After big market movements, we are eager to look for explanations, fundamental reasons why a stock or stocks collectively moved on that day, but the reality is that a great deal of the price movement on a day-to-day basis has nothing to do with earnings, cash flows or risk. On August 31, this reality was brought home by two events, neither with a strong connection to fundamentals, that represented the news of the day and contributed to price movements. The first was that two of the highest profile stocks in the market, Apple and Tesla, had stock splits that day (August 31), though the market had been trading on the expectation of these stock splits, for weeks leading into the day. On the same day, the Dow 30, a hopelessly flawed, but still among the most followed indices in the market, also announced a major reshuffling, replacing Exxon Mobil, Pfizer and Raytheon, three of its components, with Honeywell, Amgen and Salesforce. That gave rise to a wave of speculation about whether these new entrants would be helped or hurt by their inclusion in the index. While it is easy to dismiss stock splits and index inclusions as non-events, that dismissal is contradicted by market behavior, which, rational or not, seems to view them as consequential.

Value, Price and the Gap

I have long argued that value and price, while used interchangeably by many, are different concepts, driven by different forces, and lead to different numbers.

If you are an investor, no matter what your philosophy, this picture should not surprise you, since every philosophy is built around beliefs about the value and price processes.

- A value-based investor, for instance, believes that value and price can diverge, often by large amounts and for long periods, but that the price will eventually converge on value, delivering profits to those with the patience to hold on to the investment.

- A trader, in contrast, has little interest in value and plays the pricing game, gauging momentum and mood shifts to make money, and using liquidity or the lack of it to magnify these gains.

- An efficient marketer may agree that the price and value processes can diverge, creating gaps, but also believes that investors are incapable of finding and taking advantage of the gaps.

