Welcome to the December 2019 (Q4) issue of Hidden Value Stocks. In this issue, we included interviews with two fund managers as well as recent updates from the Olesen Value Fund, Saga Partners and McIntyre Partnerships. The first interview is with Samir Patel, the Founder and Portfolio Manager of Askeladden Capital Management. Samir is also the author of Poor Ash’s Almanack.

Askeladden is looking for exceptional quality businesses that have the potential to compound investors’ capital at an attractive rate over the long-term. The firm focuses on “trying to be business analysts rather than investment analysts,” and cares about making the right decisions on two different levels: First, what data to collect and second, the right investment decisions based on “whatever useful data we collect.”

Since inception, (Q2 2016), Askeladden has returned 186% cumulatively compared to the S&P 1000’s Total Return performance of 59%. On an annualized basis, that’s 32.3% and 13.3% respectively.

The second interview is with Peter Rabover, the Portfolio Manager of Artko Capital LP.

According to Peter, he started Artko as part of a desire to create “an unindexable product investing in things that are overlooked by most of the market due to their size or liquidity and staying small and concentrated.” He’s looking for investments that have some sort of margin of safety, usually backed by assets or stable/recurring cash flows at low valuations and “additional free optionality.”

Since inception (Q2 2015) Artko has returned 13.6% annualized net of fees compared to 6.2% and 3.2% for the Russell 2000 Index and Russell Micro-Cap Index respectively.

At the end of this issue, there is also a table showcasing all of the stocks previously profiled in issues of Hidden Value Stocks. We hope you enjoy this issue of Hidden Value Stocks, and if you have any questions or comments, please feel free to contact us at [email protected]. Below is an excerpt Are you a smart person? who wants to learn more?

We for a special offer for being a loyal and sophisticated reader of ValueWalk.

Our 60+ picks since we have started the publication have returned an impressive 27.9% annualized – that is not a backtest and those gains could have been yours!

Want more ideas?

We have an exclusive 40% off coupon (our most ever)

Use code VIP20 at checkout or click here.

Limited time offer only expires 3/31/2030 or next 20 subscribers whichever comes first – please do not share this discount with others

*Return is calculated using every stock profiled on our site from time of publication and using a profit target of 100% and a trailing stop loss of 25%. Past results are not an indicator of future returns

Sincerely,

Rupert Hargreaves &

Jacob Wolinsky.

