Crescat Capital commentary for the second quarter ended June 30, 2019, titled, “The Bear Case,”

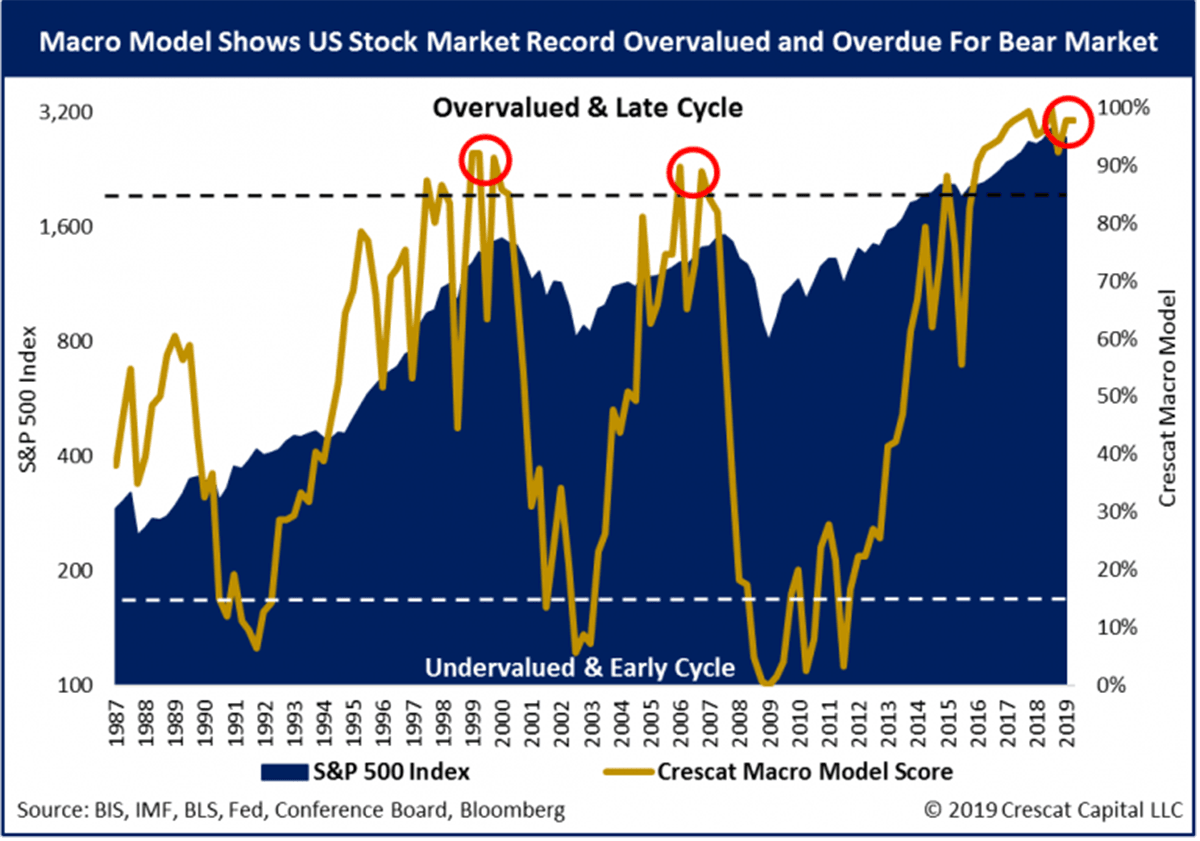

We believe there is an opportunity to capitalize on a material downturn in the business cycle based on the composite of timing and imbalance indicators in Crescat’s 16-factor macro model.

Q2 hedge fund letters, conference, scoops etc

US Equity Markets

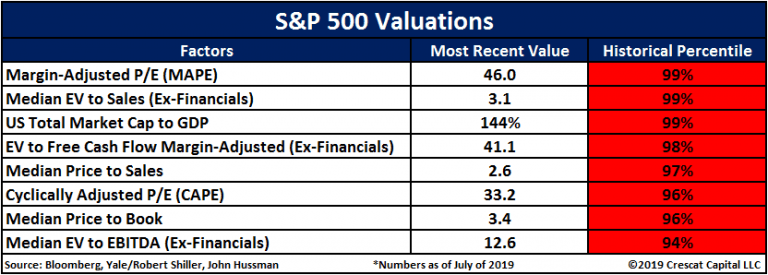

The downturn could be particularly brutal for US stocks because we are record late in a fading economic expansion and at historical high valuations relative to underlying fundamentals across a broad composite of eight measures that we follow at Crescat.

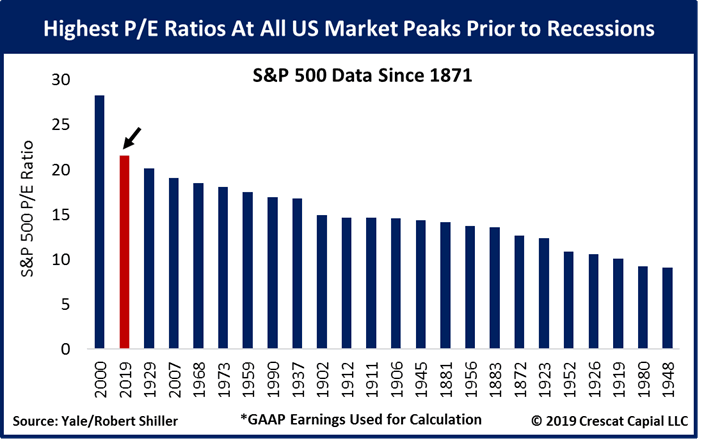

We hear two opposing valuation arguments from bulls today: 1. P/E ratios are reasonable; and 2. Valuations remain attractive relative to interest rates. Let’s address them both. First off, P/Es often appear reasonable at business cycle peaks because that’s when earnings are their strongest. For instance, back in mid-1929, prior to the stock market crash and Great Depression, S&P 500 real earnings per share (on a GAAP standard) had been growing at a unsustainably high 20% year-over-year rate, almost as high as the fleeting 21% growth we just had in 2018. Similarly, profit margins are cyclical. They top out at the peak of an expansion, making P/Es appear artificially low. US corporate profit margins in 2018 were the highest they have been since 1929. P/Es are always a potential value trap at the peak of a cycle. But today, P/Es are not even that cheap. Going all the way back to 1871, today we would have potentially the second highest P/E ratio ever for the S&P 500 at a market top prior to a recession, worse than 1929 and the housing bubble.