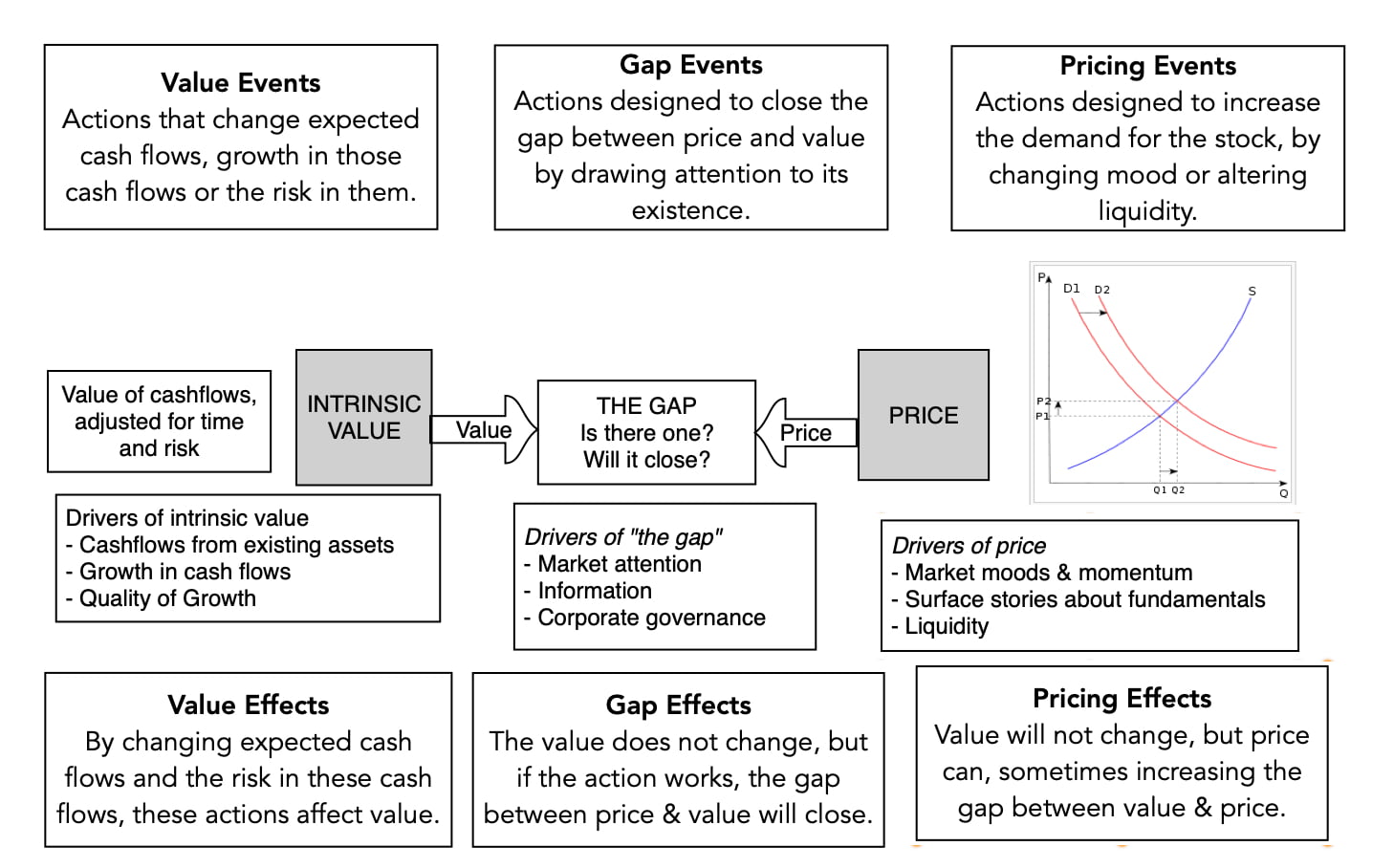

When an event occurs, whether precipitated by the company or an outside force, it can play out in one of three ways. A value event changes cash flows, alters expected growth and/or impacts the uncertainty/risk in these cash flows, and by doing so, change a company’s value. A gap event does not change value, but is designed to get markets to notice mistakes that cause price to diverge from value, and to correct those mistakes, closing the gap. A pricing event is one designed to either alter mood and momentum or to change the liquidity characteristics of a company, causing price to change, even if that price change widens the gap with value. In the graph below, I have expanded the value and price distinction to include these events and the expected effects:

Without examples, these are abstractions, but before I cite examples for each, I want to emphasize that there are very few events that have only one effect, and that most have a dominant effect (on value, price or the gap) with secondary effects on the others.

- Mostly value events: When a manufacturing company adds to its production capacity or a retailer opens new stores, the effects will almost entirely be on value. Since these actions are generally in the normal course of operations for these firms, they are unlikely to attract new market attention (which you need for gap events) or change market mood and momentum. Higher profile actions, though, almost always have spillover effects, and here are two examples. When Walmart recently announced its intent to partner with Microsoft to buy TikTok, there is clearly a value impact that this action will have, costing tens of billions in current cash flows, while promising to deliver higher growth and cash flows in the future. At the same time, though, this action, by attracting tech investors to buy Walmart, may alter momentum and have a secondary impact on pricing. When a California court ruled against ride sharing companies a few weeks ago, on the issue of drivers being employees rather than independent contractors, that decision had consequences for cost structure and value for Uber and Lyft, but it may have induced some investors to look at the gap between price and value at these companies.

- Mostly gap events: Gap events can be initiated either by the companies that are being mispriced (or at least perceive themselves to be mispriced) or by investors with the same perception. In academic finance, these events are termed signals, and while there is no guarantee that they will work, the motivation is to try to close the perceived gap between price and value. The cleanest example that I can offer for a gap event is a spin off or a split up, where a multi business company spins off one or more of its businesses or splits itself up, with no consequential changes in how it is run as a company, but with two objectives. One is that the action will expose the disconnect between the underlying fundamentals and the pricing, by providing more transparency on cash flows, growth and risk of individual businesses. The other is that the action will draw investor attention to the company, and that the attention can lead to a repricing of the stock. Not all gap events originate with the company. When activist investors target a company either as a buy or a short sale, they are attempting to provide the catalysts for the pricing gap to close, though their end games may involve changing the way the company is run, thus affecting cash flows, risk and value.

- Mostly pricing events: With mostly pricing events, the end game is altering mood and momentum or changing the liquidity in the stock, and by doing so, affecting the pricing of a stock. An emerging market company that lists its shares on a more liquid, developed market exchange, for instance, has clearly not altered its fundamentals through that action, but may benefit from higher liquidity pushing up price. There can be spillover effects from increased information disclosure, perhaps helping to close gaps between price and value, and perhaps even greater access to capital, allowing for a value effect.

Finally, there are some events that can fall into any of the three buckets, depending upon who initiates the event and how the market views the initiator. Stock buybacks are perhaps the best example, since there are arguments you can make for buybacks to be value, gap or pricing events.

- If companies buy back stock, using borrowed money, the primary intent may be to change value by altering the financing mix and the overall cost of capital for the companies.

