In 2008 banks were too big to fail! In 2020, stocks might be too big too fail! We discuss the financialization of the economy, how household wealth is impacted by financial engineering and low interest rates force people to invest. This all leads to stocks being hot and discussed by many, cheap brokers like Robinhood add to the party. Usually, it would be a huge warning sign for the stock market, but today it might be indicating that stocks are too big to fail.

Q1 2020 hedge fund letters, conferences and more

With stocks being $28 trillion of american wealth, or 23%, it is hard to imagine the FED letting the market crash due to repercussions on consumption and spending. Plus, the stimulus might keep the not so rich happy and avoid populism. It all depends how the current financial engineering situation will be managed.

How the FED and politicians react will have huge repercussions on your investing, how the stimulus is used and how it impacts the economic situation.

Too Big To Fail: STOCKS in 2020!

Transcript

Good day fellow investors. 2008-2009, first banks were too big to fail, then the problem, the debt problem was cured by adding more debt. And now who is now too big to fail? Those are the questions we're going to try to give an answer to by discussing the stock market, its warning signs, the economy, the warning signs, and there are plenty of them with the economy. But you must not focus just on the warning signs. You must also focus on the possible solutions, which is what we are going to end with to see how the Fed how the government's and what are their tools to solve the current issues. And that might give a perspective. Nobody knows what will the future look like? But it might give us a perspective on okay this is possible, this is possible, this is possible. How can I position myself that whatever happens I end up well? That's the key when it comes to investing and putting the current situation into a long term life investing cycle.

So let's start with stock market warning signs. I was reading the comments on the videos I made. Thank you for those. I always like to read those comments, but some how, over the last month or two months, there is a predominant amount of comments talking about speculating with stocks, where will this stock go? What will happen here? How can we buy now with something or buy or not? And that's a big warning sign. Let me just show you here. Do you think Berkshire is a good buy now? Are you buying? Is it a good time to buy this or that stock? And many, many comments like that. So here another comment value investing is that it's hard to do when everything is overvalued. I focus on sentiment and vaccine progress. Okay, even better than value investment, perhaps will one day have the sentiment and vaccine progress Intelligent Investor book, we'll see. Can you put subtitles in your videos? So this tells me, okay, the interest for stocks is global, not just, let's say in the US so there is plenty of money around the world and a lot of people are actually forced to invest in stocks, because interest rates are at zero and you don't get anything with your banks. So here there are a lot of comments focusing on just one thing, altman Z score on my nutrient analysis, instead of doing I'm seeing a lot of people focusing on one thing, one thing that they think they can comprehend, instead of doing the full analysis. Which means a lot of people are dabbling with stocks, but they don't understand what they are doing, because there is a lot of speculation. Would you rather read the income statement statement or the operating cash flows? It's always both, it's always 10 times that, you can just do one thing and then invest.

Then I'm way too optimistic on Disney park revenues because there will be a second virus wave. Can you analyse LIB with 7% dividend? How diversified is their clients base? We're talking new nutrient that sells fertilisers. Well, everybody who grows tomatoes uses them so that's how diversified their user base is. And then I dig a little bit deeper and then start up Robin Hood hit more than 10 million accounts over the last few years this is December for 2019. Then I look at okay what are the most popular stocks for cyclical speculative General Electric speculative, Disney, okay, half speculative at this point speculative speculative speculative, speculative speculative biggest companies they're okay due to size speculative speculative. So 10 million people speculating in stock. And this is a huge warning sign. Also in Europe we have this cheap broker and mostly traded Tesla Tesla speculative wire card fraud issues. So a lot of people speculating with the extra money they have in stocks. And also, I am really pleased with the success but also scared about it. Because at 2000 subscriber for an accounting professor, boring accounting Professor with a PhD on YouTube is crazy. Of course, I thank you for the subscribers. We do good charity work with the money we make on YouTube. But this is really insane. And the predominant thought in the past was when everybody's talking stocks, run away. But of course, we will see how will this end up. Is perhaps the stock market and all those millions that are investing in stocks, are they too big to fail? Let's look at the economy warning signs. And then let's put the stock market into a personal wealth perspective and see how important has the stock market become now.

