“For when the One Great Scorer comes

To mark against your name,

He writes — not that you won or lost —

But how you played the Game.”

Grantland Rice (from the poem “Alumnus Football”)

Also see 2017 hedge fund letters

When I was young, my mother bought me a book written by Grantland Rice. Rice was one of the all-time great sports writers and I was crazy about sports. It was the type of book you could pick up and read a quick story, put down and pick up again… a new story. She later framed the above quote and hung it on my bedroom wall.

In my favorite chair with coffee in hand, reading Mark Yusko’s “Letter to Fellow Investors,” I was lost in his story of Yogi Berra. I smiled as I read. Mark brought me back to those days as a young boy reading Grantland Rice and wishing to be great. From Mark’s letter:

Yogi Berra was well known for his off-the-cuff pithy comments, most often malapropisms (the use of an incorrect word in place of a word with a similar sound, resulting in a nonsensical, sometimes humorous utterance) that became known as “Yogi-isms.” Berra’s seemingly random sayings took the form of a tautology or paradoxical contradiction but often delivered a powerful message and real wisdom. Sports journalist Allen Barra described them as “distilled bits of wisdom which, like good country songs and old John Wayne movies, get to the truth in a hurry.” Yogi described them (as only he could) saying “A lot of guys go, ‘Hey, Yogi, say a Yogi-ism.’ I tell ’em, ‘I don’t know any.’ They want me to make one up. I don’t make ’em up. I don’t even know when I say it. They’re the truth and it’s the truth I don’t know.”

Yogi Berra was born Lorenzo Pietro Berra to immigrants Pietro and Paolina Berra in the Italian neighborhood of St. Louis, Missouri called “The Hill” on May 12, 1925. His father had arrived at Ellis Island on October 18, 1909 at the age of 23 and made his way to St. Louis to find work. Berra’s parents originally gave him the nickname “Lawdie” as Paolina had difficulty pronouncing Lawrence and Larry. Berra grew up on Elizabeth Avenue across the street from friend (and later competitor) Joe Garagiola and nearby the legendary Cardinals announcer Jack Buck. Given the baseball success of that trio, the street was later renamed “Hall of Fame Place.” Berra began playing baseball in the American Legion league where he received his famous nickname from teammate Jack Maguire. At the movies together one afternoon, they saw a newsreel about India and Maguire commented that Berra resembled the Hindu Yogi in the clip (because of how he sat around with arms and legs crossed waiting to bat) and the nickname stuck. In 1942, a sixteen-year-old Berra tried out for the St. Louis Cardinals, but when he was offered a smaller signing bonus ($250 instead of $500, about $3,600 today) than his best friend, Joe Garagiola, he refused to sign. As the story goes, the Cardinals team president secretly wanted to select Berra, but knew he was leaving St. Louis to take over the Brooklyn Dodgers and wanted to sign him there. As fate would have it, the New York Yankees offered Berra the same bonus as Garagiola and Yogi became a Yankee (and the rest, as they say, is history). World War II interrupted Berra’s baseball career when he enlisted in the U.S. Navy as a gunner’s mate on the attack transport USS Bayfield. During the D-Day invasion of France (Omaha Beach), a nineteen-year-old Berra manned the machine gun on an LCS (Landing Craft Support Boat), was fired upon, but not hit. Historians recounted that “only the steel walls of the boat and the grace of God stood between a sailor and death.” Berra received some grace and survived the assaults, later receiving several commendations for his bravery. Following his Navy service, Berra returned home and finally got his chance to play minor-league baseball with the Newark Bears.

