In this session, we continued our analysis of pricing by looking at applications. We started with the question of whether your comparable firms samples should be tightly defined (and small) or broadly defined (and large) and how to control for differences across firms. We then used the cumulated knowledge to pass judgment on a series of naive pricing recommendations.

Slides: http://www.stern.nyu.edu/

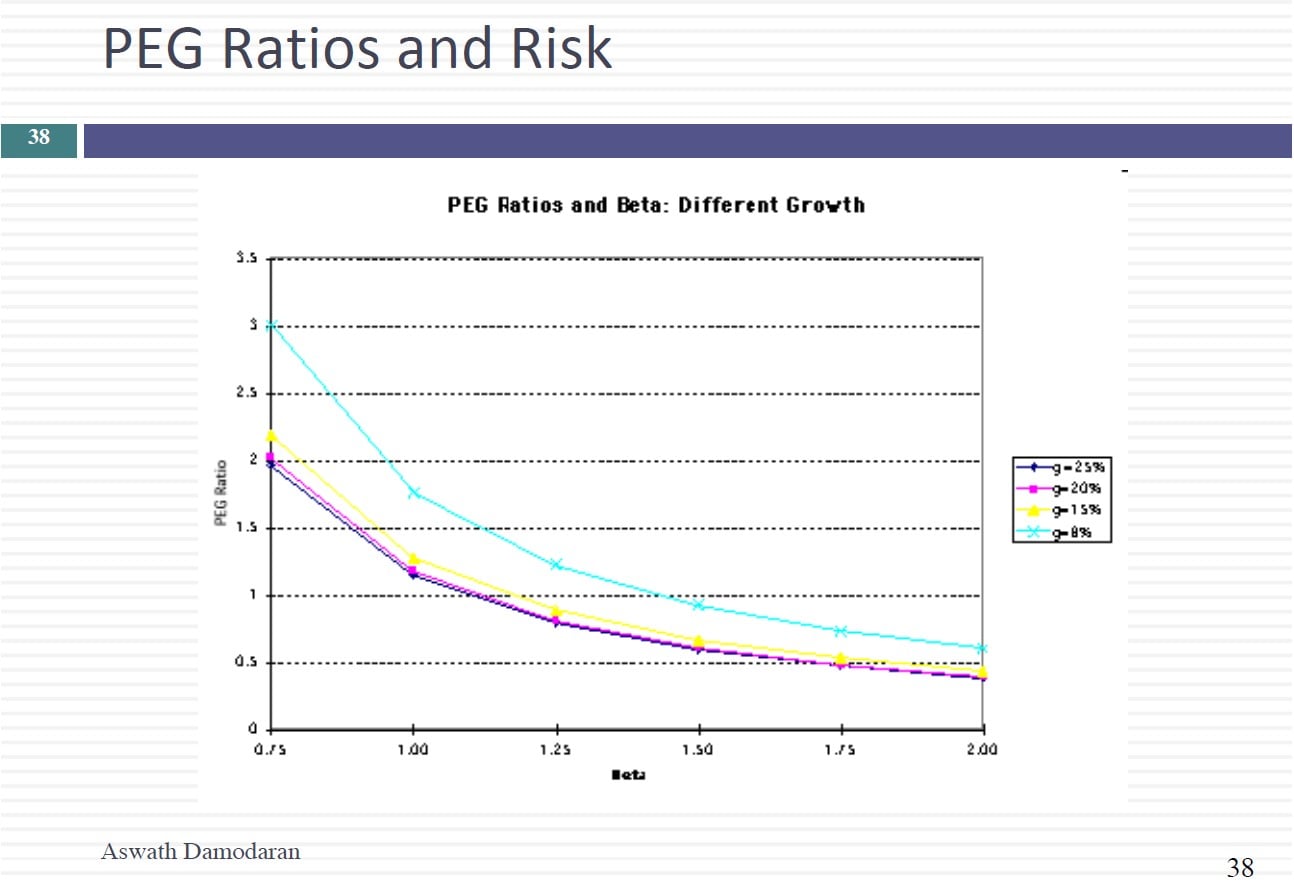

Session 18: Pricing Continued

[klarman]Q1 hedge fund letters, conference, scoops etc

Transcript

You know those two questions I use to start every class off like the first five sessions. I think it’s time I ask those questions again because there were a sneaking feeling. That for some of the answers no. Tell. Them Have you picked a company yet. I hope you have. Right. If you haven’t. Don’t let me know I don’t want to know right now. Act like you have. Them. If you haven’t picked the company obviously you didn’t turn into DCF for feedback so that part didn’t go well. And I tell you what I keep the window open. So if you’re if you get a DCF down at any point in time you just one quick feedback. Send it to me because I know I know this is for those of you kept the deadline you say. This is so unfair. This is one of those things where it doesn’t really hurt you. It had somebody out. So that’s it. I’m opening the window again. But you know at this week’s valuation of the week is going to be right. It’s going to be Wilbur. Hey I’d put up my uber valuation and post yesterday. And what I want you to do is really give this a shot because this is going to be a high profile IPO. And I don’t want to reflect my values I have my story and my value. I’ve created a spreadsheet there. And one of the things you are going to see in a spreadsheet is a very different way of approaching valuation than what we’ve done so far which is stopped down. By project revenues. I do that for you as well. But I also value a right. What’s the value of a rider tuber. We think a DCF of the value of rider. It’s a present value of the expected cash flows from the right so to get those expected cash flows what are some of the things I need to know. One is I need to know an expected lifetime that the writer is going to stay on. I guess I need to know your renewal rate that you would stay on as a writer. I need to know how much gross billing a writer brings and how much that will grow and then need a discount rate. DCF is not the reason you kind value right is that the information is my see saw value right of ruber. And I come up with the value about 474 80 dollars per rider. How many writers does Uber have right now.

