Qualivian Investment Partners commentary for the first quarter ended March 31, 2021.

Q1 2021 hedge fund letters, conferences and more

“Every multi-bagger journey is filled with the corpses of intelligent, articulate, and loud naysayers. You have to do the work, so you know when to buy. Do the work so you know when to sell. Do the work so you can hold. Do the work so you can stand alone.” – Ian Cassell

Overview

Qualivian Investment Partners is an investment partnership focused on long-only public equities. We own a concentrated portfolio of understandable companies (15 -25) with wide moats, long reinvestment runways, and outstanding capital allocation. We expect them to compound capital at a mid-teens rate and hold them for an extended period. We are seeking investors that are aligned with our long-term horizon. We do not short securities. We do not use leverage. We do not use derivatives. We are not macro investors. We believe that only a relatively small number of exceptional companies are worth investing in over the long term. Our investment process identifies and holds these companies.

Our formula:

Long-Term Orientation+ Long-Term Investors + Focused Portfolio + Quality Compounders = Maximizing Chance for Outperformance.

Our investors should understand how we invest so they make the right decision. We would encourage investors aligned with our long-term horizon and philosophy to contact Aamer Khan ([email protected]) at 617-970-9583 or Cyril Malak ([email protected]) at 617-977-6101.

The market in Q1 2021

The stock market in Q1 2021 was a bit crazy. It was characterized by:

- an initial outperformance of tech stocks,

- a rotation toward vaccine/reopening stocks,

- higher interest rates and inflation fears, and

- a sell-off of long duration equities, and a collapse of a highly levered family office which stoked fears of contagion in the financial system.

But then almost every quarter in these times is seldom perfect and sometimes crazy. To paraphrase a famous novelist, each perfect quarter is alike, but each crazy quarter is crazy in its own way.