Berra was called up to the Yankees and played his first Major League game on September 22, 1946 (interestingly, a Gann Date). Berra was a work horse of a baseball player and saw action in more than a hundred games in each of the following fourteen years. Over the course of his career, Berra appeared in record fourteen World Series, including 10 World Series championships (also a record). Given his tenure with the Yankees during one of their most dominant stretches, Berra set World Series records for the most games played (75), At Bats (259), Hits (71), Singles (49), Doubles (10), Games Caught (63), and Catcher Putouts (457). An interesting aside, in Game 3 of the ’47 World Series, Berra hit the first pinch-hit home run in World Series history off Brooklyn Dodgers (the team that originally wanted him) pitcher Ralph Branca (who also gave up Bobby Thompson’s famous Shot Heard ‘Round the World in the ’51 World Series). Incredibly, Berra was an MLB All-Star for 15 seasons, but played in 18 All-Star Games as MLB had two All-Star Games in 1959-62. Berra won the American League MVP Award in 1951, 1954, and 1955 and amazingly never finished lower than 4th in MVP voting from 1950-57. Berra received MVP votes in fifteen consecutive seasons (tied by Barry Bonds and second only to Hank Aaron’s nineteen). Even with all his accolades, perhaps the most impressive statistic (from an investment perspective) is that from 1949-55, playing on a team filled with superstars such as Mickey Mantle and Joe DiMaggio, Berra led the Yankees in RBIs for all seven consecutive seasons.

Casey Stengel once praised Berra saying “Why has our pitching been so great? Our catcher that’s why. He looks cumbersome but he’s quick as a cat” (looks can be deceiving). Berra commented on his non-traditional looks once, saying “So, I’m ugly. I never saw anyone hit with his face.”

Baseball legend Mel Ott perhaps summed up Berra best, saying “He seemed to be doing everything wrong, yet everything came out right. He stopped everything behind the plate and hit everything in front of it”. In a classic Yogi-ism, Berra once quipped, “If I didn’t make it in baseball, I wouldn’t have made it workin’. I didn’t like to work.” The irony here is his performance on the field was a direct result of his strong work ethic, but perhaps the greater takeaway (and we can relate to this one) is that if you do something you love, you never work a day in your life.

“How he played the game.” I thought about the great Grantland Rice and about the great Yogi Berra.

“It ain’t over till it’s over.”

In July 1973, Yogi was the manager of the Mets and the Mets were struggling with injuries. A reporter asked Yogi if the season was over (for non-baseball fans, post-season playoffs begin in October so there was plenty of season left to play) and Yogi answered, “It ain’t over till it’s over.” The theme of Yusko’s letter and my theft of that theme today. (Hat tip to John Mauldin’s Outside the Box newsletter.)

Where are we today? Well, “it ain’t over.” And what about the 2018 Outlook? Grab that coffee, find your favorite chair and let’s take a look. I see a number of firms targeting the S&P 500 Index at the 3,000 level. That is approximately 12% higher from where we sit today. Corporate tax cuts and the stock buyback game that will follow might get us there. But not without risk. When you read on, you’ll find my concise two cents. I point to what I believe is most important for you and me to keep our eyes on. Data dependent, as they say.

One more thing… today I was interviewed by Jill Malandrino, Nasdaq’s global markets reporter. The interview is a concise capsule of where the markets stand today and my outlook for 2018. Click on the image below to be taken directly to the video.

Included in this week’s On My Radar:

- Blumenthal’s 2018 Market Outlook

- Other Analysts’ 2018 Market Outlook

- Tweets of the Week

- Trade Signals – Trend Continues to Charge Ahead

- Personal Note – Snowbird

Blumenthal’s 2018 Market Outlook

“To refer to a personal taste of mine, I’m going to buy hamburgers the rest of my life.

When hamburgers go down in price, we sing the ‘Hallelujah Chorus’ in the Buffett household.

When hamburgers go up in price, we weep.

For most people, it’s the same with everything in life they will be buying — except stocks.”

– Warren Buffett

The weight of market trend evidence remains bullish. I remain focused on both market momentum and trend evidence. Despite the aged, overvalued and over-bullish environment, as evidenced in Trade Signals each week, I remain moderately bullish on both equities and fixed income.

On My Radar:

- Rising inflation risk

- The Fed and other Central Bankers – rising rates – “Quantitative Tightening”

- The shape of the yield curve and other recession indicators

- Don’t fight the Fed and don’t fight the trend

It is evident here in the U.S. and globally that inflation is picking up. It’s important to think in terms of cycles. Market cycles, business cycles and Fed response. Bear markets are generally created as rising inflation pressures cause the Fed to raise interest rates, which leads to recession. Since 1950, there have been 13 cycles where the Federal Reserve raising interest rates… 10 of them landed us in recession.

