As an investor, I follow a very simple model.

Q3 2020 hedge fund letters, conferences and more

I look for companies that have a track record of annual dividend increases, supported by earnings growth. I try to buy enough of these companies in order to build a diversified portfolio.

Not All P/E Ratios Are Created Equal

Naturally, everyone discusses the fact that they do not want to overpay for companies. Obviously you want to buy at a discount.

The problem with this statement is that it assumes a static environment.

We live in a dynamic environment.

If I see a company that sells at a P/E of 20, it may look optically more expensive than a company that sells at a P/E of 10.

However, we cannot just look at P/E in isolation. Not all P/E ratios are created equal.

We need to look at the stability of the earnings and cash flows for each company. A cyclical company should in general have a lower P/E ratio, because its earnings streams are not defensible and they follow the rise and fall in the economy. A more defensive company such as a tobacco or spirits manufacturer whose earnings are more immune to the short-term ups and downs of the economic cycle would be more resiliant, and therefore pricier. The market participants are willing to pay a premium (usually) for things that are easier to forecast due to the repetitive nature and stability and intanglibles such as brands.

We also need to look into the growth prospects for the company. A company with a P/E of 10, that doesn’t grow earnings is more expensive for a long-term investor than a company with a P/E of 25 that manages to double earnings every decade.

To paraphrase Warren Buffett: Price is what you pay, value is what you get

I also follow a simple model for when it comes to estimating future returns.

Future returns are a function of:

1) Initial dividend yield

2) Growth in earnings per share

3) Dividend Reinvestment

4) Changes in valuation

The Fundamentals Return

The first three items are part of the fundamentals return. The fundamental return – earnings, dividends, reinvested earnings and dividends, basically remind me that by buying a stock I am not just buying a lottery ticket, but a piece of an actual business.

That business sells products and services to customers, and hopefully it grows. Management hopefully works carefully at capital allocation too, in order to benefit shareholders. As I discussed earlier, management should invest earnings back into the business, but only if they expect those to generate a certain return on investment. If they cannot put that money back into the business and generate a high rate of return on it, they need to send it back to shareholders in the form of dividends. There is a natural limit to how much money a business can reinvest at a high rate of return and how quickly it can deploy that money as well in an intelligent manner. Just stocking up the balance sheet with cash may not be the most optimal decision. Excess cash can goad chief executives into making impulsive acquisitions at high prices, splurging on palatial headquarters or overfunding underwhelming projects. In fact, academic research shows that companies with the highest levels of cash go on to become less profitable in the long term; one recent study found that high-cash firms earn future profit margins 1.5 percentage points lower than those that carry the least cash. Source

Charlie Munger has stated that “Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you'll end up with a fine result.”

Terry Smith from Fundsmith states that Munger’s idea is a mathematical certainty.

The Ability To Reinvest Capital At High Rates Of Return

It is difficult to forecast returns or management ability to reinvest capital at high rates of return. Hence, it is important to look at predictable businesses that can deploy earnings back at a high rate of return. Not every company can do that, as there are limits to everything due to competition, nature of the industry, time etc.

But perhaps this is what Buffett was refering to with this quote “ It's far better to buy a wonderful company at a fair price, than a fair company at a wonderful price.’

It is good to buy a company that can grow earnings over time, since that grows dividends and intrinsic value. This is a good type of company to be in if you are a long-term investor. Otherwise, you would be stuck buying cheap stocks at a low P/E, that you have to sell when they get to a fair price. Only to repeat this process again and again.

Sadly, in this day and age, a lot of investors tend to view shares in terms of speculative returns.

Church & Dwight's Dividend Yield

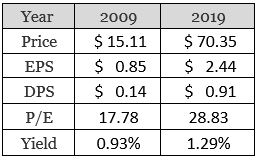

Let’s illustrate everything with an example. I will use the company Church & Dwight (CHD)

Back in 2009, the company sold at $15.11/share. It earned 85 cents/share, and had a forward annual dividend of 14 cents/share. Church & Dwight yielded 0.93% and sold for a P/E of 17.78.