Update From Previous Issues

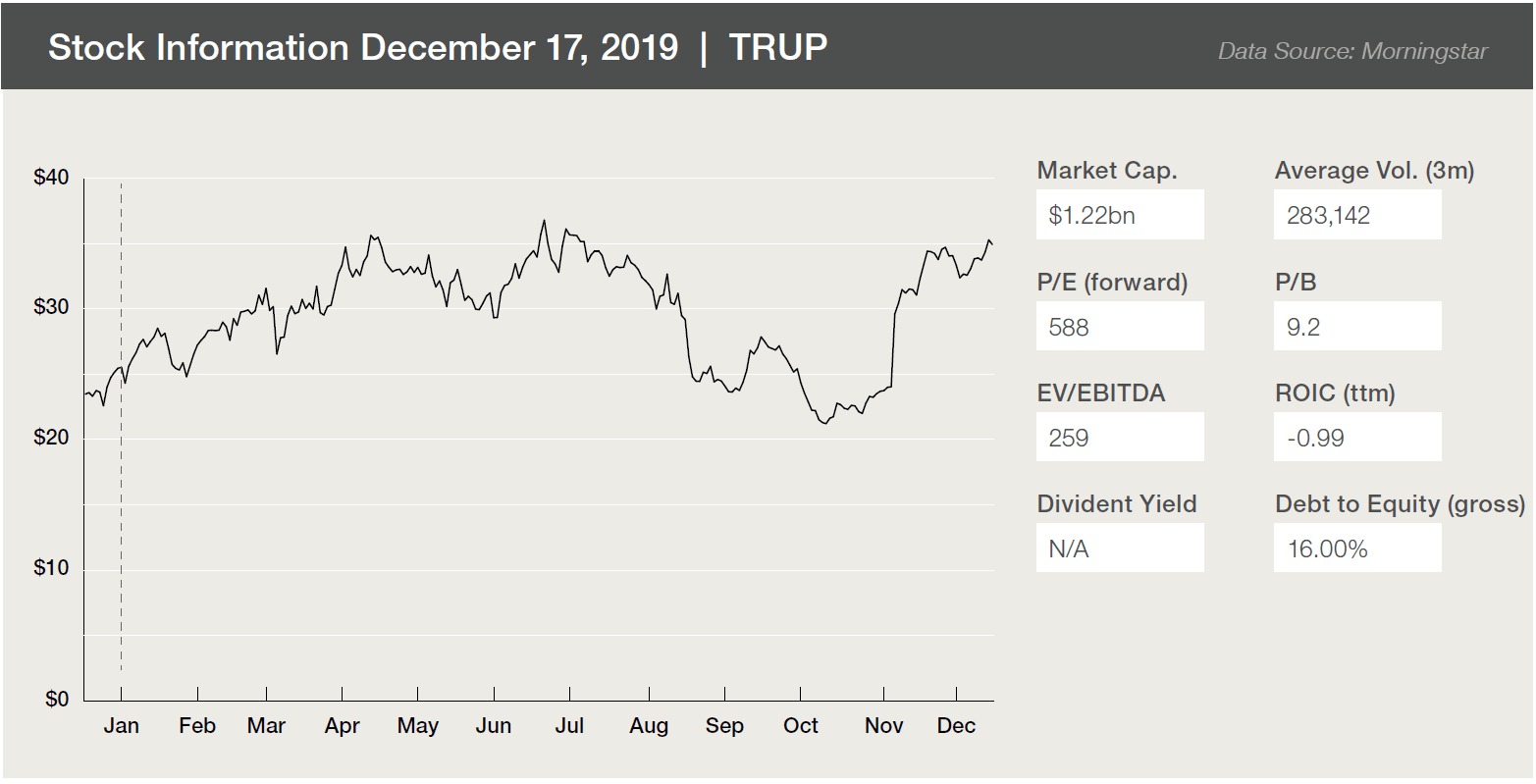

In the December 2018 issue of Hidden Value Stocks, Saga Partners highlighted Trupanion as one of its two small-cap stock picks. The fund is still feeling positive about the stock, as its Q2 2019 letter to investors explained:

“Trupanion has several advantages. It benefits from providing the highest value pet insurance coverage for premiums charged, i.e. lowcost provider. It also has a large network of territory partners throughout the country who built relationships over multiple years with animal hospitals. It also has its point of sale software, Trupanion Express, which provides the ability to speed up claim payment and pay animal hospitals directly to veterinarians. On the surface, Trupanion’s financials may look unusual in that they have no GAAP earnings. This is because insurance premiums are priced at a 30% above expected claims expense, called Trupanion’s “pricing promise”. The average loss ratio for a specialty property insurer is 56% vs. Trupanion’s 70% target, hence the best value proposition relative to competitors.

Trupanion has been cash flow positive since 2016. After paying 70% of premiums received towards claims, Trupanion has 30% of premiums to pay all other operating costs. Once all nonmarketing operating costs are paid, Trupanion uses the remaining cash to reinvest in pet acquisitions costs to grow the business, resulting in essentially no GAAP earnings but very strong growth. Once Trupanion reaches scale at 650,000-750,000 insured pets, it expects to have ~15% adjusted operating margins at which point it will be very difficult for any competitor to offer a similar value proposition. Often growth and earnings are at odds with each other. As long as Trupanion is able to effectively reinvest capital at attractive incremental rates of return, it should invest as much available capital as possible. The lower the earnings today, the greater the growth in future cash flow, and therefore the higher intrinsic value.”

McIntyre Partnerships was also featured in the Q4 2018 issue of Hidden Value Stocks.