Also on a valuation perspective, if we look historical valuations, whenever the price earnings ratio was above 20, don't take the 2009 crisis earnings were really hammered and then that's why the price earnings ratio spiked. But every time price earnings ratios were high returns weren't that good. If we put that into a doubt perspective, high price earnings ratio at the end of the century, 22 years of zero returns 1929 high price earnings ratio of 25 years of zero returns 1960 high 1965 High pricing earnings ratio of 17 years of zero returns inflation, then 1990s dot com bubble 12 years of zero returns. So if you would look at history, the valuations, the warning signs, the debt cycle that we are in, it's likely that over the long term, we'll see zero returns. And that would actually be a good thing for the economy and the world. We'll see in a moment, but then we have to ask, are we going to see negative returns in the past? It's easy to scare people. I show this and then I say, okay, 50% decline 80% decline, 50% decline. There's going to be a crash ahead, let's sell everything. But we have to also see the other perspective. The economy is where it is late part of the debt cycle, excess debt, 2008 they solve the situation by printing more money to buy financial assets. They can't lower interest rates anymore. Those have hit rock bottom. And they are now starting with direct stimulus helicopter money and money loses value because they are creating too much of it or more money less value. That's simple as that.

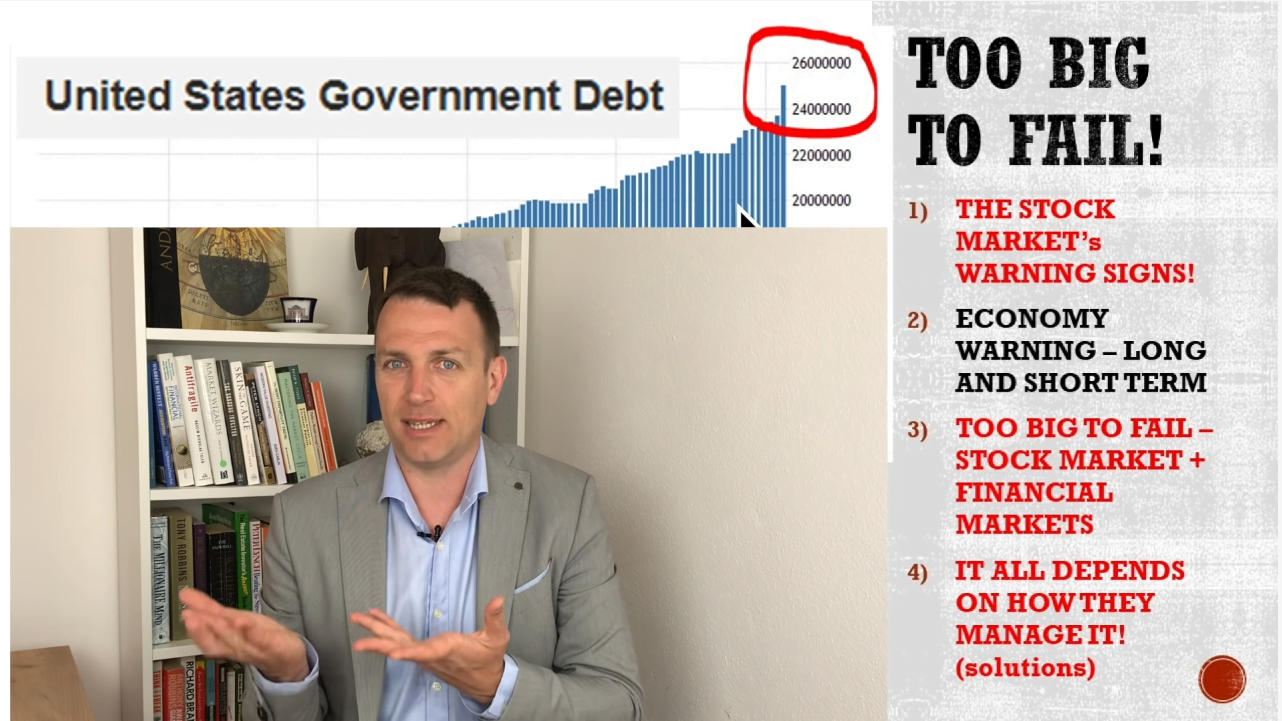

However, the issues are there globally, many entities have lower income, lower spending, there is China-U.S. fighting and there is also the large wealth gap that we'll discuss in a moment. Also, the unemployment rate, this is for April will be even worse in the United States and globally due to the current situation. We see how long it will take for this to recover and come back to a normal, to a stable percentage level. Also government debt, especially with the current stimulus is exploding has been exploding for the last 30-40 years and now it's really really going higher. So there are plenty of market warning signs economy warning signs. But on the other hand, we know what are the warning signs we didn't know we couldn't predict the current virus crisis. But the other warning signs have been there and are being managed. When it comes to long term investing, what will happen with your retirement, with everything? The question will be found in how the current situation will be managed by central banks and governments. That's what we have to focus on. If they manage it, well, then the economy level, the wealth level will remain well, and we'll be okay. Might be zero percent for 10-20 years, but it will stay stable. We are unlikely that we're going to see great depression situation because times are a little bit different.

Now, let's discuss this. Why our finances the markets are so important? The global bond market 40 years ago was just $10 trillion. Now it's a 100 trillion dollars. So that's a huge change and therefore extremely important, any changes here in this debt pile, any issues here will have repercussions, huge repercussions on the economy. So this debt has to be managed and we are seeing the Fed also buying corporate bonds now, same in Europe, etc. Because there is the issue. Then we're looking at the stock market, the global market capitalization 2019 was close to 90 trillion. So you have 100 trillion, 110 trillion in bonds, and almost a 100 trillion in stocks, mostly most the highest market capitalization is in the United