Coming into the end of 2017, APAC (Asia-Pacific) banks accounted for 50% of Basel III securities issued worldwide. This sizeable share has accumulated as a result of the fast pace at which APAC banks have issued Basel III securities since 2014.To be more specific, recent research from Moody’s highlights that in 2017 around $70bn worth of securities were outstanding from APAC banks, compared to near $45bn for all other regions assessed combined together. To put the depth of the trend into perspective, in 2014 the figures were approximately $90Bn and $85Bn respectively.1

Basel III Securities – Theoretical Loss Absorption?

Basel III is an internationally agreed set of measures that were developed by the Basel Committee on Banking Supervision after the GFC - aimed at strengthening the regulation, supervision and risk management of banks. More specifically, Basel III securities, by design, incorporate loss absorption and thus capital protection, into the balance sheets of our biggest global banks. Point of non-viability (PONV) triggers are contractually included in these instruments to create the loss absorbency characteristic.

APAC dominating issuance

A key driver of the sharp uptick in APAC issuance, which peaked in 2014, has been the implementation of ba in the region. APAC banks have needed to issue securities to both create balance sheet buffers as well as generate balance sheet growth over the past 3 years. Issuance tailed off in 2015 and 2016 – mainly due to slowing from Chinese and Australian banks who were more comfortably funded. However, 2017 brought a further up move in issuance volumes - predominantly driven by China, accounting for $48 billion worth of issuances, and making up 51% of APAC Basel III securities issuance as of November 2017 month end. 1

Risk Exposure – Heating Up with China & Tier 2

With this significant APAC, especially Chinese, exposure in capital markets investors will understandably be left wondering whether this is cause for concern? With the recent revelations of masked economic data from China’s leaders and the growing debt bubble speculation, the dependency of the global economy and financial markets does give some reason for pause.

This cautionary argument is far from countered when we consider that the majority of securities issued by APAC banks were Tier 2 contractual PONV instruments as at end-November 2017 (64%). Tier 2 capital is typically less resilient than Tier 1 capital, based on the difficulty in accurately calculating valuations and often due to inclusion of illiquid assets. Further to this the Chinese renminbi made up close to 40% of the currency exposure of the outstanding securities, followed quite a bit behind by the USD with only 25%.1

Uncharted Territory

Investors might argue that the exposures are in Basel III accordance and so loss protections have been built in. However, how the loss absorption will actually be enacted remains unclear. Moody’s highlights that a lack of real life examples prevents them from accurately assessing the ratings of Basel III contractual PONV securities. Since the time of introducing Basel III in 2013, there has only been a handful of instances of distress events to APAC banks. Therefore, how regulators will apply the terms of contractual PONV securities in practice remains uncertain. This then brings up another potential sticking point – each country has its own regulatory discretion, creating regional risk imbalances and more uncertainty of potential outcomes. The leaders of APAC nations may be in agreement with Basel III now, while positions are on side. However, if and when it comes to taking losses can we be so sure each nation will be singing from the same hymn sheet?

Sources:

1Moody’s Investor Services, Banks, Asia Pacific 5th February 2018

....................

When Bloomberg initially reported China may be considering halting purchases of US Treasuries, it initially sent yields jumping and stock market futures lower. The threat fits with a pattern of ongoing speculation that Chinese debt purchases and liquidations could be used as a weapon of intimidation.

But was China's motivation political, or, like much Chinese strategy, was it one of several strategies that could achieve multiple objectives? While global political and economic analysts were scrambling to unravel the correct interpretation behind the debt threat, Capital Economics Chief Asian Economist Mark Williams threw another variable into the motivational soup. How much of the Chinese bond decision was systematic and how much involved actual discretion? In other words, the Chinese debt decisions were already made regardless of the political dynamic.

Are Chinese debt purchases a formulamatic decision?

Chinese debt purchases might be made based in large part on a formula, not just the political whims of leaders. In other words, officials may have little choice in the matter, Williams observes in a January 10 piece titled “PBOC’s hands are tied over US Treasury holdings.”

Despite political rumblings based on the juicy assumption of geopolitical intrigue might be surrounding the decision, one probabilistic outcome is that the People’s Bank of China might simply be filling a numeric mandate.

“China has not been buying US debt for most of the last few years,” Williams wrote. “And, in practice, the People’s Bank has fewer choices over the size or allocation of its foreign exchange purchases than is sometimes assumed.”

As China de-levers its economy, with sub-par or questionable government loans a one-time concern, it creates an interesting market environment. They now have a currency that floats, part of the influential SDR Reserve system, and keeping it stable is a key concern.

