Ruffer Investment Company investment manager’s period end review for the period ended December 31, 2020.

Q4 2020 hedge fund letters, conferences and more

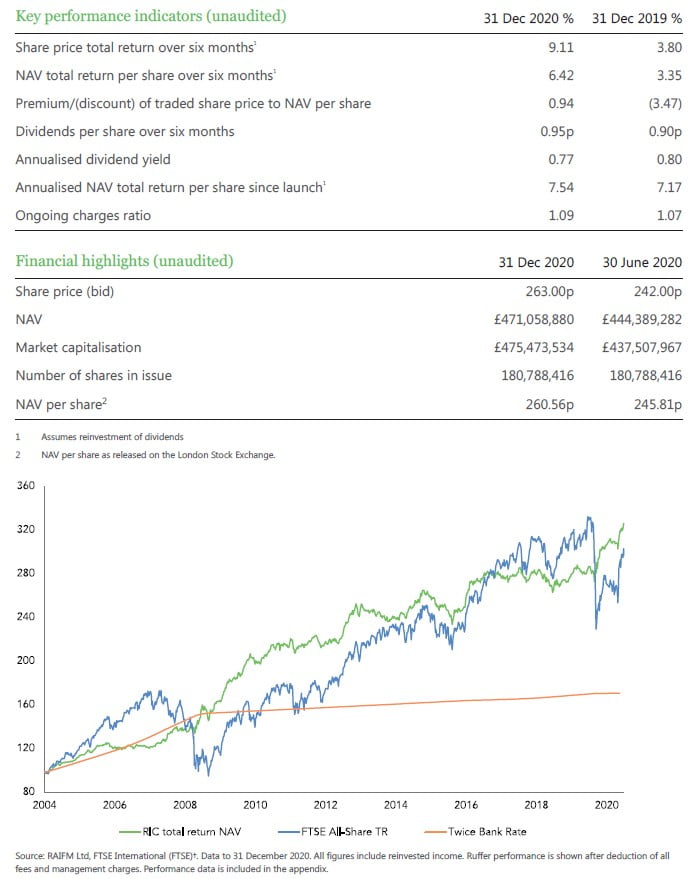

Ruffer Investment Company posted a NAV return of 13.5% and a Share Price return of 17% for 2020. However, just as importantly, at the peak of the crisis in March we were not losing money. Given the unique blow to the economy and the co-ordinated shock-and-awe global response, it seems fair to conclude that the distribution of possible outcomes from here is wider than it has ever been. This makes a genuinely all-weather portfolio even more important.

Performance review

The share price return of 17.0% and the NAV return of 13.5% for the calendar year 2020 marks two consecutive years of good returns for shareholders (+23% in NAV performance over 2019 and 2020) following a lean period in the two years before that. For the six months to 31 December 2020 the NAV return was 6.4%.

