Summary

- India has a young and growing population, which means that the addressable market for life insurance will continue increasing for decades to come.

Q2 2021 hedge fund letters, conferences and more

- Currently, only 1% of the protection needs of Indians are being covered by life insurance but that may change as the Covid pandemic has created increased awareness for protection.

- India has four life insurance companies available for public market investors (HDFC Life, SBI Life, ICICI Prudential Life and Max Financial Services). These companies don’t have ADRs but can be accessed through funds that track the Nifty Financials Services 25/50 index.

As economies around the world have re-opened after Covid, credit card companies in developed economies have been pointing to a rebound in spending on restaurants, hotels and air travel. In India, a key contributor to rebounding consumer spending has been people spending more on insurance. On its June quarter earnings conference call, ICICI Bank management noted that “Credit card spends declined in April and May but improved to March levels in June, driven by spends in categories like consumer durables, utilities, education and insurance.”[1]

What makes insurance a growth category in India? And how long can this growth continue? Answering these questions shows us why India’s publicly listed insurance companies – specifically life insurance companies – may be poised for outperformance.

India’s Demographics

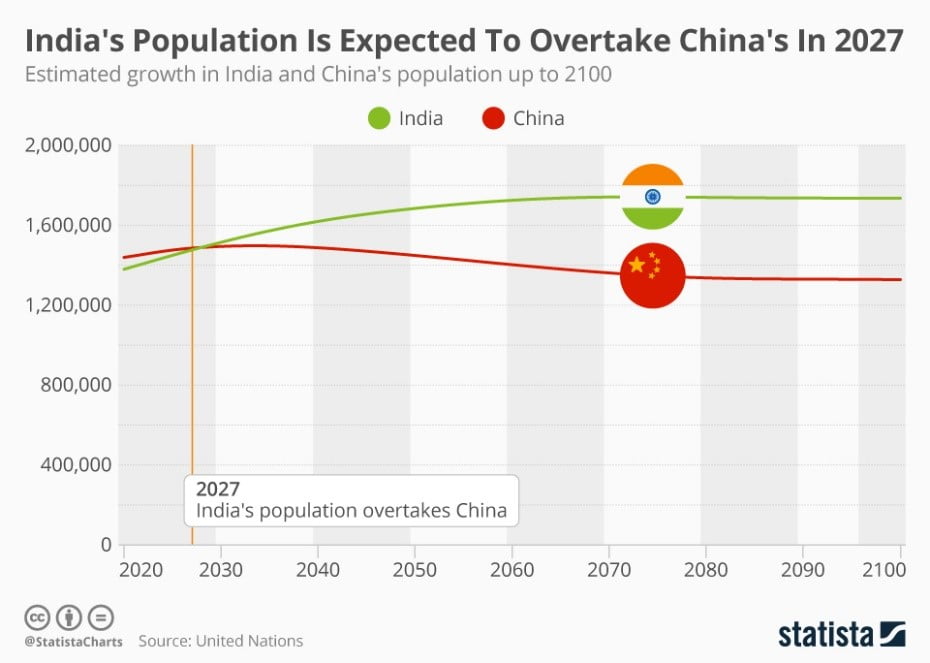

India is projected to become the world’s most populous country in 2027 and its population is projected to continue growing from there for the next five decades, according to the following chart from Statista:

