Alta Fox Opportunities Fund commentary for the fourth quarter ended December 31, 2021.

Q4 2020 hedge fund letters, conferences and more

Limited Partners,

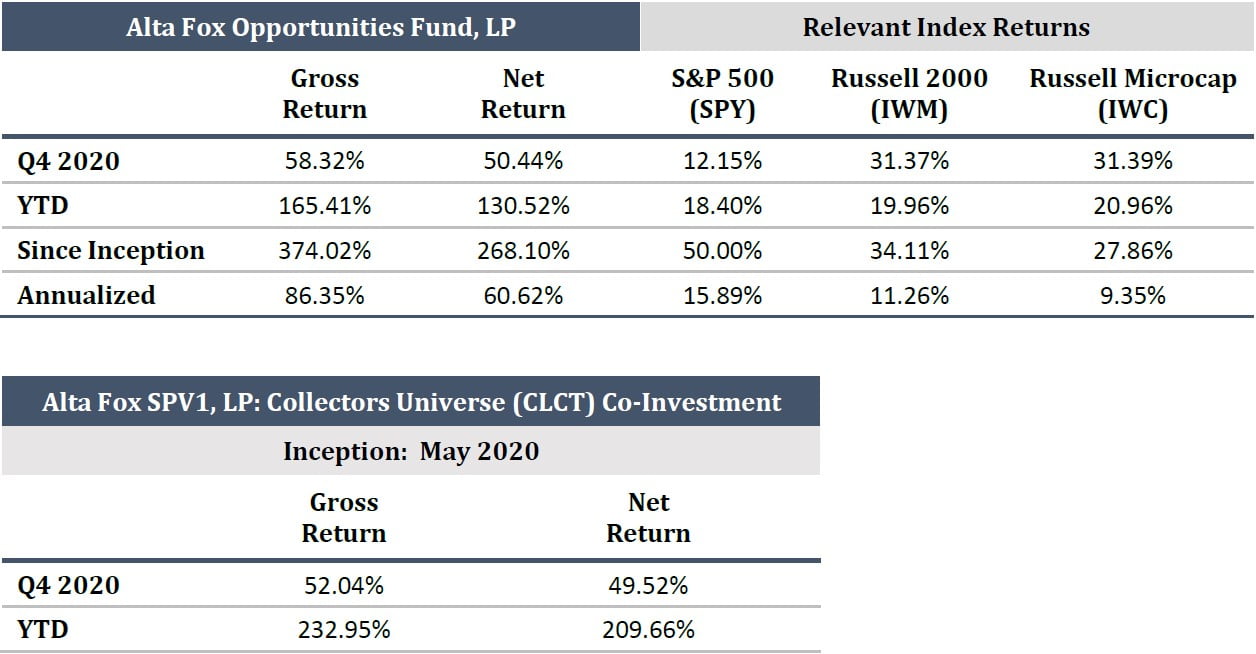

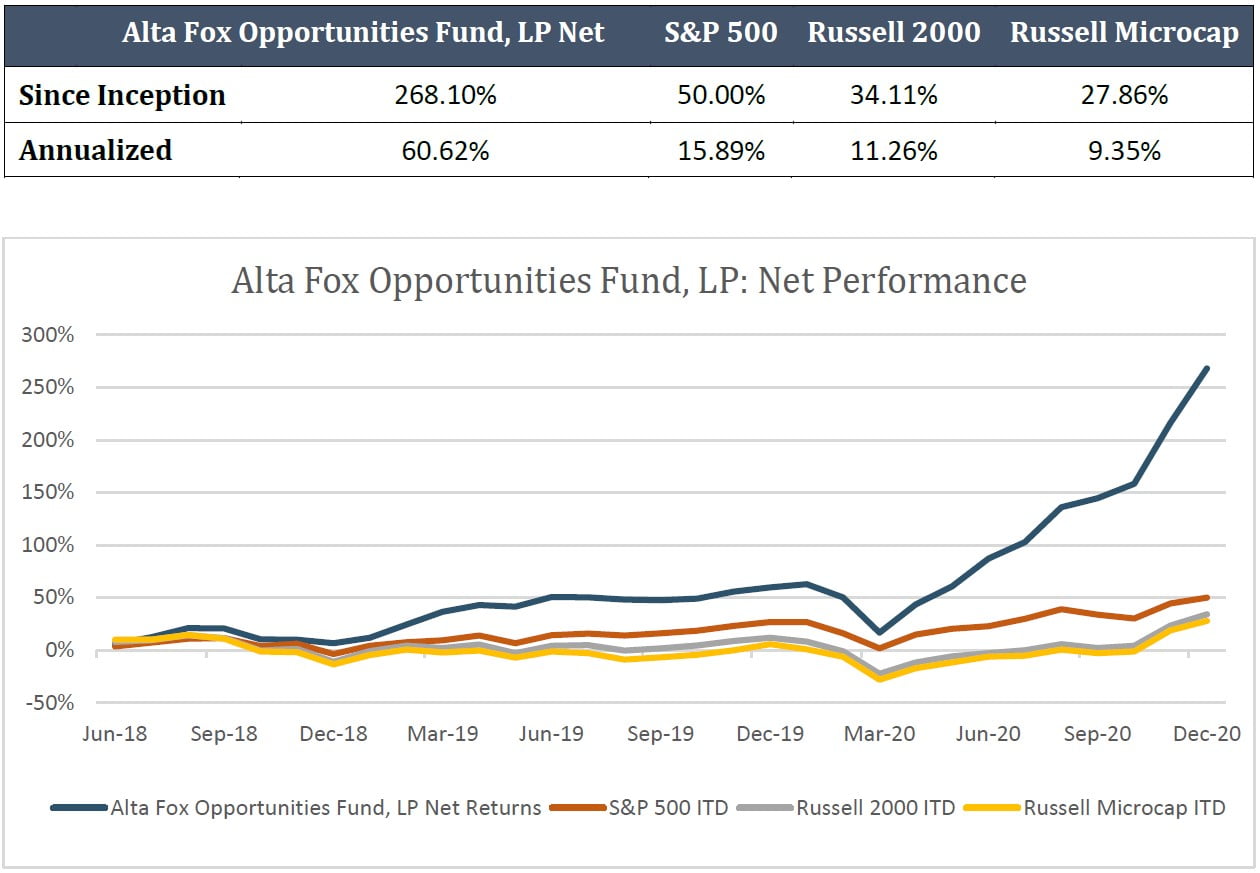

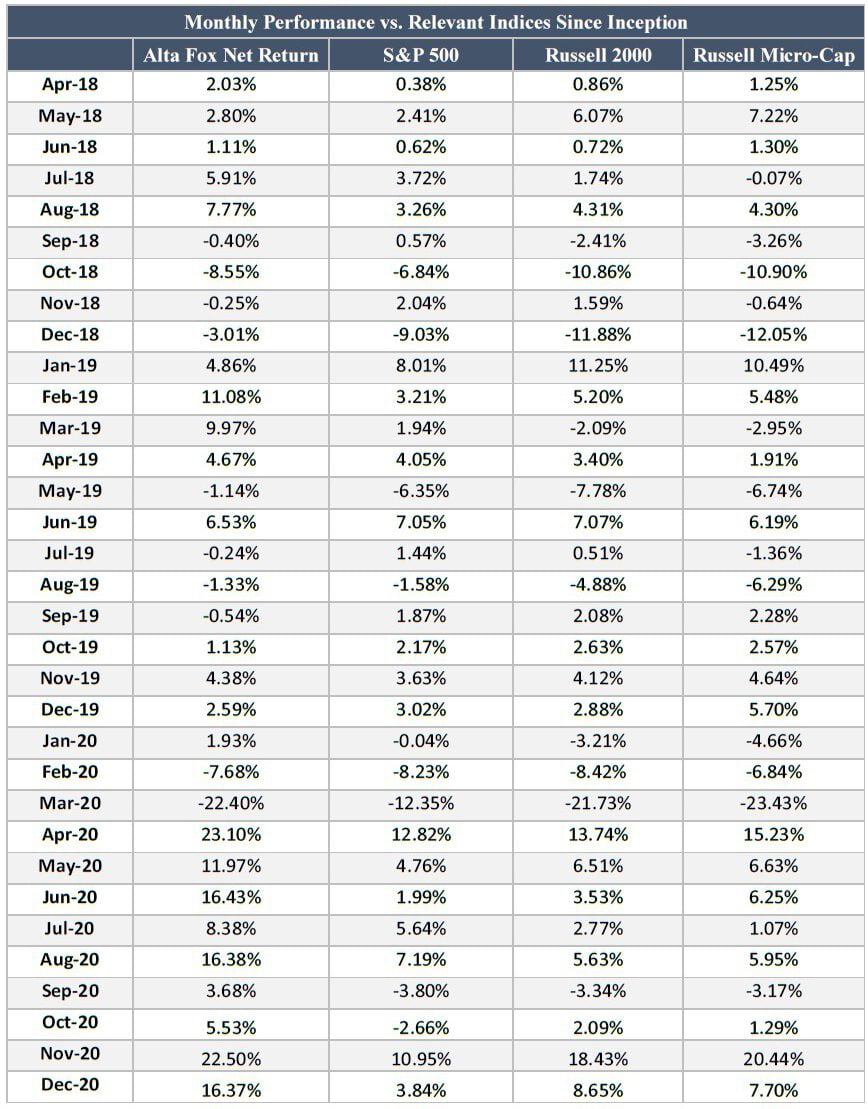

In Q4 2020, the Alta Fox Opportunities Fund (“the Fund”) produced a gross return of 58.32% and a net return of 50.44%. This brought the YTD gross return to 165.41% and YTD net return to 130.52%. The Fund’s average net exposure during the quarter was 86.92%. Since inception in April 2018, the Fund has produced a gross return of 374.02% and a net return of 268.10% compared to the S&P 500’s return of 50.00%, the Russell 2000’s return of 34.11%, and the Russell Microcap’s return of 27.86%. In addition, Alta Fox’s first co-investment offering (“the SPV”) related to our Collectors Universe (CLCT) activist position produced a net return of 209.66% since its inception in May of 2020. See the below table and appendix for further details.

At Alta Fox, we focus on the long-term growth of our portfolio’s intrinsic value and avoid being influenced by short-term fluctuations in prices or the market. We encourage our limited partners to do the same, in times of outperformance and underperformance.

