Since this is my first piece here at Sure Dividend and I’ll be focusing on a topic that can be somewhat controversial within the dividend growth community, I’d like to take a moment to introduce myself.

My name is Nicholas Ward. I’m not a professional in the financial industry; I studied English at the University level and unfortunately didn’t discover my passion for the stock market until after graduation. With that said, I think there’s something special about experiential learning and I’m certain that the creativity and critical thinking skills that my liberal arts education developed have played a major role in my success in the markets.

I’m a former division one athlete and I still spend a lot of time volunteering as a coach at the local high school. I read a lot, write a lot, and while I’m a licensed Realtor in the state of Virginia, I spend the vast majority of my working hours studying the markets and managing my personal portfolio.

Some of you may know me from my work at Seeking Alpha; I’ve been a contributor over there focusing primarily on dividend growth names for the last 5 years or so. Recently, I’ve decided to spread my wings a bit, broadening my readership, publishing work here as well as on my new dividend growth focused channel at themaven.net, Income Minded Millennial.

I’ve been writing about dividend growth investing for so long that sometimes, I feel like an old man. However, in reality, I’m anything but. I turn 28 years old later this month, meaning that I’m one of the younger members of the DGI brethren.

I’ve chosen to pursue financial freedom with a dividend growth strategy because I’m a firm believer in the long-term compounding ability of re-invested dividend paid out by very high-quality companies. Sometimes, this isn’t the most thrilling investment strategy. On the contrary, compared to the more speculative, growth-oriented assets that many of my peers from the millennial generation have chosen to own, the DGI names that I’ve chosen to partner with as an investor can be downright boring.

However, for the most part, boring is exactly what I’m going for in the investment world. Sure, sometimes when I see cryptocurrencies posting 88% gains in a single trading session or small-cap bio-techs popping 40% on positive results from a phase two trial, I begin to question whether or not I’m truly on the correct path.

Thankfully, those moments of doubt are fleeting. I’ve conditioned myself to realize that greed is a dangerous character flaw (especially when regarding decision-making capital markets) and once the initial excitement wears off it’s easy for me to re-focus on my income stream and the underlying fundamentals that justify my holdings.

Now, it wasn’t always easy to acknowledge greed and overcomes its grip. It takes time to condition one’s self against the illusions of fames and grandeur (or an early retirement) that greed can spawn. Data is always helpful though, and while I acknowledge that one has to take outsized risks to receive outsized rewards, I’ve also come to know that so long as one has a long time horizon in the markets, large risks are not likely necessary to achieve a respectable nest egg heading into retirement.

When it comes to data that supports the power of compounding and dividends, the paper titled, “Why Dividends Matter” written by Dr. Ian Mortimer and Mathew Page, CFA, fund co-managers at Guinness Atkinson Funds in 2012, is the holy grail.

If you haven’t taken the time to read this paper do yourself a favor and do so. It’s not incredibly long and offers dividend growth investors numerous graphs that will help to put their minds at ease during moments of weakness.

And what’s more, I’ve seen other posts/comments made by prominent individuals in the financial world. Here’s a link to a CNBC piece written in 2010 highlighting the fact that two Blackrock managers, Richard Turnill and Stuart Reeve, who later went on to co-manage Blackrock’s Global Equity Income Fund, believed dividends played an absolute paramount role in the market’s long-term performance.

Here’s a quote from the article attributed to Turnill and Reeve:

“Some may be surprised to learn that 90 percent of U.S. equity returns over the last century have been delivered by dividends and dividend growth.”

Unfortunately, after a quick Google search, I wasn’t able to find the actual letter to shareholders that this quote was originally attributed to. If anyone knows of such a report and could post a link, I would surely appreciate it. As a proponent of dividend growth investing, having such a primary source available to me would certainly come in handy.

Every time I do backward-looking study of a major market index (I use the index for diversification purposes so that I’m not falling victim to survivor bias with regard to the current dividend champions), I also find similar (impressive) results. Without a doubt, dividends and the compounding associated with re-investing them over the long-term is one of, if not the most powerful force in the markets.