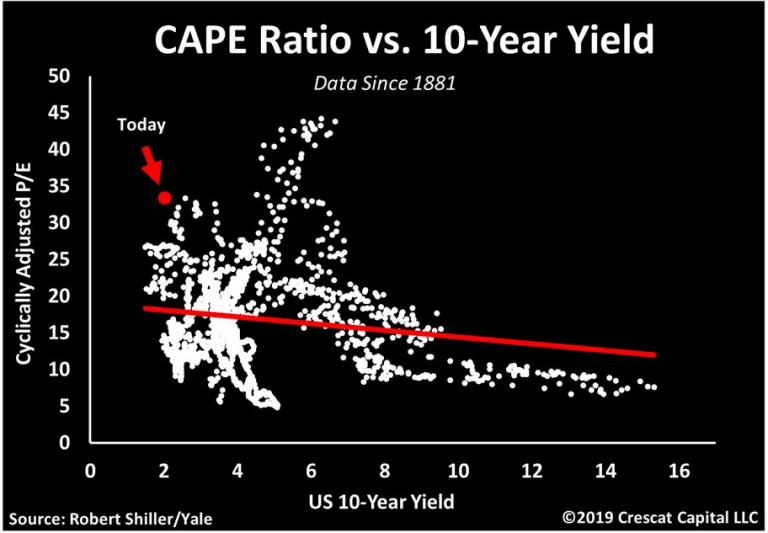

Tackling the second bull argument that low interest rates justify today’s high valuations, the flaw in this thinking is just as pronounced. The reality is that stocks have never been this expensive for how low the 10-year Treasury yield is today. It’s true that all else equal, low interest rates justify higher valuations. However, the lowest interest rates historically haven’t corresponded to the highest P/E markets because extremely depressed yields also signal fundamental problems in the economy. Ultra-low rate environments are often marked by highly leveraged economies where future growth is likely to be weak. Growth must also be discounted in the valuation formula.

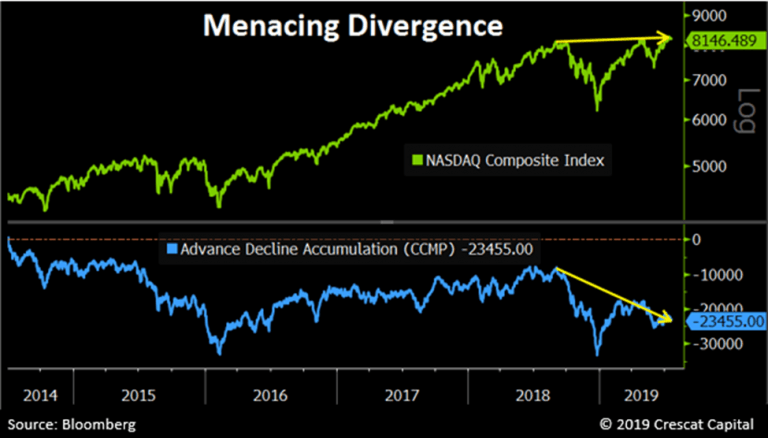

While many US equity indices have marginally broken out to new highs recently, they have done so in the face of weakening market internals. Equity indices are being propped up by a narrowing group of leaders. The deteriorating breadth is most evident in the NASDAQ Composite, home to today’s leading growth stocks. While the overall index has reached record levels, the number of declining stocks has significantly outpaced the number of advancing stocks since last September. The collapsing internals point to an exhausted bull market.

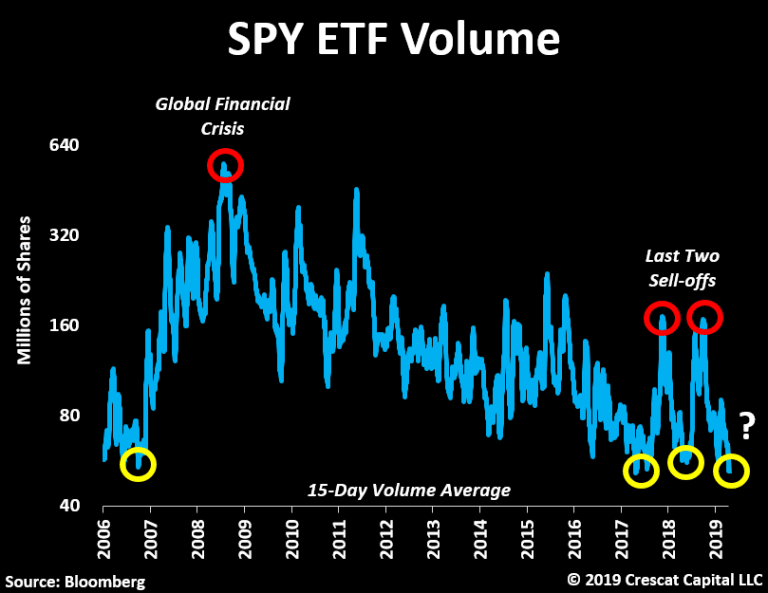

Stocks are also rising in defiance of extremely low volume. On July 16th, the SPDR S&P 500 ETF (SPY) had its lowest daily volume in almost 2 years. In a 15-daily average terms, volume is now as low as it was at the peak of the housing bubble and prior to the last two selloffs in 2018. Unusual calmness and breadth deterioration are not a good set up for record overvalued stocks.

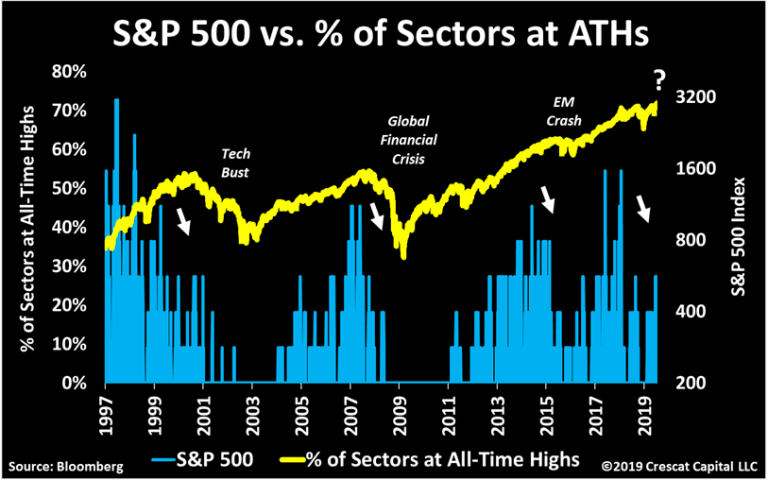

The following chart is yet another illustration of how this recent rally in equities is running on empty, and again lacking substance. On July 15th, S&P 500 reached record levels, but only three sectors were at all-time highs. Market breadth today is faltering just as much as it did ahead of the last two recessions. In 2015, this was also the case, but back then only 20% of the yield curve was inverted. Now it’s close to 60%!