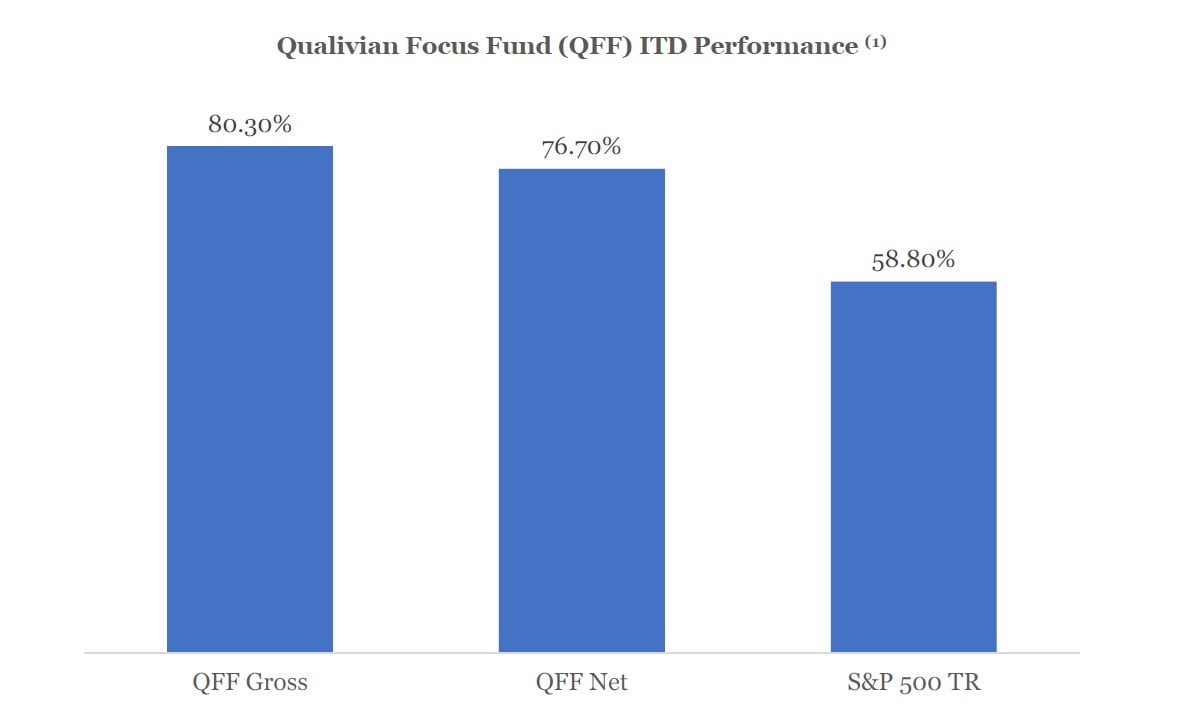

Qualivian Performance in Q1 2021

Since inception to end of Q1 2021, we have returned 80.3% and 76.7% on a gross and net basis respectively, outperforming the S&P 500 by 21.5% and 17.9% respectively.

In Q1 2021, we underperformed the S&P500 by 3.7% and 3.9% on a gross and net basis, respectively. We were negatively impacted by the rotation to more cyclical sectors in Q1 2021, like energy, financials, retailers, and travel and leisure. These sectors had weak earnings, had higher debt levels, and lower levels of profitability in 2020. As the pandemic receded, they had a strong bounce back in the last two quarters, as the market anticipated the recovery in their revenues and earnings power with the reopening of the US and global economies.

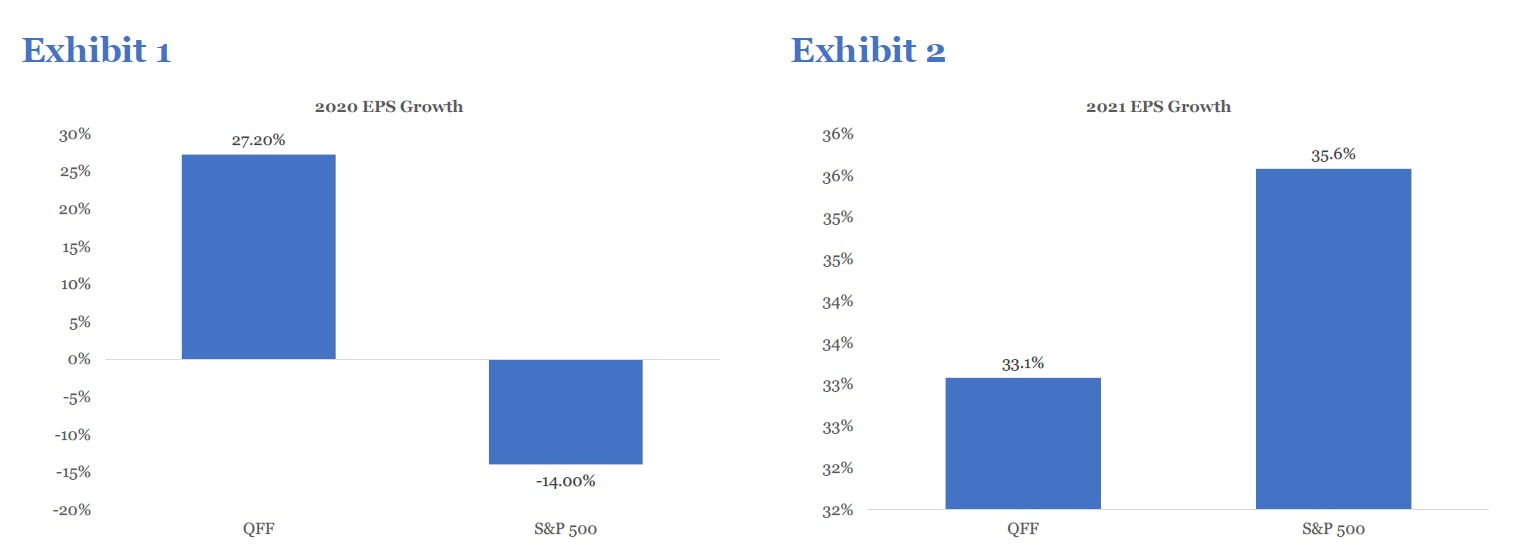

To illustrate this anticipated snapback of earnings in 2021 from 2020, exhibit 1 shows the EPS growth of the S&P 500 versus our portfolio in 2020, while exhibit 2 shows the estimated consensus EPS growth of the S&P 500 vs our portfolio in 2021.