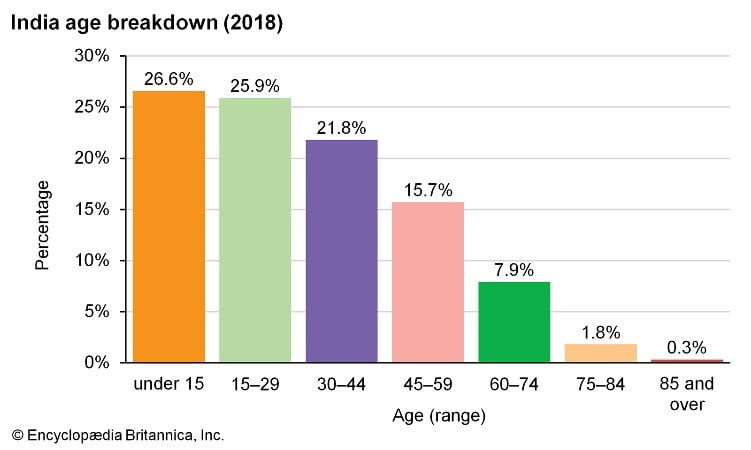

India’s population is also relatively young; the majority of Indians as of 2018 were under 30 years of age. As more and more Indians enter the workforce, their access to — and need for — all types of financial products will increase. For example, a young professional will need a credit card for consumption and durable good purchases, an auto loan for the first motorcycle or car, a mortgage loan to finance a first home, and health and life insurance for financial planning. In fact, Indian life insurer HDFC Life disclosed that the average age at which a new customer signs up for an insurance product is 36 years – which means that the majority of Indians are likely to hit the age range when they become insurance customers in the coming years.

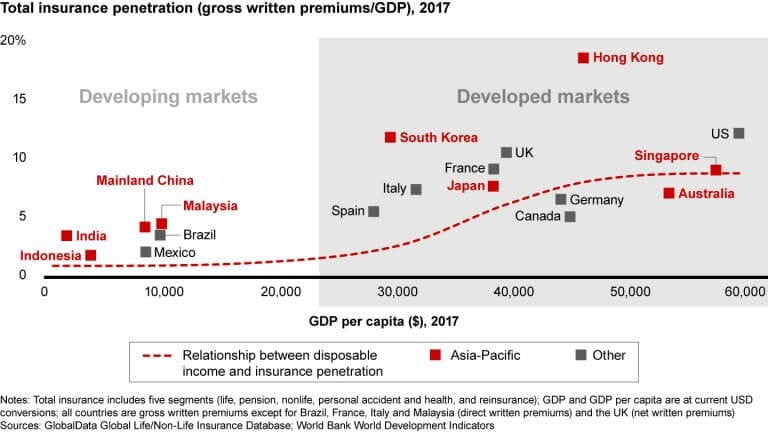

Finally, India is very much a developing market with GDP per capita of about $2,000. As economies grow – and specifically as they transition from developing to developed markets – insurance penetration as a share of GDP tends to increase. Although India’s GDP per capita is still a long way from $25,000+ per year, the chart below from Bain & Company shows the long runway ahead for India’s insurance sector:[2]

In summary, insurance companies in India benefit from multiple growth vectors: 1) a large and growing population, 2) an age distribution that lends itself to rising demand for financial products including insurance and, 3) rising GDP per capita, which correlates with rising insurance penetration as a share of GDP.