Anybody have a guess. So none of you have been reading the prospector’s over the week and I thought that’s what you’d be poring over. There are 91 million writers right now. 91 times 478 gives me about 44 billion dogs. That’s the base. My dad. Where do I have to factor next. You write that the mayor might add on and to value those new neuritis I need one additional piece of information which is. What the cost of acquiring a new writers value. You write about 378 orders and I make some assumptions about how many new writers who are saying how do you know that. I don’t it’s my story I’ll tell you a story that so I expect them to more than double the writers to about 250 million. In ten years. I come up with the value for the new writers of about 60 billion. I’m done. That takes care of existing writers new writers who say I’m done. The only problem is there are expenses unrelated writers like what are the expenses that GeoNet expenses the corporate expenses that’s still intact. This is the problem with building up you’ve got to mop up loose ends. I take the present value of those cars that knocks about 50 billion off the value. Saying that’s a lot of money a lot of expenses not relate to writers. You bring them all together you’ve got the value for the operating assets. I my damn. I’m getting closer.

But here’s the problem. Duber. I have to add cash that’s the easy part. I’ve the I. The proceeds that go to the IPO which right now I’m pulling from rumored numbers because we actually don’t know fully. But it looks like going to be about 10 billion. I’m I don’t know. Do you remember what’s happened Dewberry in Asia in the last three years what have they done. They have said it from China exited from Southeast Asia and while this is not Asia it all takes it from Russia. You’re saying that so so they’ve done great but when they exited from China where did they get in return for exiting and leaving the market. DD they got 20 percent of DD. When they exit in Southeast Asia they got 23 percent of grat when they accepted Russia they got 38 percent of Yandex taxi.

To complete my valuation. But what do I need to do. Need to buy the three private companies with zero information. I threw off my hats.

The way I do them is I took their writers that I have a value for uber and I kind of scared the value to what their net revenues are. And that adds another nine billion and cross holdings and those three companies mostly from BT.

And Uber has about six and a half billion in debt. I get about you of equity and a value for share. That’s my story my value.

That spreadsheet is there so you can go play with.

{kind=link}