Recap from April’s Picks

Our Most Attractive Stocks (+4.0%) outperformed the S&P 500 (+1.5%) last month. Most Attractive Large Cap stock Hawaiian Holdings (HA) gained 18%. Most Attractive Small Cap stock Maui Land & Pineapple (MLP) was up 20%. Overall, 26 out of the 40 Most Attractive stocks outperformed the S&P 500 in April.

Our Most Dangerous Stocks (+2.5%) underperformed the S&P 500 (+1.5%) last month. Most Dangerous Large Cap stock Vornado Realty Trust (VNO) fell by 5% and Most Dangerous Small Cap stock Uni-Pixel Inc. (UNXL) fell by 41%. Overall, 16 out of the 40 Most Dangerous stocks outperformed the S&P 500 in April.

The successes of the Most Attractive and Most Dangerous stocks highlight the value of our Robo-Analyst technology, which helps clients fulfill the fiduciary duty of care when making investment recommendations.

13 new stocks make our Most Attractive list this month and 11 new stocks fall onto the Most Dangerous list this month. May’s Most Attractive and Most Dangerous stocks were made available to members on April 5, 2017.

Our Most Attractive stocks have high and rising returns on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied by their market valuations.

Orbotech Ltd. (ORBK) is one of the additions to our Most Attractive stocks for May. ORBK is a technology sector company that provides supply-chain solutions for manufacturers of printed circuit boards, flat panel displays and semiconductors. ORBK’s revenues and profitability have been inconsistent at times over the past decade but have established more favorable trends over the past few years.

Per Figure 1, revenues grew 7% compounded annually and after-tax profit (NOPAT) grew 6% compounded annually from 2006-2016. Since 2012, however, revenue growth has improved to 19% compounded annually while NOPAT margin improved from 1% in 2012 to 12% in 2016.

Figure 1: ORBK’s Ten-Year Revenue and NOPAT Margin

Sources: New Constructs, LLC and company filings

ORBK currently earns an 11% return on invested capital (ROIC), which has risen four consecutive years from 1% in 2012 and now ranks in the second quintile of our 3,000+ stock coverage universe. Furthermore, annual free cash flow (FCF) has tripled from $32 million in 2012 to $96 million (6% of market cap) in 2016.

Low Expectations Embedded in Valuation

The stock has been rewarded for its improving ROIC and is up 48% over the past year vs. 19% for the S&P 500. Despite the increase, ORBK remains undervalued. At its current price of $35/share, ORBK has a price-to-economic book value (PEBV) ratio of 0.9. This ratio means the market expects profits to permanently decline by 10%. This expectation seems too pessimistic considering the company has grown NOPAT 6% compounded annually over the past decade and has experienced an acceleration of NOPAT growth since 2012.

If ORBK can maintain 2016 NOPAT margins (12%) and grow revenues and NOPAT just 5% compounded annually over the next decade, the stock is worth $55/share today – a 57% upside.