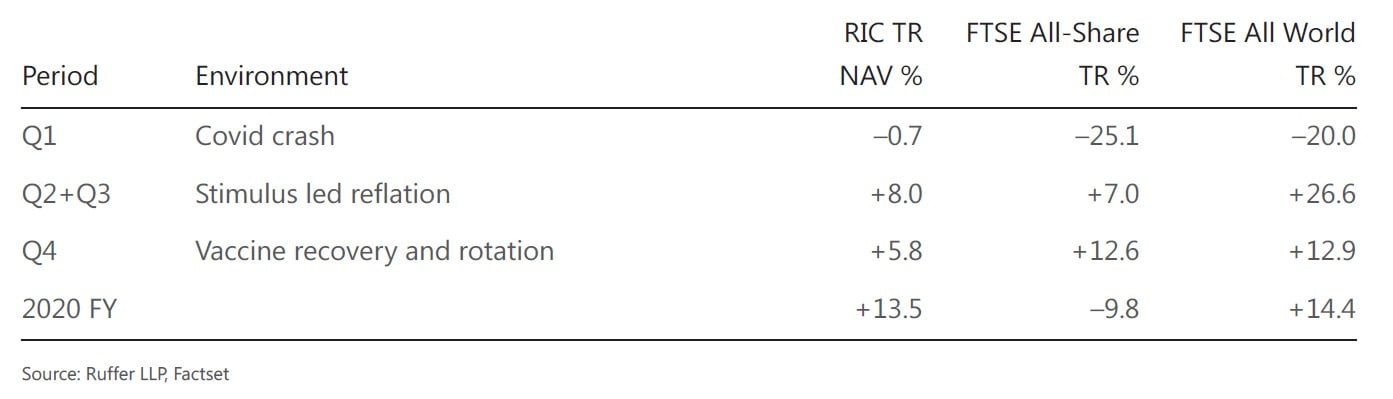

What most people will find surprising about 2020 is that through a severe global recession, most assets ended up making money. This is hard to reconcile with the lived experience of 2020. Despite the rise in asset prices, the portfolio objective of preserving shareholder capital was thoroughly tested as we experienced the broadest possible range of market and economic environments. We often describe the Ruffer investment approach as ‘all-weather’ and there was certainly a wide variety of investment weather to deal with.

There were three distinct phases of market behaviour, each of which required a different asset mix to navigate successfully.

To illustrate this another way the portfolio appreciated by 4.2% in March when equities fell 15.1% and also appreciated by 5.2% in November which was the best month for equities since 1987.

