Logos LP’s monthly commentary for the month of July 2020, titled, “All These Worries,” discussing the recovery’s shape.

Q2 2020 hedge fund letters, conferences and more

Stocks rose Friday as news about a potential coronavirus treatment increased hope for an economic recovery following the outbreak. Tech stocks also continued their hot streak.

Gilead Sciences said its coronavirus treatment candidate, Remdesivir, showed an improvement in clinical recovery and a 62% reduction in the risk of mortality compared with standard care. The news sent Gilead shares up more than 2%. BioNTech’s CEO also told The Wall Street Journal the company’s coronavirus vaccine candidate could be ready for approval by December.

Shares of companies that would benefit from the economy reopening outperformed, especially the Russel 2000.

Our Take

In the short term, several of our proprietary technical indicators suggest that the market has become over-extended (especially sentiment in the NASDAQ) and thus we would not be surprised if markets pulled back as earnings season kicks off next week. However, if history is any guide, we do think that any selloff or pullback would likely be an opportunity to increase equity exposure.

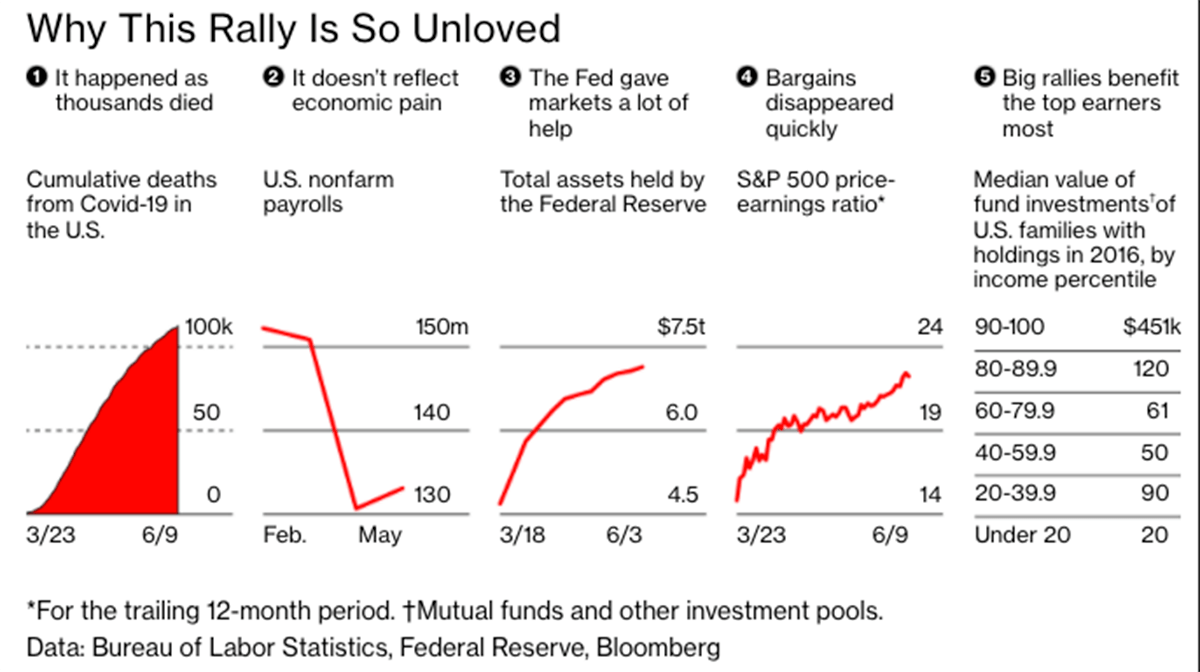

Looking at the second half of 2020, we won’t regurgitate the popular suggestions that the market has run too far, too fast, or that too many people own too few of the same “darling” technology stocks which COVID-19 has exposed as defensive investments/the new utilities (more on this below). These points are becoming so frequently argued that they could be considered to be the “consensus” view.

The same can be said for all the gloom and doom reasons which were presented in March and continue to be presented as arguments in favor of why one should be underweight equities or out of the market altogether. There are plenty of things to worry about, but these worries may be priced in as it should be stressed that in general, investors, large and small, are still in a high state of anxiety significantly underweight equities as sentiment levels remain at or near historic lows.

