ESG Pulse Says Greater Balance-Sheet Recognition Of Climate-Related Liabilities Would Enhance Financial Statements

Q3 2020 hedge fund letters, conferences and more

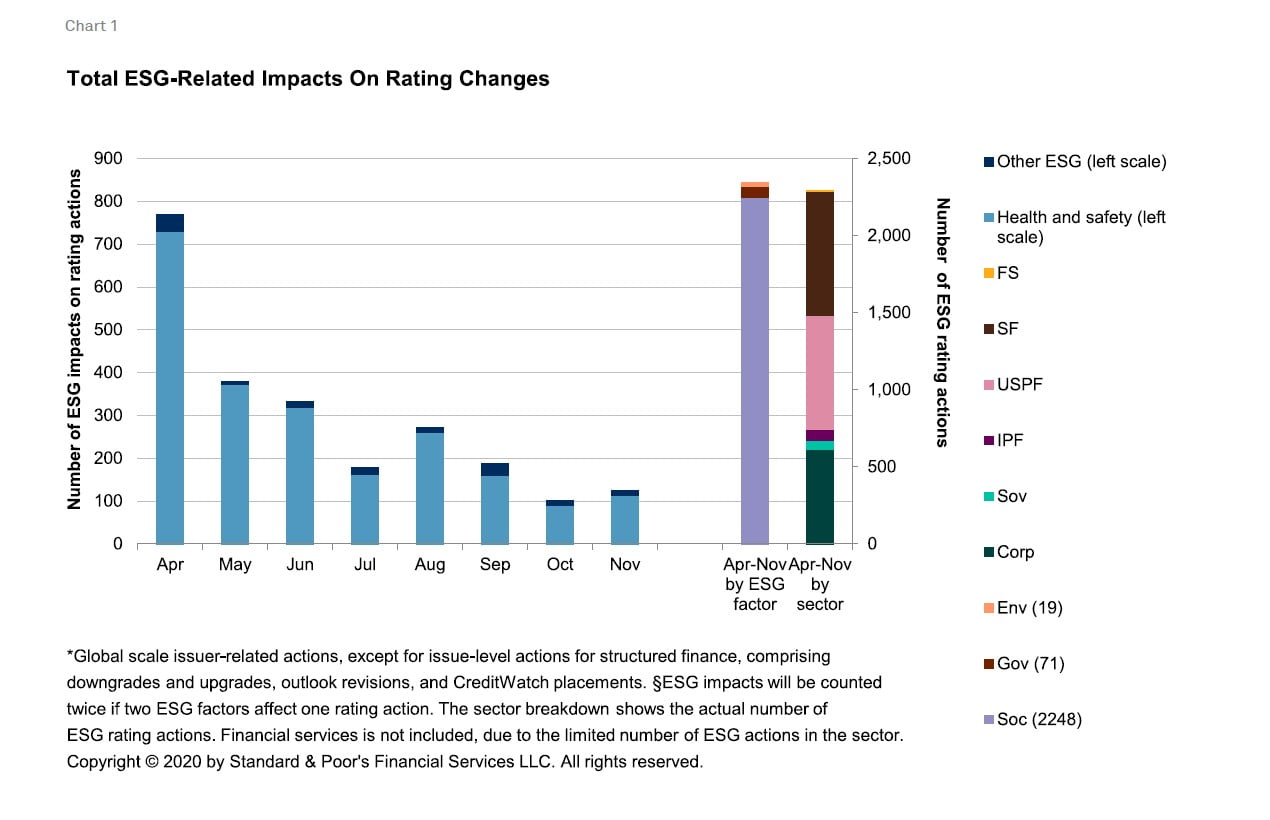

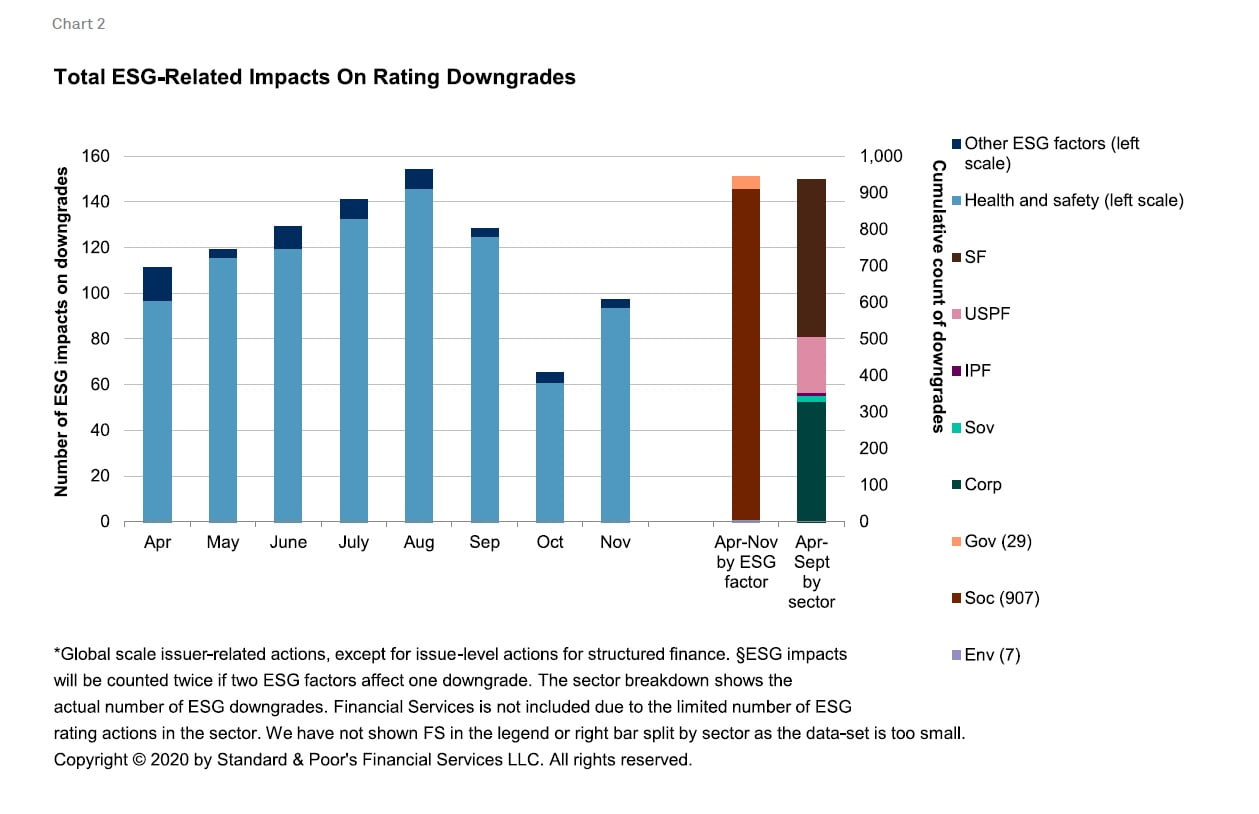

PARIS (S&P Global Ratings) Dec. 22, 2020–S&P Global Ratings’ latest edition of the ESG Pulse: Reimagining Accounting To Measure Climate Change Risks, published today, looks at how ESG factors have influenced nearly 2,300 rating actions, of which more than 900 rating downgrades, over the last eight months.

In addition, it opines on benefits of greater balance-sheet recognition of actual and potential climate-related liabilities. This would enable users of financial statements to shift qualitative measures of climate exposures to more quantitative assessments.

As a percentage of total ESG and non-ESG rating actions over April-November, ESG-related actions accounted for as much as three-quarters of actions on sovereign/international public finance entities and one-third of U.S. public finance actions. For corporate and infrastructure entities, ESG factors contributed to one in three rating actions; bear in mind that we only treat COVID-19 as an ESG factor if it has direct health and safety effects on an entity’s activities, not as a result of the economic crisis. In structured finance, ESG influenced about one in four rating actions.

ESG Pulse: Reimagining Accounting To Measure Climate Change Risks

Key Takeaways

- ESG-related rating actions fell to about 100 per month in October and November, from a monthly average of 200 from July to September. This brings the total number of ESG-related rating actions during April-November to nearly 2,300.

- The bulk (over 98%) of ESG effects have related to health and safety (COVID-19). The most affected have been sovereign and local government ratings, air travel and mass transport, media and leisure, higher education, and retail, as well as restaurants, hotels, and conference centers, with knock-on effects on CMBS.

- As a percentage of total ESG and non-ESG rating actions over April-November, ESG-related actions accounted for as much as three-quarters of actions on sovereign/international public finance entities and one-third of U.S. public finance actions. For corporate and infrastructure entities, ESG factors contributed to one in three rating actions; bear in mind that we only treat COVID-19 as an ESG factor if it has direct health and safety effects on an entity’s activities, not as a result of the economic crisis. In structured finance, ESG influenced about one in four rating actions.