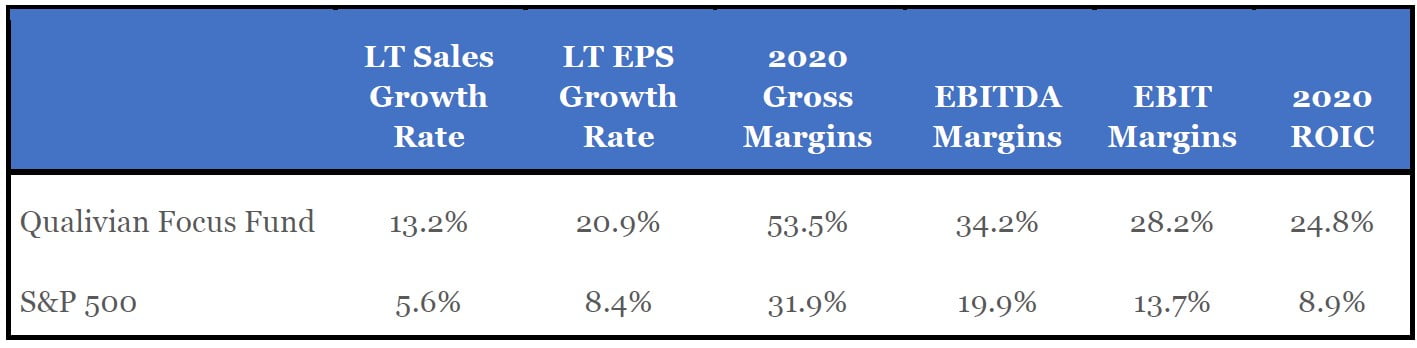

Relative earnings revisions drive relative performance over short time frames. However, the duration of growth and incremental change in ROIC drive relative performance over longer time periods and we focus on these characteristics. You can see how the Qualivian Focus Fund (QFF) compares to the S&P 500 on these characteristics in the chart below.

Tuning Out the Noise

As most long-term investors are aware, the price of long-term outperformance is short-term volatility and the ability to tolerate it without panic buying and selling.

This rotation in Q1 did not cause us to make reflexive changes out of our long-duration compounders into shorter-term cyclical high beta names, since we focus on earnings power over a five-year time frame. These five-year growth rates get affected much less than the one-year growth rates. We find that stock prices are more volatile than short-term earnings, which in turn are more volatile than long-term earnings. Focusing on long-term earnings enables us to tune out the noise.

Why We Avoid Market Cycles

Given our focus on buying and holding quality compounders we do not play cycles. To play cycles successfully requires:

- identifying the cycle correctly, which means separating the trend from the noise,

- timing the entry close to the beginning of the cycle, and

- timing the exit toward the end of the cycle.

Doing any one of the three is difficult. Doing all three sequentially is triply difficult. The odds would not be on our side even if it were our approach, and it is not. We prefer low degree of difficulty situations.

We find that performance results less from timing the entry or exit from a stock but rather in holding names that are quality compounders that we understand and are confident will be worth much more in five years.

Playing cycles is another version of market timing. Remember the adage: “time in the market beats timing the market.”

Portfolio Changes

The only change we made to the portfolio was that we purchased more Watsco (WSO). Watsco is a dominant HVAC distributor in a stable industry sector. It has a widening moat, a dominant and increasing market share, high returns on invested capital, a long reinvestment runway, and a founder-led mentality. We have discussed Watsco in two of our previous letters (Q2 2019 and Q3 2020).

The Impact of Higher Inflation on Long-Duration Assets

Quality compounders are long-duration assets. What is the impact of higher inflation on their valuation? Here is the standard argument:

- The value of an asset is the value of its unlevered cash flows discounted at its weighted average cost of capital (WACC).

- Higher inflation causes interest rates to increase.

- Higher interest rates lead to a higher discount rate.

- This reduces the value of the discounted cash flows.

- Hence, the value of the asset decreases.

However, the above argument neglects the following consideration:

- higher cost inflation can be countered by firms that can raise prices or cut costs to maintain gross margins,

- thereby increasing their cash flows in an inflationary environment,

- thus, offsetting the higher discount rate, and

- resulting in the value of the asset potentially not changing with the rise in rates.