India’s Life Insurance Sector

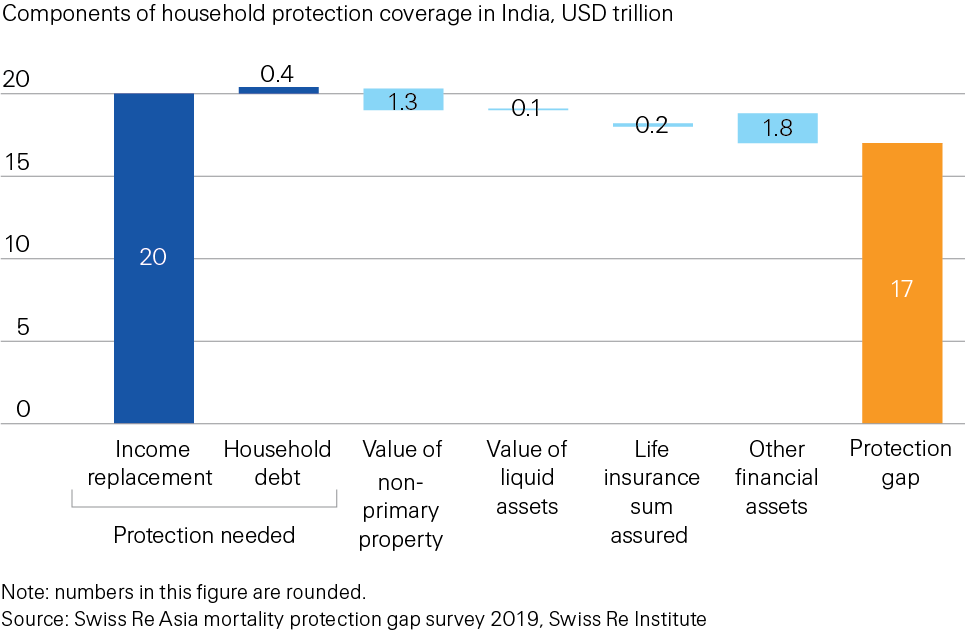

The global reinsurance company Swiss Re has estimated a “protection gap” across major economies in Asia. The concept of a protection gap refers to the amount of money needed to replace income and pay off financial debts in the event of death of a household’s primary breadwinner. In its 2019 mortality protection gap survey, Swiss Re found that “life insurance as a means of protection is virtually non-existent. This leaves over 80% of protection needs unmet, the highest in Asia.”[3] In fact Swiss Re estimated that India has a $17 trillion protection gap, which compares to $0.2 trillion of life insurance sum assured, indicating that life insurance is only covering 1% of the unmet protection needs of Indians. For comparison purposes, life insurance sum assured in China is $2 trillion compared to a protection gap of $41 trillion (indicating that life insurance covers about 5% of the unmet protection needs). A more advanced economy like Japan has $2.8 trillion in life insurance sum assured compared to a $8.4 trillion protection gap.