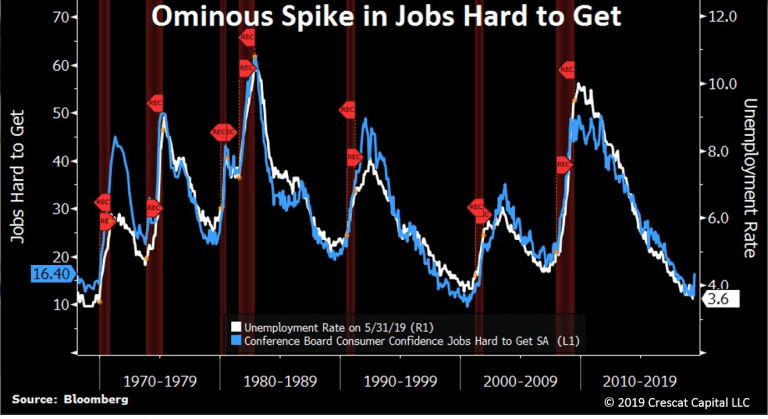

As we previously said, the unemployment rate has been one the most reliable contrarian indicators throughout history. It reaches a cyclical low prior to every recession since the 1970s. The year-over-year change, however, is what tends to confirm the turning points in the economy. Most of the times this rate shifted to positive, a market downturn followed. In this business cycle, the YoY change likely bottomed in late 2014 and it has now been flirting with the positive camp since then. However, other labor market indicators are already showing signs of weakening economic conditions. The Conference Board’s Jobs Hard to Get Index is one of them. It has recently spiked and is yet another classic late-cycle development in the economy.

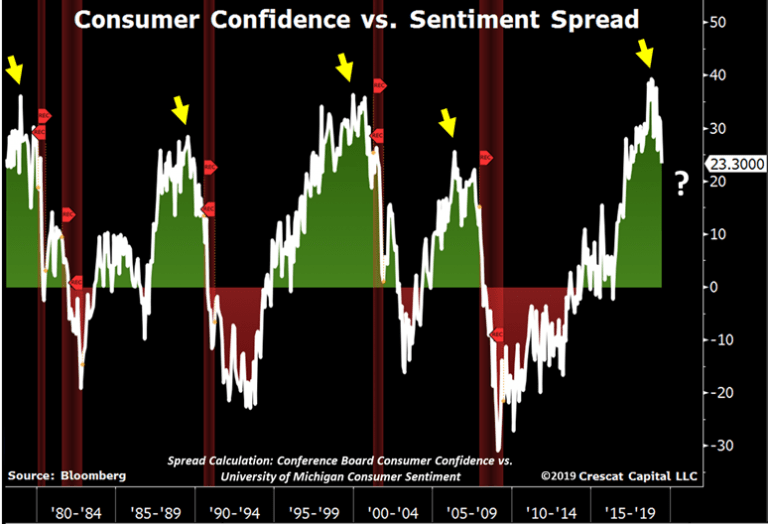

Consumer surveys are also critical to identify the stage of the economy we are in today. It’s another great contrarian indicator as strong consumer confidence has an uncanny relationship with market tops. We’ve noted this before, but since the 1960s, every time the Conference Board index surpassed the 135 level, it coincided with the peak of the economic cycle. The same source also reports two components of this survey that differentiate between consumer’s present situation and future expectations. As John Hussman originally pointed out, the spread between these two sub-indices tends to reach an extreme prior to a recession. That’s usually caused by consumers’ future expectations starting to fall first. The University of Michigan also publishes a survey on consumer sentiment. That compared with the Conference Board index forms another important indicator. All previous declines from cyclical highs in the spread between these two indices led to recessions. This time, the spread is plunging after reaching record levels.

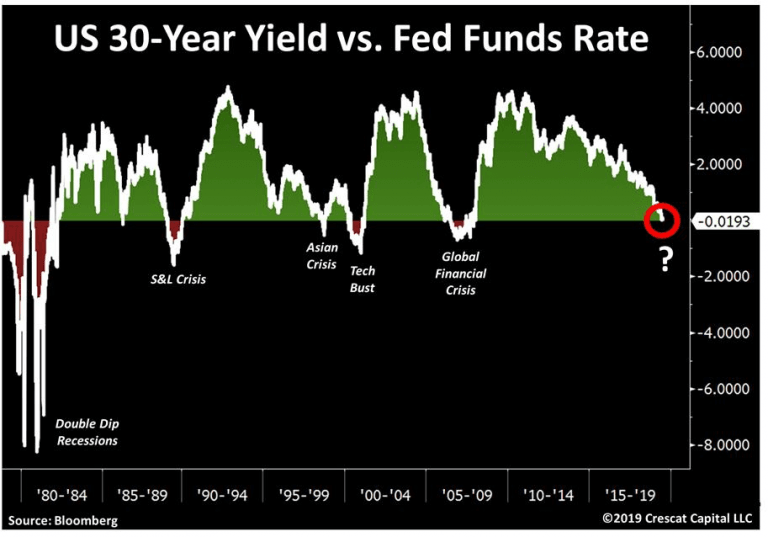

Crescat’s robust calculation of percentage of inversions in the US yield curve remains at recession-signaling levels. Over 55% of all 44 spreads are now inverted, being just as much as it was at the peak of the tech and housing bubbles. Nevertheless, another important development in credit markets occurred in the first week of July. As show below, the US 30-year yield dropped below the upper bound of the federal funds rate (FFR) for the first time since the global financial crisis. It’s one more bearish signal that adds to Crescat’s fire hose of cycle-ending macro data. The same warning occurred ahead of the GFC, tech bust, Asian crisis, S&L crisis, and 1980’s double dip recessions. The only false signal was in 1986, but one could argue that it did ultimately lead to the 1987 crash. Above all, as of July 2nd, we had the entire US Treasury curve below the Fed overnight rate. Perhaps the bond market is trying to tell us something.

