RGA Investment Advisors commentary for the first quarter ended March 2021, titled, “Growth vs Value.”

Q1 2021 hedge fund letters, conferences and more

Highly Levered Hedge Funds

The story of the Q1’ 2021 in many respects centered around the positioning of highly levered hedge funds. In January, prominent hedge fund Melvin Capital experienced significant losses when GameStop and several other highly shorted stocks went parabolic. In March, Bill Hwang’s family office, Archegos, blew up long several highly shorted names and left its prime brokers holding the proverbial bag. In both cases, the funds in question deployed considerable leverage (suspected to be in the range of 8:1 dollars of invested capital to net asset value). The leverage combined with operating at scale meant these funds could not quickly exit their troubled positions and, in the process, wreaked havoc on markets.

Typically, other fund travails would not warrant inclusion in these letters, but for the fact these funds had large positions across the market and markets themselves experienced whiplashing moves as a consequence. We take solace that our investment process does not rely on leverage. In the cases of both Melvin and Archegos alike, the managers were operating strategies that were designed to exchange beta risk for basis risk. Beta risk in stock market parlance is the risk of the S&P itself, whereas basis risk is the relative risk between two assets that are paired against one another. More specifically, each of these funds had a long book where they would try to remove market risk to some degree (and the extent to which is seen in their “net exposure”), via an offsetting short book. The return of the portfolio is thus a function of the spread between the long book and short book’s returns. In structuring a portfolio this way, hedge funds (and this is where the name “hedge fund” originated) can theoretically deliver lower volatility (by hedging out market risk) and higher returns (with leverage) to more purely express stock selection skill.

We appreciate the abilities of many friends and colleagues to actively manage high gross, low net exposures, though that is not what we at RGA Investment Advisors do. We embrace market risk. We accept that at some points along the way our portfolio will face drawdowns alongside the market (and at times independently of the market) and that we aim to realize our return both from harvesting beta and delivering alpha by virtue of deep analysis and higher concentration than indices alone can afford. In our last letter, we specifically outlined our stock selection recipe and think it helpful to share some key pillars of our portfolio management process here.

- Semi-concentration, with outright concentration an outcome of success and time. Semi concentration is a reflection of both our conviction and humility.

- Stratified risks of portfolio positions-as little overlap in revenue drivers and risk factors as possible. This helps ensure that no one force can destroy our portfolio.

- Understand factors the portfolio is exposed to and how flows are driving returns of each factor. This helps reduce the path dependency of our portfolio and helps ensure that in all market environments, there is at least some portion of our book that’s “working.”

- No portfolio level leverage (as distinct from securities with embedded leverage).