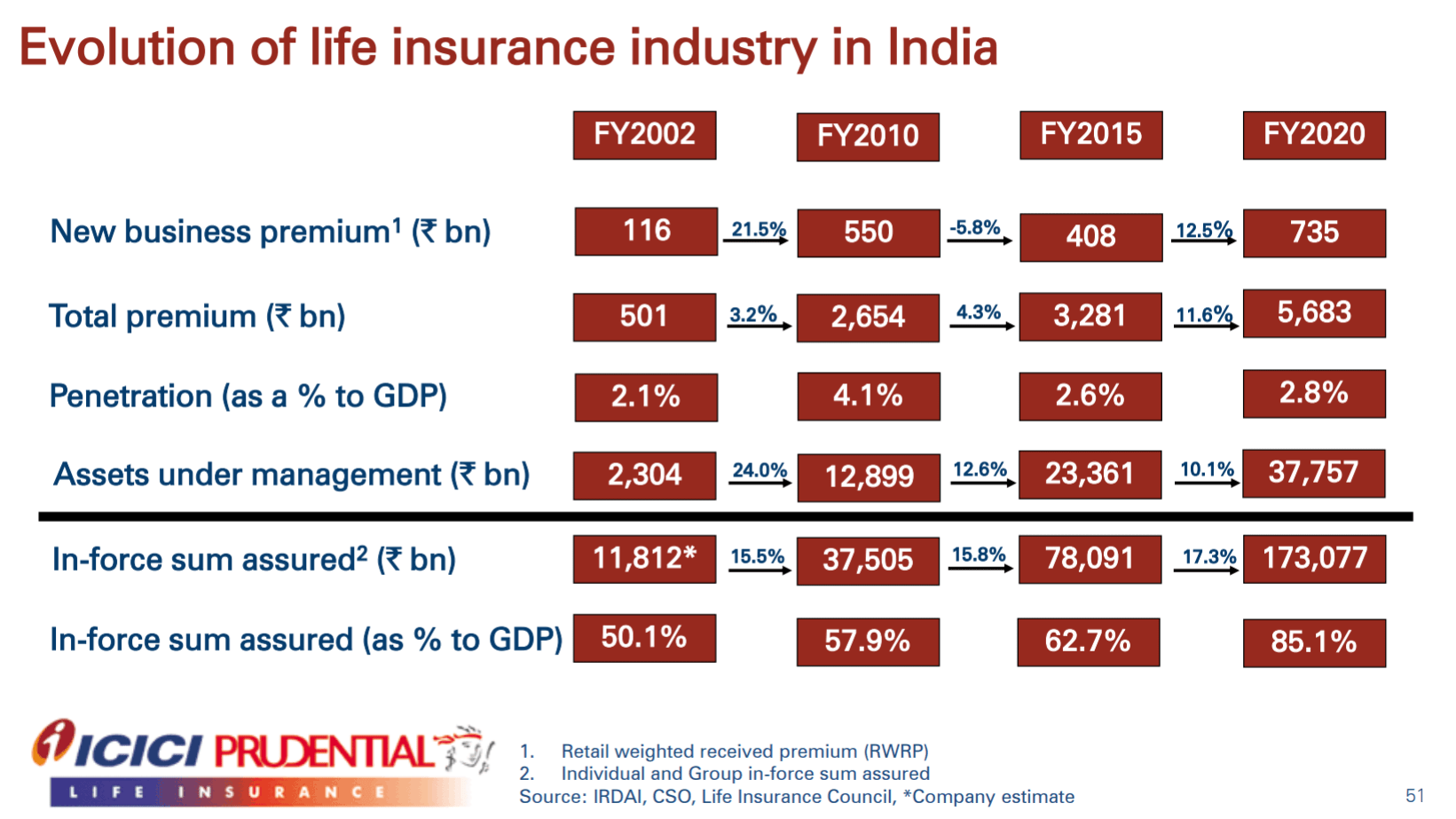

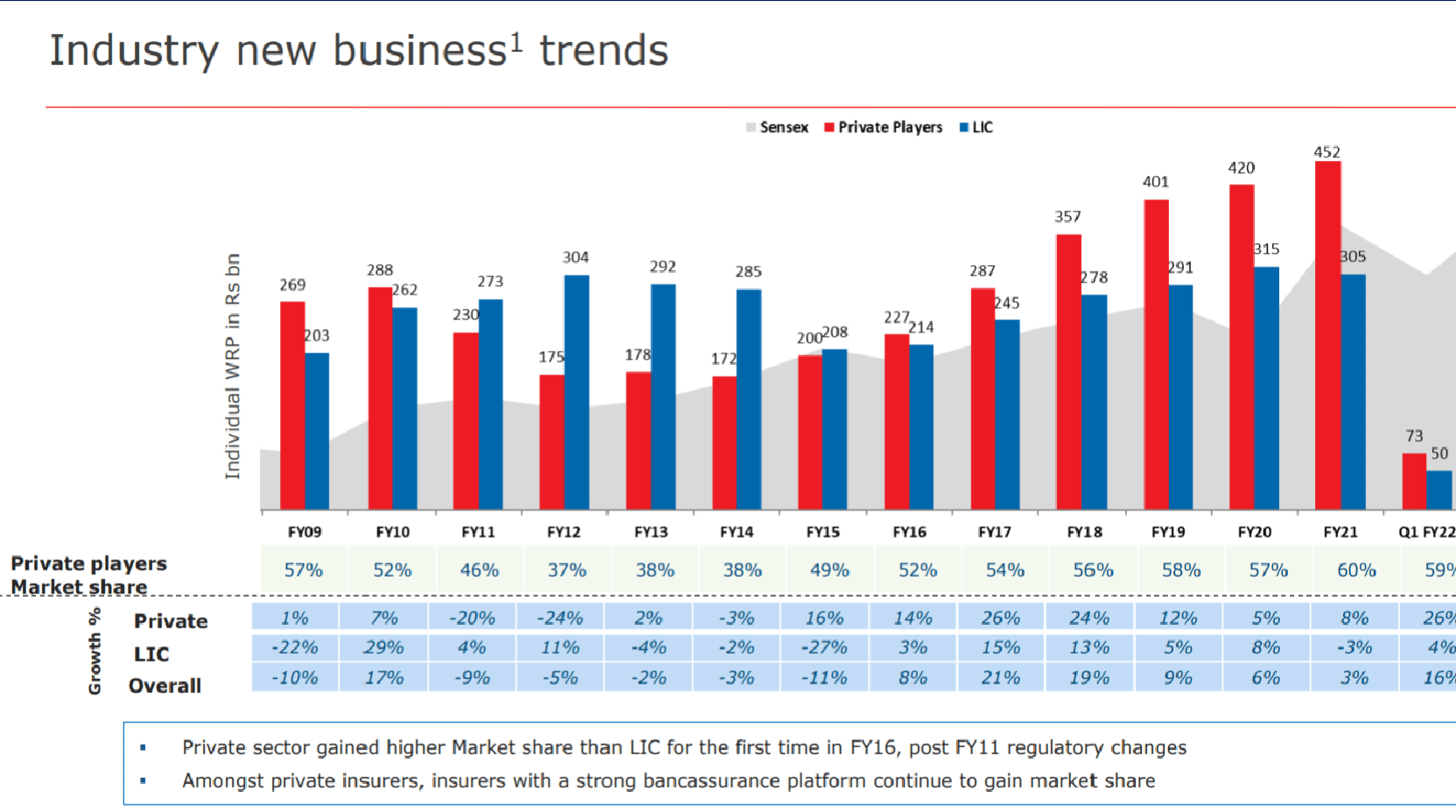

India’s life insurance sector has been a growth sector, albeit with its share of cyclicality. From FY 2002 to FY 2010, new business premium (which is the leading indicator of total life insurance premium and in turn sum assured) grew at a 21.5% CAGR, according to the Indian insurance company ICICI Prudential Life. In her research paper, “Liberalization of India’s Life Insurance Sector,” Dr. Lalitgauri Kulkarni argues that the rapid growth of India’s insurance sector during this timeframe was due to India allowing private sector insurance companies to compete with state-run Life Insurance Corporation (LIC)[4]. The private sector companies rapidly increased their market share from 1% in FY 2002 to 35% in FY 2010 in part by promoting a hybrid insurance/investment product called Unit Linked Life Insurance. This type of policy came under increased regulatory scrutiny in 2011 which caused the market share of private sector insurance players to stagnate. Beginning in FY 2015 and until FY 2020, new business premium for India’s life insurance sector returned to a growth CAGR of 12.5%. The chart below is from ICICI Prudential’s investor presentation for F1Q 2022.[5]