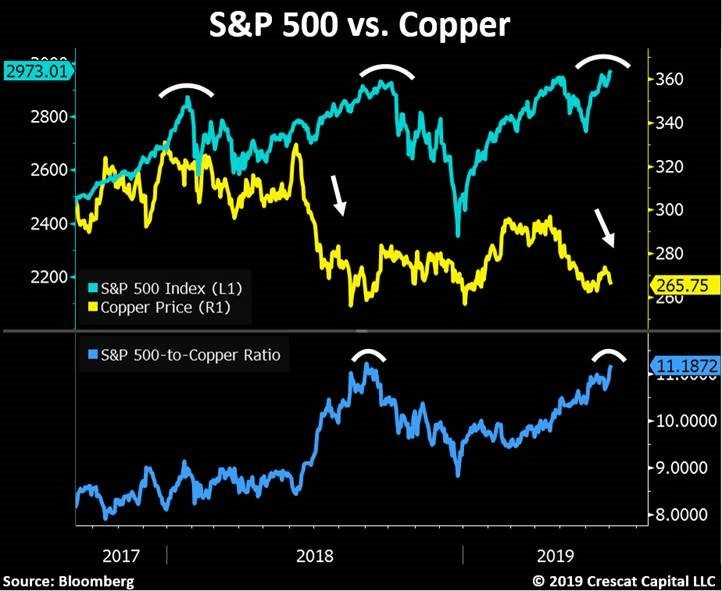

Cracks in the market are spreading and it could be pointing to a market meltdown. Copper, for instance, is now diverging from the S&P 500 by over 35% since September of 2017. Last time this separation reached similar extremes was at the September 2018 market peak. Dr. Copper is reputed to have a Ph.D. in economics because of its ability to help predict turning points in the global economy. Because of copper’s widespread applications — from homes and factories to electronics and power generation and transmission — strengthening or weakening demand for the red metal can be a leading indicator for the economy at large. The decline of the industrial metal itself doesn’t necessarily tell us enough to call for a downturn in the economic cycle. However, its deterioration versus other risk assets in combination with a litany of macro indicators adds conviction to our overall bearish thesis.

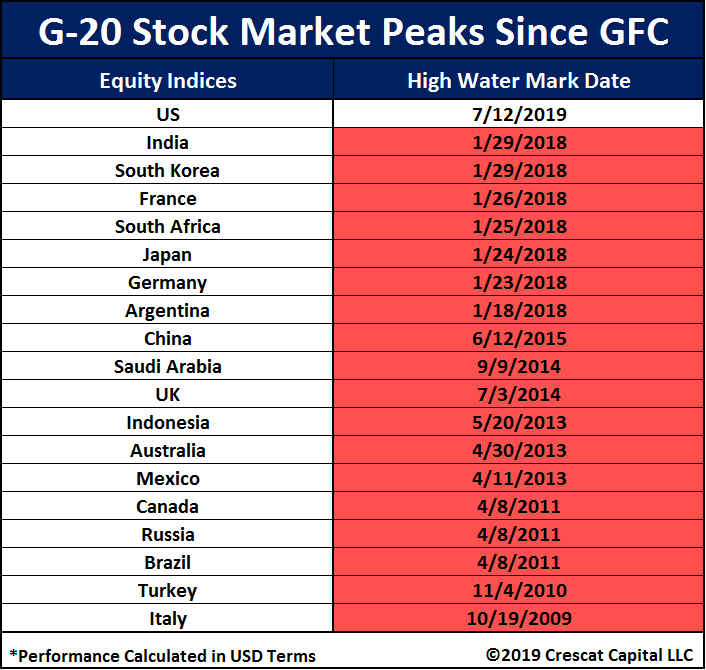

The US is the only equity market in the world to make new highs recently in US dollar terms. Every other G-20 index already peaked a long time ago, a troubling divergence. We believe the US stock market is likely to be the one to catch up to the downside.

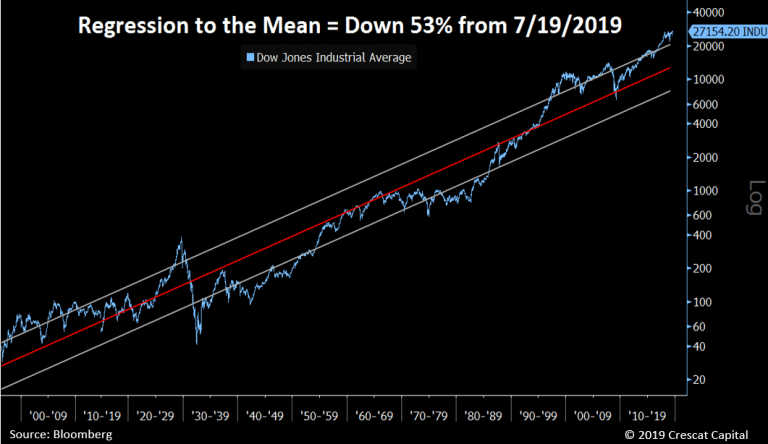

The US market is fundamentally and technically overvalued to an extreme. But, how much should we expect it to be down in a coming bear market? Just to get to mean historical valuations, it could be a 50% plunge. The problem is, a 50% decline would equate to the highest ever valuation at the depth of a bear market and recession in the US, so it could be a best-case scenario. That is how over-valued the US equity market is today! The downside in the market today is perhaps easiest to visualize in a logged version of the longest running US stock index, the Dow Jones Industrial Average.