- In contrast, if companies buy back stock, but only if they perceive their shares to be under valued, the buyback becomes a gap event, focused on moving prices up to intrinsic value.

- Finally, if companies buy back stock to feed pricing momentum or to provide a floor to the price, buybacks are primarily pricing events. The question for today then becomes where stock splits and index inclusions fall in this spectrum of value, gap and pricing events.

There is one final point that needs to be made about all these events. With each event, there are two dates of note. The first is the announcement date, when the market learns about the event, albeit it with some leakage to insiders ahead of the date. The second is the action date, when the event actually happens. Almost every effect that I described in this section should happen on or around the announcement date, and action dates are largely ceremonial. Put simply, if you believe that an acquisition, a spin off or a developed market listing is going to have an effect on price, the time to take investment action is at the time that it is announced, not when it happens.

Stock Splits

A stock split is a change in share count, without altering ownership shares. If you are an Apple stockholder, for instance, after Apple’s four for one stock split on August 31, you would own four times as many shares as you did on August 30, but so would everyone else in the company.

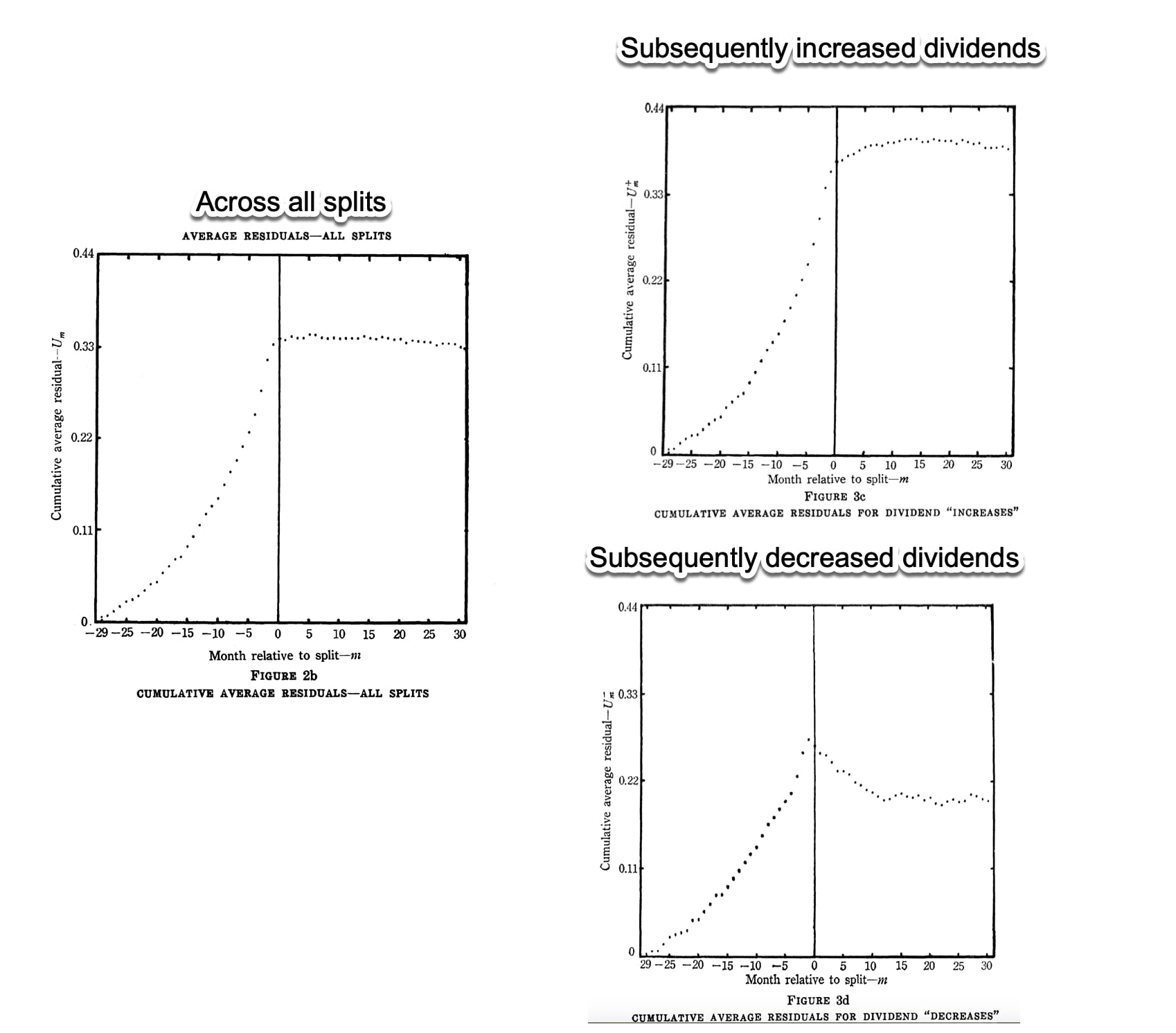

The Evidence: In one of the earliest empirical studies in academic finance, Fama, Fisher, Jensen and Roll looked at the effects on stock splits on stock prices in 1969 and found (not surprisingly) that, on average, they happened after big stock price run-ups and that the splits themselves create no additional run-up, at least in the aggregate. However, when the sample was broken down into companies that subsequently increased and decreased dividends, they found that stock prices rose after splits for the former and dropped for the latter.

In the decades since, there have been dozens of studies and while they generally find that split announcements are accompanied by small stock price increases, they disagree on the reasons. Some argue that it is because of post-split changes in liquidity, some posit that it is because splits operate as signals and some claim that they change value.

Value Effect: I pride myself on being creative in coming up with value effects for almost any corporate action, but I must confess that I am floored with stock splits. It is a purely cosmetic action, and the analogy that I would offer is that a pizza, sliced into six pieces, will not taste better and nor will there be more of it, if it is sliced into twelve pieces. Neither Tesla nor Apple become more valuable companies, because of their stock splits, because nothing fundamental has changed in either company, as a consequence of the split. In short, if you thought Apple was overvalued on August 30, trading at $500/share, you would still find it overvalued trading at $125/share, after a four for one stock split, since both price and value will be a fourth of what they were the prior day.

