Ashva Capital Management commentary for the first quarter ended March 31, 2021, discussing the Poor Man’s Covered Call strategy.

Q1 2021 hedge fund letters, conferences and more

Dear Limited Partner,

Change in Strategy

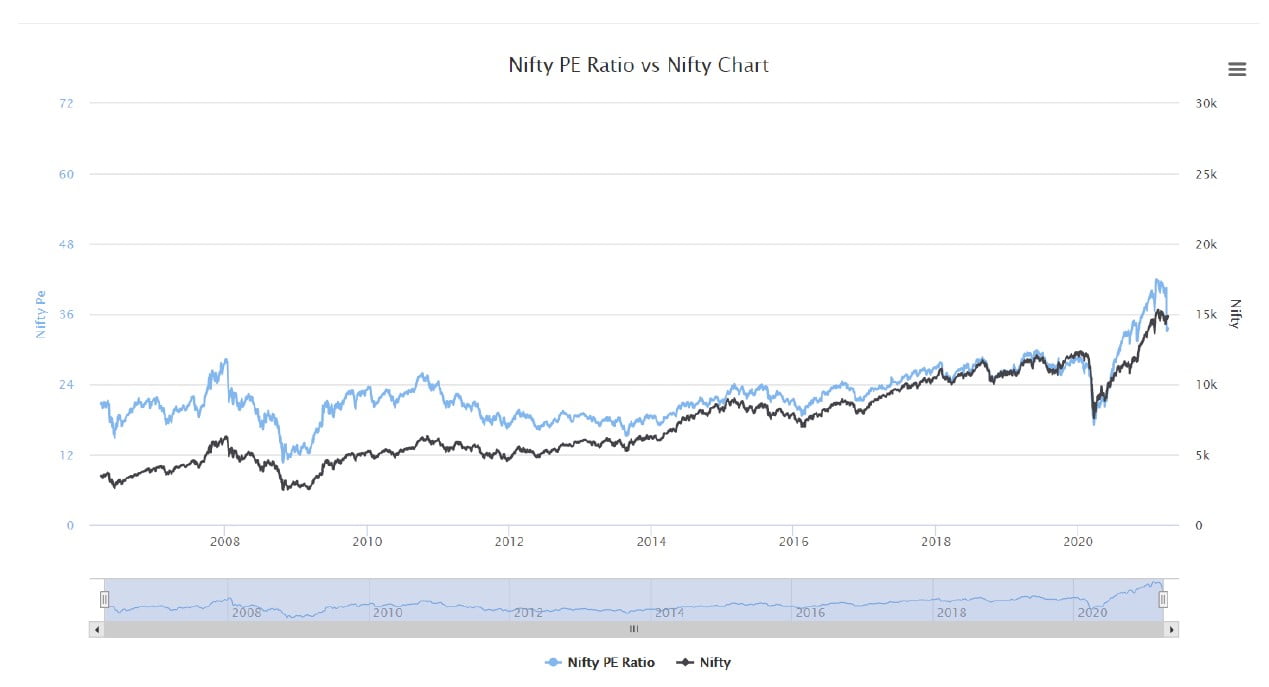

Ralph Waldo Emerson once wrote: “A foolish consistency is the hobgoblin of little minds, adored by little statesmen and philosophers and divines.” I believe the point he was trying to make is that only small-minded people don’t change their views when the circumstances change or evidence contrary to your beliefs is uncovered. 2020 was a memorable year for a number of reasons. Excluding the far-reaching impact of the Coronavirus Pandemic, I made a decision to alter the strategy of the Ashva Capital LP fund. As you know, Ashva Capital LP was originally launched as an investment vehicle focused on the Indian equity market. However, our original investment mandate gave us the flexibility to invest globally to find the best investment opportunities. Even prior to the Covid pandemic, I was becoming concerned about valuation levels in the Indian equity market. The stellar market performance from March 2020 to December 2020 will not be repeatable going forward. The chart below shows that the Nifty TTM P/E (blue line) bottomed at 17.2x in March 2020 as the market began pricing in the negative impact of global lockdowns. The Indian market has subsequently rallied but I think we’re late in the cycle where valuations are stretched, and significant upside is limited. Furthermore, I don’t see the scope for a material improvement in the underlying fundamentals. I think at best the Indian market will remain rangebound as P/E valuations remain stretched.

Despite my prior focus on the Indian equity market, I’ve always been on the lookout for opportunities globally. In late 2020, I was finding interesting investment opportunities in the US equity market focused on blue-chip companies providing excellent dividend yields. Given all the hype around the tech sector a large amount of high-quality blue-chip companies were and continue to be largely ignored. It’s no surprise that even Warren Buffett bought large amounts of these types of companies such as AbbVie and Bristol Myers Squibb in the fourth quarter of 2020. He definitely knows a bargain when he sees one. I’ve also initiated positions in both stocks via options strategies that I’ll discuss in more detail later in this letter. My main goal was to highlight that there are currently numerous bargains in certain sectors of the US equity market despite the S&P 500 crossing the 4,000 mark for the first time in its history. Chuck Carnevale, the founder of Fast Graphs, always says “it’s a market of stocks, not a stock market.” Thus, attractive investment opportunities always exist but you have to look harder when the indices are sitting near all-time highs.