Impacts of Footnotes Adjustments and Forensic Accounting

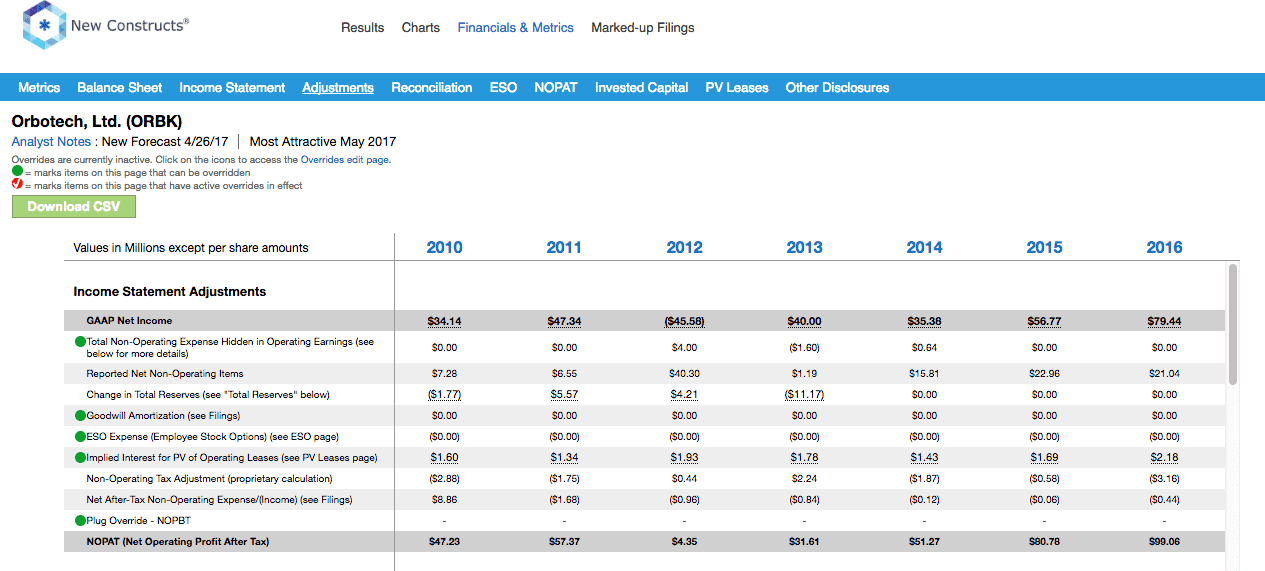

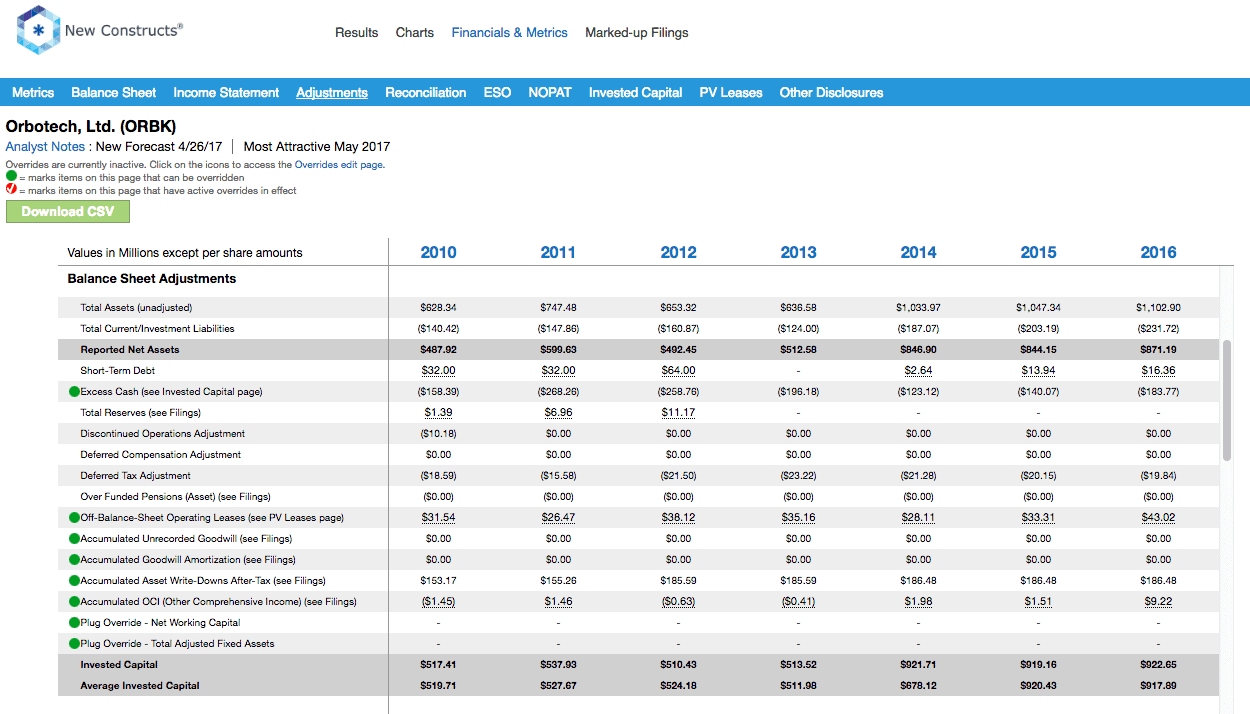

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to ORBK’s 2016 10-K:

Income Statement: we made $27 million of adjustments, with a net effect of removing $20 million in non-operating expense (3% of revenue). We removed $4 million in non-operating income and $23 million in non-operating expenses. You can see all the adjustments made to ORBK’s income statement here.

Balance Sheet: we made $467 million of adjustments to calculate invested capital with a net increase of $47 million. One of the largest adjustments was $186 million due to asset write downs. This adjustment represented 21% of reported net assets. You can see all the adjustments made to ORBK’s balance sheet here.

Valuation: we made $332 million of adjustments with a net effect of increasing shareholder value by $38 million. Apart from total debt, which includes $43 million in off-balance sheet operating leases, the most notable adjustment was $184 million (11% of market cap) of excess cash.

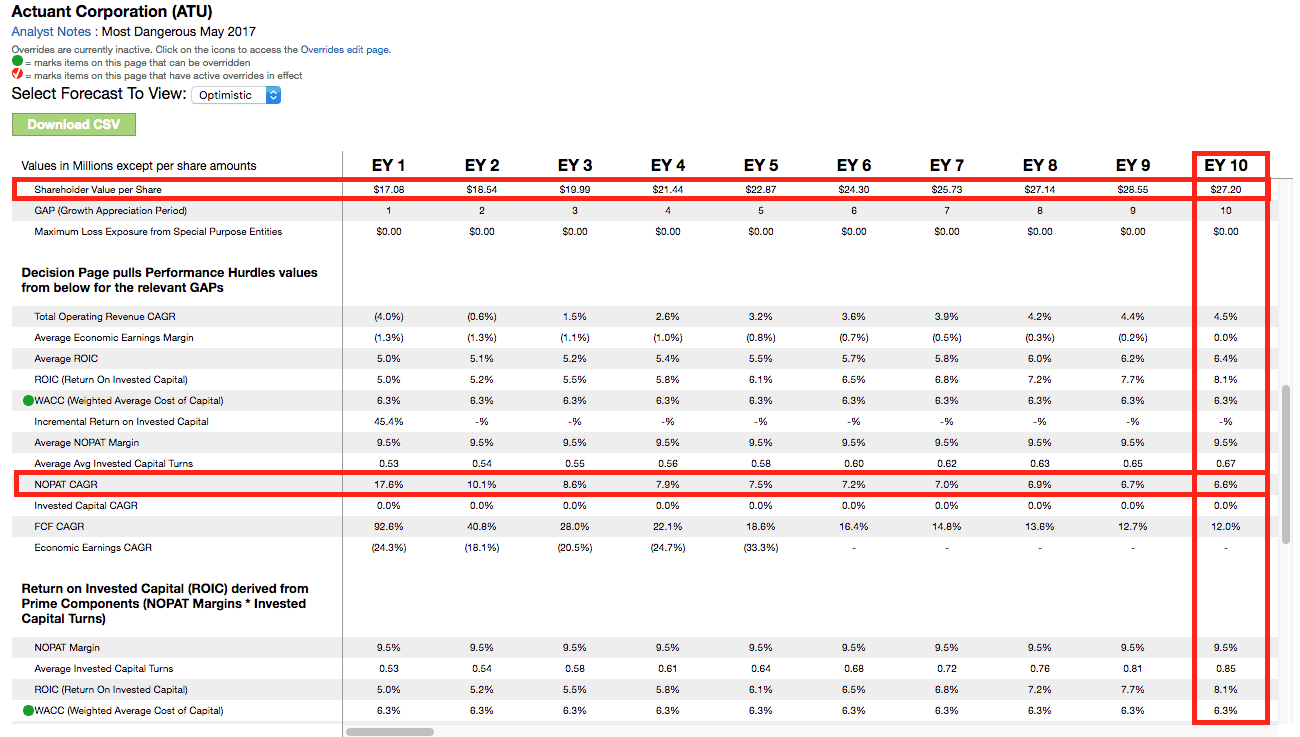

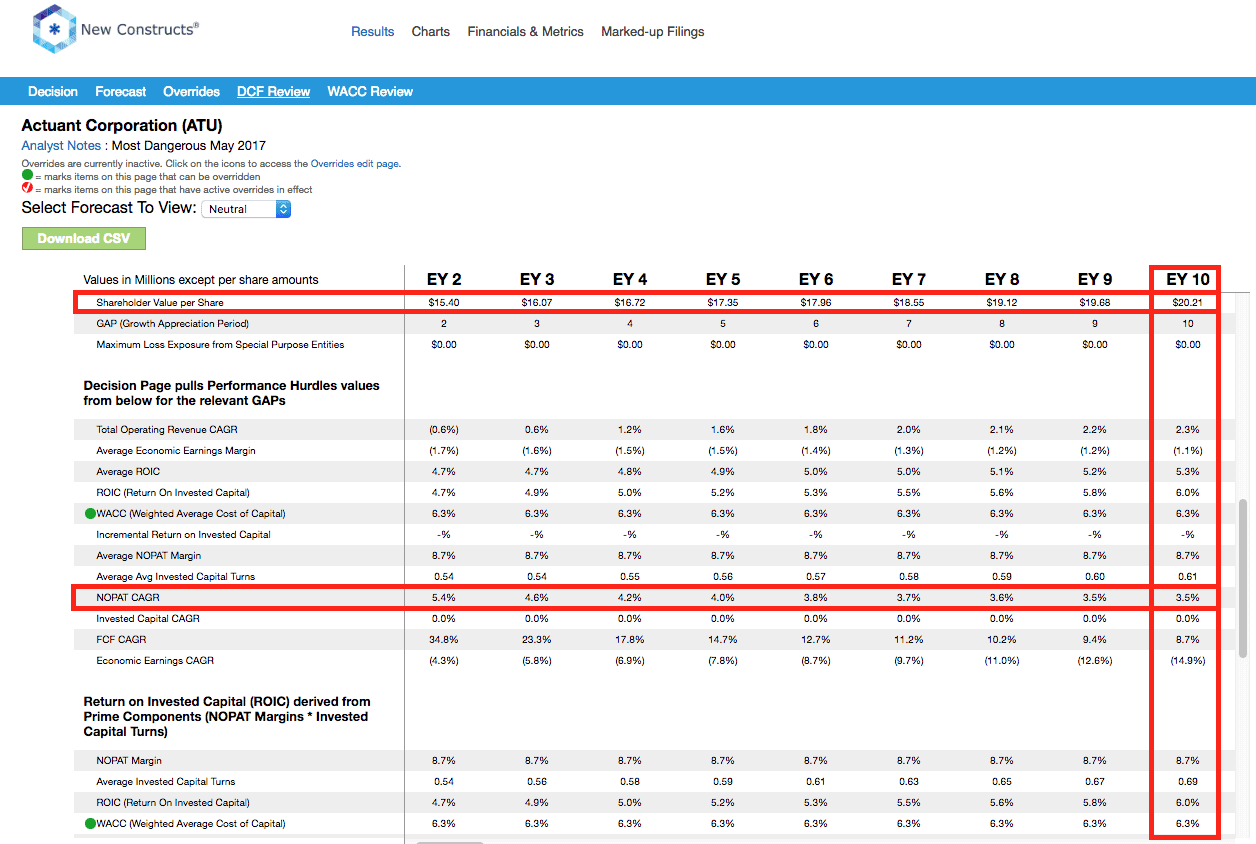

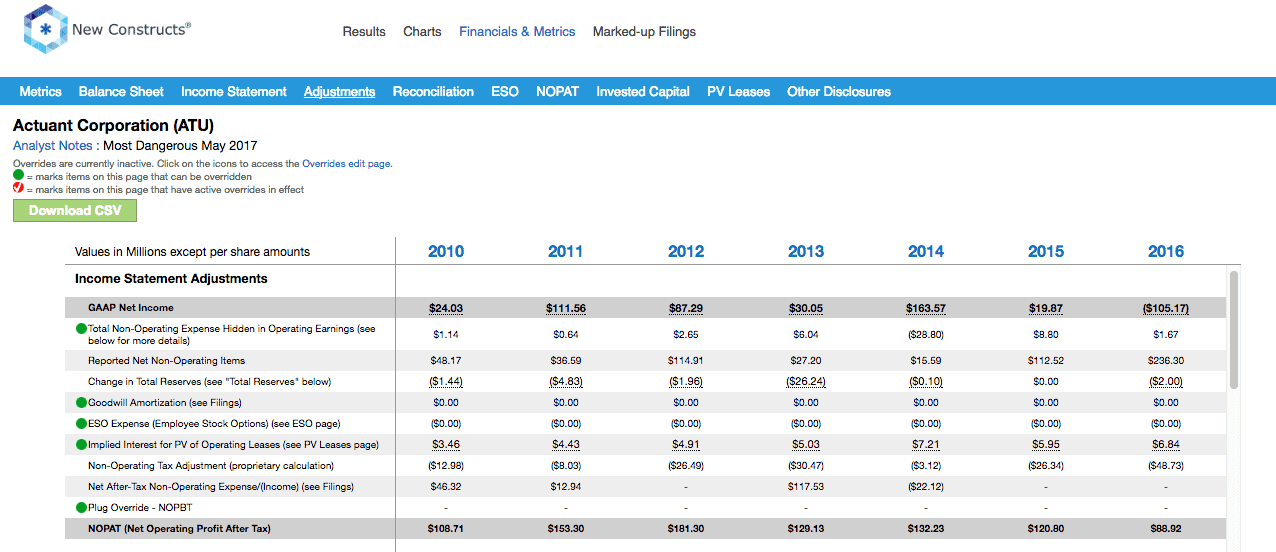

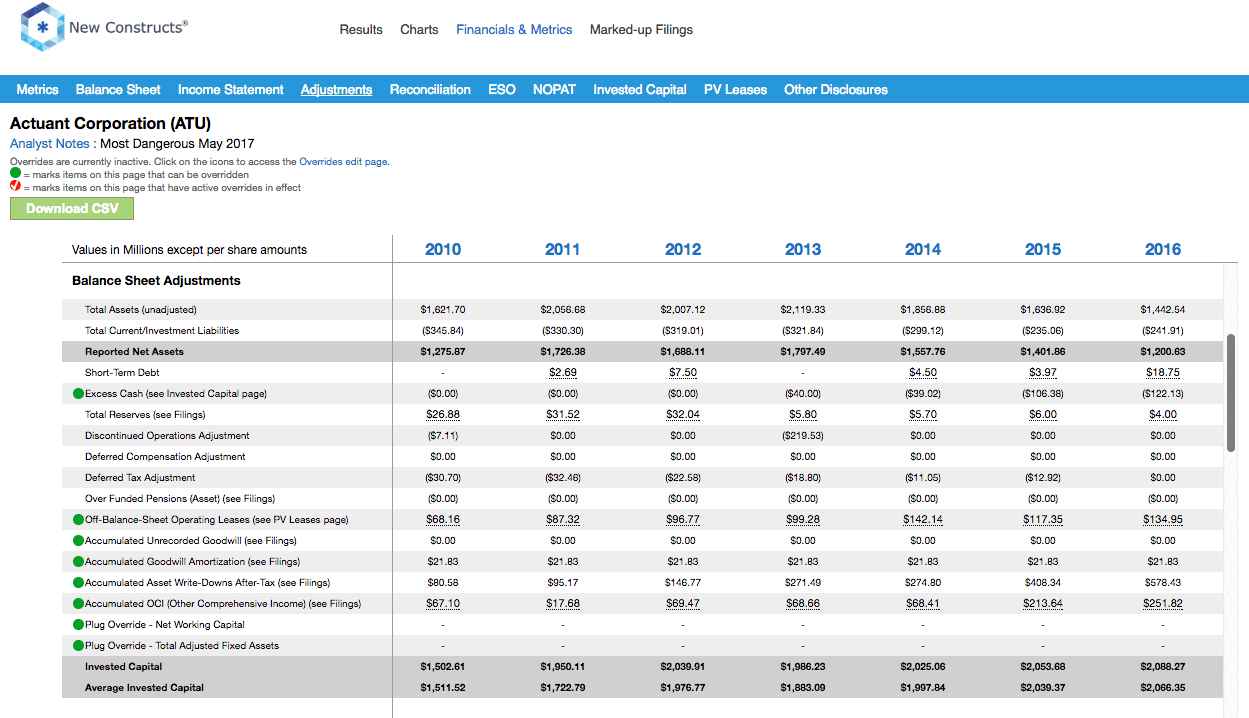