Gap Effect: There is an argument to be made that stock splits can operate as gap events, especially if a company is lightly followed and little attention is being paid to it, leading it to be under valued. The split, while just cosmetic, can bring the company (at least briefly) into the news and that attention may be sufficient to causing the gap to close, by pushing the price towards value (which remains unchanged). This argument does not hold for Apple, the most highly valued company in the world, and Tesla, a company that clearly has never had a problem with attention seeking, but it could be used by a company like Marten Transport, which announced a 3 for 2 split on July 17, 2020, after seeing its stock price stagnate for a three year period.

Pricing: There are two components to a pricing argument for stock splits. The first is that stock splits, by altering price per share, can affect liquidity, which can change the price. Ironically, a stronger case can be made for this with reverse stock splits, where as a stock falls to low levels, say less than a dollar, folding in five or ten shares into a single share can reduce transactions costs. With high priced stocks, the argument that stock splits reduce transactions costs and increase liquidity had more resonance in the past when trading shares in less than round lots often cost substantially more than in odd numbers. In addition, an argument can be made that when share prices reach really high levels, some investors will be shut out of the stock, because they cannot afford to buy any shares in it, round lot or not. Here, a stock split, by bringing the price down to more affordable levels expands its investor base, and by doing so, its stock price. The second argument for stock splits being pricing events is that they feed momentum that is already prevalent in the stock, perhaps because of the perception that lower priced shares (even if there are more of them out there) just seem cheaper to investors. In effect, those investors (like me) who bought Apple at $75/share in 2017 and have seen it go up to $500, and are troubled by how much it has gone up in a short time period, will feel more comfortable when the stock price settles back in at around $125 after the stock split, because we compare this price (perhaps irrationally) to $75/share instead of $18.75/share. With Tesla and Apple, the fact that these splits are coming after a unprecedented run-up in both stocks suggests that the primary reason for the splits is pricing, and that it more momentum-feeding than liquidity-building. You will be able to test the latter, by tracking trading volume and bid-ask spreads on both stocks in the coming weeks, since a liquidity story should show up in higher trading volume and lower spreads (as a percent of the stock price).

Index Inclusion/Exclusion

We use stock market indices to track market movements, but we also attribute qualities to companies, based upon the indices that they are part off. Thus, a company that is part of the S&P 500 is considered to be safer and more secure, and with good reason, since market capitalization is one of the key factors that determine whether a company is part of the index. It is not the only reason, though, since based upon its market cap, Tesla should clearly be in the index, but it is not, because its cumulated profits over four consecutive quarters have never been positive, a requirement for index listing. In recent decades, another phenomenon has fed into the index game, and that is the growth in index funds and ETFS, tailored to mirror indices, often by buying shares in companies that are part of the index. When a company is added to an index, these passive investors will then buy its shares, altering both its stockholder base and the demand for its shares.