Poor Man’s Covered Call

Additionally, I began my investing career heavily focused on options trading. Although my current investment strategy can best be summarized as buy and hold high quality companies for the long-term, I was exploring ways to increase current income and mitigate downside risk. Naturally, a covered call strategy made sense and can provide both current income and downside protection. A covered call strategy means buying the underlying shares and then selling a call option at a specified strike price. A call option gives a buyer the right to buy shares at the strike price. We as the sellers receive a premium for selling the right to buy our shares. The premium we collect from selling call options can be substantial and, in many cases, effectively doubles the dividend yield of the underlying shares. However, there is a significant tradeoff as with most things in life. By selling call options you will limit your upside potential in the stock. Since the call option buyer will exercise his right to buy your shares if they trade above the strike price. You can mitigate this risk by selling calls that are significantly out of the money, but you’ll also generate less current income. The ideal situation is that after selling a call option the share price stays below the strike price on the expiration date. Thus, you get to keep the premium you received from selling the call and the underlying shares. Additionally, you can always buy back the shares if you think that the shares still have significant upside potential.

In addition to writing covered calls, I’ve implemented a related strategy called the Poor Man’s Covered Call (PMCC). Mechanically it’s the same as writing a covered call but instead of owning the underlying shares you take a long position in a far-dated call option at a lower strike price than the one you’re selling. The main benefit of the Poor Man’s Covered Call position is that it requires significantly less capital than buying shares outright. For example, if you wanted to write a covered call on Amazon (AMZN) you would need to purchase at least 100 shares at a current price of $3,226.73 for a total of $322,673. In comparison, you could purchase a LEAPS contract for January 21, 2022 at a $3,200 strike price for a total $35,000. LEAPS, or long-term equity anticipation securities, are basically options contracts with an expiration date more than a year away. We use LEAPS as a replacement for stock ownership in a covered call transaction to reduce theta decay. I won’t go into a laborious discuss of options “Greeks”, which are delta, gamma, vega and theta. The “Greeks” basically measure the sensitivity of an option’s price to quantifiable factors. I’ve entered into a Poor Man’s Covered Call position in AbbVie during Q1 and expect to sell near-term calls against the position over the course of the year to generate income and lower our cost basis on the original position.

Additionally, we have also implemented an income cycle strategy in the portfolio. The income cycle begins with selling cash secured puts on a stock we would like to own. Put options give the buyer the right to sell his shares at a specified strike price. As the seller of the put, you receive a premium and will be required to purchase the shares at the specified strike price. Put options are generally only exercised if the share price is below the strike price upon the expiration date. In the event our short put option is exercised, we will then purchase the shares at the specified strike price. At the same time, we will sell a covered call on the new position and will also collect all dividends. If the shares are called away, we again sell put options and the entire income cycle repeats. We have initiated an income cycle strategy on BMY in Q1 by selling puts that expire on April 30, 2021.

Despite the shift in strategy, our underlying principles of identifying high-quality companies trading at reasonable valuations remains the same. However, we will now use the PMCC and income cycle strategies to enhance current income and reduce our cost basis in our long positions. Mainstream US equities have compounded at 7% above the rate of inflation for over a century. We expect the US economy and US equities to prosper in the years ahead. There will obviously be significant corrections and even crashes, but we believe that US equities will ultimately return to their long-term trendline growth. Furthermore, we expect the individual companies that we invest in to outperform the market over the long-term.

US Equity Market

March 23, 2021 marked the one-year anniversary of the pandemic’s bear market low. On that Monday over a year ago the S&P500 closed at 2,237.40. As I’m writing this letter the S&P500 has just crossed 4,000 for the first time in its history. The Federal Reserve must be given credit for stepping up and offering unlimited liquidity to support the economy. The US economy is well on the recovery path and the equity market will continue to be a primary beneficiary. With the proliferation of vaccinations, the pandemic is clearly now in the rearview mirror.

Total nonfarm payroll employment increased by 916,000 jobs in March and unemployment edged down to 6%. Economists are now forecasting potentially 1+ million monthly job gains through the end of summer. Most prognosticators are now fretting about the likelihood of inflation roaring back into the economy. I’m not sure anyone can really forecast with any degree of certainty whether inflation will come back. However, I can tell you that with the 10-year US treasury yield at 1.72%, you don’t want to be holding fixed income with the prospect of higher inflation ahead. Equities are not a perfect inflation hedge but will perform significantly better than bonds in any scenario where inflation starts rising. Furthermore, most economists don’t expect the US economy to start slowing down until the 10-year yield goes above 3%. We’re still a very long way from that scenario.

Our Performance

As of March 31, 2021 the Ashva Capital LP fund was down (1.56%) year-to-date. This was largely a function of the portfolio not being fully invested. Due to the switch in strategy, it will take some time to get the portfolio invested. It’s generally detrimental to performance to keep a cash balance in a market that continues to hit new highs, however, I believe that it’s the prudent thing to do. I only wan to put high conviction ideas in the portfolio. As it takes time to conduct research and build conviction, the short-term impact will be negative in terms of relative performance to the market. However, in the long-run only investing in our best ideas will result in superior long-term returns. With the broader equity market trading at elevated valuation levels it’s easy to overpay for quality. As a result, we remain focused on identifying blue-chip companies trading at reasonable valuation levels. Fortunately, we’re finding enough opportunities to populate the portfolio.

Sincerely,

Ankur Shah

Managing Member

Ashva Capital Management LLC