Alternatively, the more interesting story in our opinion is that interest rates are incredibly low and likely to remain so for a very long time in our low productivity/low growth world. This environment creates challenges for the trillions of dollars, institutional and otherwise, that have to be invested for one reason or another.

As such, if the economy continues to recover, COVID-19 cases and deaths trend in the right direction, and we get more positive vaccine/treatment news, the market is likely to continue its hot streak as cash comes off the sidelines and large institutions attempt to reach their historical median equity exposure.

Despite such predictions, as we hit the midpoint of 2020, we can notice that the cost of bad market timing decisions this year has been annihilation. As Vildana Hajric for Bloomberg so eloquently reminds us:

"But for all the dizzying turbulence, it’s worth noting that the S&P 500 is nearly flat for anyone who sat tight and held through the chaos. Mistakes stand out in an environment like that -- the back-breaking costs of even a few wrong moves in a market as turbulent as this one. Maybe volatility is the time for active managers to shine, but the downside of getting it wrong has rarely been greater.

One stark statistic highlighting the risk focuses on the penalty an investor incurs by sitting out the biggest single-day gains. Without the best five, for instance, a tepid 2020 becomes a horrendous one: a loss of 30%."

Another gem from Aswath Damodaran, an expert on valuation at New York University’s Stern School of Business:

"The people who hate the rally are the people who are market gurus, because it makes it seem like their expertise is useless. And guess what? It is useless,” says Aswath Damodaran, an expert on valuation at New York University’s Stern School of Business. “Those people exist to make soothsayers look good.”

Such statistics remind us of the danger of trying to call the market’s peak, something that investors are feeling tempted to do again now with the S&P 500, DOW and NASDAQ fresh off significant rebounds, coronavirus infections rising and the worst earnings season in a decade about to kick off. Bearishness and general market timing as a strategy has a cost and 2020 is no exception to such a rule as over the long run stocks tend to go up.

In a recent survey conducted by Citigroup, more than two-thirds of investors see a 20% decline in the market as more likely than a gain of a similar amount. Is the consensus view really destined to get it right as the second half of 2020 begins? Or will “staying the course” again deliver the best investment outcomes?

We have launched an exclusive daily newsletter including actionable daily insights for DIY investors from Logos LP

- Each Digest Contains the Following:

- Key Market Technicals

- Logos LP Watchlist Technicals

- Macro News

- Logos LP Update

- Alerts

Membership will initially be limited to 1000 members. Please subscribe here.

Musings On The Recovery's Shape

When thinking about the real economy and the stock market of late - whether reading about them, observing them, or listening to friends and clients talk about their experiences - it becomes clear that there is still a lot of uncertainty and anxiety surrounding what the future holds.

Will the recovery be a V, an L, a W-shaped or perhaps some other letter? Will certain industries be forever impaired or worse, collapse? What will all of these newly unemployed people do if their old jobs never come back?

I read a few paragraphs on these topics in the Washington Post the other day. The author was skeptical of the V shaped narrative:

“United airlines announced plans to lay off more than one-third of its 95,000 workers. Brooks Brothers, which first opened for business in 1818, filed for bankruptcy. And Bed Bath and Beyond said it will close 200 stores.

Welcome to the recovery.

If there were still hopes of a “V-shaped” comeback from the novel coronavirus shutdown, this past week should have put an end to them. The pandemic shock, which economists once assumed would only be a temporary business interruption, appears instead to be settling into a traditional, self-perpetuating recession.”

One thing we can say with relative confidence as penned in the New York Times by David Leonhardt is that:

“the course of the virus itself will play the biggest role in the medium term. If scientific breakthroughs come quickly and the virus is largely defeated this year, there may not be many permanent changes to everyday life. On the other hand, if a vaccine remains out of reach for years, the long-term changes could be truly profound. Any industry that depends on close human contact would be at risk.

Large swaths of the cruise-ship and theme-park industries might go away. So could many movie theaters and minor-league baseball teams. The long-predicted demise of the traditional department store would finally come to pass. Thousands of restaurants would be wiped out (even if they would eventually be replaced by different restaurants).”