The Evidence: Not surprisingly, the evidence on index inclusion has been focused on the S&P 500, with studies examining how stock prices are impacted by a company’s inclusion in or exclusion from the index. While there are dozens of papers, the findings can be broadly summarized as follows:

- Positive or negative: The consensus view across studies is that a company that is added to the S&P 500 sees its stock price increase modestly, and that the increase is permanent, and that companies that are removed from the index see small drops in stock prices that persist. There are two caveats. The first is that this increase may be more a consequence of the circumstances that led to the the company being added on to the index than the index addition. This paper, for instance, looked at a matched sample, where companies added to the index were paired with companies with similar characteristics (high momentum, rising earnings etc.) that were not added to the index and concluded that there was no index addition effect. The second is that there seems to be some evidence that the index effect has become smaller over time, rather than larger, even as passive investing has become a larger part of the index.

- Volatility and variance: There is some evidence that a stocks that get added to the index see increased volatility, as institutions become bigger players, and move more with the index, for the obvious reason that they are now part of it.

Value Effect: As with stock splits, it is difficult to make an argument that index inclusion or exclusion changes value, but there is a possible, albeit unlikely, path. When a company becomes part of a widely followed and tracked index like the S&P 500, its investor base will change to become more institutional and more passive. You can argue that these investors bring very different views on risk and preferences investing, capital structure and cash return than investors in the rest of the market. For instance, this study documents that companies that become part of the S&P 500 tend to behave more like their peer group on dividends and buybacks and become less profitable, after the index inclusion than before the inclusion, and these changes can affect value adversely.

Gap Effect: As far as I know, there is no index that looks at how much a company is under or over valued in making a judgment on whether to include it. That said, though, companies that get added on to the index tend to be companies whose stock prices have done better in the period prior to that add on, than the companies removed from it were doing prior to their removal. For some contrarians, the act of being included in an index may therefore be a signal that the stock price has outrun value.

Pricing Effect: The pricing argument for index inclusion is that it can increase the investor base for a company, by drawing in investors who invest only in that index (like index funds) or primarily in the index (like many large active institutional investors), and that increase should play out in a jump in stock prices on the stock. The effect, though, will vary depending upon the company in question and the index on which it is listed. The Dow 30 may be widely followed index, but it is not an index fund favorite or even one that institutional investors use to track their returns. Consequently, I don’t think that Honeywell, Salesforce and Amgen are going to be helped by being added to that index or that Exxon Mobil, Pfizer and Raytheon will be hurt by their exclusion from it. In contrast, when ServiceNow was added to the S&P 500, its stock price climbed 4%, reflecting both the company’s status (low profile, not widely followed) and the S&P 500’s standing as an index. I know that many Tesla bulls are awaiting its inclusion in the S&P 500, and with the full recognition that I will be wrong in hindsight, there is nothing that leads me to be believe that it will be a game changer for the company. In fact, you could argue that this company’s rise in market capitalization has come from individual investors with strong views on the company, and that the investors that may be drawn to the company post-index-inclusion may not be in sync with the company’s business practices.

Why should you care?

At this stage, you may be wondering what all of this means for you, especially if your focus is on whether to buy, sell or hold Apple or Tesla, and the answer is that it depends on your philosophy.

- If you are an investor, nothing that happened on August 31 should alter your views on the company. In other words, if you believed that Tesla and Apple were (under) over valued on August 30, 2020, you will continue to do so on August 31, notwithstanding the stock splits and the chatter of Tesla becoming part of the S&P 500.

- If you believe that one or both of these stocks is under or over valued, and you are hoping that the stock splits will close the gap, I am afraid that you are disappointed. These are among the most widely followed stocks in the world and stock splits are not going to draw new attention or cause neglected details to come to the surface.

- However, if you are a trader and you play the momentum game, this is your moment of maximum pain and gain. It is conceivable, and perhaps even likely, that the split will keep the momentum going for the near term, and that you can take advantage by buying today and holding for a period. The problem with momentum is that it is fickle and for those who bought the stock expecting the stock split to be their big payday, if the results fall short of expectations, there will be disappointment. If it sounds like I am playing both sides when I say this, I am, and that is one reason I stay on the sidelines as a trader. I am not good at it.

At the risk of sounding cynical, much of the commentary (including mine) that you read or hear on why stocks move is more post-mortem than analysis, an attempt to provide a rational veneer to a process where human beings move prices, sometimes for good reasons, and sometimes not.

YouTube Video