As COVID-19 continues to create economic uncertainty around the world, will more progressive climate policies help or hurt state economies? An embargoed report from WRI’s U.S. climate team says the former.

Q2 2020 hedge fund letters, conferences and more

According to the report, 41 states (such as Maryland, Georgia, Alaska and Indiana) have reduced their carbon emissions while growing their economies in recent years, debunking the myth that growth can only occur by compromising on the environment. The paper has a ranking of states based on how much they curbed emissions while they grew economically.

America's New Climate Economy: A Comprehensive Guide To The Economic Benefits Of Climate Policy In The United States

Executive Summary

Highlights

- The COVID-19 crisis emerged at a time when the U.S. low-carbon transition was experiencing significant momentum. Low-carbon technologies have become more affordable compared to fossil fuels, and U.S. clean energy investment and deployment have reached new heights.

- The impact of COVID-19 on the low-carbon transition has yet to be fully determined and will depend on how the federal government responds.

- This paper draws on the latest economic and policy research, which demonstrates that strong climate action and investments in low-carbon infrastructure can be effective ways to stimulate jobs and investment in the wake of the COVID-19 pandemic and secure the economy’s long-term success.

- In contrast, delaying action on climate change will further expose the United States to costly damages from climate impacts, air pollution, and other public health crises.

- The United States can improve its manufacturing competitiveness by building a domestic market for low-carbon technologies and tapping into foreign markets. Moreover, climate action will help revitalize rural communities by diversifying their economies and providing affordable clean energy.

- The United States can ensure that climate policies are fair and equitable by supporting fossil fuel workers and communities, providing quality jobs, and ensuring the benefits are shared by all.