In our report, “Reimagining Accounting To Measure Climate Change Risks,” published Dec. 4, 2020, we opine on the benefits of greater balance-sheet recognition of actual and potential climate-related liabilities. This would enable users of financial statements to shift qualitative measures of climate exposures to more quantitative assessments.

IFRS only requires an entity to recognize an on-balance-sheet provision if the payment is “probable” (that is, the likelihood of payment is greater than 50%) and the amount can be estimated reliably. Under U.S. GAAP the interpretation of “probable” has an even higher threshold. If the identified present obligation would only result in “possible” cash outflows, no provision would be recognized but a contingent liability needs to be disclosed. And the disclosure requirement falls away when the payment becomes even less likely or “remote”.

With the current strict provision-recognition criteria requiring future cash flows to be probable or more likely than not, most climate-related risks do not result in on-balance-sheet accrual. Today, both climate physical and transition risks tend to fail this test due to the unpredictability of the timing and quantum of their impact.

S&P Global highlights three potential improvements:

- Set a lower threshold than “probable” for the provision recognition criteria in order to crystallize liabilities earlier.

- Apply a probability-adjusted approach to measure the liability, such that events carrying a 51% versus 49% likelihood get proportional rather than binary recognition.

- Redefine/introduce disclosure norms for carbon pricing or, more generally, a pollution pricing mechanism (PPM) given that emissions will increasingly become a transition risk in view of net zero carbon commitments by many countries. Even if the effect may not be material today, more forward-looking information–explaining how potential future carbon-pricing risks affect an issuer’s income and cash flow statements–could notably enhance the understanding of credit-relevant risks.

We believe a bolder reimagining of financial reporting could be even better so that capital markets can be driven more by sustainability considerations. Harvard Business School has recently developed a concept called Impact Weighted Accounts. These are line items in a set of financial statements (including the income statement, balance sheet, and statement of cash flows) that supplement the standard picture of a company’s financial health and performance with additional information about how the company is affecting employees, customers, the environment, and wider society.

Read the full report here.