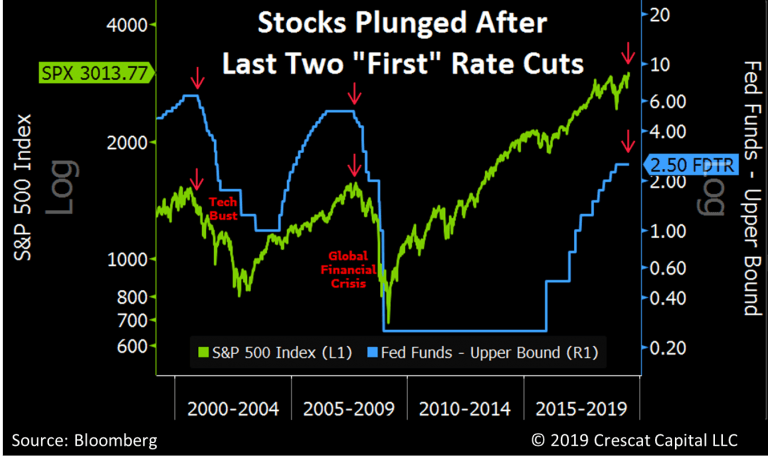

Conventional wisdom is that the first Fed rate cut is bullish, but this was not true with the last two business cycles as we clearly show in the chart below. It will likely not be true in this one either because we are record late into the expansion at historic high valuations. It’s true that all else equal, monetary easing is fundamentally bullish for stocks and the economy, while tightening is bearish. The problem is that central bank policy works with a lag. The delayed reaction to Fed interest rate policy is why our macro model uses the 24-month trailing rate-of-change in the federal funds rate as one of our factors to forecast the economy and the stock market.

The interest rate hikes and quantitative tightening of the last three years, are the substantial bearish macro drivers that have only now started to transmit into economic weakening in the US. Meanwhile, the Fed has also just acknowledged the deterioration in the overall global economy. We think the truth of the economic weakening matters more than the hope from imminent Fed easing. Only at the depths of the recession, when everyone else is panicking and dumping stocks that are already down substantially, should we get excited about Fed easing transmitting to a new bull market.

The Fed’s polices of near-zero interest rates and quantitative easing since the global financial crisis have created enormous asset bubbles in stocks and corporate credit. Investors’ speculative behavior is a natural reaction to cheap money and has played an integral role in inflating these bubbles. Just as asset prices rise in a positive feedback loop of easy credit, investor speculative behavior, consumer and business spending, so they decline in the opposite self-reinforcing fashion: credit defaults, credit tightness, investor risk aversion, and business and consumer retrenchment. Such is the natural ebb and flow of the business cycle.

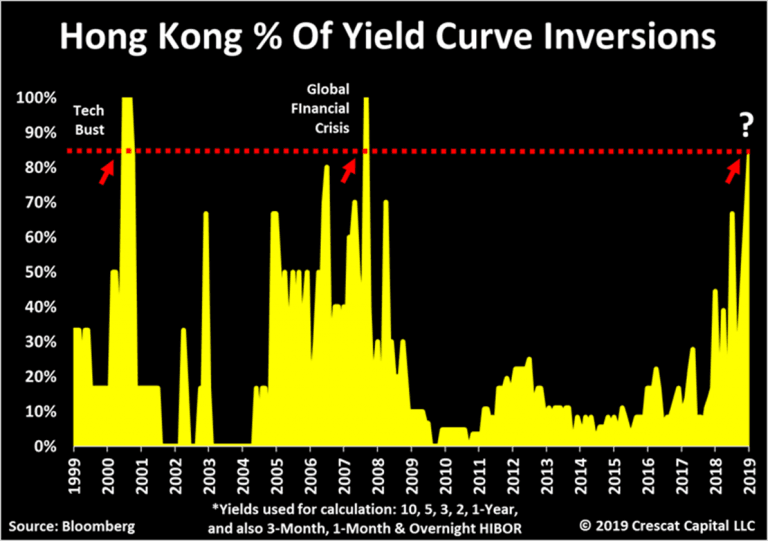

The property market in the US is also richly valued, in our view, though home prices are not as frothy relative to income and household debt as they were in the housing bubble. The big housing bubbles in the world today by these measures are in China, Hong Kong, Canada, and Australia.

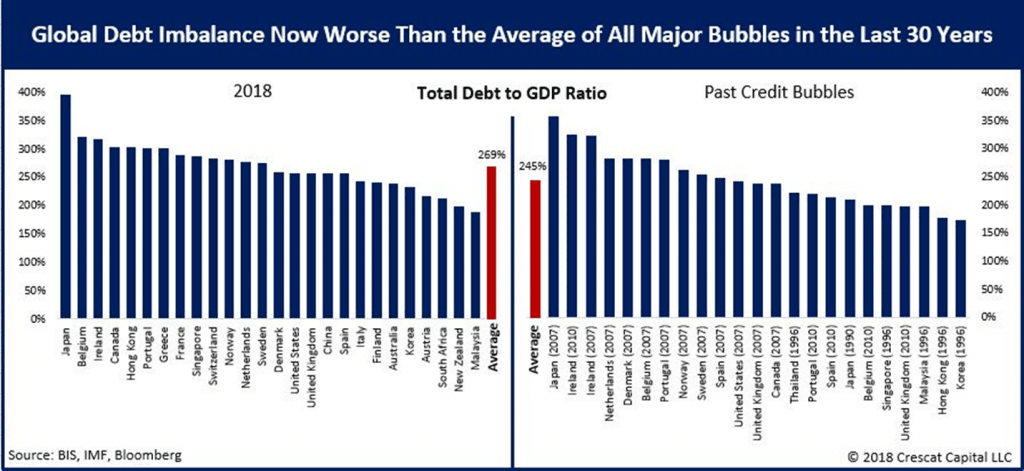

Because the US dollar is the largest fiat reserve currency, the Fed’s past accommodative policies has allowed other countries to pursue their own easy money schemes and accumulate record levels of debt. Across the globe, these levels are higher on average than they were prior to all major credit busts of the last 30 years.