The key here is the ability to maintain gross margins. The names we own, quality compounders, are names that have the ability to maintain margins because many of them are:

- Platforms.

- Oligopolies.

- High market share leaders with few substitutes.

- Have high gross margins to begin with and get minimally affected by cost inflation.

- Low capex to earnings which means that future investments (at higher cost due to inflation) will affect them minimally.

Our Overweighting in Founder-Led Businesses

A disproportionate number of our holdings are founder led. The equities of founder-led businesses tend to outperform those of non-founder-led businesses.

Bain research3 shows that founder-led firms are four to five times more likely to be top quartile performers in terms of shareholder value creation. An index of S&P 500 companies in which the founder is still engaged performed 3.1 times better than the others over the past 15 years.

Our own anecdotal observations are that non-founder-led businesses are more bureaucratic, overly risk averse, sclerotic in decision making, and often focused on size rather than returns.

A study by Bain & Company found that the reason for founder-led businesses outperformance came down to:

Founder-led businesses often have a special purpose and are often insurgents

They often, like Robin Hood (the mythical outlaw and not the trading site), fight industry behemoths on behalf of neglected customers. Netflix did this in video rentals. Or they identify a completely new niche or new market. Businesses often lose this sense of purpose as they age and grow. They become directionless. Employees become time servers or salary collectors. New ideas do not make it through the bureaucracy. These firms get out innovated and out competed.

They are front line obsessed

They are focused on the customer and not on rules, protocols, and career management of the middle and back office. Power has not shifted to an out of touch bureaucracy distant from the front line. There is unique instinctual and personal knowledge coded in the culture that cannot be reduced to procedures and handbooks. Founders can maintain this culture. Hired management often cannot.

An owner’s mindset

Founder-led businesses typically act quickly and take responsibility for risk taking and company results. Contrast the owner’s mindset with the hired manager’s mindset: they first mutate into custodians, and then into bureaucrats.

A Refresher on Concentration

We are believers in portfolio concentration. Occasionally, it is good to remind our investors as to why we believe this.

The data shows that active managers generate positive alpha when picking 10 stocks but have negative alpha when picking 100+ stocks. In fact, the data suggests that concentrated alpha is positive even after 2%/20% fees.

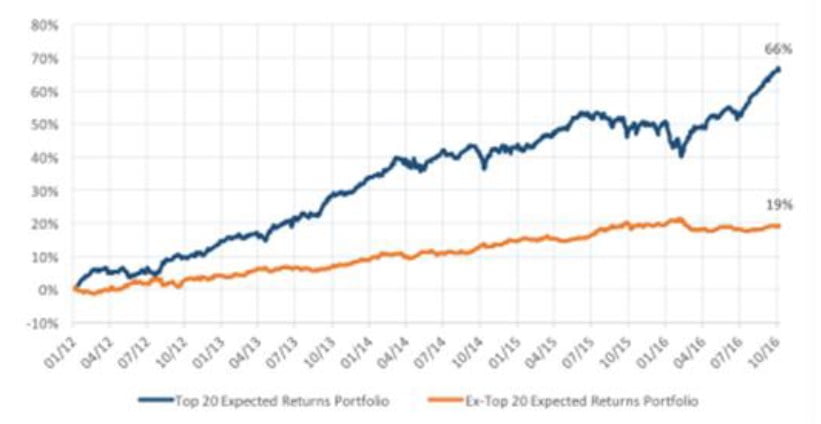

In a study by Alpha Theory,4 a Fund of Fund manager, they studied their asset managers’ funds and measured the returns of the 20 largest positions in the 60 or so funds (representing $70 billion in AUM) that they invested in, which they used as a proxy for their asset managers’ conviction levels. In the graph below, the top 20 positions generated returns that were 65% better than the rest of the portfolio (38% alpha versus 23% for the rest of the portfolio). The evidence shows that managers are good at stock selection on a small scale (20 positions).

Another way of determining clients’ expressed conviction level for different positions is by comparing their forecasted expected returns (Alpha Theory captures asset managers’ prospective probabilityweighted price targets). The 20 highest expected returns (longs and shorts) generated three times the returns with 66% compounded alpha versus 19% for the remainder of the portfolio.