States. And then this is very important. Why are stocks too big to fail? If we look at the components of GDP, this is the United States, personal consumption is 70%. Then business investment, then the government net exports make it 100%. So total GDP is 19 trillion of that 70% is personal consumption. Personal consumption depends on the income you have, and on the net wealth, which gives you confidence to spend. And let's look at this. This is how much households in the US held in stocks in 2009. It was $7 trillion. Now, 10 years later, we are at $28 trillion. So that's a 4x increase. If I compare that to the net wealth, the household wealth, it was $60 trillion in 2009, 7 trillion, that's 11-12% of the wealth, was in stocks. So okay, not that big. Now, the net Wealth is $118 trillion. And we have 28 trillion in stocks. So it went from 10% to 20%, of even more of your wealth. So it is a more and more significant part of your wealth, which also impacts your consumption.

This is the chart that shows how wealth went up two times from 60 billion to higher from 60 billion, 7 billion and the assets, stocks owned by people went up four times. So from 60 to 120, and from 7 to $28 trillion. So suddenly, stocks are a significant part of the household wealth, and we have seen how many people are investing. So are people owning stocks too big to fail? That's the question we have to ask ourselves and see how that is going to be managed. Real estate, also significant but growing in line with net wealth. So financial assets are the key here we are in a more and more financialized world, and you can print dollars, thus you can manage the situation. And how do you print dollars? Just look at the Fed's balance sheet. Prior to the Great Recession 2009. It was below a trillion dollars, boom, first printing of money, 2 trillion, then more and more stimulus, stimulus, stimulus, stimulus, stimulus. Then they said, Okay, let's stop. Let's see how what happens if we lower the stimulus. Armageddon happens and then stimulate, stimulate and now with the COVID crisis, boom, to $7 trillion dollars, they will expand because they need to keep this wealth at a high level. Because it impacts personal consumption. And therefore, it's all about how people are too big to fail. Same situation in Europe, huge stimulus, and then coverage crisis, even more stimulus. Of course, there is always the issue of the wealth gap. And the bottom 50 have really unfortunately the rock bottom 50% in the US have really little wealth. When you put it here we are at $6 trillion, which is a quarter of the top 1% has 4 times more than what has the bottom half, unfortunately. We'll see how will this also be managed because these guys have the corporate equities these guys have the assets, have the real estates, have most of the, let's say business wealth. Then from 99% down to 50%, these guys have most of the pension entitlements, the bonds, the stocks in pension funds, also here more real estate. So, by saving financial assets, you are saving the top 50% of the population. And with direct stimulus, you are trying to manage the happiness. This sounds ugly, but that's the true I cannot make a difference, the happiness of the bottom 50%. If you can manage their happiness without leaving it to prior to second world war situation, nationalism, etc, then this will be well managed. And this is the question, how will the stimulus help keep the spending the personal consumption in form of this wealth, making the rich unfortunately richer, but also keeping the poor poorer? And that's the question that will give us the solution to what is next.