China

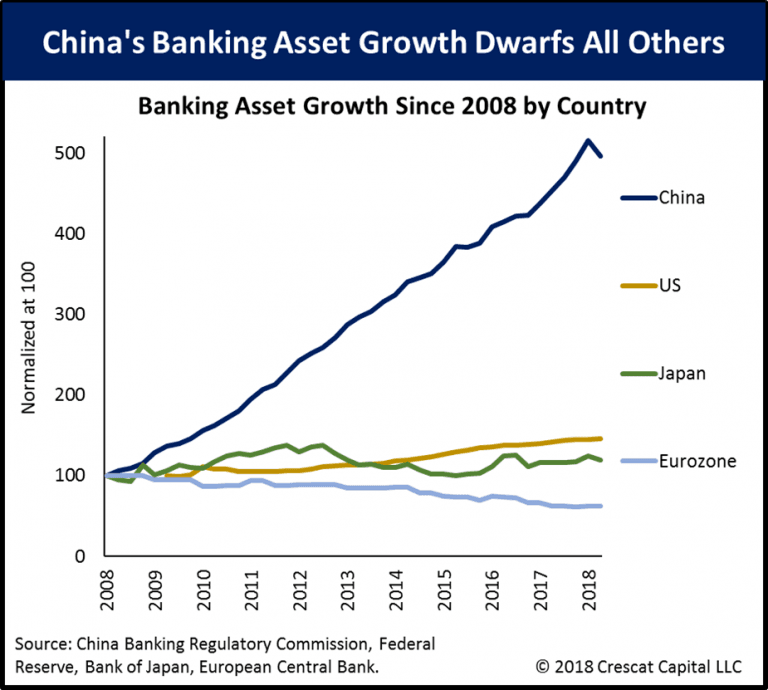

We have written extensively about China’s currency and credit bubble in past letters. China was responsible for over 60% of global GDP growth since the global financial crisis. The country’s massive investments in non-productive infrastructure assets was financed on credit and created high GDP growth but failed to add wealth or debt-servicing capacity. China has created an enormous currency and credit bubble in the process. The problem is that its central planners accomplished this incredible economic growth through an unsustainable growth in fractional reserve bank credit. Since 2008, China’s banking system assets have grown 400% to USD 40 trillion!

This insane level of expansion for a large economy was made possible because China’s communist leaders mandated high lending growth from its state-owned banks. At same time, they ignored the true write-down of non-performing loans.

As a result, we believe the value of China’s banking system today is grossly mismarked. The Chinese financial system in our view is a Ponzi scheme poised to unravel and is likely to be a major contributor to the coming global economic downturn. The Chinese citizens are the primary creditors who could be on the line, but the rest of the world that has invested in China will almost certainly suffer with them.

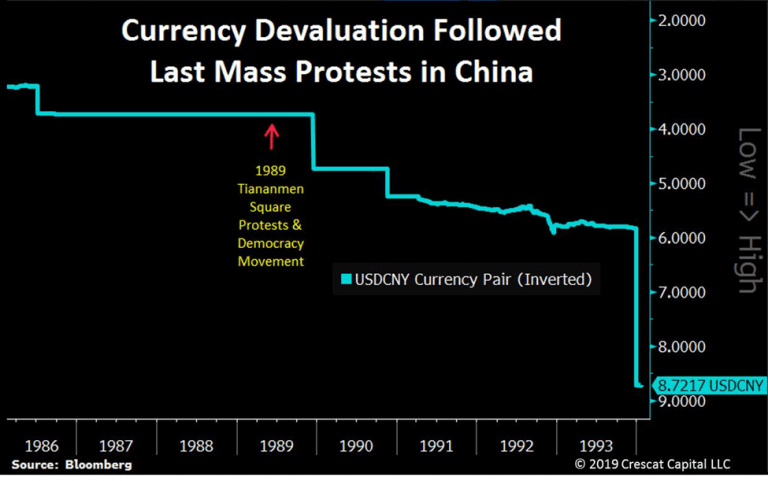

We believe the Chinese government will be forced to print money to recapitalize its banks and bail out its citizens to attempt to quell social unrest. The massive monetary dilution could lead to a currency crisis which is the lesson of almost every emerging market credit bubble in history from Latin America to Asia. Currency crisis is also the ultimate consequence of economic failure of centrally planned communism as we have learned from the Soviet Union to Venezuela.

Our outlook for both the Chinese yuan and Hong Kong dollar is extremely bearish and we are positioned accordingly in our global macro fund. The warning signs of the coming Chinese crisis are everywhere from the Trump administration’s year-long hardball on Chinese trade, to the recent Chinese government seizure of failed Baoshang Bank, to the current mass anti-Chinese Communist Party protests in Hong Kong.

Precious Metals

Precious metals are one of the few pockets of this market offering tremendous value to hedge against extreme monetary policies, bursting asset bubbles, and record global leverage. We see this opportunity playing out across gold, silver and related mining stocks. Gold is the ultimate form of money with a long history of storing value for investors and outperforming risk assets during market downturns. In our view, a new wave of global fiat currency debasement polices is now in its early stages. Gold should become a core asset for those who believe in this macro development, but it is still widely under-owned today.

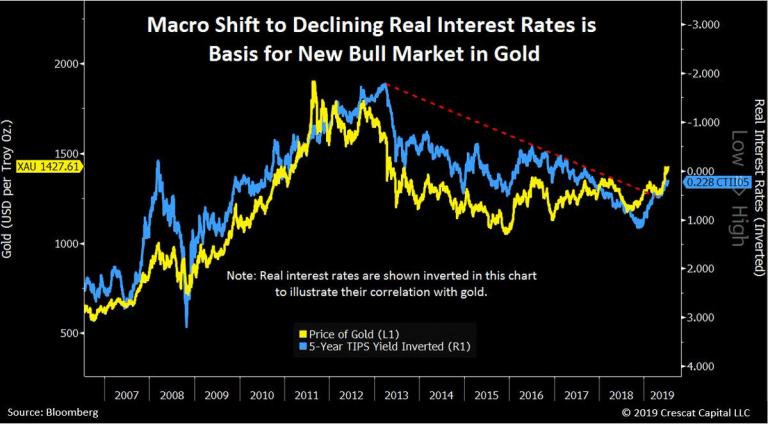

With the Fed shifting back to easing mode as the global economy is faltering, new fuel has ignited a precious metals fire. It is still very early in the game in our analysis. Rate cuts point to a new trend of declining real yields to drive precious metals higher even before inflation returns. Below we show seven-year trends in real rates and gold that have just reversed.

