Financial security is important to so many Americans but perhaps never more than during the last year. Over the course of the pandemic, people’s lives have been turned upside down in many ways, including financially – with a lot of people losing their jobs, needing loans, or accruing back rent, and the like.

Q1 2021 hedge fund letters, conferences and more

With many taking on new debt and finding themselves in difficult financial positions, Medical Alert Buyers Guide wanted to get an understanding of people’s financial security before and during the pandemic to figure out what has changed and what hasn’t. They recently conducted a survey to get a sense of just that, and the results showed a pretty varied response – much of it surprising.

Financial Security Of Americans: Then vs Now

With the question of financial health in the forefront, Medical Alert Buyers Guide asked 1,006 respondents about the shape they were in before the pandemic compared to now. About 20% of those surveyed said they were extremely to very financially healthy, while 62.9% said somewhat to slightly, and 17% said they weren’t financially healthy at all.

Has the pandemic changed how manageable debt is, though? According to the survey, not very much. Interestingly, 52.4% said their debt was just as manageable as it was before the pandemic. Nearly 3 in 10 said it was less manageable, and 18.1% found it more manageable. Millennials and Latinos, the study found, were more likely to say they had less manageable debt during the pandemic.

Despite feelings on the manageability of debt, the majority of respondents – 42.6% – said their debt increased during the pandemic. Nearly 22% said their debt decreased, while 35.5% said theirs stayed the same. The results got even more eye-opening when broken down by race/ethnicity: 45.7% of Black Americans said their debt increased, 39.7% of Asian Americans said the same, and 43.5% of Latinos and 40.9% of white Americans did as well.

The Unemployment Situation

Of course, questions have loomed about the impact of unemployment and furloughs over the course of the pandemic – as they relate directly to people’s financial security. An astonishing 59% of people who were either furloughed or laid off during the pandemic said that their debt increased over that time. Only 19.7% said that theirs decreased, and 21.3% said theirs stayed the same. Among those not laid off or furloughed, 48.1% said their debt remained the same.

Spending

Stimulus checks, for so many people, were sent throughout the pandemic as a way to help people get on their feet and get bills paid following layoffs and furloughs. For others, though, they were seen as a way to potentially help stimulate the economy. Though a majority spent theirs when the first check went out in mid-2020, it seems that many either saved it or paid off debt with those funds. That begs the question: How did people’s spending habits change in 2020?