Low-Carbon Technologies: Progress Towards America’s New Climate Economy

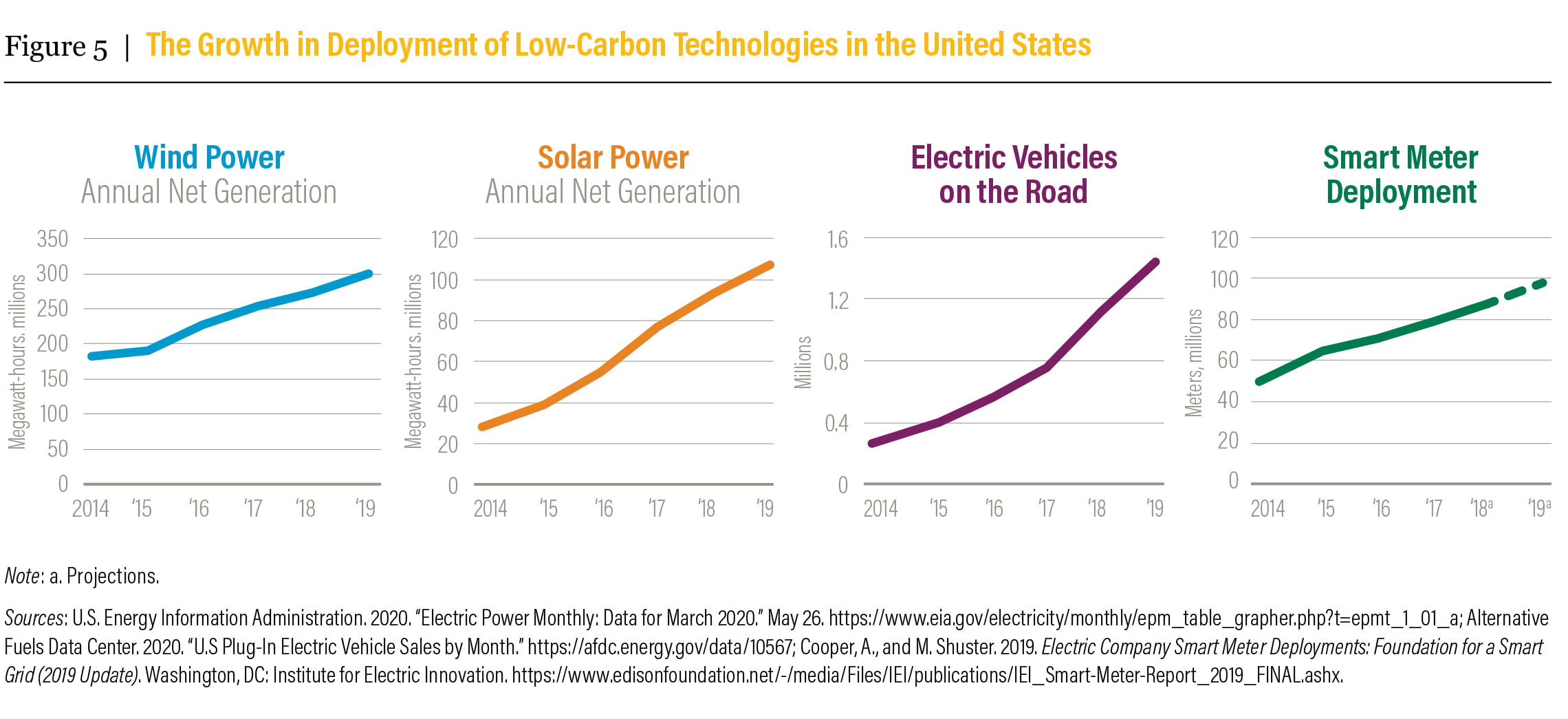

In recent years the United States has been growing its economy while reducing emissions. Although the COVID-19 pandemic is likely to cause a temporary decrease in U.S. emissions, an economic downturn is not the right kind of progress on climate change. The United States must work to combine emissions reductions with economic well-being, including GDP, income, and economic equality. While more needs to be done, the evidence shows that this is possible. From 2005 to 2018, U.S. real gross domestic product (GDP) increased 25 percent1 while energy-related carbon dioxide (CO2) emissions fell 12 percent.2 This is due to a combination of technological and policy factors, including the rapid deployment of renewable energy technologies, a shift from coal to gas in the power sector, and progress in vehicle emissions standards. Forty-one states and the District of Columbia have reduced their energy-related CO2 emissions while increasing real economic growth between 2005 and 2017. This includes states in all major geographical regions. The states that are taking action on climate change as part of the U.S. Climate Alliance have grown their GDP per capita twice as fast and have reduced their emissions per capita faster than the rest of the country.3

Climate leadership from U.S. states, local governments, and businesses is laying a strong foundation, but it needs to be augmented with federal policies to achieve deeper long-term emissions reductions. U.S. states, cities, and counties that are committed to climate action in line with the Paris Agreement now represent almost 70 percent of U.S. GDP and population and more than half of U.S. emissions.4 State and local climate leaders have implemented many impressive policies, including carbon pricing, renewable portfolio standards, energy efficiency resource standards, appliance efficiency standards, commitments to 100 percent clean electricity, and zero-emissions vehicle mandates. However, the administration of President Donald Trump is dismantling many existing federal policies, which makes it difficult for the country to truly reach a low-carbon economy and costs American consumers money. The rollback of vehicle fuel efficiency standards alone is expected to cost American drivers more than US$200 billion over the next 15 years.

Low-carbon technologies are becoming more efficient and affordable for households and businesses. In the past decade, the costs of solar panels, wind turbines, LED bulbs, and lithium-ion batteries have fallen dramatically while performance has improved.6 As low-carbon technologies have matured, they have become increasingly competitive with fossil fuel technologies, even without subsidies. Building new clean energy portfolios for power generation is now cheaper than keeping most existing coal plants in operation and is cheaper than building and operating most proposed gas-fired plants.7,8 This has changed the calculus of many utilities. For example, PacifiCorp has proposed a plan to retire four coal units in Wyoming and replace them with a portfolio of wind, solar, and storage technologies, a move it says will save customers $248 million over the next 20 years.9 Significant room exists to further bring down the costs of various low-carbon technologies. Electric cars and sport utility vehicles are already cheaper to operate than gasoline or diesel vehicles, and they are expected to reach purchase price parity during the mid-2020s.10,11,12 Yet at the same time, many low-carbon technologies remain out of reach for low-income households, highlighting the need for an equitable transition to a low-carbon future.