Alta Fox Opportunities Fund: Review of 2020

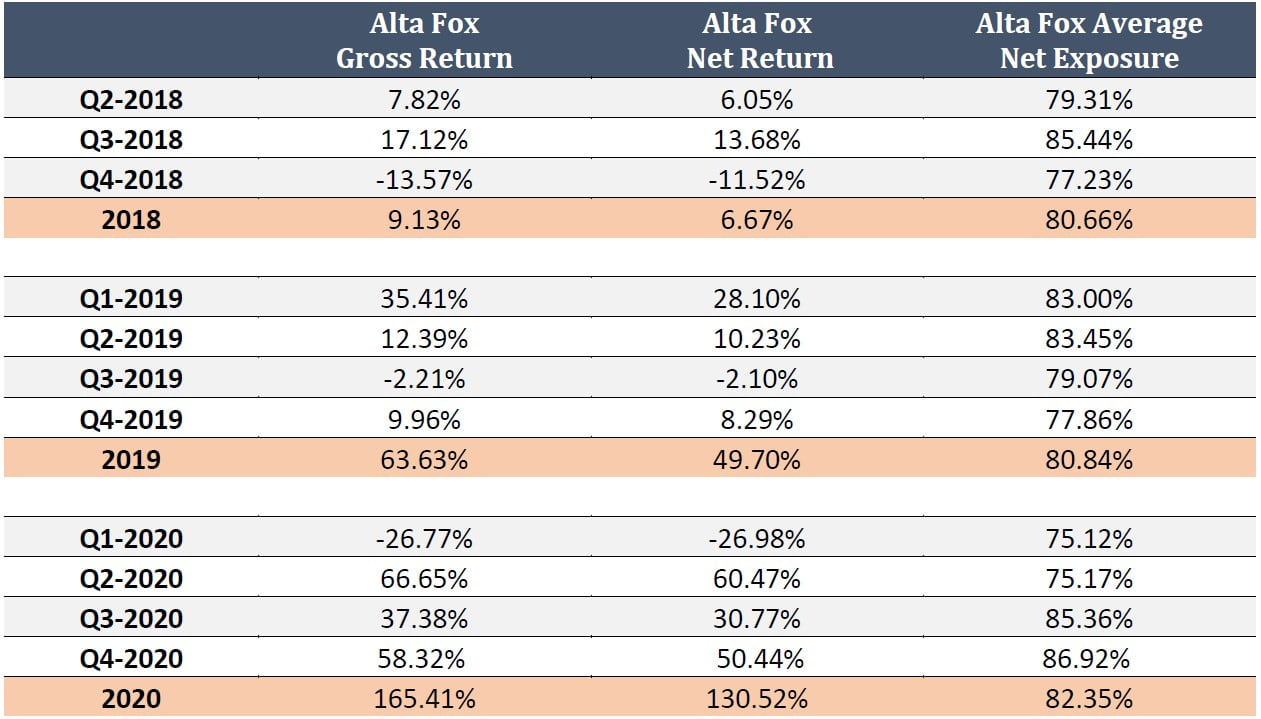

2020 was a strong year for the Fund, which generated a net return of 130.52%. Throughout the year, the market provided an extremely favorable environment for Alta Fox Opportunities Fund given significant volatility, panic selling, and meaningful dispersion.

Over the course of the year, Alta Fox remained focused on identifying opportunities to buy high-quality businesses with competitive advantages at cheap multiples of medium-term earnings power. We applied a consistent framework to all companies that we researched and assigned a numerical score across several categories, including one of the more important metrics this year, “conviction.” During the COVID-19 market crash in March, our level of conviction became more important than ever because we (along with the market) were faced with too many unknowns to have high conviction in medium-term estimates for a large percentage of companies we were tracking. After all, when businesses are closed down and the world is facing a once in a century pandemic, it is safe to assume that most medium-term earnings estimates are at risk. However, for some of the companies on our watchlist, COVID-19 actually increased our conviction in our medium-term forecasts. For themes like online gaming and certain consumer staples businesses, our medium-term fundamental forecasts increased even though stock prices were falling precipitously. For many of these oversold names, we had gathered high-quality channel checks that further increased our conviction that the market was mistakenly selling off good businesses for non-fundamental reasons. This was the proverbial “baby thrown out with the bathwater” that we referenced in our Q1-2020 letter.

As we diligently revisited each position in the portfolio and all companies on our watchlist, we cycled out of names with low conviction scores, despite high IRR estimates, into names with equal or greater IRR estimates and much higher conviction. This repositioning created higher than expected turnover in the portfolio, but many of these high IRR, high conviction names returned several hundred percent over the remainder of the year. Despite this higher-than-expected turnover, the vast majority of 2020’s returns were either long-term or unrealized. While we cannot ensure this outcome in any given year, the Fund always strives to be tax efficient.

Our strong 2020 still included several mistakes in the research process (versus outcome) and provided opportunities to learn and improve. We sold some companies at the worst possible time in March, misdiagnosed some key risks related to customer concentration and management evaluation (even pre-covid), and could have better prioritized our limited research bandwidth. After reviewing these weaknesses, we introduced new checklist items to improve our process and are always looking to supplement human capital with scalable productivity tools. As we reflect on 2020, we are satisfied with the return that the portfolio generated but most proud of the process that was consistently applied along the way.