Furthermore, Alpha Theory cites additional reasons when they reviewed the results and had discussions with their managers, citing the following reasons which we have also talked about in our previous investor letters:

Mental Capital

Each manager has a limited supply of mental capital to deploy. A stable of analysts does not mitigate this constraint because the portfolio manager is the ultimate arbiter of idea quality and must understand every investment idea completely to properly size them.

Great Ideas Are Hard to Find

Finding more than 30 positive expected return ideas is incredibly difficult because of widely available information and the number of very smart professional investors scouring that information. When the amount of time needed to find a good idea increases, then the number of good ideas found per measure of time decreases.

Investors Can Diversify on Their Own

Allocators do not need an individual fund’s diversification and low volatility because they get it by investing in multiple funds.

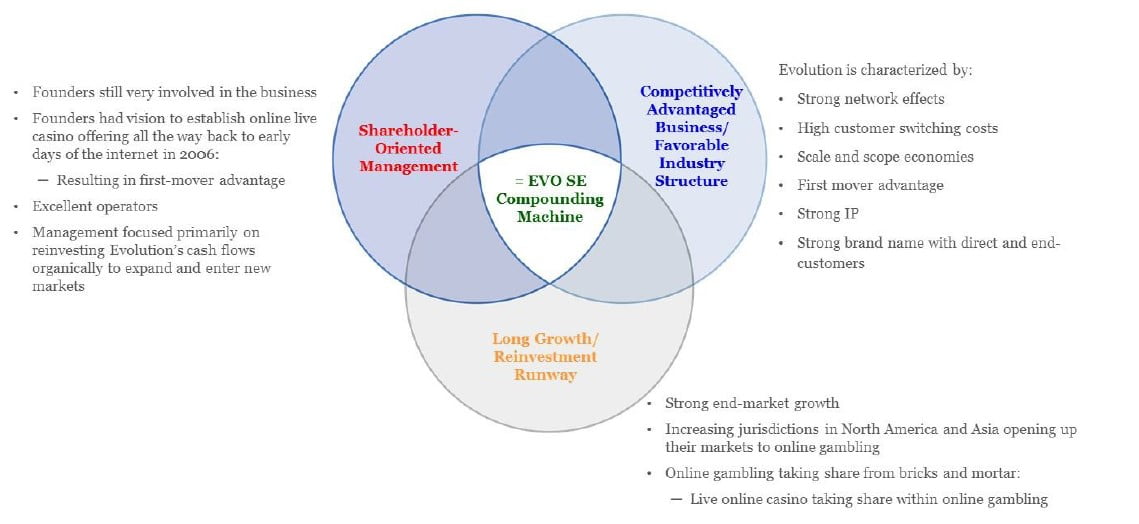

Evolution (EVO SE)

We are primarily focused on US stocks. However, we can hold up to 20% of our portfolio in non-US stocks. When we find an especially attractive quality compounder outside the US, we consider it. Evolution is one such stock.

Evolution is a Sweden-based leading B2B supplier of online live casino games and solutions to the gambling industry. It is the market leader with 60-70% market share in Europe, and single digit market shares in Asia, and North America. Land-based casinos hire Evolution to run their online live casinos and their lottery operations.

The Most Important Message

Evolution is a rare combination of:

- a wide and deepening moat,

- strong market growth for the foreseeable future,

- attractive economics, and

- a reasonable valuation.

A Wide and Deepening Moat

First Mover Advantage

Evolution has a first mover advantage in that it has developed well regarded editions of online live casino games like roulette, blackjack, and baccarat. It has also developed new casino games and live game shows. These offerings require live casino studios in several different jurisdictions, operate in different languages, and have cleared the onerous regulatory process for casinos and slots. A new competitor would have to make a significant investment in studios across different markets, must have better standard games (roulette, baccarat, and blackjack), and have superior proprietary games and game shows. It would have a much smaller customer base over which to spread these fixed costs. It would have no guarantee that its offering would find traction with land-based casinos which may not want to experiment with a new provider until it was firmly established.