Low-carbon investment is growing in the United States but needs to scale up significantly for the country to meet its climate goals. Addressing climate change will involve a massive shift of financial resources from carbon-intensive production and consumption to less-polluting, low-carbon alternatives. This shift has already begun. Banks and investors are increasingly using climate finance instruments like green bonds and are divesting from fossil fuels. BlackRock, the world’s largest asset management firm, has committed to making sustainability and climate risks central to its investment strategy, signaling a turning point for the investment community. However, the need to accelerate investment in low-carbon technologies remains more urgent than ever before. Despite U.S. clean energy investment reaching a new high of $78.3 billion in 2019,13 the United States still does not invest as much as China in renewable energy or electric transportation, and it has yet to commit significant resources to reducing emissions and increasing carbon sequestration in the heavy-duty transport, industrial, and land sectors. Meanwhile, COVID-19 is making it more difficult for clean energy projects to find financing. Without federal support - for example, extending federal tax credit deadlines for renewable project - promising projects could fall apart.

The Economic Case for a New Climate Economy

In 2019, about 3.6 million Americans had clean energy jobs, and although many are threatened by the COVID-19 crisis, the sector is still set up for promising growth. In 2019 there were about 2.4 million U.S. jobs in energy efficiency, 266,000 in electric and alternative fuel vehicles, 248,000 in solar energy, 114,000 in wind energy, 108,000 in biofuels, and 66,000 in battery storage.14 These jobs are well distributed all over the country and have been growing at a faster pace than overall employment. One study has indicated that clean energy and low-carbon jobs offer higher wages than the national average, and many are available to workers without college degrees, though there are important concerns about the lack of benefits like health care and lack of contract security.15 Although it is too soon to tell the full impacts of COVID-19 on the economy, one study estimated that almost 600,000 clean energy workers lost their jobs in March and April 2020.16 There are initial signs, though, that the renewable energy industry is weathering the crisis far better than fossil fuels. If this is true, and renewables receive appropriate government support, they could overcome the short-term shock and be in a better position in the future.17

With high unemployment, investing in clean energy and other low-carbon sectors as part of the economic recovery from the COVID-19 pandemic can be an effective way to create jobs in the near term. Economic research has found that whereas $1 million spent on renewable energy or energy efficiency in the United States generates about 7–8 full-time equivalent jobs in the short to medium-term, $1 million spent on fossil fuels generates about 2–3 jobs.18 In addition, investments in transit, pedestrian, and cycling projects have bigger employment impacts than investments in roads. For example, as part of the American Recovery and Reinvestment Act, each dollar spent on public transit projects created 70 percent more job hours than a dollar spent on highways.19 Increasing plug-in electric vehicles (EVs) to 27 percent of U.S. vehicles on the roads in 2035 would generate approximately 52,000 additional net jobs per year and increase GDP by $6.6 billion per year on average from 2015 to 2040.20

Strong climate action is also consistent with longterm economic growth and a healthy job market. Many energy system and economic models find that the economic impacts of climate action will be minimal compared to the economy as a whole. These models find that with strong climate action, U.S. GDP will be between 0.7 percent lower and 0.6 percent higher compared to the baseline in 2030, and employment will be between 0.25 percent lower and 0.6 percent higher compared to the baseline in 2030. These models likely underestimate the benefits of climate action because they do not include the air quality benefits of climate action, the risks of economic damages without action, and the potential benefits of disruptive change. While these models were developed prior to the COVID-19 crisis, early research on the economic impacts of new U.S. stimulus spending estimates that large public investments of $320 billion per year in clean energy and agriculture programs could create 4.5 million gross jobs every year for 10 years. Likewise, $260 billion per year for upgrading infrastructure more broadly could create an additional 4.6 million gross jobs every year for 10 years. These investments would put the United States on track to reduce emissions in line with the Paris Agreement.