The firm initiated a new deep value position at the beginning of 2019, which it described in its Q2 letter to investors. Here’s a summary of the new position in Trinity Place Holdings. The full thesis can be found in the fund’s secondquarter letter to investors:

“Trinity Place Holdings (TPHS) is a relatively simple “workout”-esque security. The ~$4 stock has ~$2.50- $3.00 in easily valued investments and one large other bet: a new build residential construction in lower 4 Manhattan called 77 Greenwich that we believe will yield $3-$5+ in value by year end 2021, yielding a sum of the part (SOTP) of $5.50-$8.00, a 40-105% return in two years. The critical variable in TPHS’s NAV is what average sales per square foot (PSF) 77 Greenwich ultimately achieves. Our $3-$5+ estimate corresponds to a $2,000-$2,500 PSF sales price, which we believe is adequately conservative versus recent comparable sales in the area.

Construction of 77 Greenwich is already over 50% finished with completion scheduled for the second half of 2020. Marketing and sales commenced in Spring 2019 and are scheduled for completion in 2021. As the initial units are sold, we believe there is a possibility the market will see the relevant PSF marks for the asset and could reweight shares in advance of completion. We believe TPHS shares are an opportunity where we stand to lose little, if any, if our thesis is incorrect and stand to make a great deal if 77 Greenwich is sold in line with our projections. Further, we believe management will be good stewards of capital with the proceeds from 77 Greenwich.

Management and the board are large shareholders who plan to pursue buybacks, dividends, or purchases of other stable NYC residential real estate.”

Interview One: Samir Patel of Askeladden Capital

Why did you decide to start Askeladden Capital?

Samir Patel: While working as an analyst for a fund, I enjoyed the intellectual/analytical process of investing but realized I’m allergic to working for other people. Analytical work is mostly disintermediated from time and location: other than earnings reports, my job is basically reading stuff on the Internet and making good decisions based on the findings. So, it didn’t make sense for me to waste time (and give up flexibility) by commuting downtown and chaining myself to a desk five days a week.

My job made me sleep-deprived and miserable. Since the job I wanted didn’t seem to exist, I decided to create it myself.

You say your process is based on “making good decisions instead of perpetually seeking incremental data points.” Can you explain what this means?

Samir Patel: Here’s the philosophical underpinning of my process for both investing and life: people waste a lot of time doing nonsensical, pointless things that don’t make anyone better off. An easy source of “better returns” is to simply reallocate that wasted time to more productive endeavors.

For example, you’ll often hear people advise starting your day by making your bed.

I disagree. There has not been a single occasion in my life where making my bed resulted in any tangible (practical) or intangible (emotional/psychological) benefits for me… Unless you count not being yelled at by Mom.

On the contrary, making my bed has a welldefined opportunity cost: several minutes of time, which could be spent on something that will actually make my life better, like talking to a friend or watching a John Oliver clip.

How is this relevant to investing? As one of my professors used to say, all models are wrong, but some models are useful. If you want to be a good investor, you need a useful model – not a detailed one with hospital corners.

A stock’s current trading price implies a set of expectations about a company’s future results. If there’s a meaningful gap between marketimplied expectations and your analyticallyimplied expectations, then you have an opportunity. If you can consistently identify such opportunities, then you will likely achieve strong results over time – perhaps not in any given year or on any given situation, but over the long term, over a large enough sample size of portfolio positions.

I strongly believe in the Pareto principle (the 80/20 rule), insofar as I think that a few inputs usually have a disproportionate impact on outputs. Charlie Munger mentions, for example, that a few dozen mental models carry most of the freight in allowing you to understand how the world works. In the business world, I think that three fundamental metrics really drive intrinsic value creation (or destruction): revenue growth, margins, and capital allocation.

Amidst an overwhelming number of data points, if you broadly get those three items right, then everything else is less relevant – when was the last time the exact balance of accounts receivable over the previous seven quarters made or broke an investment thesis? The answer is never. Oftentimes, directionally correct assumptions about a few key metrics obviate the need for building a DCF, although a rough model can sometimes be a useful tool.