So inflation is important. The Fed raised rates for a fourth time since December 2015 this past Wednesday. They are expected to raise rates next year. My personal view is that higher interest rates will impact the economy more quickly than times past due to the record high level of debt in the U.S., Europe, China and Japan. I see risks from Europe (debt and faulty EU structure) and Chinese debt is off the charts. If there is going to be a problem, it is going to show up in stock prices to which simple trend models can help us navigate.

We’ll also need to keep a close watch on our recession indicator charts. The best indicator is an inverted yield curve. Like 2008, people will say it doesn’t matter or it’s different this time. It’s not. Number one on the list is when short-term interest rates are higher than long-term rates (known as an inverted yield curve). This is the best predictor of recession. Recessions matter because that is the environment where all the bad stuff happens. The average bear market declines 37%.

Key charts I’m watching:

- Ned Davis Research CMG U.S. Long/Flat Index – currently bullish

- S&P 500 Index 13- over 34-Week Moving Average Trend Lines – currently bullish

- Volume Demand vs. Volume Supply (more buyers than sellers) – currently bullish

- Don’t Fight the Tape or the Fed – currently bullish

- Zweig Bond Model – currently bullish

- My Favorite Recession indicators – no sign of recession in the next six to nine months

Every investment is simply a claim on a very long-term stream of cash flows that will be delivered to investors over time. Your current starting conditions matter. Meaning, how richly or inexpensively priced an asset is can tell us a great deal about the returns you will likely receive over the coming 7, 10 and 12 years.

If valuations were attractive (e.g., the Buffetts singing the “Hallelujah Chorus”), then I’d be far less concerned about risk. The problem is we sit near the most expensive level in history – higher than 1929, 1987 and 2007 and nearing the great tech bubble high of 2000. Can earnings magically catch up to justify the high prices? It’s a big gap to fill. I have my doubts. Watch the trend evidence and step forward with a game plan that allows you to seek growth while meaningfully limiting your downside risk of loss. Emphasis on “game plan.”

Key takeaways:

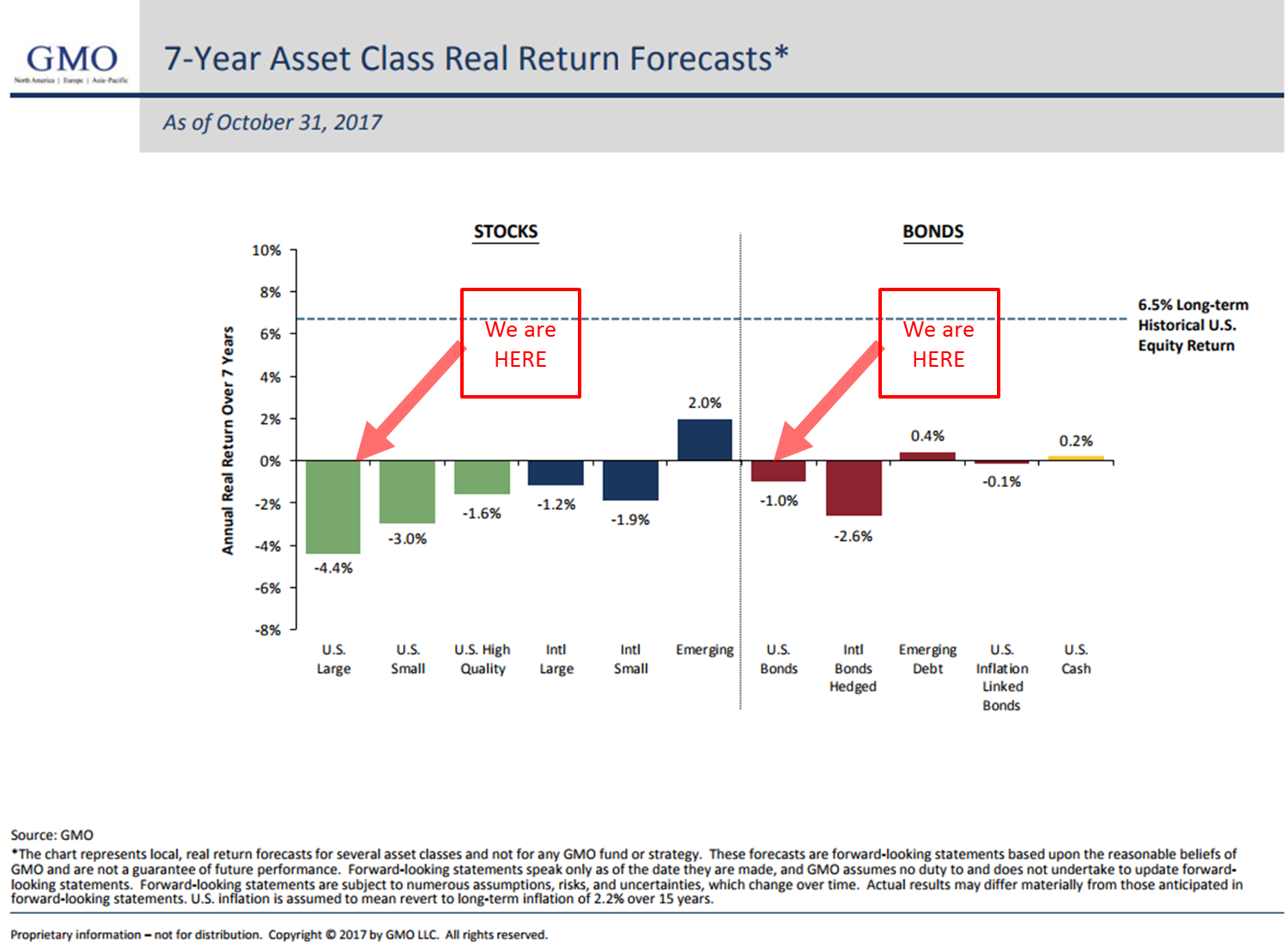

- GMO’s 7-year Real Return Forecast for U.S. Large Cap Stocks = -4.4% per year

- GMO’s 7-year Real Return Forecast for U.S. Bonds = -1.0% per year

- NDR 10-year Median Return Forecast for Equities = 1.75% per year

- Hussman’s 12-year Nominal Return Forecast for Equities = -2% per year

- State Street’s SPDR’s U.S. Investor Poll for Equities = +10% per year (NOT GOING TO HAPPEN)

The current market bubble can inflate even more. But at some point over the next year or so, we are likely to have a recession. That’s when equities correct the most. I see a 66% correction in equities before we get to attractive valuations (i.e., inexpensive hamburgers). Let’s next take a quick look at where valuations sit today.

GMO’s 7-Year Asset Class Real Return Forecasts

This following chart is posted on the GMO website each month. They’ve been posting it for a very long time. What’s important to note is the high degree of correlation between what they predicted and what turned out to be. Their process is sound but in no way makes it a guarantee. I’m simply saying their work should not be ignored.

Note the “We are HERE” arrows. They point to negative returns over the coming seven years after inflation is factored in. Yes, “yikes!” Thus my risk management mindset…

How about the return of the traditional 60/40 stock bond allocation over the coming 12-years? Reflected are nominal returns.