Portfolio attribution

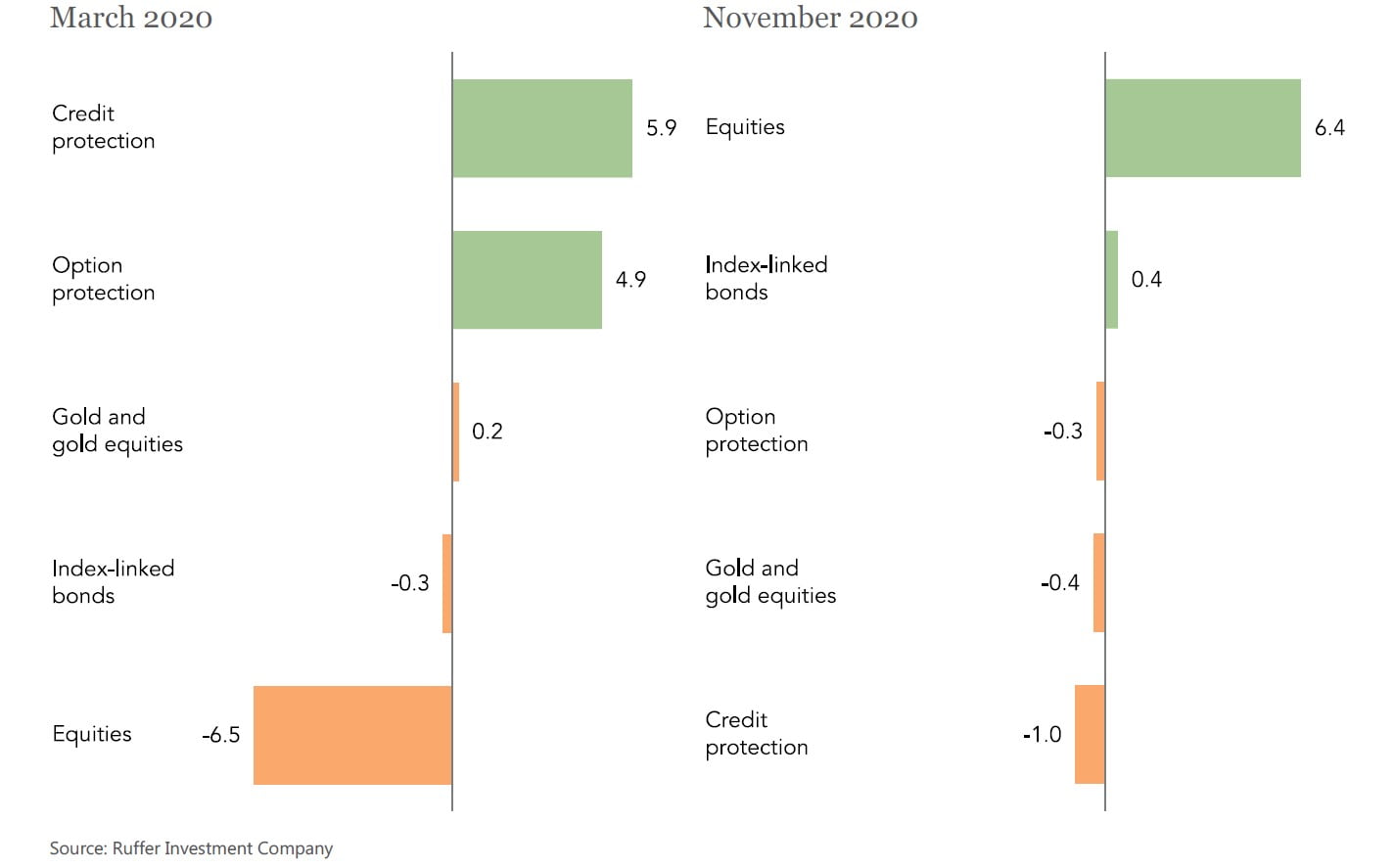

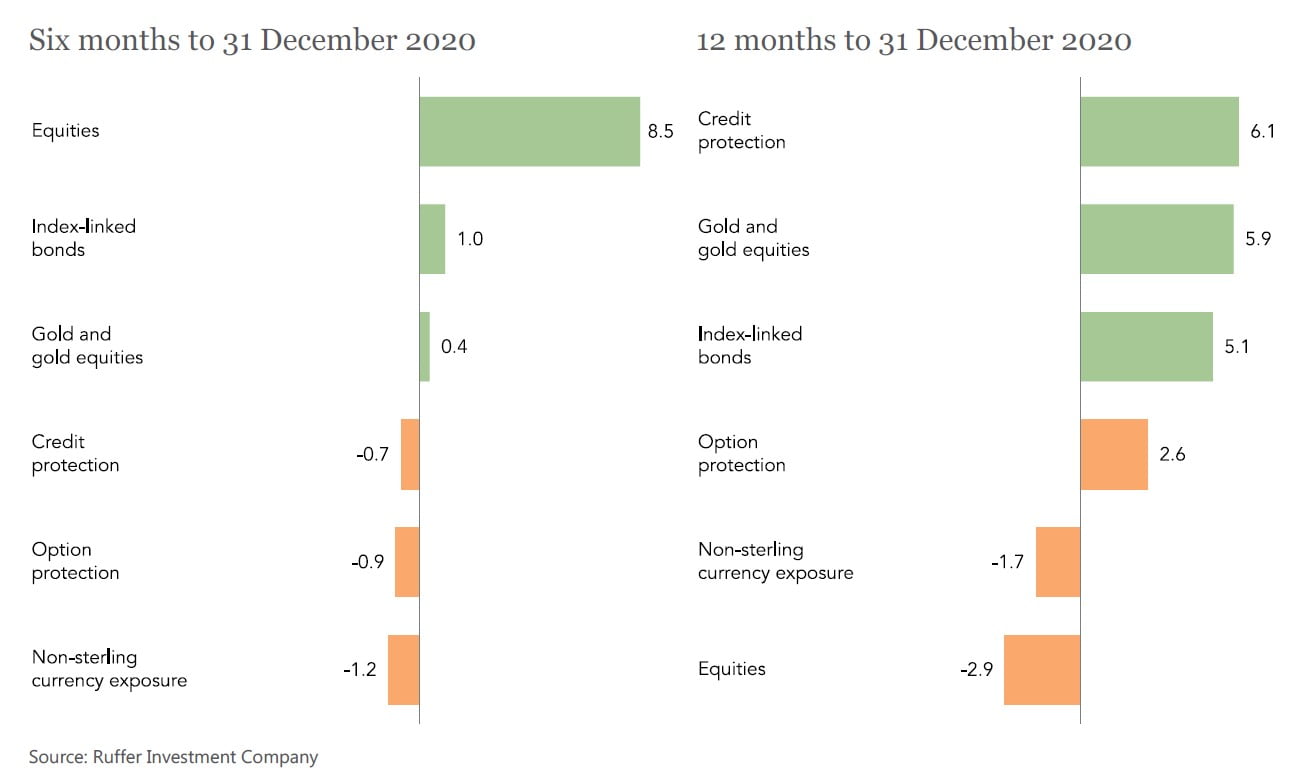

Attribution for the year 2020 tells only part of the story. What was important was not just what you owned, but when you owned it.