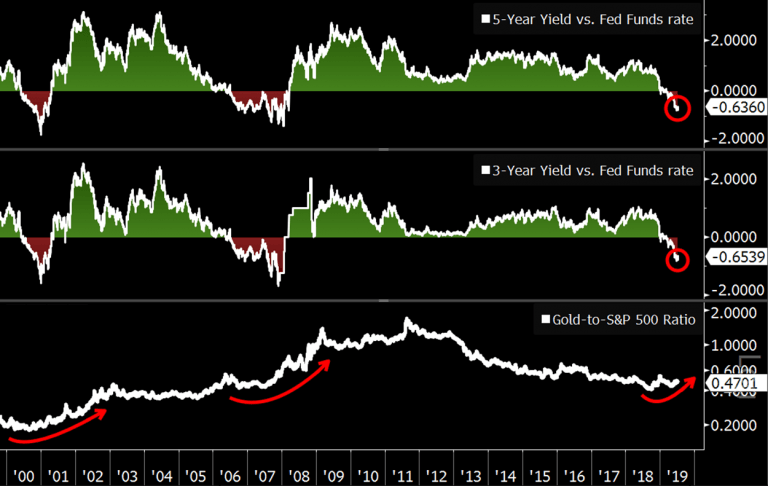

Credit markets tend to serve as a bellwether for stocks and the economy, and rising yield curve inversions happen to be great times to buy gold and sell stocks. For instance, 3 and 5-year yields have recently dipped below Fed funds rate for the first time since the global financial crisis and the tech bust. As history has shown, this is bullish for the gold-to-S&P 500 ratio.

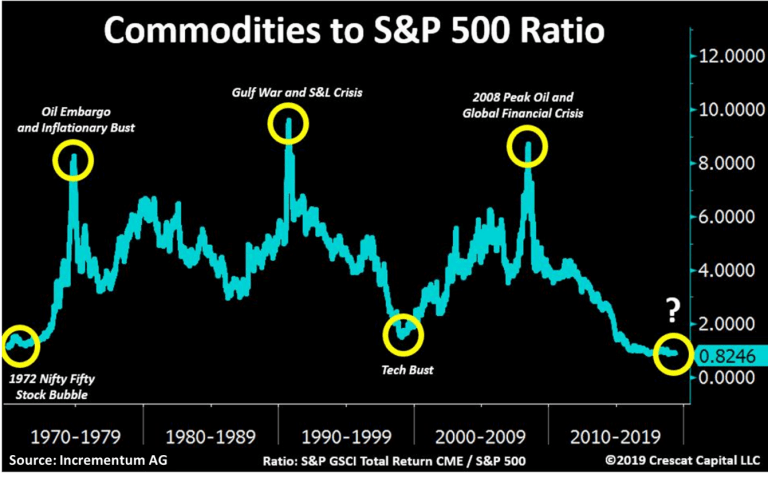

Another way to see how incredibly undervalued precious metals are relative to other risk assets is by looking at the relative performance. The commodities-to-S&P 500 ratio has just reached a fresh 50-year low. The last times we had such historic imbalances we were at the peak of the 2000 tech and the 1972 “Nifty Fifty” stock bubbles. If one uses a simpler version of this relationship, using the Dow Jones Industrial Average index, the ratio is well below the cyclical 1929 lows that lead to the Great Depression.

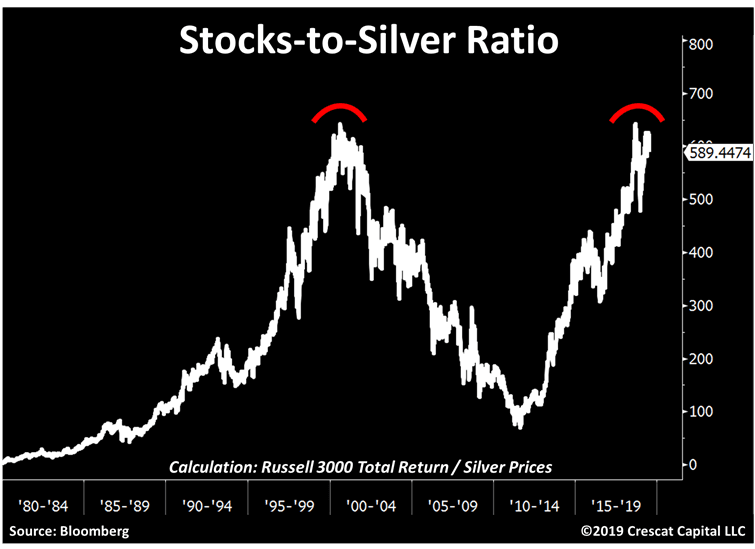

Silver, a more speculative version of gold, also looks historically cheap. One way to see this is by comparing it against the total return for broad US stocks. The Russell 3000-to-silver ratio is still near all-time highs. This puts into perspective the incredible opportunity likely ahead of us today and how truly early and undervalued it is. In technical terms, look at the double top formation after a retest of peak tech bubble levels.

We also feel very strongly that gold and silver mining stocks are undervalued as the current macro set up seems largely optimistic for precious metals. This entire industry has been through and eight-year bear market with some of these stocks down by over 80% since 2011. Given our strong outlook for a new secular bull market in gold and silver, we have decided to launch a new precious metal long-only strategy focused solely on a selective number of mining stocks to capitalize on this trend. Crescat’s Large Cap, Long-Short, and Global Macro strategies already have significant allocations to precious metals mining stocks. Our goal is to carve out this theme specifically for those who want to tap into it directly.

Outlook for Crescat’s Strategies

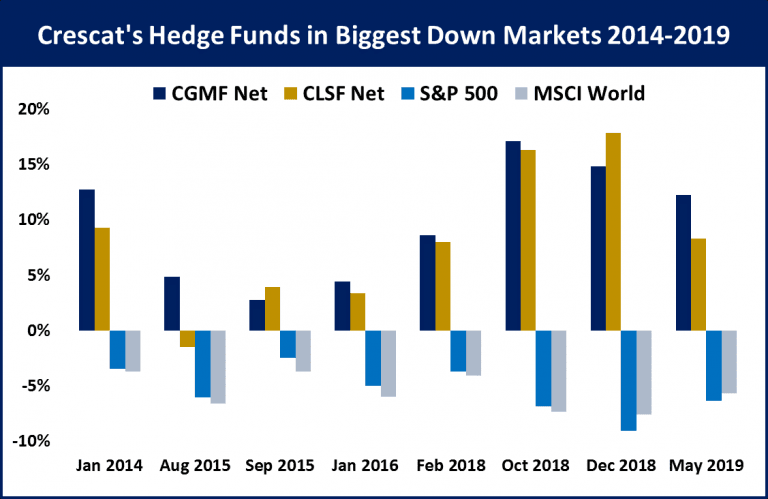

At Crescat, we are tactical bears based on our macro and fundamental models. We are looking to capitalize on the highly likely downturn in the economy that should be soon upon us. We had a glimpse of what a downturn might look like in the fourth quarter last year. Crescat’s hedge funds profited extremely well during that period as many of our macro themes and positions worked in our favor. We strongly believe that was only a foretaste of what is to come in the markets over the next one to two years on a grander scale. The chart below shows how Crescat’s two hedge funds performed during the worst down markets of the last five years. One can clearly see how increasingly bearishly positioned we have become over the last two years. We remain so today. One can also see how well we have profited from the down markets recently. We believe they have only just started to emerge.

