China is slowing and generally leading Asian economic strength with it. But with those investors who had predicted an economic meltdown in mind, what appears to be occurring in the region is a gradual slowing at a time when the US economic engine is starting to heat up.

After hitting a five-year high, growth in Asia has “peaked,” according to Capital Economics first-quarter outlook in the region.

sasint / Pixabay

One of the top performance drivers in the region, China, is facing a cooling property market and a “pollution crackdown.”

China had seen its property values soar in top-tier regions, with individual investors becoming paper millionaires. In 2017, however, that hockey stick-like price chart has started to moderate, with the pace of price appreciation in September, for instance, then hitting its lowest level in 17 months, according to data from China’s National Bureau of Statistics.

The rise in property values correlated with higher pollution levels in major cities that created health problems for its residents. With the economy being given top priority, its rivers had become industrial sewers and its smog was so bad it could be seen in satellite photos from space. Then nearly a year ago Chinese officials instituted the first “red alert” warning residents of dangerous smog levels and a recent report noted that 85% of the river water in Shanghai was undrinkable and 56.4% was unfit for any use whatsoever.

Cleaning this mess is partly to blame for China’s economic slowdown, there are other factors as well.

China’s export growth expected to mean revert while regional economies a mixed bag

After experiencing “unsustainable” export growth, Capital Economics looks for a mean reversion to various degrees.

They forecast export volumes to grow on average 5%, down from 9% the previous year.

“With exports set to weaken, the onus will be on domestic demand to take up the slack,” the report noted, pointing to rapid wage growth throughout Asia, particularly Vietnam and Indonesia, as driving the regional economy.

“Bangladesh’s economy should continue to post solid growth rates over the next couple of years, though the threat of political instability remains a key downside risk,” Capital Economics Asian Economist Mark Williams and his team predicted, looking at central bank policy. “Bank Indonesia’s monetary policy easing cycle has further to run, but the pace and timing of further rate cuts will be dependent on the performance of the rupiah.”

In the Philippines, “worrying signs” coming from the President’s office regarding an “erratic manner” that has been troubling to investors. President Rodrigo “Rody” Duterte has been accused of Gestapo-like tactics to bring the country’s underground drug business under control. Geopolitical observers are concerned that the slippery slope of authoritarianism might turn the government into an apparatus targeting political opponents in the Asian island nation.

While an increasingly repressive government bordered by the South China and Philippine seas is becoming repressive, a (slightly more) liberal Thailand is booming. “Thailand’s economy is likely to remain in good health in 2018, supported by a recovery in the tourism sector and rising government infrastructure investment,” Capital Economics noted.

China’s economy has very different performance drivers, with automated manufacturing and global trade contributing significantly more than tourism, for instance.

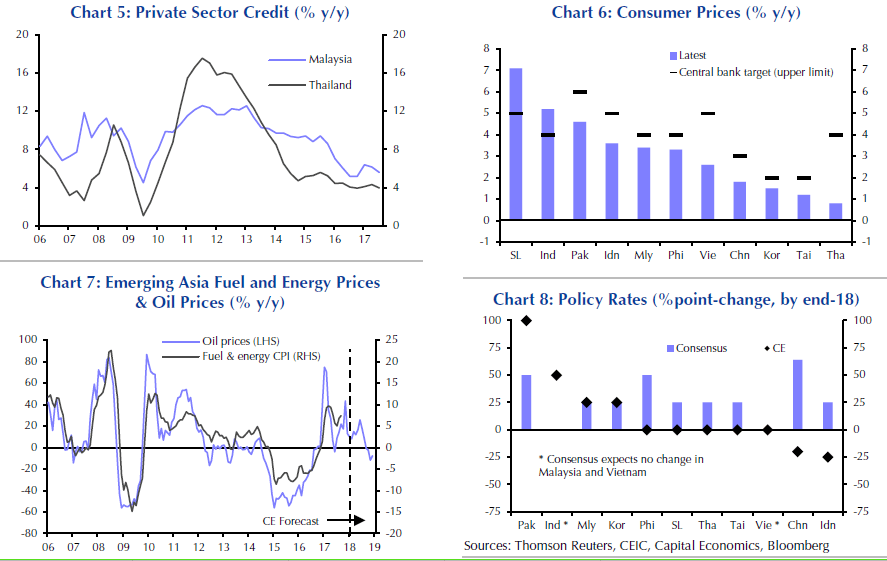

While China’s global economic leadership may start to slow, other areas with common problems are worth watching as well. Singapore, Thailand and Malaysia have seen meaningful increases in private sector debt, a factor that often chokes off spending. Credit growth in these regions has started to slow as a result, and “this should help to reduce financial risks, the downside is that weak credit growth will drag on consumption and investment.” An analysis that is not entirely different from that of China.

{kind=link}