In order to hold onto the major positive contributions from gold, credit protection, US Treasury Inflation Protected Securities (TIPS) and option protection, we needed to add opportunistically and lock in gains at various points during the year. Similarly, while we lost money in equities over the year as a whole (too much cyclical exposure in Q1), timely additions in the middle of the year and a further rotation into cyclical stocks meant that this part of the portfolio performed strongly in the bounce in markets and vaccine announcement in November.

Within the equity book the standout stock has continued to be Ocado, rising 79% in 2020, 13% since 30 June and 774% since purchase. Three other notable successes were Fujitsu (+45% in 2020, +82% since purchase), Sony (+39% in 2020 and +271% since purchase) and Weiss Korea (+57% in 2020 and +138% since purchase).

Having been a drag in the first half of 2020 our positions in cyclical and value stocks were justified in the second half of the year as they acted as an offset to long duration assets and covid winners (gold and long dated index-linked bonds for us, technology and growth stock for many others). Stocks exposed to a ‘v for vaccine’ recovery have done well since purchase – notable contributions came from Cemex (+98%), Uber (+44%), Barratt Development (+42%) and Vinci (+42%). At the very end of the period under review the announcement of a post-Brexit trade deal benefited our position in domestic UK equities and the decision to add to this part of the portfolio in October. The reaction was more muted than we expected, but as the covid clouds start to clear we expect the discount on UK equities to narrow.

Portfolio changes

There was some profit taking in gold and trading in US TIPS as mentioned above and the equity weighting rose from c30% to c40%. As we reported in July, a portfolio of index-linked bonds, gold and cyclical/value stocks (which benefit from stimulated GDP growth) and a significant sprinkling of protection against market calamity looks to be the right mix for the current environment.