What is lost in much of the commentary about the recovery's shape/trajectory is that when the economy weakens, poor companies with flawed business models and/or products/services that consumers and businesses can live without and/or easily replicate, are always those that will suffer the most, if not die.

Downturns are opportunities to revisit inefficiencies and can be healthy as they are part of the “creative destruction” process that economist Joseph Schumpeter famously described, allowing more efficient and innovative companies to rise.

What is also lost in the commentary is that although we find ourselves in the middle of this process of creative destruction, the novel coronavirus shutdown induced recession did not begin the forces of change. It merely accelerated trends that had been blessed by the capital markets long before the pain began.

In a fascinating article in a recent issue of the Economist the author cites research that the risk-adjusted returns of a high-resilience portfolio of stocks (mostly technology companies offering highly differentiated products and services that consumers and businesses simply can’t live without) were roughly 25% higher than a low-resilience portfolio of stocks (mostly cyclical companies offering non-differentiated products and services that consumers and businesses can live without and/or easily replicate) during the same period this year.

“The authors of the above research extend their analysis back in time and come to the rather striking conclusion that the outperformance of less vulnerable firms predates the pandemic. They detect that returns began steadily diverging in 2014, before widening further in the second half of 2019, and then exploding early this year.

This does not imply that markets foresaw the pandemic. It is owed, in part, to a boom in the price of technology stocks. Yet it helps illustrate why much of the reallocation now under way is very likely to stick- because it represents a continuation of trends that were long blessed by capital markets.”

As such, there will likely be no turning back. No return to the pre-covid economy. Research has shown that roughly 42% of lay-offs linked to the pandemic are likely to prove permanent while options prices imply that over the next two years investors require a far higher expected return in order to accept exposure to vulnerable firms than more resilient ones.

As such firms, investors, workers and perhaps most of all, politicians will have hard choices to make of whether or not to keep struggling companies, jobs and skill sets afloat.

Each stakeholder above will need to rethink their operations, trim fat that was accumulated while the economy was growing and reallocate resources more nimbly and creatively towards skills, pursuits and innovation more suited to the future.

Politicians should be more honest with their citizens about the power of these structural economic changes as they try and strike a delicate balance between generous support (which can discourage workers and firms from seeking new jobs and opportunities in expanding sectors) vs. too little support for those workers and firms dislocated by these changes (which can cause greater inequality and thus even greater social unrest and a prolonged slump).

In this new paradigm, humility, flexibility and a growth mindset will separate those who thrive from those that merely survive.

“The future rewards those who press on. I don’t have time to feel sorry for myself. I don’t have time to complain. I’m going to press on.” -Barack Obama

Charts of the Month

Chart courtesy of Worldometer - Coronavirus

Logos LP June 2020 Performance

June 2020 Return: 11.78%

2020 YTD (June) Return: 44.54%

Trailing Twelve Month Return: 58.81%

Compound Annual Growth Rate (CAGR) since inception March 26, 2014: +21.34%

Thought of the Month

"“When I look back on all these worries, I remember the story of the old man who said on his deathbed that he had had a lot of trouble in his life, most of which had never happened.” – Winston Churchill

Articles and Ideas of Interest

- Are tech stocks the new utilities for investors? Tech stocks weren’t considered defensive investments in the past. But as the coronavirus crisis reinforces technology’s fundamental role in our lives, investors can find sources of risk reduction and growth potential in companies that have become digital utilities enabling global networks.

- Over the past 60 years, more spending on police hasn’t necessarily meant less crime. If we look at how spending has changed relative to crime in each year since 1960, comparing spending in 2018 dollars per person to crime rates, we see that there is no correlation between the two. More spending in a year hasn’t significantly correlated to less crime or to more crime. For violent crime, in fact, the correlation between changes in crime rates and spending per person in 2018 dollars is almost zero.

- A mathematician calculated how to keep fans safe at Yankee Stadium. Based on social distancing guidelines, only 11% of seats should be filled.