Williams explains the technical underpinnings:

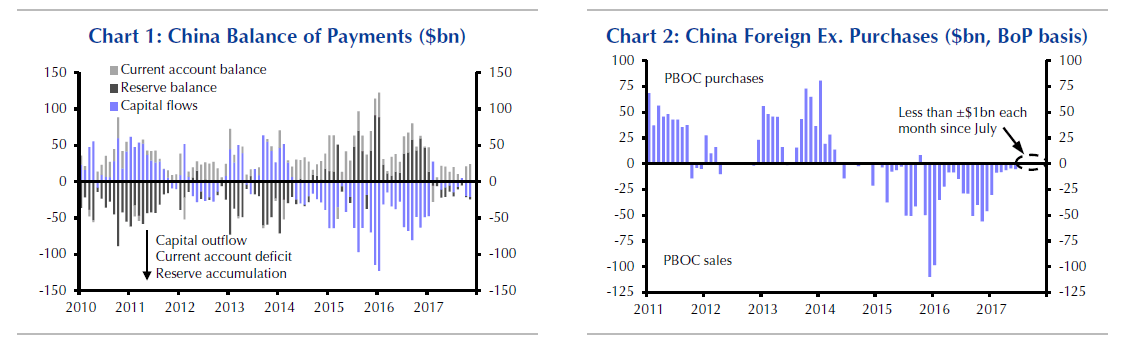

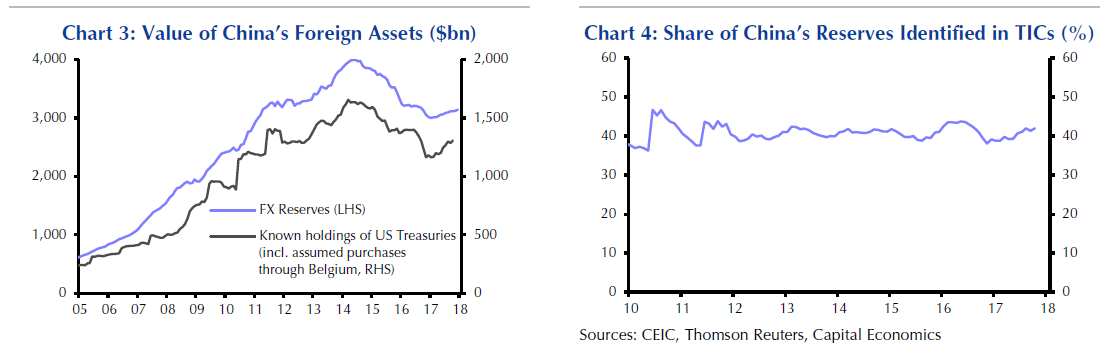

For any economy, the volume of foreign asset purchases is simply the inverse of the current account surplus. In economies with floating currencies, the two are balanced by movements in the exchange rate. For those with managed currencies, like China, monetary authorities adjust purchases and sales of foreign assets to keep the exchange rate at the desired level.

The bottom line, he points out, if China wants to keep its currency broadly stable “it can’t choose how much foreign exchange it buys or sells.”

Chinese warnings came at a time President Trump appears to be engaging in "New York-style" negotiations

The intrigue over properly interpreting shifting Chinese intentions is almost as meaningful as the economic changes the “communist” country has experienced.

The initial concept of a “workers’ paradise” through a socialistic economic model has given way to the leading source of computer automation in the world, one with a capitalistic bent but without the democracy component.

Depending on how one measures success, it has worked. It created a class of successful entrepreneurs and booming economy, but it also created some of the worst pollution problems in the world, which they are attempting to address.

These shifts are not all that unusual in the arch of the Chinese story.

First Bloomberg reported Chinese consideration of cutting off debt purchases just as tension levels with North Korea have been rising. Bloomberg, citing sources familiar with the discussions, said the nation with the world’s largest foreign-exchange holding was considering “slowing or halting” purchases of US debt. The comments came as the US has been attempting to pressure North Korea to abandon its aggressive nuclear weapons expansion program. During the negotiations, Trump has repeatedly played “good cop, bad cop” with North Korea, who has long relied on economic support from China.

From Trump's standpoint, this is the taken from the "Art of the Deal" now expressed on a global stage.

The day after the Bloomberg piece broke, the New York Post reported Chinese officials denied reports they might halt debt purchases. “The news may quote the wrong information source, or it may be fake news,” a post on the website of the State Administration of Foreign Exchange in China said. On the one hand, the statement lent support for Trump’s “fake news” claims, while at the same time working to lower tensions.

But don’t ever forget the Chinese have several weapons, one of them being economic. A war in the region without general consensus could result in a battle on multiple fronts, including economic.

But none of this matters, says the Capital Economics report. Chinese debt purchases are, to various degrees, relatively systematic.