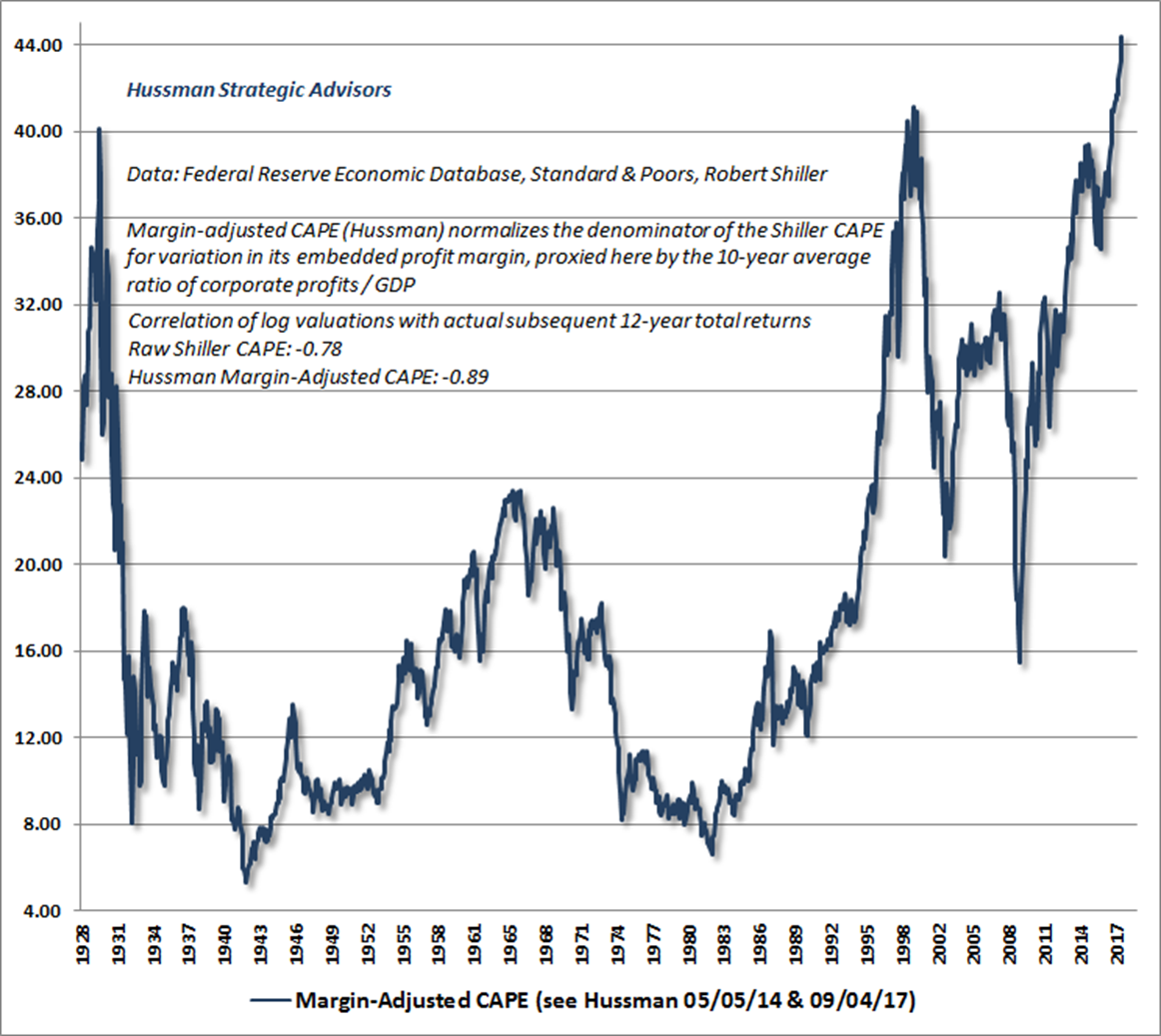

Dr. John Hussman is a fund manager who believes in risk management. He accurately sidestepped 2000 and 2008, but missed much of the recovery since. Call it a great central bank head fake to which his model missed. He’s been transparent, honest and has adjusted. If you were invested in his fund, don’t let that miss discredit his research. He does important work. The following quote is from John on 12-year returns for the traditional 60% stocks, 40% to bonds investor (quickly glance at the blue line and follow it to the bottom left of the chart. Note how the red line closely tracks the blue line. The red line plots the actual 12-year returns. The blue line is the forecast, the red line is what actually happened.)

The chart below presents our estimate of prospective 12-year annual total returns for a conventional portfolio mix invested 60% in the S&P 500, 30% in Treasury bonds, and 10% in Treasury bills (blue line). The red line shows the actual total returns for this portfolio mix over the subsequent 12-year period. Presently, passive investors face the most dismal total return prospects in U.S. history.