Cuckoo Bird Effect

Evolution gets a percentage of revenue generated by its games and shows (around 10%). As land-based casinos spend on marketing and acquire new customers, Evolution’s revenue growth benefits from their investment, without having to spend its own resources. This is what cuckoo birds do, by planting their eggs in other bird’s nests.

Brand

Despite being a B2B supplier, end customers often ask the online casino companies to offer Evolution’s games and shows, indicating how strong their brand is not only with their online casino customers, but just as importantly with the end customers.

Larger Data Set

In slots, they have a larger data set via the NetEnt acquisition. This enables them to price their games more accurately than their competitors.

Scale and Scope Economies

Evolution has huge scale advantages versus the competition. To compete against Evolution, a competitor would need:

• a global studio presence where online games are filmed and streamed,

• unique games that are popular, and

• traditional live casino games in multiple languages.

Typically, a subscale competitor will have a limited number of games and tables which often leads to a poor customer experience and greater customer churn. Furthermore, given that Evolution has more players, developing a new game is cheaper on a per player basis than for any competitor.

Network Effects

When more people play live casino games, it improves the experience for all players. The number of active players currently on Evolution is well ahead of its competition. When you combine the scope and scale economy benefits that Evolution enjoys with the best proprietary game IP in the industry, this generates very high retention rates among their online casino customers and much higher end customer engagement with Evolution-branded games. These competitive advantages have discouraged competition in Europe and limited it in North America.

Licenses

Obtaining licenses in different jurisdictions takes time and effort. Evolution already has 10 licenses in different jurisdictions. The competition is behind. Evolution’s knowledge of the regulatory process in the European Union, and increasingly in various North American and Asian jurisdictions provides them with a speed advantage when entering new markets.

High Switching Costs

If a casino were to replace Evolution, it would lose their investment in their dedicated tables and would risk losing customers.

Strong Market Growth for the Foreseeable Future

The online live casino market, currently at 6% of the total global gambling market, is expected to double its share to 12% by 2025. The rising penetration of online gambling has benefitted from:

- increasing smartphone penetration,

- broadband availability, and

- better streaming quality.

Furthermore, COVID provided a tailwind to the sector as bricks and mortar casinos shut down operations for much of 2020 and are now operating at reduced capacity levels. However, we expect online gambling to continue grabbing share at the expense of bricks and mortar casinos well beyond the temporary COVID bump, as more national and local municipalities look for new revenue streams and open their markets to online gambling. According to Goldman Sachs, online gambling’s market share should double to 12% of the global gambling market by 2025. Furthermore, the share of live casino gaming within the online casino market should increase from 33% in 2019 to 48% in 2025 as per Goldman Sachs estimates.

The US live online casino market is in its infancy and growing fast. Currently 12 US states permit online gambling. Goldman Sachs estimates that online casino will double its share of the US market to 6% in 2025.

Attractive Economics

We forecast Evolution to grow revenue and EPS at 40%+ and 50%+, respectively, from 2020 to 2023, and at very healthy 25%+ levels between 2023 and 2025. With attractive free cash conversion attributes (FCF/EBITDA conversion of 85%) and (FCF/Sales margins of 60%), high net income margins of 55%, and very attractive returns on invested capital (ROIC) of 65%, Evolution’s high returns and long reinvestment runway, allows it to self-fund all its growth with no need to access the capital markets and diluting shareholders. Furthermore, given the semi-fixed cost nature of Evolution’s business, the investments they have made in their global studios and the online filming and streaming infrastructure, revenues from incremental customers come in at very high incremental margins.

Valuation:

Admittedly, when one looks at EVO’s valuation on one-year out earnings, trading at 29.8X 2021 Sales and 57.4X 2021 EPS, the stock looks expensive. But the company is expected to grow its top and bottom lines at 40%+ over the next 3 years. When you normalize for that growth, the stock is really trading at 1.4X PEG ratio which is reasonable in our view.

Ending Thoughts

We look forward to continuing to share our thoughts on our investment approach, and to keep you abreast of our performance and changes to the portfolio. In the meantime, if you have any questions, please feel free to reach out to us at the links below.

With best wishes,

Aamer Khan

Co-founder

Cyril Malak

Co-founder