According to Indian insurance company HDFC Life, the resumption of growth since FY 2015 has been on the back of private sector life insurers resuming their market share gains against state-run LIC. In the aftermath of regulatory changes to their main product in 2011, the private sector life insurers developed new products and broadened their distribution footprints.

Today, for India’s private sector insurance companies, over 60% of premium received is from non-unit linked insurance products and distribution channel mix is 23% from individual agents, 54% from bank relationships, 17% from direct/online and the remainder from other sources.[6]

Share of Individual Weighted Received Premium – Private Players vs. LIC. Source: HDFC Life.

Investing Ideas In India’s Life Insurance Sector

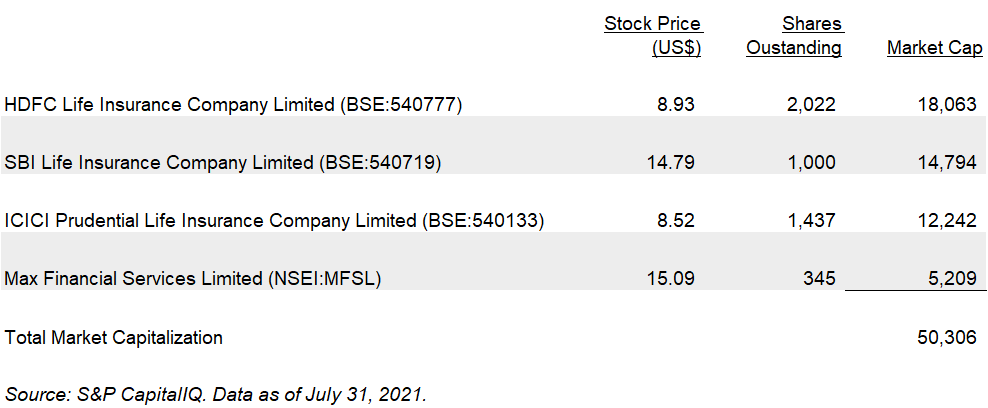

With that background, let’s take a look at some of the investment opportunities available to public market investors in India’s life insurance sector. There are four publicly listed insurance companies in India with an aggregate market capitalization of $50 billion.

All publicly listed life insurance companies trade on the National Stock Exchange in India and don’t have ADRs. However, certain life insurance companies be accessed via funds that track the Nifty Financial Services 25/50 Index.