More from Hussman:

Over the course of more than three decades, I’ve demonstrated that the valuation measures best correlated with actual subsequent S&P 500 total returns are those that account for variation in profit margins over time. Indeed, even Robert Shiller’s cyclically-adjusted P/E (CAPE) is much better correlated with actual subsequent market returns, across a century of market cycles, when we account for the profit margin embedded in the 10-year average of earnings. In 2014, I introduced an alternative measure, the Margin-Adjusted CAPE, which substantially improves the reliability of the raw CAPE. This measure now stands at the most offensive level in history, surpassing even the 1929 and 2000 extremes.

In short, valuations are high. Expect low forward returns and a very bumpy ride. I favor growth with downside risk protection, so we can set ourselves up for the great return opportunity that the next dislocation will create.

Other Analysts’ 2018 Market Outlook

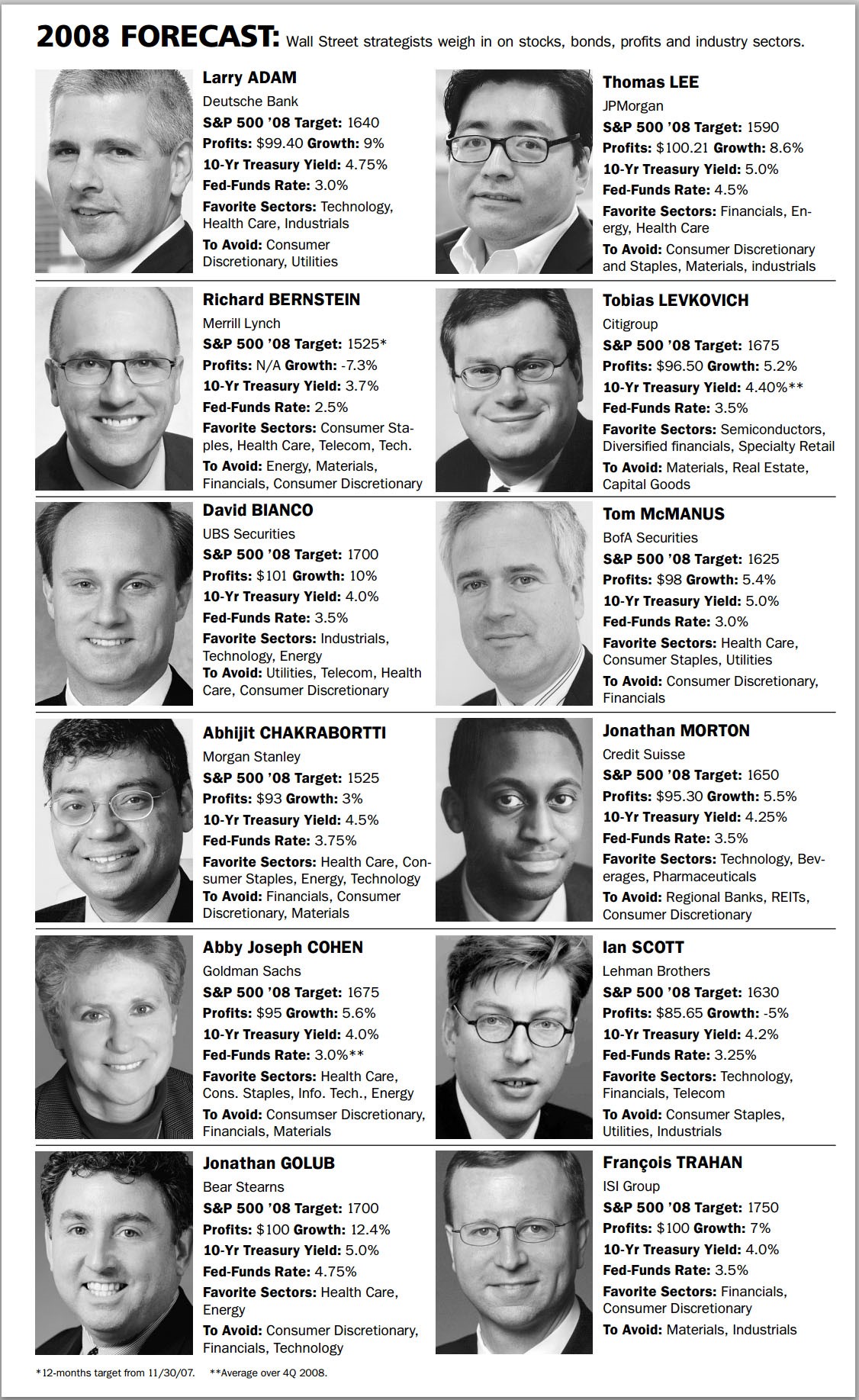

As you read various 2018 return predictions, I advise you to take them with a grain of salt. Following is a look at Barron’s Roundtable of Wall Street Experts in 2008. Note the massive misses.