However, this success has become a bit of a double-edged sword in recent years. Dividend growth investing’s popularity has skyrocketed. All of the positive data surrounding dividend growth and compound interest, combined with historically low interest rates in recent years creating an abnormally high thirst for year within the capital markets (driving income-oriented investors into the equity markets where they find themselves willing to face much higher risk because acceptable yields just aren’t available in the fixed income space) has significantly increased the premiums that investors are willing to pay to buy many of the dividend aristocrats of today.

This valuation concern surrounding many of the traditional DGI equity names is a major factor behind the primary premise of this piece: owning non-dividend paying names within a DGI-designated portfolio.

As powerful as compound interest can be as a positive force, slowing and/or negative growth, overvaluation, and contracting multiples can be just as damaging. While I do not believe the market is totally efficient in the short-term, over longer periods of time, I do believe the market generally realizes its follies and corrects them.

Placing 20x earnings multiples on companies without top-line growth to speak of is simply not a sustainable trend. The fundamentals will catch up with these companies as management squeezes everything it can out of margins with efficiency measures and bottom-line growth becomes nothing more than a product of financial engineering. The market is ruled by fear and greed in the short-term; however, eventually logic prevails.

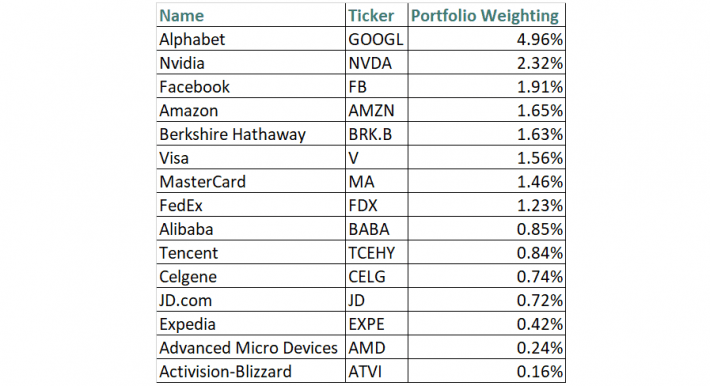

But until it does, making the purchase of high-quality names with reliably increasing dividends is more viable for value investors, I’m making an argument for owning non-dividend paying names. Right now, approximately 13% of my portfolio is made up of shares that don’t contribute to my income stream at all and another ~7% of my portfolio is comprised of companies that pay a dividend of less than 1%.

I spoke about fear and greed earlier and I want to make it clear that while greed is certainly a sin, as much as certain dividend growth investors might lead you to believe, there are many wonderful companies that do not pay a dividend and owning them within a dividend growth portfolio is not a grave transgression.

I’m holding the vast majority of these shares as long-term positions due to their attractive growth prospects fueled by strong secular tailwinds and I expect for them to play a significant role in my eventual financial freedom, dividend or not.

Other than Berkshire Hathaway (BRK.A) (BRK.B), which was one of my earlier investments due to my belief that it’s probably the best defensive holding in the market, combined with an affinity for all things Warren Buffett, it took me a couple of years to begin to build my non-dividend paying positions.

I believe that the willingness to break my basic income-oriented rules was a sign of maturation as a portfolio manager and although I’m not currently maximizing my capital with regard to augmenting my income stream, I believe that my portfolio is stronger overall because of improved diversification created by the more speculative, high growth additions that I’ve made in recent years.

I know many DGI investors see F.A.N.G. names and turn up their noses. But honestly, I think buying companies like Facebook or Alphabet, which are expected to grow both their top and bottom lines at strong double-digit rates for the foreseeable future, trading for ~28x and ~26.5x 2018 EPS estimate, respectively, makes much more sense than paying 23x for Coca-Cola, which has posted negative sales growth every year since 2012 or 22x for Procter and Gamble, which hasn’t grown its top-line since 2013. Sure, the 3%+ yields that KO and PG pay are attractive and more than likely sustainable, but without sales growth, these Dividend Aristocrats will not be able to grow their dividends like they have in the past which really drastically slows down the power of compounding.