Growth vs Value

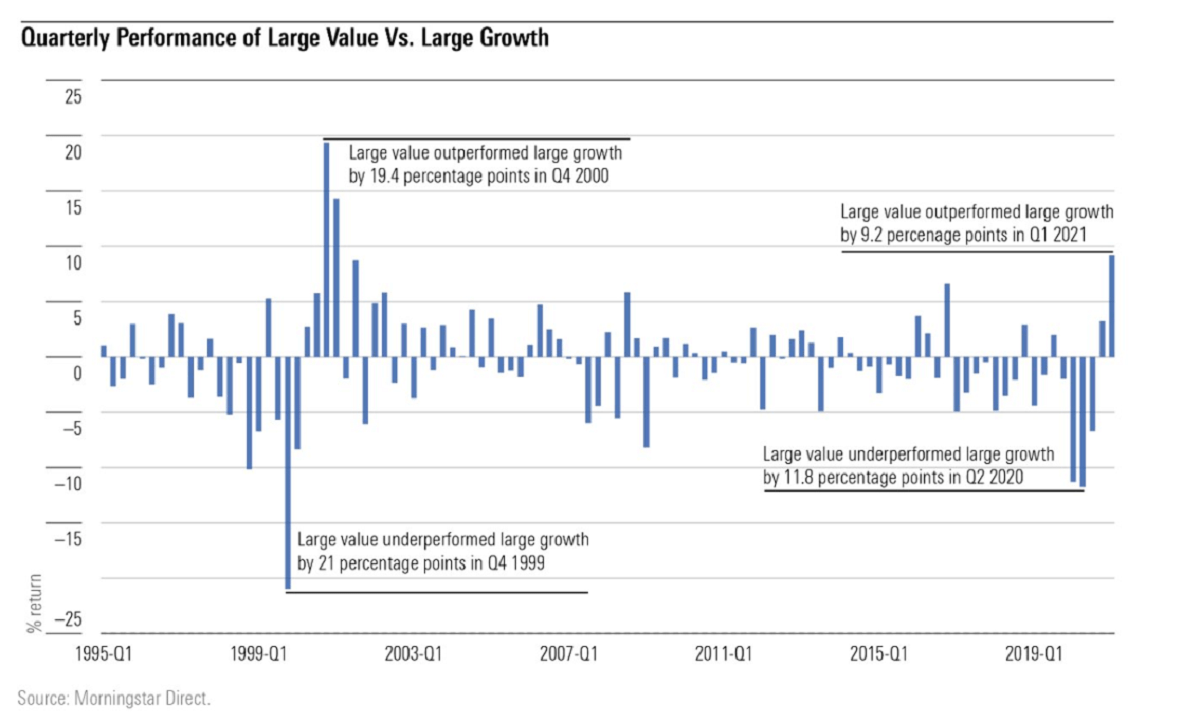

In aggregate, this action is healthy for markets as it wrings out leverage and encourages brokers and portfolio managers alike to question their underwriting assumptions, pare down leverage and operate with discipline. One of the more interesting consequences is that the reigning in of leverage across markets led to the strongest outperformance of the “value” factor over the “growth” factor in over two decades (per Morningstar data):

This has led to questions like “will 2021 be the year for value stocks.”[1] We find the industry’s obsession with growth vs value interesting to think about philosophically but ultimately somewhat misguided. The morality with which some tried-and-true value investors approach the question about the inevitability of value’s eventual outperformance strikes us as an unwillingness to reflect on the essence of value investing itself. We like drawing analogies between baseball and investing. We imagine most people have heard of Moneyball: The Art if Winning an Unfair Game by now, considering it was released as a Hollywood movie. Popular culture still uses “to Moneyball” as a verb of sorts to describe the phenomenon of 1) deploying advanced statistical analysis in an effort to 2) identify which players or assets are undervalued. We put those numbers in place, because often people conflate these two points and because each has unique new realities in a post-Moneyball world. Identifying undervalued assets is the goal of value and growth investors alike, though value investors analysis tends to start with cheapness and growth investors begins with analyzing the growth.

A little over a year ago, Elliot facetiously tweeted out this is the “Best explanation I’ve seen yet for why growth continues to outperform value” with an excerpt from a book entitled The MVP Machine: How Baseball’s New Nonconformists are Using Data to Build Better Players by Ben Lindbergh and Travis Sawchik.[2][3] The book is fascinating for baseball and non-baseball fans alike in how it evolves the lessons of Moneyball. In the excerpt is an assertion from Billy Beane that “The old days of getting something for nothing are over. There are too many good [GMs} out there now.”[4] This quote is essentially the story of markets becoming increasingly efficient and is one we commonly hear from our peers in active investment management, especially those who describe themselves as more traditional value investors focused on low multiples. A further quote within the excerpt hits at the heart of the issue in baseball’s eroding analytical edge for Moneyball analysts:

