A 15 minute summary of Berkshire‘s 2020 shareholder meeting and key topics. Warren Buffett tells you to never bet against America, how the current situation is just an interruption in the process of growth and how stocks, buying stocks, is always the best long term investing decisions. Warren Buffett uses historical examples to explain what kind of a situation are we currently in.

Q1 2020 hedge fund letters, conferences and more

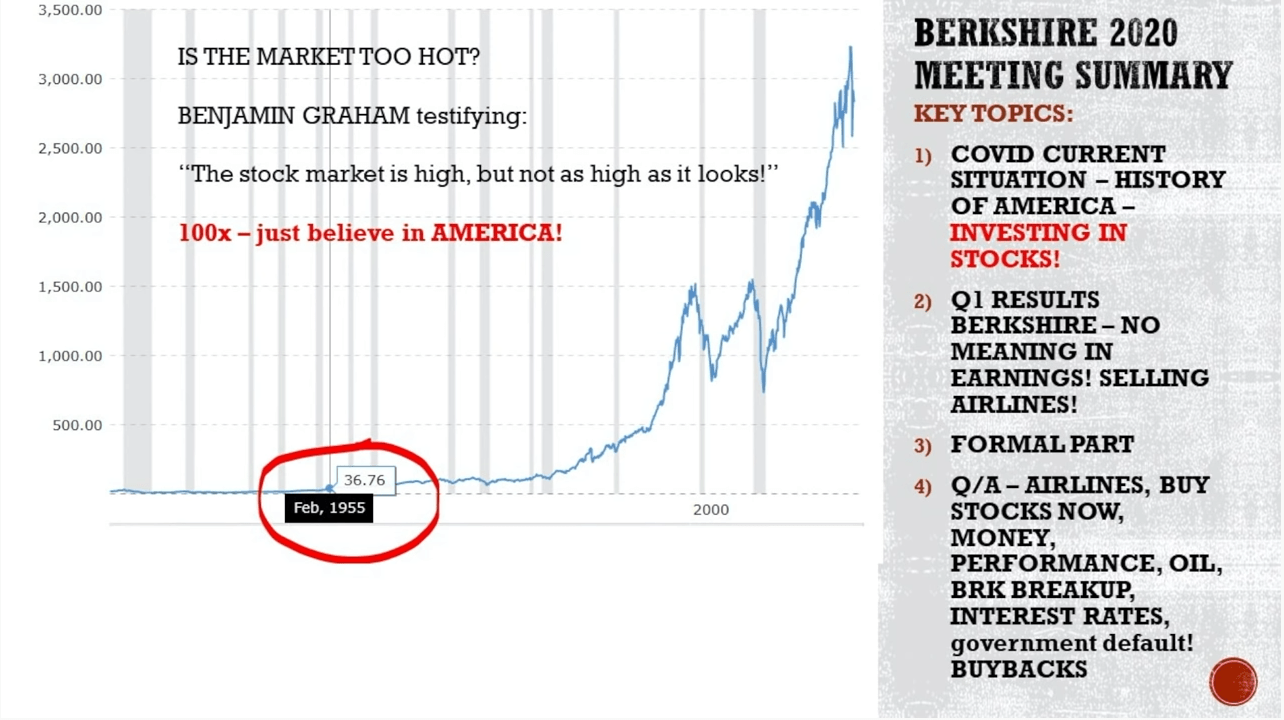

What is also important for valuations are interest rates. Low interest rates increase stock prices.

In the Q/A section Buffett answers many questions from why he sold all his airline stocks, interest rates, praising the FED for immediate action, buybacks, Berkshire and shares his eternal investing wisdom. Enjoy the Berkshire Shareholder Meeting 15 minute summary.

Warren Buffett: Berkshire Meeting 2020 - 15 Min Summary

Transcript

Good day fellow investors. Well here we are, the most expected value investing event of the year Warren Buffett's shareholder meeting this year, a little bit shorter online, but still always great topics to discuss, to analyse and to see how to apply them to our own investing long term strategy. If you're a long term investor, please click like, comment below share this video, we're going to dig into the topics now enjoy.

So online version of the Berkshire Hathaway shareholder meetings this week, and Becky Quick was asking the question, so it was much more efficient than it usually is. Warren Buffett answering the question directly efficiently and in four hours, he did much more than usually in even six hours. So let's go over the topics. The structure of the meeting was made in four parts. So his presentation his discussion about America, investing in America, not betting against them. America, touch on earnings selling aircrafts, his loss on aircrafts just a formal meeting the formal part of the meeting and then questions by Becky Quick that she got from the public and online.

So let's immediately start with his presentation. He created slides and he discussed okay how to invest in the current situation with the Coronavirus crisis. He called the crisis an interruption in growth, so just an interruption, and that over the long term economy will grow America will become a better and better country. And you have to believe in the economic future of the country and that he has best a lot of crisis from the Second World War, Cuban missile crisis, 9/11 2009, and the American magic will prevail. He used a lot of examples how the age of the United States is just 231 years, the combined age of Charlie Munger and himself 185. And just look at what happened in three normal human ages, from a population of 3.9 million in 1790, of which 0.6 million were slaves. So from that, to what happened today, what is America today the most powerful economy in the world in just 231 years,.

Then a lot of interesting slides with historical data from the wealth of the country discussing the Louisiana purchase, the return on the Louisiana Purchase, how big was the return? How big was the wealth created there? And then comparing to the coverage crisis, how 16 million males there were in 1861 and 6% of that group was killed in the civil war that lasted five years. That would be to today's equivalent of 4 million people dying, he compared the crisis with the flu in Omaha, the Spanish Flu 100 years ago, how that was deadlier than the current COVID crisis. So there will always be interruptions when it comes to the economy life. That's simply life, but you have to believe in the future. And you'll do well also to investing into economic growth.

Then talking more specific about stocks, he said from his birthday, the Dow Jones Average was 381 points, then it declined 48% to 198 points, then it went up to 240 points, and nobody was really expecting a great depression. But then it went down again to 41 points. So from 381 points to 198, 240, 41 points when Warren Buffett was born in the few years after he was was born. But again, people survived that invested. And even if it took more than 20 years to break, even if you bought stocks when Warren Buffett was was born, still, you could have done well, but simply investing through time and also taking care of those dividends that were coming. And something very peculiar 25 years later from the peak in 1929. commission was set up to investigate whether the market is too hot in 1955. And Benjamin Graham testified I think it was Congress testifying that the stock market is high, but not as high as it looks. And the rest is history since then. Since then $1 invested would have been 100 times that initial investment and that stocks. The stock market yes is high, but it might be not be as high as it looks, is what Warren Buffett is saying. And later he also discusses interest rates. And we'll touch on that and how that affects stock prices.

So his conclusion on his presentation is never ever bet against America. Because that's not the smart thing to do, especially in the long term, and the people are innovative, there will be interruptions, that's normal. But the long term strategy, the long term trend is pretty clear. And then on why invest in stocks, comparing stocks with equities, the 30 year Treasury, you're practically losing money. He explained how if you lend money to the government at 1.5, with 2% inflation, you're practically losing money. So stocks are a better long term investment than lending money to the government now, for example, as long as those are an investment, not speculation. So if you invest in an index like the S&P 500, you own a cross section of America and you can forget about it. The only problems can arise if you use leverage, if use psychology, if you have the wrong psychology, then you sell it the wrong time you panic. You listen to the news, you listen to the rational market giving you constantly lower a lower price, then you sell at the wrong moment in time. Instead of investing in businesses. When you buy a farm you buy to produce food, you don't focus on the price of the farm every day. And he said they will continue to buy businesses.

On earnings, the earnings currently are not important because A) we don't know the consequences of the current situation on future earnings so it's not really comparable. B) the 50 billion loss was an accounting loss, okay? Because they have to account for the Changes in the stock prices can change again in the next quarters. And then he discussed how 124 billion in cash is not really 40% of the stock market portfolio in cash, it's far less than that around 20%. When you calculate all the values of all the businesses in the Berkshire holding. So don't think that Buffett is sitting on that much cash, he doesn't think he's sitting on that much gas. And he said that if the deal comes off around 50-60 billion, he would take it. So let's say he sitting on 50-60 billion of available cash, not that more. And even if it all put together 124 billion, we are at 20% of the portfolio. He has discussed how Berkshire will always be a financial fortress. That's why they have so much cash on the balance sheet and he praised also Powell for the fast reaction with the fed the speed and determination they have showed. Whatever it takes mentality started by Mario Draghi in Europe, now copied by the Fed. And the on the consequences of the money printing. He says that what would be the consequences of doing nothing is the best question.

Now, he sold, he closed all his airline position. So he owned four of the biggest, largest American Airlines and he sold everything. They spent around 8 billion to own those top four stocks. They sold at a loss. And he says that he was clearly wrong about airlines. Airline business changed in a major way. And they had all to borrow 10 billion the time for them, even if big business is there to repay those 10 billions will be very long and very painful. And he doesn't know whether three years from now how many people will fly and that's not clear to him and there are too many planes and if it's just 80% of the current flying numbers. It's not enough to justify the investments in the new planes in the growth. And this will cost Berkshire money. But it's his mistake. And actually, if you think about it, since ever, he has been against airlines because there's no competitive advantage. And now he found himself unfortunately due to this situation right again, and lost money in airlines. But they closed everything close the position and took the loss. So very interesting how even Warren Buffett, the long term investor is selling when it simply doesn't show like a smart investment.

Now formal part just quickly discussing some proposals, denying the proposal of a mixed board, etc. So we can immediately go to the questions and then again on airlines. So explaining how it's not good than 80% of prior traffic. So he sold and the airlines will be really hurt. And this was something very interesting. He discussed how only big companies were somewhere where he could put his money into owning maximum 10%. So if you think at the market capitalization of Delta Airlines, he can own only 10% on 20-40 billion. That's the limitation he has with investing. So for Buffett to invest in something that companies should be at least 30-40 billion in market capitalization, which eliminates a lot of things where we as individual investors can look at.

Then there was a question, should we buy stocks now when he's sitting on so much cash, and then he reiterates himself, it's not a large cash position in case of worst case insurance scenario. He needs to have a lot of cash and it's about the psychology of investing versus speculation whether you should invest or not. If you're buying businesses, and you don't have to account for that money in the medium short term, then you have nothing to fear and he never felt financial fear. That's what made him a great investor. And if you invest now in stocks, it will work out well over the next 20-30 years. But don't ask him how it will work out over the next one year, two years, three years.

Then he also discussed money, how there is no shortage of money in the market. Like it has been the case in 2008 2009. Therefore, we are not seeing the convertible investments, eight of them that he did back then with the Bank of America, Goldman Sachs, etc. There was short period with panic in the markets in March, but when that froze, but the Fed acted promptly. And he has no idea what will happen next, but he says they borrowed Money and it's a good time to borrow money because of the very low interest rates. And if we look at the 30 year fixed rate mortgage average, which is something more peculiar for personal borrowing of money, the interest rate on that is very, very low.

On the question of performance, how Berkshire underperformed the s&p 500 over the last 5, 10 and 15 years. He says that on one hand, yes, size makes it difficult, and there is no guarantee about future performance. But he has 99% of his money in Berkshire. And then there are also advantages. For example, nobody can do what Berkshire can do in energy insurance. Nobody can shuffle the money depending on where it's most needed. Where is their highest return on capital, depending on the holding company that Berkshire has.

Then on oil, it doesn't work at $20 a barrel, production will be down. And there is a lot of oil in storage, and it will take some time to clear out. So we might see lower prices for longer. And therefore there is a risk of permanent loss of capital from oil companies to affecting even the banks that are lending to those oil companies and bad debt in energy loans, if that happens, then equity will be wiped out. So that's a risk of investing in oil. He knew about that. He knows about that. And it's all about the price of oil and he doesn't know where it will go long term.

On the question of breaking up Berkshire. He says that it will be a high tax endeavour that it eliminates the possibility to move capital around his capital allocation. That is one of the best Berkshire advantages. Of course, also discusses Wall Street doesn't get fees if nothing happens, like it is the case with Berkshire.

On interest rates, he says that there is more money printing and negative interest rates are low interest rates, and he has to see it to believe it that it will not affect inflation somewhere in the future. He doesn't see negative interest rates and more that for eternity. He was wrong 10 years ago, he might be wrong now, but he is now really saying how we are testing the question with much more force. Now, the most interesting question in economics, how come we have such low zero interest rates, negative interest rates and no inflation? So he's looking at the answer. He doesn't have the answer, but he's ready for anything. And they also discussed pricing power of their businesses like the railroad, like the energy businesses that will do good in an inflationary environment.

The question was related on the government, US government defaulting because of the huge debt, and he simply said, that can't be happening because the government owns the printing press. And if you own the printing press you cannot default and how the debt will just grow, grow and grow. And it's not a concern because they're borrowing in their own currency. Therefore, no default. The currency, my addition is can lose value real purchasing power, but that's a different story.

And then the most interesting question answered at the end on buybacks. How, okay, if you need the money to keep growing as company then it's not intelligent to do buybacks. You have to buy only below what the business is worth. And then he says how saying like, okay, we as a company are going to do 5 or 10 billion in buybacks over the next year is insane. It's crazy because then you are not thinking about the most important things when it comes to buybacks, which is priced. At some price, it does pay to do buybacks at some it doesn't. But as you announce it to the market, then that's not really sane. And then if some companies do stupid financial engineering to do buybacks to leverage the maximum out of their balance sheet, he was practically referring to here to Boeing, that is something that he says it's stupid.

I hope you're enjoying the summary. If you really enjoyed this mindset Buffett's investing mindset, this is the channel to subscribe to. So please subscribe, click that like button if you don't like this video, change your taste, click that like button. Thank you for watching, looking forward to your comments, and I'll see you in the next video.