In turn, to have useful ideas about those three value creation KPIs, you have to think about the underlying business drivers – elements such as customer value proposition, relevant secular trends, industry dynamics, company strategy and positioning, and so on. These drivers do not tend to fit neatly into an Excel spreadsheet, but they are often understandable via qualitative analysis of publicly available information.

Our process, therefore, eschews the precise and comprehensive near-term quantitative modeling practiced by much of the industry. We feel that if your process revolves around building such models, then you spend most of your time seeking incremental (but not useful) data points to fill out those models, rather than trying to deeply understand the key drivers of the business.

So we focus on trying to be business analysts rather than investment analysts. Many of our research memos exceed 30 pages, but usually, no more than a few pages discuss valuation and modeling. Compelling value investments rarely require detailed modeling.

Our process also heavily emphasizes differentiating between the knowable and the unknowable. Think of these two dimensions (knowable/not and useful/not) in a two-by-two matrix. We try to focus on obtaining useful information, but we also need to consider that just because it might be useful to know something, does not mean that it can actually be known.

As such, we are willing to forecast aggressively on angles we consider knowable if we have the research to back it up. Conversely, we’re extremely cautious on angles which we consider unknowable, as we believe research can’t shed much light on these issues. We’re also focused on information that is long-term: even if short-term information (such as nearterm earnings momentum) is useful, it’s like a rose you get from a florist: it wilts quickly.

We prefer planting rose bushes, i.e. developing intellectual property that is valuable for many years rather than just a few weeks or months.

Ultimately, we believe that smart decisions trump hard work. You can work very hard collecting lots of information; most analysts at most funds work very hard (the finance industry is not known for its nap pods and free massages). But, clearly, based on industry-wide performance, this hard work is not actually translating into value creation for clients.

So instead of simply collecting more data, we care more about making the right decisions on two levels – first, the right decisions in terms of what data might be useful to collect, and second, the right investment decisions based on whatever useful data we collect.

Our watchlist allows us to engage in this process objectively, over time. In many cases, we build up a nuanced understanding of companies over many quarters or years before ever taking a position, with the opportunity in the interim to assess whether or not our expectations were reasonable. This doesn’t guarantee success (we’ll discuss a notable failure later), but on average, we think it leads to better results than ad-hoc idea generation without context. We analyze the business without prejudice and wait for the valuation to come to us.

To bring this back to where we started, we believe our competitive advantage (setting aside our small/micro focus and intentionally constrained capacity) is recognizing that bed-making is an aesthetically impressive but ultimately pointless exercise. We focus our time on things that we believe create value – not things that look good, or things that you’re “supposed” to do.

So which qualities are you seeking in a potential investment?

Samir Patel: Setting aside valuation (which we will address below), quality factors that tend to be important to us include low or no leverage (i.e. <=2x net debt to EBITDA), strong customer value propositions, strong competitive positioning, meaningful growth opportunities, high margins (both gross and EBITDA), strong returns on capital (or capital-light businesses that do not need meaningful capex to grow), a reasonable capital allocation framework, and recurring / non-discretionary demand.

Obviously, it’s rare to find all of these factors in a single investment, but the more factors checked off, the more likely we’ll like it. Alternatively, the more red flags, the less likely we’ll like it.

How do you determine if the company has the potential to hit your returns target (20% compounded annual returns over a three-year investment horizon)? Could you guide us through your process?

Samir Patel: Our process contains elements of both the trending quality-focused “compounders” investing, and classic low-multiple value investing.

On the one hand, we’re simply not comfortable paying extremely high multiples based on rose-colored glasses forecasts. We believe that over time about half of our returns will come from multiple rerating, so we’re very focused on buying companies that trade at low multiples – our new positions typically have high single-digit – and in some cases double-digit – cash flow yields. This can occur on an actual basis, or on a “steadystate” basis if these companies are reinvesting substantial portions of cash flow in attractive growth opportunities such as customer acquisition or footprint expansion.