Fast forward a decade, and the stock sold at $70.35/share, and earned $2.44/share. The annualized dividend rose to $0.91/share, and the dividend yield was 1.29%. The P/E ratio had expanded to 28.83.

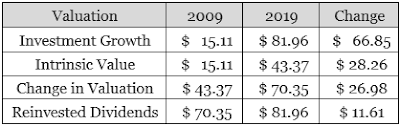

If you had bought 1 share of Church & Dwight at the end of 2009, you would have paid $15.11 for it. If you had reinvested those dividends along the way, you ended up with 1.165038 shares by the end of 2019. At a share price of $70.35/share, the total investment value went to $81.96. Not a bad return for a decade.

You can see the breakdown of sourced of return.

Intrinsic value resulted in a $28.26 increase in value, while changes in valuation resulted in a $26.98 increase in value. The rest is attributed to dividend reinvestment. I believe that changes in valuation are part of the speculative return, so I would not expect that to be a key source of investor returns going forward. As an investor I would focus more on the fundamental returns, mostly growth in earnings per share and dividends. Over time, I would expect that valuations revert to the mean.

Between 2010 and 2019, Church & Dwight earned $17.04/share in earnings in total. It distributed $6.03/share in dividends. This means that the company retained $11.01/share to reinvest in the business.

A 13% ROIC

According to Morningstar, the company has been able to achieve a return on invested capital of roughly 13% - 14%, which is pretty impressive. I do not want to venture any further into calculating more numbers however. At first look, it may seem that retaining $11.01/share resulted in increase in earnings from 85 cents to $2.44 and intrinsic value by $28.26. However, it may be hard to break down what percentage of growth was derived from past capital investments versus the investments from 2009 - 2019. Some long-term investments may not bear fruit for many years; others may have been misallocated.

Right now, Church & Dwight is expected to earn $2.82/share in 2020. The stock sells at $90.99/share for a forward P/E of 32.21. At the annual dividend rate of 96 cents/share, the dividend yield is at 1.05%. If earnings and dividends grow by 7%/year over the next decade, then they will double by 2030. The basic return would be at least 8%/year ( 1% from dividend yields and 7% from earnings and dividend growth). There are various scenarios going on of course, one where P/E ratios remain elevated and another where they shrink. The speculative return is hard to estimate, which is why I doubt it matters too much, unless you plan to invest for less than 5 years. If Church & Dwight doubles earnings in a decade, but the P/E ratio shrinks, the share price may not deliver much in terms of returns. This has happened before and won't surprise me from happening again in the future.

Under this scenario, the stock would still sell around $90/share, but would be earning $5.60/share and have a P/E of 16. The stock would be paying a dividend of $1.92/share and yield 2.10%. If you hold for several decades, and the business is durable enough to continue compounding wealth and income, that valuation shrinkage won't matter. This is why Buffett states that you want to invest in quality businesses, and let the power of compounding do the heavy lifting for you.

I do want to emphasize focus on quality companies that have a strong brand, strong moat, repetitive purchases, strong competitive positions, which can also grow profits over time. We want a durable and predictable business model, with a slower pace of industry change.

The Lessons Learned

Today, we learned a few important lessons.

We learned that when valuing companies, we need not look at P/E ratio in isolation. We need to take into consideration growth and stability of the earnings.

We learned the factors that drive future investment returns, notably initial dividend yield, earnings growth and changes in valuations. We need to focus on fundamental return, because the speculative return based on changes in valuations cannot be relied upon, as it reverts to the mean.

If management is able to reinvest earnings at a high rate of return in the business, they should do so. But for excess cashflows, they should distribute it to shareholders. For most of the dividend growth stocks we have covered extensively over the past decade and a half, managements have managed to balance the long-term needs of the business and its earnings growth with the ability to distribute a growing stream of dividends. But those rising earnings and rising dividends, reinvested over time, really turbocharge returns for investors.

The really important lesson is to focus on quality, even if it looks optically more expensive. If you are a long-term investor, a quality company is more likely to deliver solid returns over time than a statistically cheap, but poor one.

Relevant Articles: