A new research from Harvard Business School and MIT Sloan …it reveals major market inefficiencies in understanding earnings, and core earnings, esp unusual charges.

It shows that analysts and investors do not fully understand earnings.

Q3 2019 hedge fund letters, conferences and more

A few of the many great quotes from the paper:

"…these figures show that the New Constructs dataset provides a novel opportunity to study the properties of non-operating items disclosed in 10-Ks, and to examine the extent to which the market impounds their implications." - page 19, 2nd pp, last sentence

"...this is the most comprehensive dataset that captures what a fundamental analyst would be likely to identify as transitory or non-operating earnings items ..." - page 9, 2nd pp, 2nd sentence

Here’s a quick overview and key takeaways:

In “Core Earnings: New Data and Evidence”, Ethan Rouen and Charles C.Y. Wang of Harvard Business School (HBS) and Eric So of Massachusetts Institute of Technology (MIT) Sloan School of Management use our “novel database” of earnings adjustments to reveal market inefficiencies and show investors how to:

- Measure & predict earnings more accurately

- Lower risks of using misleading data from traditional providers

- Generate alpha

Only our research utilizes the superior data & earnings adjustments featured by the paper.

"…many of the income-statement-relevant quantitative disclosures collected by NC do not appear to be easily identifiable in Compustat…" - page 13, last paragraph, 1st sentence

"The implications of these findings are potentially far-reaching for investors and for researchers." - page 31, 2nd paragraph, 1st sentence

Core Earnings: New Data and Evidence

Harvard Business School Accounting & Management Unit Working Paper No. 20-047

- Ethan Rouen, Harvard Business School

- Eric C. So, Massachusetts Institute of Technology (MIT) - Sloan School of Management

- Charles C. Y. Wang, Harvard Business School

Abstract

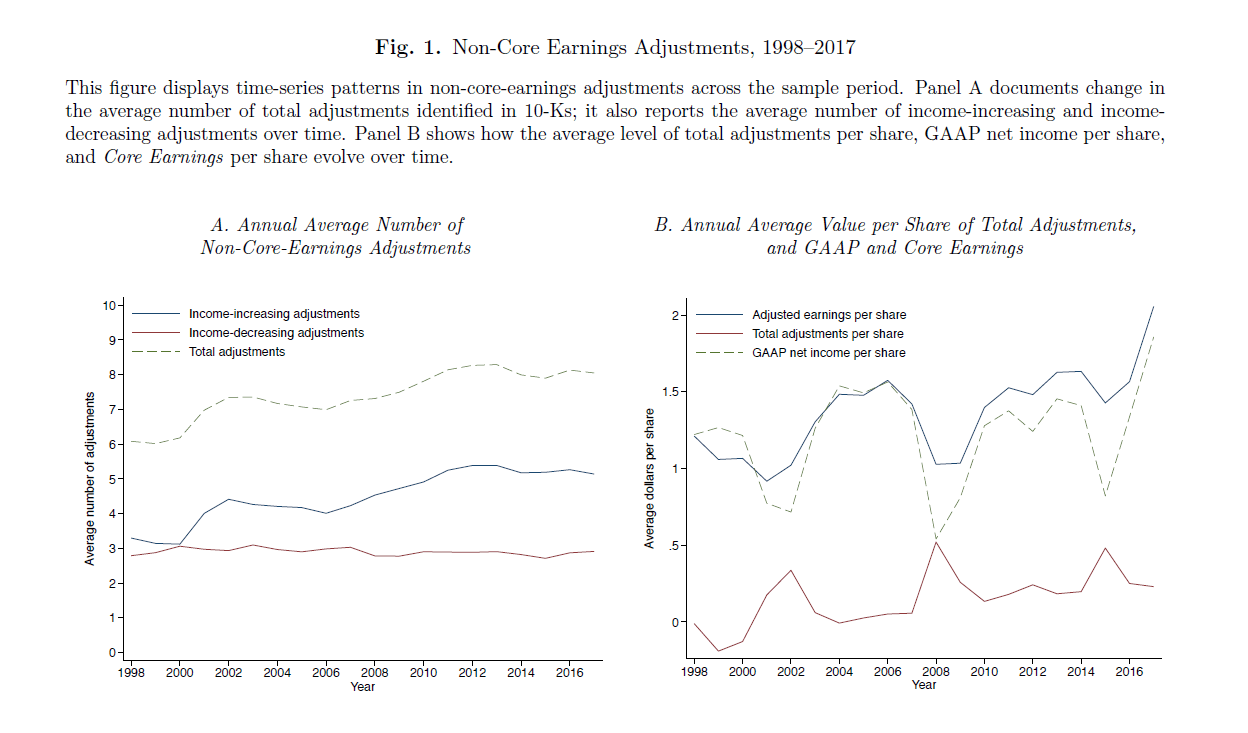

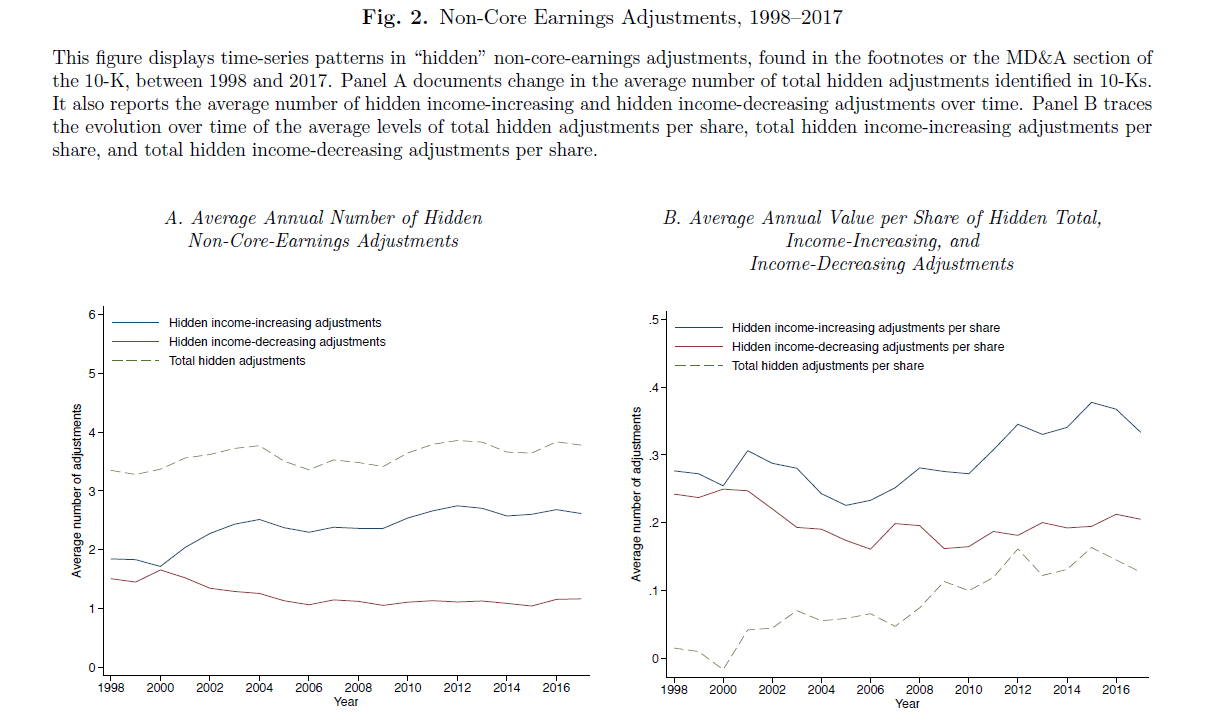

Using a novel dataset that comprehensively classifies the quantitative financial disclosures in firms' 10-Ks, including those hidden in the footnotes and the MD&A, we show that disclosures of non-operating and less persistent income-statement items are both frequent and economically significant, and increasingly so over time. Adjusting GAAP earnings to exclude these items creates a measure of core earnings that is highly persistent and that forecasts future performance. Analysts and market participants are slow to impound the implications of transitory earnings. Trading strategies that exploit cross-sectional differences in firms' transitory earnings produce abnormal returns of 7-to-10% per year.

Get the full paper at SSRN

{kind=link}