- We’ve reached peak wellness. Most of it is nonsense. In Silicon Valley, techies are swooning over tarot-card readers. In New York, you can hook up to a “detox” IV at a lounge. In the Midwest, the Neurocore Brain Performance Center markets brain training for everything from ADHD, anxiety, and depression to migraines, stress, autism-spectrum disorder, athletic performance, memory, and cognition. And online, companies like Goop promote “8 Crystals For Better Energy” and a detox-delivery meal kit, complete with “nutritional supplements, probiotics, detox and beauty tinctures, and beauty and detox teas.” Across the country, everyone is looking for a cure for what ails them, which has led to a booming billion-dollar industry—what I’ve come to call the Wellness Industrial Complex. The problem is that so much of what’s sold in the name of modern-day wellness has little to no evidence of working. Brad Stulberg for Outside magazine provides an excellent list of what actually works.

- 2020's top 15 market moments according to Business Insider, from COVID-19 crashes to huge rallies. At the start of 2020, the killing of Qassam Soleimani, and the Iranian-US tensions that followed, was the biggest story in town for markets. But COVID-19 soon began to spread across the world, causing markets to tank. It's been a rollercoaster ride ever since. From oil prices turning negative in April to famed investor Warren Buffett selling his airline stocks in May, here are the top 15 market events of 2020 so far.

- Active fund managers trail the S&P 500 for the ninth year in a row. After 10 years, 85 percent of large cap funds underperformed the S&P 500, and after 15 years, nearly 92 percent are trailing the index.

- We’re not likely to have a Covid-19 vaccine anytime soon. In the meantime, two scientists have developed an antibody-based shot that provides a similar level of protection. A growing number of doctors, including Anthony Fauci, think the approach is promising and readily scalable. So why do US officials and pharmaceutical companies keep refusing to mass-produce it? Emily Baumgaertner takes a look in the Los Angeles Times.

- A buy everything rally beckons in a world of yield curve control. Should yield curve control go global, it would cement markets’ perception of central banks as the buyers of last resort, boosting risk appetite, lowering volatility and intensifying a broader hunt for yield. While money managers caution that such an environment could fuel reckless investment already stoked by a flood of fiscal and monetary stimulus, they nonetheless see benefits rippling across credit, equities, gold and emerging markets.

- Like a ton of bricks - Is investors’ love affair with commercial property ending? Covid-19 has upended the impression of solidity. Most immediately, it has severely impaired tenants’ ability to pay rent. It also raises questions about where shopping, work or leisure will happen once the crisis abates. Both are likely to prompt investors to become more discriminating. Some institutions may shift funds away from riskier properties; other investors, meanwhile will hunt for bargains, or seek to repurpose unfashionable stock. As it turns out, more and more people think we can work from home, and should continue to do so. For a nation long frustrated with offices, the coronavirus offers an excellent excuse to avoid them. According to McKinsey, 69% of people who now work from home are equally or more productive than they were at the office. 60% — three in five — say they would prefer to stay home — even after the pandemic is over. Guy Vardi digs into the future of work.

- Where did my ambition go? A drive to succeed has become a drive to just get by. Why workplace ambition is flickering out in this endless limbo. Maris Kreizman writes that the tectonic shift currently shaking our culture/society feels profound. In a time when the pandemic has caused so much uncertainty about the future of so many industries, professional ambition begins to feel like misplaced energy, as helpful to achieving success as chronic anxiety. This is fascinating in light of Robert Shiller’s recent suggestion that the psychological toll from the coronavirus pandemic could completely reshape our societies. He warns that the big risk is people start thinking the setback will last forever and it impacts their willingness to take risks. That mindset could turn into a self-fulfilling prophecy, dramatically hurt demand and push more businesses to the brink. “We don’t have to keep up with the Joneses anymore,” said Shiller. “That might create a different kind of culture that would last for years that you don’t have to show the latest fashions and drive a spanking new car. We just learn that you can relax. But that is bad for the economy.”

- The end of tourism? The pandemic has devastated global tourism, and many will say ‘good riddance’ to overcrowded cities and rubbish-strewn natural wonders. Christopher de Bellaigue asks if there is any way to reinvent an industry that does so much damage?

Missed a Post? Here's the Last 5:

- The Beauty of Discomfort

- Has the Stock Market Gone Mad

- Crystal Balls and Bottom Calling

- COVID-19 - It Will Pass

- Late-Capitalism and Gratitude

Our best wishes for a month filled with discovery and contentment,

Logos LP

Interdisciplinary Value Investing.

www.logoslp.com/