Much of the drama in Moneyball’s narrative arises from transactions: picking players in the amateur draft, trading for undervalued relievers, and signing the unsung Scott Hatteberg, whose patience at the plate went underappreciated at a time when runs batted in and batting average still reigned as the game’s most prized offensive indicators. As Moneyball portrayed it, Oakland’s ability to compete despite noncompetitive payrolls was about being better at acquiring players. “You can identify value or you can create value,” says former San Diego Padres senior quantitative analyst Chris Long….Ideally you’d do both, but Oakland’s cutting-edge efforts were focused on the former….Apparently developing players wasn’t part of the art. [emphasis added]

There is an important point here that gets at exactly why ‘value the factor’ (purely the quantitative variety, heavily reliant on screening public data) has underperformed over the past decade despite its recent reprieve. The proliferation of smart people deploying increasingly accessible (read: drastically cheaper in price and increasingly digestible) data set of statistics to identify cheapness was purely transactional in nature, much like Moneyball itself. There is this oft-repeated myth that on one side of every transaction in financial markets is a winner and the other side a loser. This may be the case in some transactions, but it’s certainly not the case in the core essence transaction of financial markets—those situations where a company raises capital from an outside investor to fund growth, or what we call a “primary issuance.” In a world where every edge is transactional and outperformance merely results from “buying cheap” it is convenient to see the world in such zero sum terms, but convenient does not mean correct. We think too much of the debate of value vs growth is phrased in binary, zero sum terms, when the actuality of markets is building towards non-zero sum outcomes.

MVP Machine asserts the next frontier exists in deploying a growth mindset throughout an organization for players and teams to find angles for improvement, using advanced data and tools. Stated another way, whereas the edge in Moneyball is transactional in nature, the evolving edge in baseball goes to teams that are able to “create value” by helping their players reach their fullest potential.

This evolution is one that we have seen in Warren Buffett himself. It is not too dissimilar from Buffett’s retained earnings test whereby we are told to look for “historical evidence, or when appropriate, by a thoughtful analysis of the future” towards how a company turns a dollar of retained earnings into something worth more than “one dollar of market value…created for owners.”[5] In effect, it is the search for companies who have the opportunity to “create value” and the success of an investment results not in the transactional moment (ie the magnitude of the discount to “fair value”), but in the analysis and assessment of an ability to hold through a period of value creation by the company. This is fully captured in Buffett’s 1967 Letter to Partners (coincidentally illustrated with a baseball analogy):

…although I consider myself to be primarily in the quantitative school…, the really sensational ideas I have had over the years have been heavily weighted toward the qualitative side where I have had a ‘high-probability insight.’ This is what causes the cash register to really sing. However, it is an infrequent occurrence, as insights usually are, and, of course, no insight is required on the quantitative side – the figures should hit you over the head with a baseball bat. So the really big money tends to be made by investors who are right on qualitative decisions but, at least in my opinion, the more sure money tends to be made on the obvious quantitative decisions.[6]

One of our favorite sub-plots in Walter Isaacson’s brilliant biography of Steve Jobs was this idea of Jobs being a genius for how “he connected the humanities to technology.”[7] This is very similar to both identifying and creating value as expressed in the Chris Long quote in MVP Machine. In many respects, this is why we have long subscribed to a GARP (growth at a reasonable price) investment philosophy that adheres to both value and growth investing frameworks. It is why we refuse to believe there is “One True Way” to make money in markets and study people who have succeeded in deploying drastically different toolsets than our own. Inevitably, what it all means to us, is that to succeed in markets today you need to understand all the transactional elements while hunting for opportunities where the target company is in position to add value beyond what is presently anticipated by the market.

While we cannot per se “create value” in our holding companies like teams can do with players, we can pay attention to which companies have done this historically and which are best positioned to do this prospectively, all the while remaining disciplined on the price we are willing to pay for future value creation. In the end, we think far too much ink is spilled on growth vs value and contemplating which kinds of stocks based on today’s multiple should be doing better. The one thing we guarantee is there will be good (and bad) performers in both the growth and the value basket and one need not subscribe to either label to find opportunities. What distinctly does not work and will not work in the market is merely scraping for statistical cheapness and expecting outsized returns in perpetuity. If one wants truly great returns it requires both low starting multiples and high value creation over a long period of time.