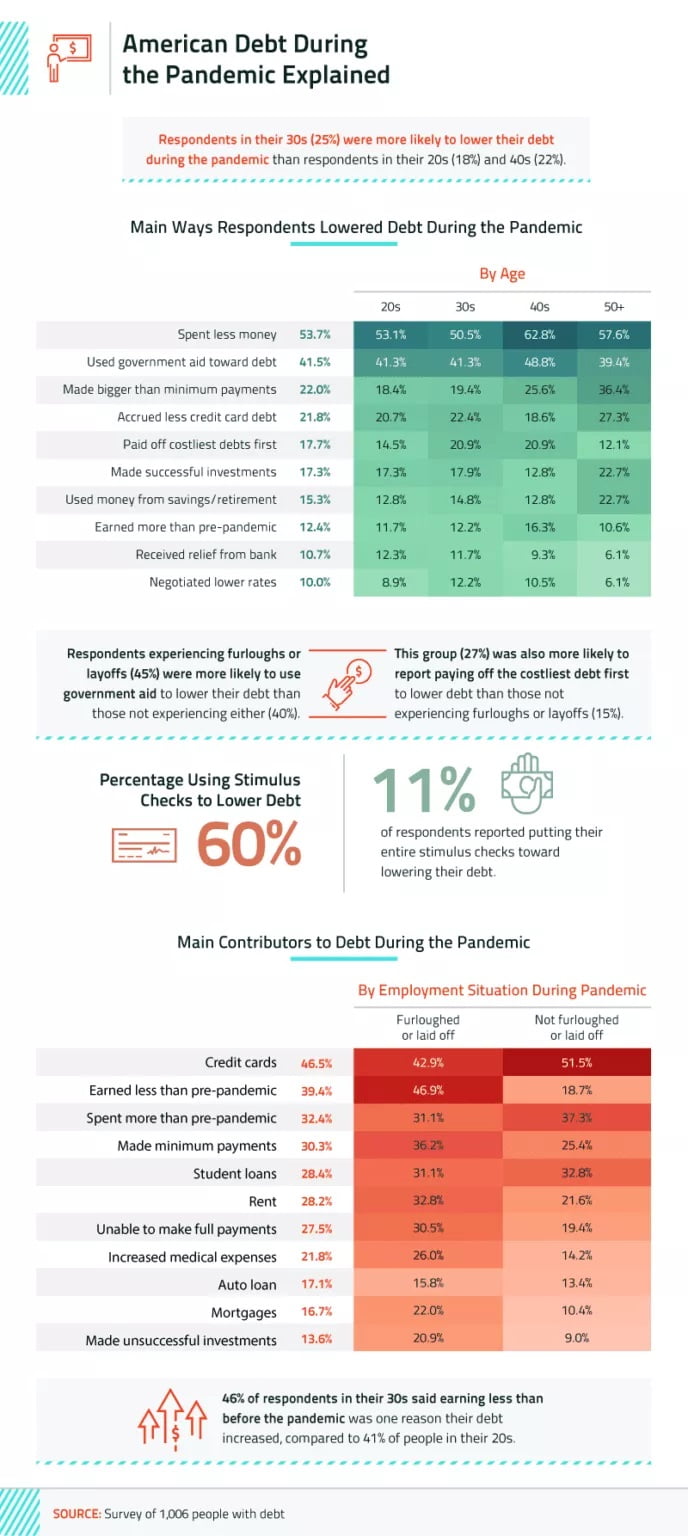

The Medical Alert Buyers Guide study showed that the majority of people in their 30s were more likely to have less debt at the start of the pandemic, compared to people in their 20s and 40s. And the ability to spend less money was overwhelmingly the reason that it seems people managed to lower their debt over the course of the pandemic.

Specifically, 53.1% of those in their 20s said that spending less was the primary way they lowered their debt since the pandemic, with 50.5% of those in their 30s, 62.8% of respondents in their 40s, and 57.6% of those over 50 saying the same. When it comes to using their stimulus toward debt, 48.8% of those in their 40s said they lowered their debt by cashing their stimulus check.

Interestingly, 45% of respondents who were laid off or furloughed said they were more likely to use their stimulus check for lowering debt, compared to 40% who didn’t get furloughed or laid off.

What contributed to debt during the pandemic, though? Perhaps unsurprisingly, credit card debt was the biggest culprit. Overall, 46.5% of respondents said credit cards were the main source of debt during the pandemic – with 42.9% of those who were laid off or furloughed naming this as the reason, and 51.5% of those who weren’t saying the same.

Making less money than before the pandemic was also a major factor in debt accruing, with 39.4% of respondents overall saying this factored heavily into the reason for their debt. Almost a third of those surveyed said they felt that their spending increased during the pandemic, causing debt, and 30.3% pointed to making minimum payments on their existing debt as a major reason behind the struggle.

Reducing the Debt

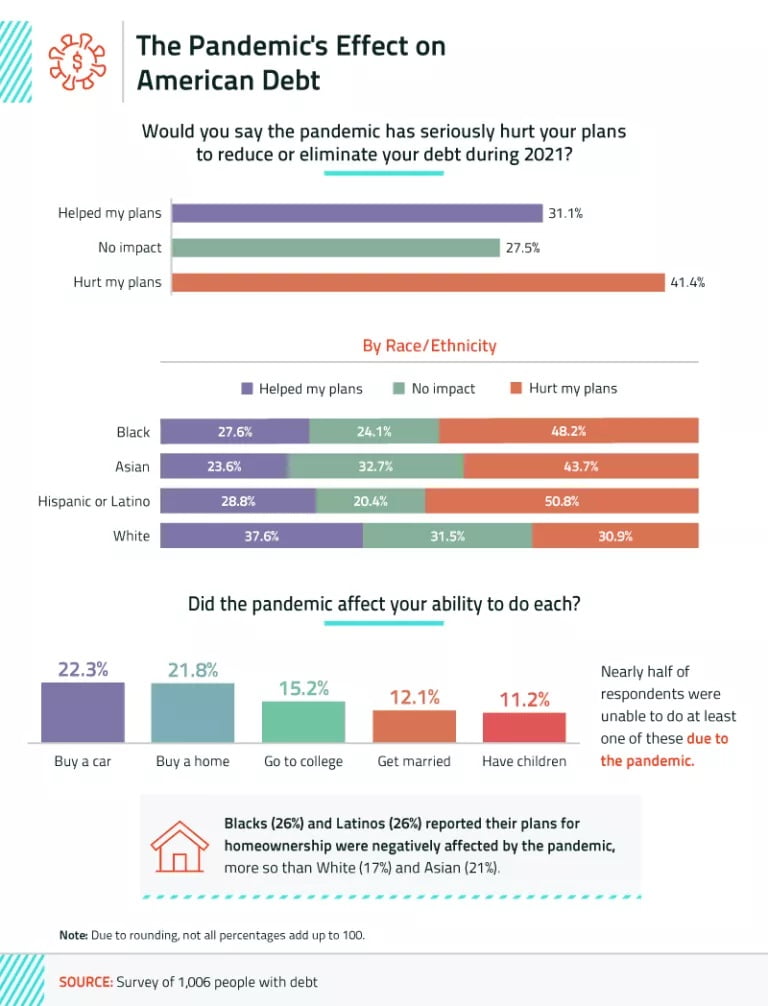

How did the pandemic impact people’s aspirations and plans to reduce debt in the new year? As it turns out, 41% said it had a negative impact. For 31%, though, it actually helped them in their plan to lower debt in the new year. Broken down by race/ethnicity, these numbers get really eye-opening.