On the other hand, we’ve had very bad results with “dumpster diving” situations. For example, when dealing with cigar butts, time is your enemy, not your friend. If you buy a pile of assets that isn’t compounding value, time substantially erodes IRR. You can sit on the assets for a long time and earn nothing.

Conversely, for quality assets, your IRR will still erode with time, but much less. If you underwrite correctly, the positive carry of cash flow and growth will allow you to earn a high single to double-digit return even in the absence of multiple rerating.

Our valuation process is extremely simple: we use a 10% equity discount rate and underwrite conservative assumptions. Sometimes this involves a DCF; more frequently, however, it involves back of a napkin math on a fair EV/NOPAT or P/B multiple, making some straightforward assumptions about returns and growth.

This is perhaps easiest to understand via inversion: while reasonable people could quibble over whether a certain company is worth 15x or 18x its earnings, it’s difficult to credibly argue that a good-to-great business with a clean balance sheet and GDP+ growth prospects over the long term is worth 10 to 12x its free cash flow.

Those are the sorts of obvious opportunities we like. We typically like to buy things for <10 to ~16x EV/NOPAT that we think are worth 14 – 20x+ EV/NOPAT.

We evaluate all stocks on the basis of their three-year CAGR; i.e., if we bought it today at the current market price and it traded at fair value in three years, including the value of cash flow and growth generated during that period, what CAGR would we earn over our holding period?

We typically require a minimum hurdle of 20% per annum, which essentially equates to requiring a 20-25% minimum discount to fair value at the time of purchase.

We are always looking to optimize our portfolio-wide CAGR, with the caveat that this number is not the end-all-be-all determinant of what goes in our portfolio. We have topdown “risk buckets” and even without them, we might prefer a lower-CAGR investment with fewer risk characteristics (such as cyclicality and leverage) to a higher-CAGR investment.

We have substantially exceeded our 20% threshold since inception, but the environment has been unusually favorable, and we’re focused on continuing to expand our watchlist, and improve and execute our process, to maximize our chances of continuing to meet this goal over the long term.

One stock you’ve owned for a few years now is Franklin Covey (FC). Can you go into detail about how this investment was initiated?

Samir Patel: I met Franklin Covey’s CFO, Steve Young in 2014-2015, pre-Askeladden, on a non-deal roadshow. Franklin Covey is a corporatelearning company. Their mission is to enable greatness; their value proposition is creating significant and lasting change in human behavior, at scale, to address clients’ most intractable performance challenges.

In order to prepare myself properly, I read Stephen Covey’s The 7 Habits of Highly Effective People, one of Franklin Covey’s landmark content offerings. The power and truth of the lessons resonated deeply with me. Steve and I had a very interesting (albeit nontraditional) investor meeting.

My watchlist process is predicated on following companies over time, so I continued to check in. In spring 2016, Franklin Covey’s stock price fell significantly after an earnings report that wasn’t bad, and I ended up taking a position. I believe the company has been a continuously-held portfolio position since that time, although position size has varied dramatically, from low-mid single digit all the way up to 35%+ of the portfolio.

What appealed to you in terms of the firm’s operational ability and growth prospects?

Samir Patel: First and most fundamentally, I care about the customer value proposition, because it drives many important business phenomena. If you provide compelling value to your customers, you are not only less likely to be displaced by competitors, but you are more likely to retain and/or grow your business with existing customers over time. There are various ways to measure this, such as net promoter score, or customer ROI.

Prior to 2016, “legacy” Franklin Covey typically provided courses for $200 per person. Let’s do grade-school math: that’s 0.4% (40 basis points) of a hypothetical $50,000 average employee salary. So for Franklin Covey to deliver a 3-5x ROI on customer spend, it only has to make the average employee 1 or 2% better at their job. 7 Habits has made me way more than 1 or 2% better at my job.

The value proposition became even more superlative when Franklin Covey transitioned from selling discrete individual courses to, for the same $200 price, offering an “All Access Pass” annual subscription with access to all of the company’s content catalog. It’s analogous to a Six Flags season pass.

The corporate learning industry is large (multibillion-dollar revenue TAM) and fragmented (most vendors offer only a single course, provided in a single modality.) Although “legacy” Franklin Covey already had a strong competitive value proposition, All Access Pass changed the basis for competition in the industry.

Now, instead of evaluating companies head-to-head on a single course, customers evaluate the AAP value proposition vs. singlecourse offerings (at the same price) from other vendors. Few competitors have the depth and breadth of content to match Franklin Covey’s AAP offering.

This compelling value proposition has resulted in rapidly increasing customer demand – many new customers have signed up, and many existing customers have rolled out Franklin Covey solutions to more of their employee base and purchased additional services from Franklin Covey to accelerate the behavioral change.

Amidst all of this, I began to realize how powerful the subscription-based recurring revenue business model is. In the “legacy” model, a Franklin Covey sales rep would have to sell a certain number of courses one year, then sell them all again the next year, and then more still, to generate growth. In the “new” model, Franklin Covey not only typically retains 90%+ of the prior year revenue under annual contracts but is increasingly signing multiyear contracts that guarantee revenue will be retained over a 2-3+ year period.

This does two equally important things. First, it makes it far easier for the company to consistently sustain high-single to low-double-digit revenue growth. When you start the year with 90%+ of last year’s revenue in the bag, instead of 0%, it’s obviously much easier to drive growth.

Second, the track record of peers, whether in the same space (such as Skillsoft) or in different verticals (such as Gartner and CEB), demonstrates the resilience of the business model. While no company is entirely immune to severely challenging macro environments or occasional execution stumbles, recurring revenue business services companies tend to be able to hang onto much (or all) of their revenue and profitability even in the face of such issues and rebound quickly after any challenges.

Looking back, how has the idea played out? Did the company hit your growth target?

Samir Patel: Franklin Covey has successfully taken advantage of its strong business model and compelling value proposition to drive high-single-digit top-line growth, with the potential to accelerate that to double-digit growth over time. Their Adjusted EBITDA (plus change in deferred revenue less costs) and cash flow in 2020 will exceed where they were in their legacy business model despite extensive investments in the meanwhile.

More importantly, based on achievable, nonheroic assumptions, management expects 2022 free cash flow to be double that of 2019. While the growth rate will undoubtedly moderate over the longer-term, mid-teens growth in EBITDA/free cash flow seems likely to us for many years to come.

Looking back, is there anything you think you missed, and do you still like the stock today? If so, why?

Samir Patel: We almost missed most of the upside with Franklin Covey – I was almost out of the position at prices in the high teens and low $20s, compared to a price near $40 today, until I realized in 2017 how badly I was underestimating what was about to happen. I subsequently loaded up.

For context, I am a value investor first and foremost, and a core tenet of my process is underwriting businesses conservatively. I encounter many idea pitches that envision blue-sky scenarios where the world never deals you a bad hand, where execution is always perfect, and all projects cost half as much and are completed twice as fast as budget.

This is the opposite of our approach. As such, I was uncomfortable with underwriting high growth rates or substantial margin expansion. There is certainly a rationale to this, as the “base rate” of companies achieving targeted growth and margin expansion is generally not great, and few companies can sustain doubledigit growth and margin expansion over long periods of time.

It is certainly possible to construct a sample of such “compounders” ex post facto, but this suffers from a severe selection bias: ten years ago, it may not have been obvious that many of those companies would go on to have such ten-year runs. Similarly, there are many more companies that people predict will perform to such a high standard than, in fact, meet that standard over time.

All of that said, studying Franklin Covey and its peers helped me realize that you can’t apply the same analytical model to a recurring revenue business as you can to a one-off discretionary demand business.

If you think about selling something like a car or a refrigerator, an inherent challenge is that every time you make a sale, you’re removing a customer from the market for a long period

{kind=link}