So, we are here now. This place where we are is the consequence of the financial engineering that started 50 years ago since the dollar was defect from gold. But that's how things are, you can be angry, you can think what ever you want. There are many comments, there are many videos about crashes about the zombie governments, etc. But this is what it is. And we have to look at this in real perspective, see what can happen and then see how to adjust how to prepare for whatever, whatever can happen so that we are ready anyway even take advantage of it. Big companies are taking those stimulus loans, and they're trying to do the best of it. That's nature, that's capitalism, even if it is stimulus to the maximum. But that's where we are, we have to accept it and make rational decisions.

So let's compare this, many compare this to 1929 and 2008. Well, the New Deal. The difference between now and then is that they waited four years to for the New Deal. 2008 the reaction wasn't immediate, they let Bear Stearns go bankrupt and then we had the Emergency Economic Stabilisation Act passed in October for the bailouts for the house later came the printing. Now the reaction was immediate with huge global stimulus. And the question is okay, what's going to happen next? How is this going to be managed? And if the Fed is printing money, so if everybody's printing money, they're trying, they will try to stabilise this. I don't know whether they lose control or not. That also depends on what you are going to do. What we are going to do, are we going to stay focused, be confident because it's all a reflective process. If we are focused, if we are confident, if we trust what's going on, then it will be good. If we lose control, if we panic, then it will be disaster. That's also very important. It's a reflexive process. And that's also what the Fed and central banks are trying to manage.

Very interesting always from Ray Dalio, he also emphasises this a bit. How will we divide the pie? And how to make the pie bigger? Is the answer of the current stimulus packages and of the long term strategies. What are the solutions? Well, we can continue to stimulus as long as there is no hyperinflation. Why not give the people what they want, give them money, helicopter money, and test it. We'll never see the real interest rates were unthinkable 1015 years ago, now it's a normal, who knows maybe helicopter money will be a normal, the world in 10 years will be much different than it is now. 15 years ago, it was totally different than it is now. So we have to be ready for everything we have to expect. Also, those things that seemed crazy four years ago, 5, 10, 20 years ago. If they push inflation to let's say, 5% per year over the next decade that solves a big part of the debt problems, the difference between now and the past speed in reaction, communication, connectivity, globalisation, Cold War in 1970s, second world war, first world war just worse prior to that globally. So that is the situation now looks much, much better than the past and we'll see how they manage it.

I have two messages for to conclude this video, pretty simple. There is investing and there is speculating. If you invest, and you invest in a way, okay, whatever happens, the Fed does really well. The Fed doesn't do well. governments do really well. governments don't do really well. Whatever happens. I do well, and the process of investing is accumulating assets over time. Warren Buffett became the richest person in the world. In the 1970s, because he was accumulating assets, even if the times were terrible. That's the key of being an investor. What will go up 20-50% in the next six months? Nobody knows that speculating. But I see 95% of people doing just that, instead of accumulating assets and finding the best solution for them. Which leads me to, okay, it's about you. How does this recession, situation, stimulus fit you and what you're going to do with it? I'm personally looking to buy a house, take a fixed mortgage loan, those that have that are likely to be saved by the governments ECB, Fed printing money, easing that if there allow for more inflation, then the repayments of that will be easier, but you have to put it into a perspective, personnel perspective and then see how can you accumulate assets over time, which is the core of investing. Everything else is speculating and if you accumulate good assets, no matter whether it is good or bad over the next 10-20 years, you'll do well. If you like this thought please subscribe to this channel. I'm trying to give as much value as I can in each video. If you want to read more about what I do my research and everything, check my website. And please click like if you enjoyed this video, subscribe if you haven't clicked that notification bell and I'll see you in the next video.