The study showed that 50.8% of Latinos said their plans to lower debt were hurt by the pandemic, though the numbers for Black Americans and Asian Americans weren’t too far behind. Just over 48% of Black Americans and 43.7% of Asian Americans said the pandemic hurt their debt-lowering plans in the new year.

Overall, other plans like buying a home or car, going to college, having children, and getting married were impacted by the pandemic from a financial standpoint as well. Roughly 22% of respondents said the pandemic hurt their plans to buy a car, while 21.8% said their plans to buy a house were impacted. Thankfully, when it came to things like getting married and having children, the numbers were much lower – only 12.1% of respondents said they felt the pandemic negatively impacted their marriage arrangements, and 11.2% said their plans to have kids were hurt.

The Future

There does seem to be an end in sight for this pandemic, which has upended the lives of so many people. With vaccines rolling out, cases slowly but surely dropping, and stimulus checks helping people stay afloat, things seem to be very gradually getting better. For many of those surveyed, the future of their financial health seems bright as well.

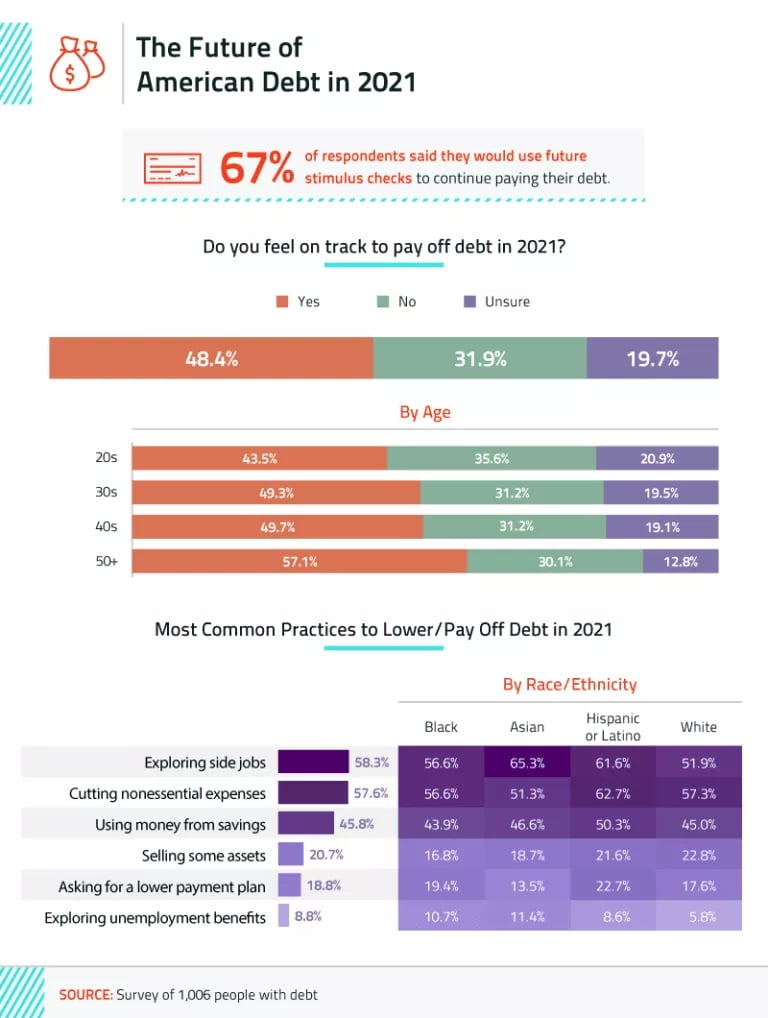

More than 48% of those surveyed said they felt they were on track to paying off their debt this year, while 31.9% said they weren’t, and 19.7% said they were unsure. When it comes to ways people planned to pay off their debt in 2021, 58.3% said that they were exploring side gigs or part-time work as a way to chip away at debt.

Whatever the strategy, there’s no doubt that 2020 was a difficult financial year for many. The survey showed just a glimpse into people’s financial health during this time, and although many felt the impact, it certainly seems that there are brighter days ahead.

Article By Sean Kelly