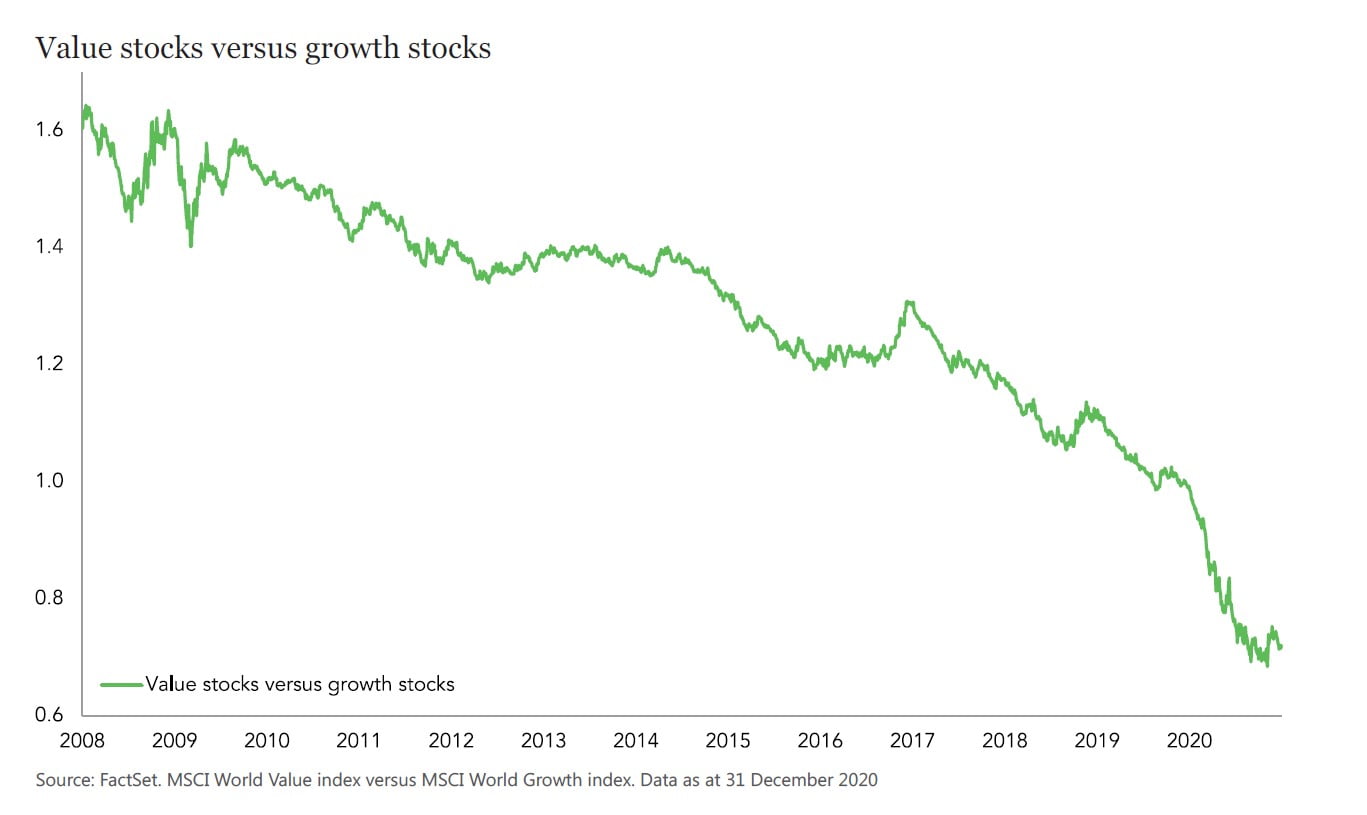

Although our cyclical/value stocks were strong immediately following the vaccine news, we must remember both the portfolio role they play and the longer-term context. These stocks are geared to improving economic prospects and rising interest rates – this is vital as the rest of the portfolio stands to benefit more from continued financial repression and poorer market and economic outcomes. Secondly, as the chart below shows, these types of stocks have underperformed growth and quality factors for a decade. If there is an extended rotation, which would rely upon improved economic growth, then the recent outperformance has much further to run.

One notable addition to the portfolio during November was bitcoin exposure. We gained our bitcoin exposure via the Ruffer Multi Strategies Fund and two proxy equities in Microstrategy and Galaxy Digital. At the period end the combined exposure of these was just over 3%. In the short period since investing both stocks are up more than 100% and bitcoin is up 90%. Our rationale has been well publicised but briefly, we have a history of using unconventional protections in our portfolio. This is another example, a small allocation to an idiosyncratic asset class which we think brings something significantly different to the portfolio. Due to zero interest rates the investment world is desperate for new safe-havens and uncorrelated assets. We think we are relatively early to this, at the foothills of a long trend of institutional adoption and financialisation of bitcoin. Think of bitcoin’s bad reputation as a risk premium – as we move through the process of normalisation, regulation, and institutionalisation, the compression of this premium can have a dramatic effect on the price. If we are wrong, bitcoin will return to the shadows and we will lose money – this explains why we have kept the position size small but meaningful.

Investment outlook

As we enter 2021 there is near consensus in financial markets on four things –

- Covid-19 will be conquered by the vaccine

- Central banks will keep printing money without limit

- Governments will keep spending without limit

- Valuations no longer matter because the winners and losers have been settled

But coming into 2020 there was near universal consensus that global growth would accelerate. The one thing that mattered in 2020, coronavirus, was on few people’s radar. Most did not see it coming and markets were complacent to the risk. As Daniel Kahneman put it: “the correct lesson to learn from surprises is that the world is surprising”. Given the unique blow to the economy and the co-ordinated shock-and-awe global response, it seems fair to conclude that the distribution of possible outcomes from here is wider than it has ever been. This makes a genuinely all-weather portfolio even more important.

The economy

It now seems we are in a K-shaped recovery – that means winners and losers. The unique shape of the covid crisis and accompanying recession has meant some industries have thrived whilst others have suffered. What does the K mean? In caricature, everyone now uses Zoom and Peloton and offices and gyms are forced to close. Big beats small. The digital economy beats everything. Covid-19 acted as the Great Accelerator to a whole host of trends which were already in motion. This applies to individuals as much as it does to companies. The rich have benefited from asset prices rising, access to cheap debt and more independence. Those less fortunate have faced job losses and managing precariously through a patchwork of government support.

Read the full commentary here.