Activism/Corporate Governance

In 2020 and very recently, we played the role of reluctant activist on two occasions. The first was related to our investment in Collectors Universe (CLCT). We began building our position in March of 2020 and bought most of our shares in the low to mid $20’s. Alta Fox first filed a 13D in June and settled with the company in September. The company then received a tender offer in November at $75.25. Alta Fox publicly filed for appraisal rights in December. The offer was recently revised at $92.00/share. Today we updated our 13D filing, as required by the SEC, to confirm our demand for appraisal rights at the updated offer price. We have conducted a tremendous amount of research on this investment and we are in no rush to relinquish our significant stake given the surging demand, growing backlog, and numerous attractive reinvestment opportunities. Alta Fox typically enjoys sharing our work with our dedicated investor following, but in this case, the vast majority of our research remains unseen, even by the Fund’s limited partners. The depth of the work we did on Collectors Universe sets an aspirational standard for work we will do in the future. We did many things right with this investment and learned a few first-time activist lessons, but overall, we are extremely proud of what we were able to accomplish thus far for our limited partners. Although this position was a significant contributor to the Fund’s performance in 2020 (and all of the SPV’s performance), its contribution represented less than a third of the Fund’s total return for the year. The story is not over.

The second and more recent case of activism is related to our position in Enlabs AB (NLAB), an online gambling company based in Sweden, which has been a significant position in the portfolio over the last year. We first published research on the name in July, revisited our work publicly in October, and in early January 2021, the company received a bid to be purchased at a 1.1% premium. While activism in Sweden is not as formal and does not have the same regulatory framework as in the U.S., our recent involvement has included taking a public stance against the Board of Directors and working hard with other shareholders to prevent an opportunistic takeover of the company. Our research, press release, and additional commentary can be found at: www.altafoxcapital.com/nlab. While we do not enjoy the hostility associated with activism, we believe there is currently a crisis in governance in the small-cap space which has been exacerbated by the growing percentage of passive ownership. When necessary, Alta Fox will fight for the interests of our limited partners and the rights of minority shareholders. It is unfortunate when Corporate Boards forget that they have an obligation to serve shareholders’ interests before their own. Rest assured, in these cases, Alta Fox will remind them of their obligation.

Current Portfolio and Positioning

As a guiding metric, we aim to have at least twice as many exciting new ideas on our watchlist as there are positions in the portfolio and at this time, the opportunity set appears plentiful. Recently, we have been spending considerable time on international opportunities given a significant rally in the U.S. small-cap market. One non-U.S.-based company we are very excited about is a small-cap, family-run business that has generated outstanding shareholder returns for many years. The business is benefitting from a strong secular trend, and we believe it is about to experience a significant inflection in profitability. The obviousness of this impending inflection point is obscured from consolidated financials, making this name a suitable Alta Fox gem. We plan to share our research on this name soon and investors can sign up for our email distribution list for all future updates and publicly posted ideas here: www.altafoxcapital.com/contact.

As always, we do not believe we have an edge in predicting the direction of the general market at any given point in time. While there are certainly many signs of froth (SPAC mania, retail option buying, etc.), we are still finding more interesting opportunities than we have time to fully research and look forward to continuing to dig deep, ask the right questions, and identify the next set of winners.

Alta Fox – Business Updates

In January of 2021, we received a significant commitment from an extremely aligned and long-term investor that has spent years following and getting to know Alta Fox. The commitment will absorb all available capacity for new investors through at least the first half of this year. We will be deploying this capital slowly at a pace that aligns with the opportunity set available to the Fund. Our goal at Alta Fox remains to be the best (as measured by Fund performance net of fees), not the biggest. We believe the Fund’s AUM is still significantly below estimated capacity, and we will continue to be conservative in how we deploy capital in the future. Nonetheless, we look forward to staying in touch with like-minded allocators who are considering an investment in the Fund once capacity becomes available.

We are in the final stages of adding a Senior Analyst to the team. We are excited to share additional details on that hire in the Q1 2021 letter. We were overwhelmed with the quantity and quality of candidates who expressed interest in joining our team and believe this bodes well for our ability to attract significant talent in the future. On the operations side, we onboarded Constellation Advisors as our Outsourced CFO in support of our commitment to continuously strengthen all aspects of our business.

Conclusion

The continued support of our LP-base has been especially important and appreciated in such a tumultuous year. Alta Fox remains committed to building a world class investment firm and we are proud of our early progress towards that goal.

If you would like to indicate interest in investing once we re-open, please note that the minimum initial investment is $1.0 million and, due to regulatory requirements, the Fund will only be available to Qualified Purchasers.

Sincerely,

Connor Haley