2008 Forecasts:

- The S&P 500 Index peaked in October 2007 at 1,576. It finished 2007 near 1,500.

- Merrill Lynch’s Richard Bernstein was the least bullish predicting 2008 would end the year at 1,525.

- The S&P 500 Index closed near 900.

- A Fed raising rates. Recession… The market bottomed on March 6, 2009 at 666.

- How about Thomas Lee’s favorite sector – Financials. They went on to lose 80 to 90%. Others recommended the same. Goldman’s Abby Joseph Cohen advised to avoid Financials in 2008.

2016 Forecasts: Ranged from 2,100 to 2,500 for the S&P 500 Index.

- The index started the year at 2,012.

- The index finished 2016 at 2,000.

- A miss by all the experts.

2017 Forecasts:

- The S&P 500 Index began 2017 near 2,000.

- The experts’ mean S&P 500 Index target was 2,380.

I searched for the 2018 Roundtable predictions, but I don’t believe they are out yet. I do see bullish expectations dominating the airwaves. For example, JPMorgan has a 3,100 S&P 500 target. I hope they are right.

The point I am trying to make is that we really don’t know what the next year or so will bring in terms of returns. However, valuations can help you know your current starting conditions and they do an outstanding job at telling us what the coming 7-, 10- and 12-year returns are likely to be. And that is where we should set our focus.

If you do nothing else, use the 200-day moving average line as a risk management tool. The great Paul Tudor Jones told his MBA class students that he could save them thousands of dollars in tuition. He told them to use the rule. Simply, participate in market gains but do so in a way that limits your downside. Long-term returns come from the power of compound interest. Losses kill the magic. To learn more, read “The Merciless Mathematics of Loss.” And feel free to share it with your clients.

Feel free to skip over this section and/or save it for later. Think of it as a consolidated list of a number of different 2018 outlook research. You may need three more coffees to get through it all. I’m going to pick and choose a few and skim for content.

Here are a few others I have read:

“Financial Investors’ Wish List for 2018 by Mohamed El-Erian

US Stocks, Bonds, and Real Estate Most Expensive in History by Peter Boockvar

Others I have not yet read:

Invesco U.S. 2018 Investment Outlook

(For compliance reasons, this paper is only accessible in the USA)

Given the backdrop of Brexit, US tax reform, North Korean turmoil, and other geopolitical events, Invesco’s 2018 Outlook is designed around achieving investment objectives and keeping ahead of the dynamics driving the global markets.

Outlook 2018: Time for change? (Fidelity International)

(For compliance reasons, this paper is only accessible in the UK and Europe)

Fidelity International’s 2018 Outlook discusses how the year ahead could see the unwinding of the incredible bull run in both equities and bonds, and the experiments in global policy that have underpinned it.

Outlook 2018: Playing in extra time (Robeco)

In their 2018 market outlook, Robeco likens the current macro-economic backdrop to “playing in extra time” – a period where the best part of the game is over, but the outcome is still undecided.

2018 Global Market Outlook (SSGA)

Global growth is now more evenly distributed, inflation remains muted, and the coming year should be supportive for risk assets. SSGA’s Global Market Outlook discusses these key themes and other topics as we look forward into 2018.

2018 Long-Term Capital Market Assumptions (JP Morgan AM)

The 2017 edition of this report explores the secular themes such as global aging and new technologies, and cyclical factors that will impact returns over a long-term investment horizon.

2018 FX Outlook: Happy hour! (ING Bank)

ING presents their definitive analysis of the current FX environment going into 2018.

Panorama: UBS Investment Outlook (UBS Asset Management)

As 2018 approaches, senior investors across UBS Asset Management assess the global investment landscape.