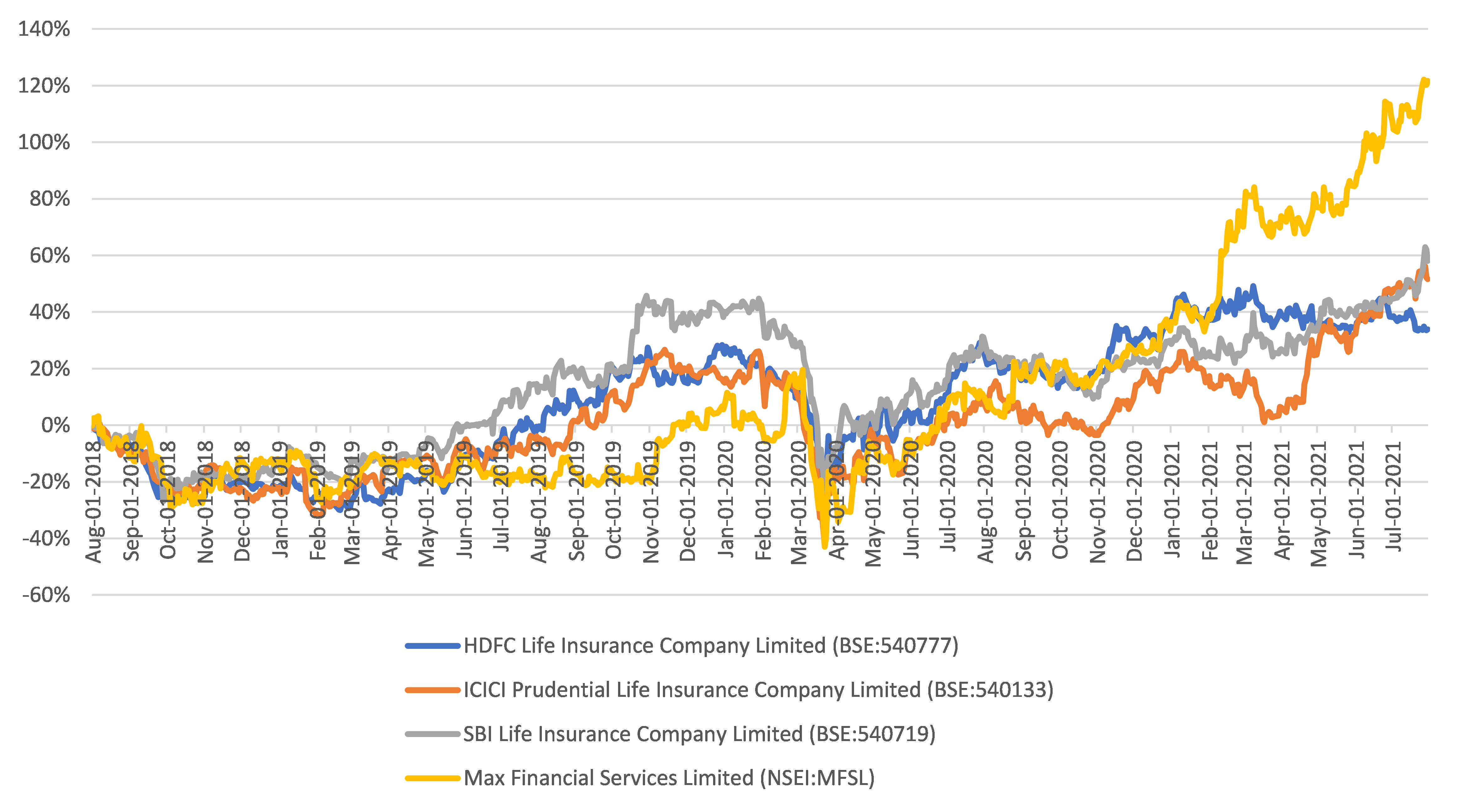

India’s four publicly listed life insurance companies have seen their share prices go up between 34% and 122% over the last three years. After suffering a sell-off when India announced a nation-wide lockdown during the first wave of Covid-19, Indian life insurance stocks have recovered as investors have re-focused on the outlook for future growth.

Stock Price Performance Of India’s Four Publicly Listed Life Insurance Companies

Source: S&P CapitalIQ. Data as of July 31, 2021.

What explains the performance of India’s life insurance stocks despite the country experiencing one of the world’s worst Covid outbreaks? According to official government data, India experienced 424 thousand deaths related to Covid out of 31.7 million total cases (for comparison, the US has reported 613 thousand Covid-related deaths from 35 million cases). In fact, Indian life insurer SBI Life Insurance disclosed that Covid-related death claims in the June 2021 quarter were 1.3x the number of Covid-related death claims in all of the twelve months ended March 31, 2021. Nevertheless, SBI Life produced profits and grew its net worth during the June 2021 quarter.