In our flagship global macro hedge fund, our most significant exposures today are long precious metals and related miners, net short global stocks including US stocks as well as stocks in China, Hong Kong, Australia, and Canada. The global macro fund is also substantially short the Chinese yuan and Hong Kong dollar in a risk-controlled, asymmetric trade though laddered put options.

We believe in taking a moderate amount of risk to deliver a strong return. We have been following our risk controls to contain the necessary pullbacks along the way. While past performance is not a guarantee of future returns, across all our strategies, we have been through moderate pullbacks before and have always recovered substantially from them. We are highly confident that we can and will push to a new high-water mark again soon. We have honestly never been more excited about the opportunities directly in front of us.

All Crescat strategies are in the black in July month to date. Being net short in our hedge funds, this is a material development with equity indices pushing to new highs. Market breadth is faltering, so many of our shorts have been working. We believe the risk of being net short today’s market is significantly diminishing. Meanwhile, our precious metals longs have been moving up substantially.

About Crescat

Crescat is a global macro asset management firm. We develop tactical investment themes based on proprietary value-driven models. Our mission is to grow and protect wealth by capitalizing on the most compelling macro themes of our time. We aim for high absolute and risk-adjusted returns over the long term with low correlation to benchmarks.

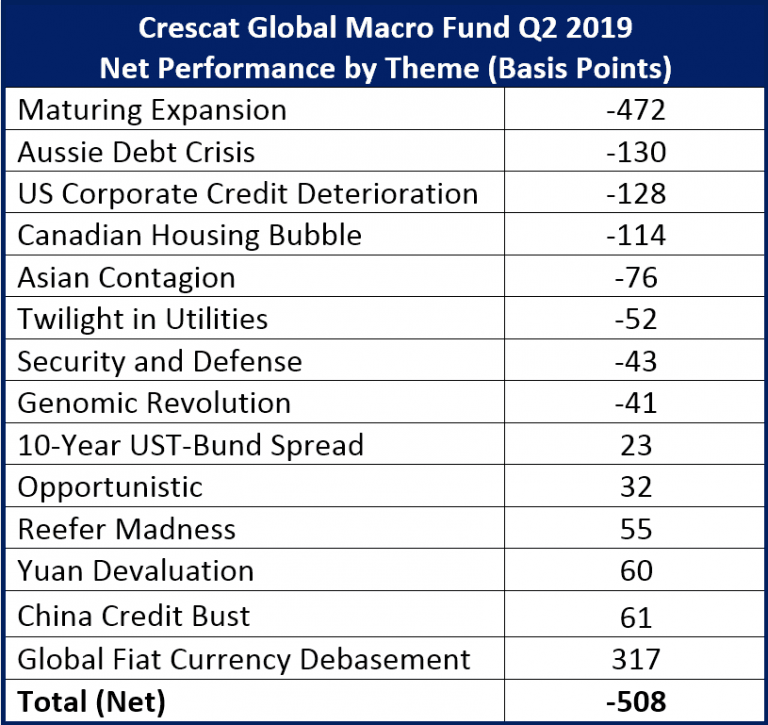

Q2 2019 Profit Attribution

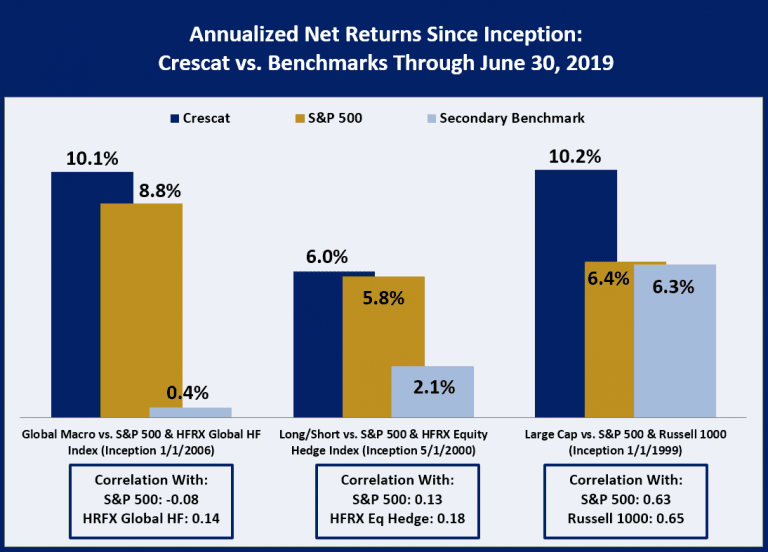

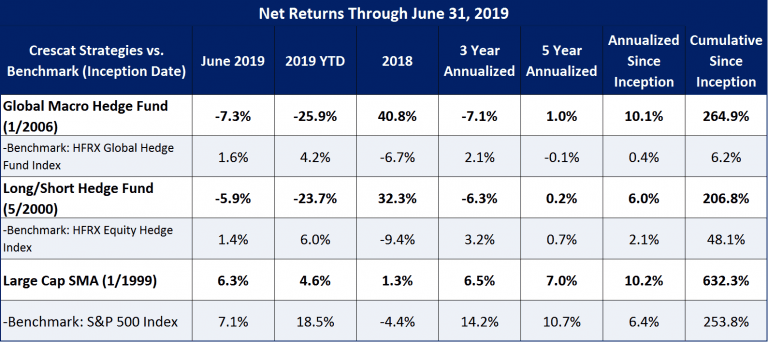

Performance through June 30, 2019

Sincerely,

Kevin C. Smith, CFA

Chief Investment Officer

Tavi Costa

Global Macro Analyst

Article by Crescat Capital

{kind=link}