Portfolio Update

“The bird has wings”—Twitter’s quarter started off somewhat ominously, with Twitter the worst performing stock in the S&P 500 following the January 6th insurrection and questions about the stickiness of the userbase after permanently suspending the account of President Trump.[8] By the end of the quarter, Twitter was one of the best performers in the index after exceptionally strong fourth quarter earnings and guidance for the year and an upbeat analyst day that highlighted a rapidly evolving product roadmap placing the timeline at the center of ephemeral (fleets), long form (Revue) and voice (Spaces). The improvements to the experience makes the platform more accessible and provides more opportunity to continue growing the userbase. Importantly, Twitter also embraced what we have been calling “creative empowerment” in previewing SuperFollows and a host of features designed to help content creators and contributors monetize their own audience on Twitter itself. These developments, alongside considerable progress on the advertising platform give us growing conviction that Twitter will deliver on its largely untapped opportunity—in other words, the value creation opportunity on top of the low multiple we were able to build our position at. Elliot spoke at length about these developments on Yet Another Value Podcast with Andrew Walker and The Business Brew with Bill Brewster, which we invite you to check out.[9] [10]

Thank you for your trust and confidence, and for selecting us to be your advisor of choice. Please call us directly to discuss this commentary in more detail – we are always happy to address any specific questions you may have. You can reach Jason or Elliot directly at 516-665-1945. Alternatively, we’ve included our direct dial numbers with our names, below.

Warm personal regards,

Jason Gilbert, CPA/PFS, CFF, CGMA

Managing Partner, President

O: (516) 665-1940

M: (917) 536-3066

@jasonmgilbert

Elliot Turner, CFA

Managing Partner, Chief Investment Officer

O: (516) 665-1942

M: (516) 729-5174

@elliotturn

[1] https://www.kiplinger.com/investing/602611/will-2021-be-the-year-for-value-stocks

[2] https://twitter.com/ElliotTurn/status/1143877437236948992

[3] https://www.amazon.com/MVP-Machine-Baseballs-Nonconformists-Players/dp/1541698940

[4] Lindbergh, Ben and Sawchik, Travis. The MVP Machine: How Baseball’s New Nonconformists are Using Data to Build Better Players. Page 14.

[5] https://www.berkshirehathaway.com/letters/1984.html

[6] https://www.valueinvestingworld.com/2015/03/warren-buffett-on-qualitative-and.html

[7] https://www.inc.com/magazine/201410/walter-isaacson/steve-jobs-biographer-inside-look-of-jobs-greatness.html

[8] https://www.bloomberg.com/news/articles/2021-01-21/twitter-s-trump-ban-puts-stock-at-rock-bottom-of-s-p-500

[9] https://www.youtube.com/watch?v=7O2rUc_4KfY

[10] https://podcasts.moiglobal.com/business-brew-s1e17/

Past performance is not necessarily indicative of future results. The views expressed above are those of RGA Investment Advisors LLC (RGA). These views are subject to change at any time based on market and other conditions, and RGA disclaims any responsibility to update such views. Past performance is no guarantee of future results. No forecasts can be guaranteed. These views may not be relied upon as investment advice. The investment process may change over time. The characteristics set forth above are intended as a general illustration of some of the criteria the team considers in selecting securities for the portfolio. Not all investments meet such criteria. In the event that a recommendation for the purchase or sale of any security is presented herein, RGA shall furnish to any person upon request a tabular presentation of: (i) The total number of shares or other units of the security held by RGA or its investment adviser representatives for its own account or for the account of officers, directors, trustees, partners or affiliates of RGA or for discretionary accounts of RGA or its investment adviser representatives, as maintained for clients. (ii) The price or price range at which the securities listed.

Article by RGA Investment Advisors