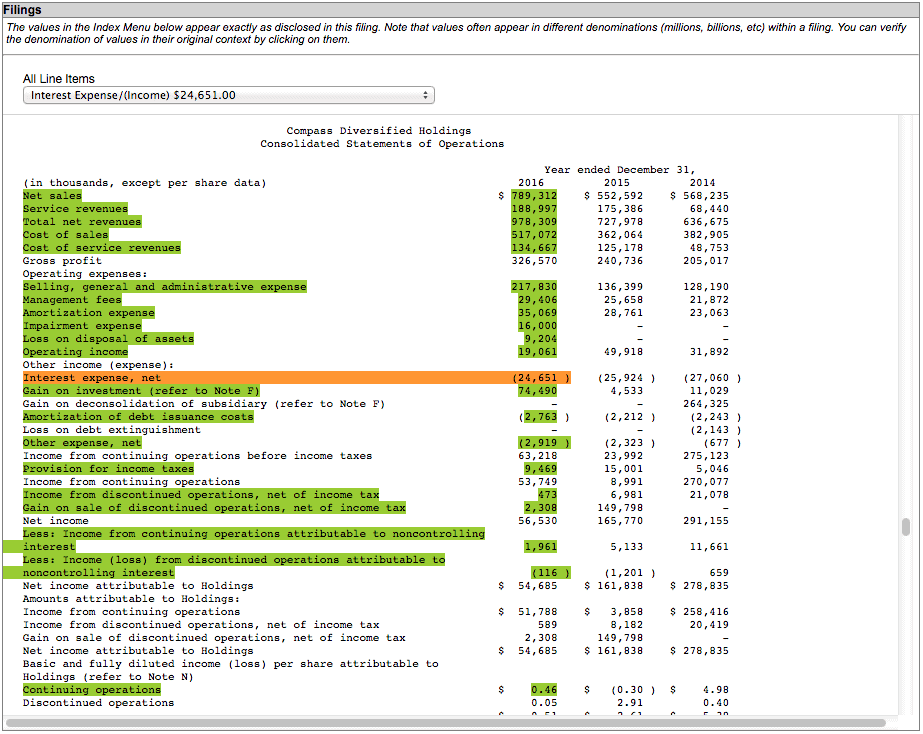

- Adding back $25 million in interest expense to NOPAT

- Subtracting $660 million in long-term debt and deferred tax liabilities from our calculation of economic book value

After making these adjustments, we found that CODI’s NOPAT in 2016 was $107 million compared to GAAP net income of just $25 million. CODI was significantly more profitable than its income statement would suggest.

We still have concerns about CODI, including its negative free cash flow and its relatively modest return on invested capital (ROIC) of 7%. Still, the improvements in 2016 were enough to push the stock out of Dangerous territory.

This article originally published on March 20, 2017.

Disclosure: David Trainer, Lindsay Bohannon, and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Article by Sam McBride, New Constructs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}