Actuant Corporation (ATU) is one of the additions to our Most Dangerous stocks for May. ATU is an industrial sector company that manufactures heavy equipment for industries such as energy and infrastructure. ATU’s revenues and profitability have been eroding for several years and fell below 2006 levels in 2016.

Per Figure 2, revenues grew 0% compounded annually and after-tax profit (NOPAT) declined 2% compounded annually from 2006-2016. Since 2012, the revenue decline has accelerated to 8% compounded annually while NOPAT margin has fallen from a high of 11% in 2012 to a ten-year low of 8% in 2016.

Figure 2: ATU’s Ten-Year Revenue and NOPAT Margin

Sources: New Constructs, LLC and company filings

ATU currently earns a 3% return on invested capital (ROIC), which has declined four consecutive years from 9% in 2012 and now ranks in the bottom quintile of our coverage universe. Making matters worse, free cash flow (FCF) has declined 40% from $92 million in 2012 to $54 million (3% of market cap) in 2016.

High Expectations Embedded in Valuation

Declining ROIC has been a headwind for the stock as the shares remain roughly 33% below late 2014 highs. However, the near 50% rally off the late 2015 low leaves the shares overvalued, especially when considering the continued deterioration in the fundamentals of the business.

To justify its current price of $27/share, ATU must grow NOPAT by 7% compounded annually over the next decade. The scenario seems rather optimistic given that NOPAT has declined 2% compounded annually over the past decade.

Even if ATU can grow NOPAT at a more reasonable, yet still optimistic, 3.5% compounded annually over the next decade, the stock is worth only $20/share today – a 26% downside.

Each of these scenarios assume ATU is able to grow revenue and NOPAT/FCF without increasing working capital or investing in fixed assets. This assumption is very unlikely but allows us to create very optimistic scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, ATU’s invested capital has grown on average by $105 million (9% of 2016 revenue), or 7% compounded annually over the past decade.

Impacts of Footnotes Adjustments and Forensic Accounting

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to ATU’s 2016 10-K:

Income Statement: we made $302 million of adjustments, with a net effect of removing $194 million in non-operating expense (12% of revenue). We removed $54 million in non-operating income and $248 million in non-operating expenses. You can see all the adjustments made to ATU’s income statement here.

Balance Sheet: we made $1.2 billion of adjustments to calculate invested capital with a net increase of $866 million. One of the largest adjustments was $578 million due to asset write downs. This adjustment represented 48% of reported net assets. You can see all the adjustments made to ATU’s balance sheet here.

Valuation: we made $910 million of adjustments with a net effect of decreasing shareholder value by $676 million. One of the largest adjustments to shareholder value was the removal of $135 million in off-balance sheet operating leases. This adjustment represents 8% of ATU’s market cap.

This article originally published on May 11, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, style, or theme.

Article by Kenneth James, New Constructs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}