Investors may be looking ahead to accelerating growth for the sector. In June 2021, Reuters reported that “When a devastating second wave of the pandemic peaked in India during April and May, the numbers of people aged between 25 and 35 buying term insurance was 30% higher than in the previous three months combined, said PolicyBazaar, India’s largest online insurance aggregator,” and that “Industry executives say enquiries about insurance plans have rocketed despite the second wave of infections subsiding, probably due to strong prospects of a third wave given the slow start India made to the mammoth task of vaccinating its people.”[7] These anecdotes suggest that awareness and demand for life insurance have been positively impacted by India’s devastating Covid experience.

Even if business trends don’t accelerate, the management teams of India’s private sector life insurers have put forth impressive growth plans. A key metric that investors track is “value of new business” or VNB. VNB takes into account both the value of new insurance policies sold and the expected profit margin on those policies (which can vary depending on business mix). Investors consider VNB a better metric that reported profits in any given period because as selling costs are front-loaded, an insurance company will show higher losses the faster it grows.

ICICI Prudential Life Insurance expects its VNB to grow at a 28% annual growth rate between FY 2021 and FY 2023. Similarly, sell-side analysts expect HDFC Life and SBI Life’s VNB to compound at 20% or more during that timeframe.[8]

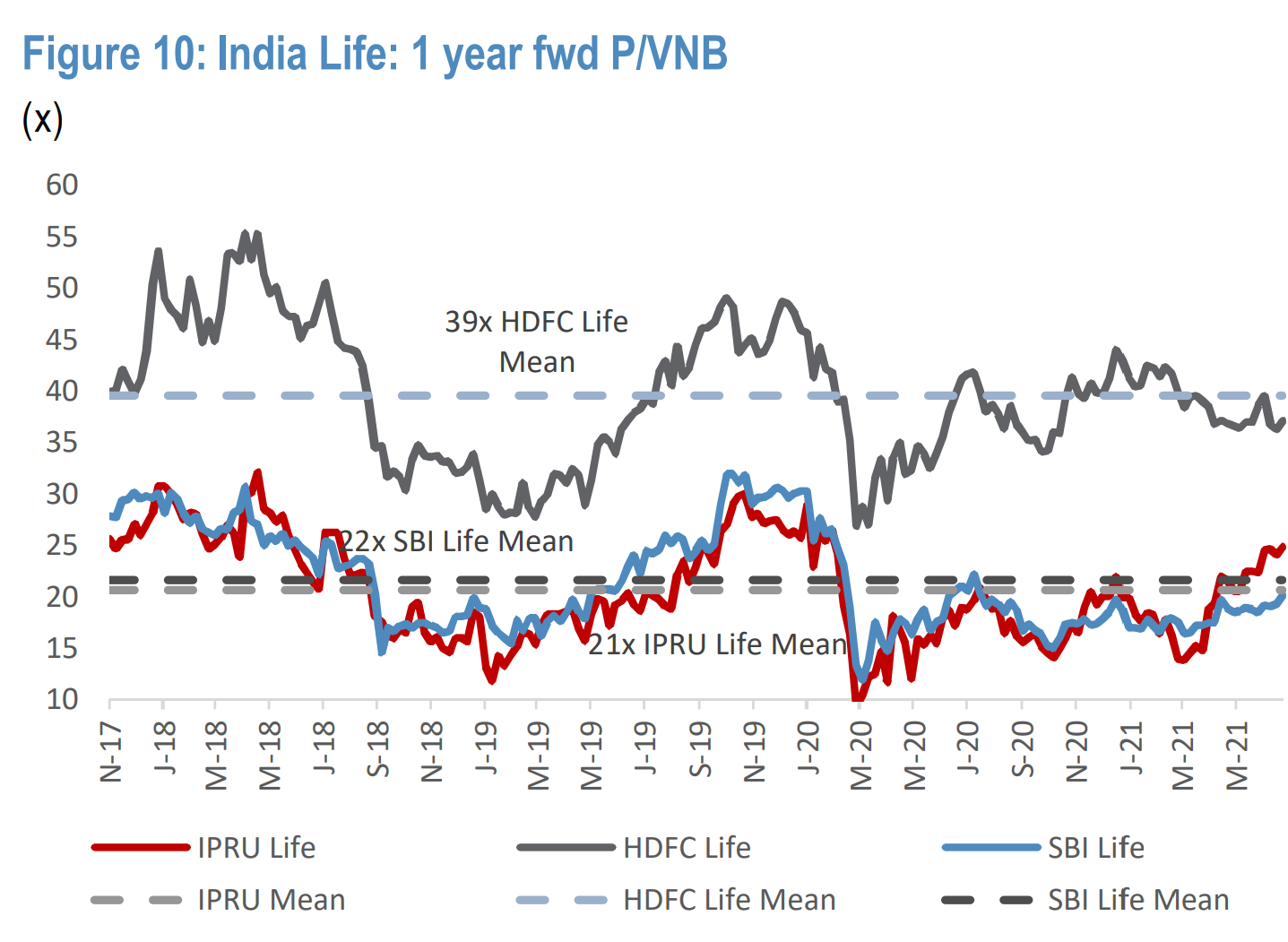

The three large publicly listed life insurers (HDFC Life, SBI Life and ICICI Prudential Life) are trading at or around their historical multiples of price to VNB. Therefore, even if their VNB compounds in line with current projections (i.e. not assuming any accelerating in the business), Indian life insurers’ shares may provide attractive returns over the next two years.

Price/1 Year Forward VNB

Source: JPMorgan.

However, with cheap capital available to insurance companies and other strategic investors globally and given the long growth runway available to Indian life insurance companies, it is possible that increased strategic interest will cause Indian life insurers’ multiples to expand. In February 2021, India’s government made it easier for foreign companies to invest in India’s insurance companies. It announced that foreign entities will be able to control up to 74% of insurance companies, up from 49%.[9]