2018 Investment Outlook: Weathering Heights (GSAM)

Despite some headwinds and due to a broadly supportive macro environment, GSAM discusses how investors can weather the heights in asset valuations and the potential risks in 2018 via a dynamic approach to asset allocation.

Global Outlook 2018 (Lazard)

Lazard explains several different reasons to have a positive outlook for the United States, China, Japan, and Europe in 2018.

2018 Economic and Market Outlook (TIAA)

Investors will have to work harder, take more risk, and get an information edge. This report by TIAA identifies pockets of opportunity across public and private markets.

Janus Henderson Market GPS Outlook 2018

As we enter 2018, Janus Henderson presents their take on the current bull market, monetary policy normalization, the potential return of volatility, technological innovation, and risks and opportunities in emerging markets.

2018 Investment Views: Selectivity is Key (Investec AM)

This outlook by Investec Asset Management examines the prospects for different asset classes, and whether the current post-GFC expansion is enduring or merely a temporary cyclical respite.

Global Macro View – Will Goldilocks stay in 2018? (ABN Amro)

The current “Goldilocks” scenario for the global economy is going strong, but can she stick around in 2018? ABN Amro discusses potential 2018 trends in growth and inflation, in addition to their views on specific economies.

2018 Outlook: Guard against real-world inflation (Allianz Global Investors)

Less accommodative monetary policies will force some investors to make adjustments to their approaches.

Tweets of the Week

OK – just a bit more fun and we’ll call it a day. Following are a few charts I tweeted out this past week.

Which leads to this fine quote:

U.S. investors are allocating five times more to stocks than cash. We haven’t seen this much allocation to risk since the 2000 tech bubble.

Which brings to mind this quote from Howard Marks:

We know what central bank liquidity did to boost the markets. We should be mindful of what the reverse of such action (Fed raising rates and reducing its balance sheet) might be.

Here’s how you read the chart:

- Note how much money was printed and created since the 2008 crisis.

- We have never been here before.

- The Fed wants a more normal monetary stance.

And so it begins.

- Red circle highlights the beginning of the Fed’s Quantitative Tightening

And finally, let’s finish where we started – Warren Buffett. Let’s make sure we are mentally prepared to get “greedy only when others are fearful.” Such periods tend to present quickly.

If you would like to follow me on Twitter use @SBlumenthalCMG and you can follow me on LinkedIn.

Trade Signals — Trend Continues to Charge Ahead

S&P 500 Index — 2,665 (12-13-2017)

Notable this week:

Broad market indicators — the Dow and S&P 500 Index — set new trading records yesterday. The bullish trend continues intact for equities and fixed income. We note that daily investor sentiment slipped to neutral. HY remains in a buy signal. Trade the trend with a focus on downside risk management.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — Snowbird

“Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true.

Think only of the best, work only for the best, and expect only the best.

Forget the mistakes of the past and press on to the greater achievements of the future.

Give so much time to the improvement of yourself that you have no time to criticize others.

Live in the faith that the whole world is on your side so long as you are true to the best that is in you!”

– Christian D. Larson

In 1990, I approached my father asking if he’d be comfortable forming CMG. I was working for a large wire house at the time and they weren’t keen on me setting up my own advisory business. Now many firms offer that option but, back then, no way.

Marv was a partner of a CPA firm and took his slow and prudent path before he nodded yes. Together we formed CMG. Well, today’s the big guy’s birthday and I sure do miss him. Dad passed away 5½ years ago but I sure do feel him with me often. Tonight, with cold IPA in hand, I’ll be toasting my old man. His favorite was Michelob Ultra, so maybe it’s a stop at the beer store for old time’s sake.

I feel my dad in the above quote. “Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true. Think only of the best, work only for the best, and expect only the best.”

I’m heading to Salt Lake City next Tuesday for several advisor meetings and, yes, a few days of skiing at Snowbird. The snow is not looking promising and just a few runs are open. I’m traveling with three of my boys and really looking forward to some down time with them and the coming Christmas holiday. I’ll be holding an Ultra high in hand at the top of the mountain. And saying a silent prayer to my old man. The first run down is always for him.