As a relatively younger investor, I think it makes a lot of sense to have a significant part of my portfolio exposed to these high growth tech names when they’re trading at valuations just a couple of clicks above bloated names in the some of the more traditional areas of the market (consumer staples, telecoms, utilities, REITs, etc) where DGI investors have found companies that could reliably contribute to their incomes streams. This is especially the case in a rising interest rate environment; as income-oriented investors who’ve been forced to become overweight in equities have the opportunity to cash out and rotate back into fixed income, I suspect we’ll see contracting multiples in many of the rate sensitive names.

I pay much more attention to total return than many older DGI investors do because while I really enjoy receiving and re-investing my dividends in the present, I’m not living off of them. I’m still in the early stages of the accumulation phase and I’ve come to realize that it’s probably more important for me to build a portfolio of very high-quality companies trading at fair or better valuations than it is for me to reach for yield that I don’t necessarily need.

But it’s not just a change of sentiment regarding the balance between total return and dividend income that has led me to begin accumulating non-dividend paying names. It’s a bit ironic, but it was actually the strength of the income stream generated by my early, more traditional DGI investments, that gave me the confidence to be more flexible with my asset allocation.

I do a lot of conservative, forward-looking prognosticating with regard to my portfolio/income stream making sure that my wife and I are on track for retirement and once my portfolio’s income stream grew to the size that if compounded annually at a 7% rate for the next couple of decades it would more than likely meet our future needs, a weight was lifted off my shoulders.

Because of my focus on balance sheet strength, fundamental growth, and competitive advantages, I believe 7% to be fairly conservative when thinking about organic dividend growth combined with re-investments. Low/falling dividend growth rates oftentimes serve as sell signals within my DGI portfolio and I don’t plan on partnering with companies long-term that are not helping me achieve my goals.

It’s actually my intense focus on dividend sustainability and the reliability of strong dividend growth that lead me to focus on evaluating growth names in the first place. Over the years I’ve developed a somewhat hybrid approach to the DGI strategy, prioritizing value, income, and growth (usually in the order, but obviously, not always).

When buying growth stocks, investors must factor growth rates into their valuation calculus. Companies posting top and/or bottom line growth in the double digits generally trade with premium valuations that are hard to justify using a traditional P/E ratio. However, when you add in the “G”, we see that PEG ratios within the high growth tech or biotech spaces begin to look much more attractive than many of the DGI names we typically follow.

And although I can’t be sure about this, I fully expect many of the companies I own that currently play low and no dividends will evolve over time and eventually become future dividend aristocrats. Many DGI investors believe this to be the case when talking about up and coming dividend growers with relatively low yields like Starbucks (SBUX) or Nike (NKE), but you don’t hear names like NVIDIA (NVDA) or Tencent, which both offer investors miniscule dividend yields, or companies like the aforementioned Facebook (FB) or Alphabet (GOOG), which haven’t instituted a shareholder dividend (yet), enter into that conversation.

Well, I’m here to advocate for them. When growth companies become highly profitable many of them decide to go the dividend growth route. Technology names like Apple (AAPL), Oracle (ORCL), and Cisco (CSCO) come to mind in this regard. I’m not sure if any of the F.A.N.G. members view themselves as mature enough companies to allocate capital towards a shareholder dividend just yet, but I wouldn’t be surprised if that day wasn’t close around the corner for the “F” and the “G”, which operate highly profitable business models.

Only time will tell if I’m correct about companies like NVIDIA, Facebook, or Alphabet becoming eventual dividend aristocrats, but one thing is for sure, these companies have produced tremendous results for investors in recent years and so long as they continue to produce above average top-line results, this trend isn’t likely to end. Not only am I happy to have exposure to these high growth names, but I’m sleeping well doing so.

Sure, Amazon’s valuation is nearly impossible to justify by any traditional valuation standards, but its growth runway appears to be nearly infinite. As we enter into the digital age, there is a new legion of companies paving the way. I want exposure to them, regardless of whether or not they contribute to my income stream. Frankly put, as a young investor, it seems borderline irresponsible not to.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by by Nicholas Ward, Sure Dividend

{kind=link}