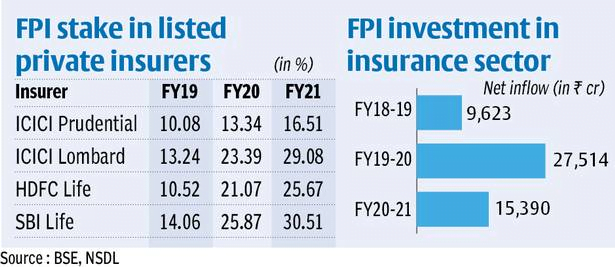

Foreign investors in Indian equities have been fans of the Indian life insurance story and money has flowed into the insurance sector for each of the last three fiscal years. Foreign ownership in Indian insurance companies has steadily increased and now represents between 16% and 30% of the total shareholding of those companies, according to this chart from The BusinessLine[10]:

Based on the potential growth runway available to Indian insurance companies, investors’ appetite for Indian insurance stocks may continue for years to come.

About the Author

Amit Anand is the co-founder of NextFins. NextFins was founded in 2020 with the goal of democratizing access to powerful investment ideas. For more information, please visit http://www.indiafinancials.com/

Footnotes

[1] https://www.icicibank.com/managed-assets/docs/investor/quarterly-financial-results/2022/Transcript-for-Analyst-Call-held-on-July-24-2021.pdf [2] “Asia-Pacific’s coming insurance boom” https://insuranceasianews.com/asia-pacifics-coming-insurance-boom/ [3] “Indian consumers are the most vulnerable out of all Asia-Pacific markets surveyed,” https://mortalityprotectiongap.swissre.com/#/overviews/India [4] https://dspace.gipe.ac.in/xmlui/bitstream/handle/10973/46953/GIPE-WP-39.pdf [5] https://www.icicibank.com/managed-assets/docs/investor/quarterly-financial-results/2022/2021_04_Q1-2022_Investor_presentation.pdf [6] https://brandsite-static.hdfclife.com/media/documents/apps/HDFC%20Life%20Presentation%20-Q1%20FY%202022.pdf [7] “Shocked by COVID deaths, young Indians rush for life insurance” https://www.reuters.com/world/india/shocked-by-covid-deaths-young-indians-rush-life-insurance-2021-06-16/ [8] Source: JPMorgan research. [9] “India’s more relaxed rules on investment in insurers set to attract U.S., European players” https://www.reuters.com/article/india-budget-insurance/update-1-indias-more-relaxed-rules-on-investment-in-insurers-set-to-attract-u-s-european-players-idUSL1N2K71H4 [10] “FPIs bet big on private insurers” https://www.thehindubusinessline.com/money-and-banking/fpis-bet-big-on-private-insurers/article34480992.ece