Gator Financial Partners commentary for the first quarter ended March 31, 2021.

Q1 2021 hedge fund letters, conferences and more

Dear Gator Financial Partner:

We are pleased to provide you with Gator Financial Partners, LLC’s (the “Fund” or “GFP”) Q1 2021 investor letter. This letter reviews the Fund’s first-quarter investment performance and the sale of our Credit Suisse position. We also discuss our investment thesis on Royal Bank of Canada.

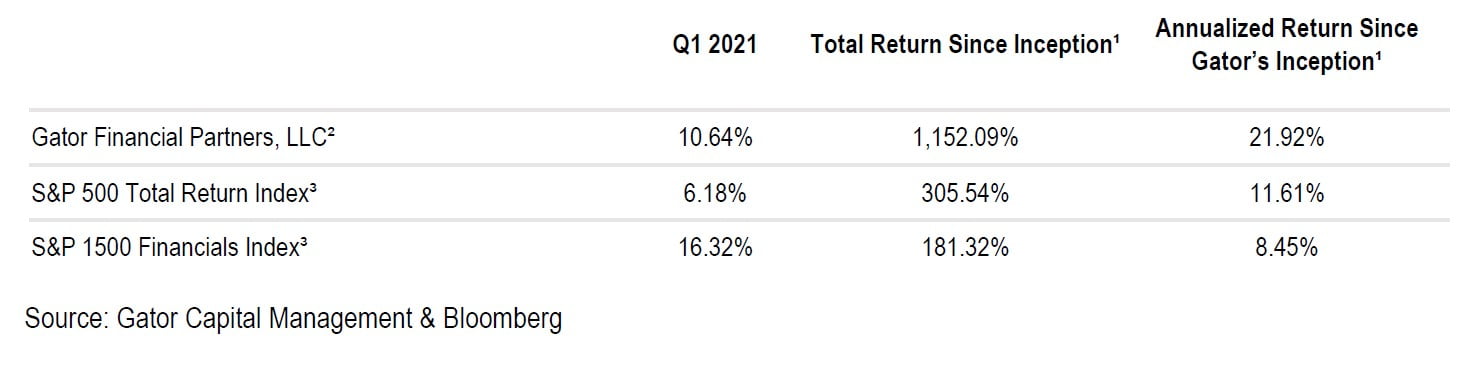

Review Of Q1 2021 Performance

For the first quarter of 2021, the Fund outperformed the overall market but lagged the Financials sector benchmark. Navient, SLM Corporation, and Western Alliance Bancorporation were top contributors to performance. The largest detractors were Fannie Mae preferreds, Credit Suisse, and our short position in Lending Club.

Credit Suisse

We were extremely disappointed with the news from Credit Suisse in March. We were blindsided with a double dose of management incompetence. In early March, Credit Suisse announced they were suspending redemptions on the bank’s investment funds related to Greensill’s trade finance business. Then, in late March, the bank announced that it had exposure to the family office Archegos. We believe that of all Wall Street banks, Credit Suisse had the worst response managing the risk presented by Archegos. The combination of these two events in the same month made it clear that the bank does not have adequate risk controls.

We sold our position in Credit Suisse in late March, ending a three-year period of holding shares in the company. Our investment thesis had been Credit Suisse 1) was a global wealth management franchise with an attractive growth rate, 2) had a low-risk, highly profitable domestic Swiss banking franchise, 3) had reduced capital intensity and volatility in the investment bank, and 4) traded for just 75% of tangible book and 8x forward earnings. We believe the bank will be in the penalty box with investors for multiple years due to these risk management failures. We view this situation as similar to Wells Fargo’s account opening scandal from four years ago. Wells Fargo has underperformed the S&P 1500 Financials Index by 95% during that. We believe Credit Suisse’s stock will probably underperform its peers for several years as well.

Canadian Banks

We believe Canadian banks are attractive relative to US banks right now. Canadian banks are as cheap as they’ve been compared to US banks in the last 20 years. The Canadian banking system is an oligopoly of five national banks. This oligopoly in Canada has allowed the banks “North of the Border” to post higher returns with less cyclicality than their US peers.

US banks have had a huge run in the last six months due to investor optimism about potential economic strength as a result of the good news about coronavirus vaccines. Since we wrote about regional banks being a “once in a decade buying opportunity” in our Oct. 27th letter, the S&P Regional Banking ETF (“KRE”) is up 64%! Although we feel US banks still have upside, the opportunity in US banks from here on out is not as attractive as Canadian banks due to relative valuations. Canadian banks have slowly lost their valuation premiums over the past 10 years.

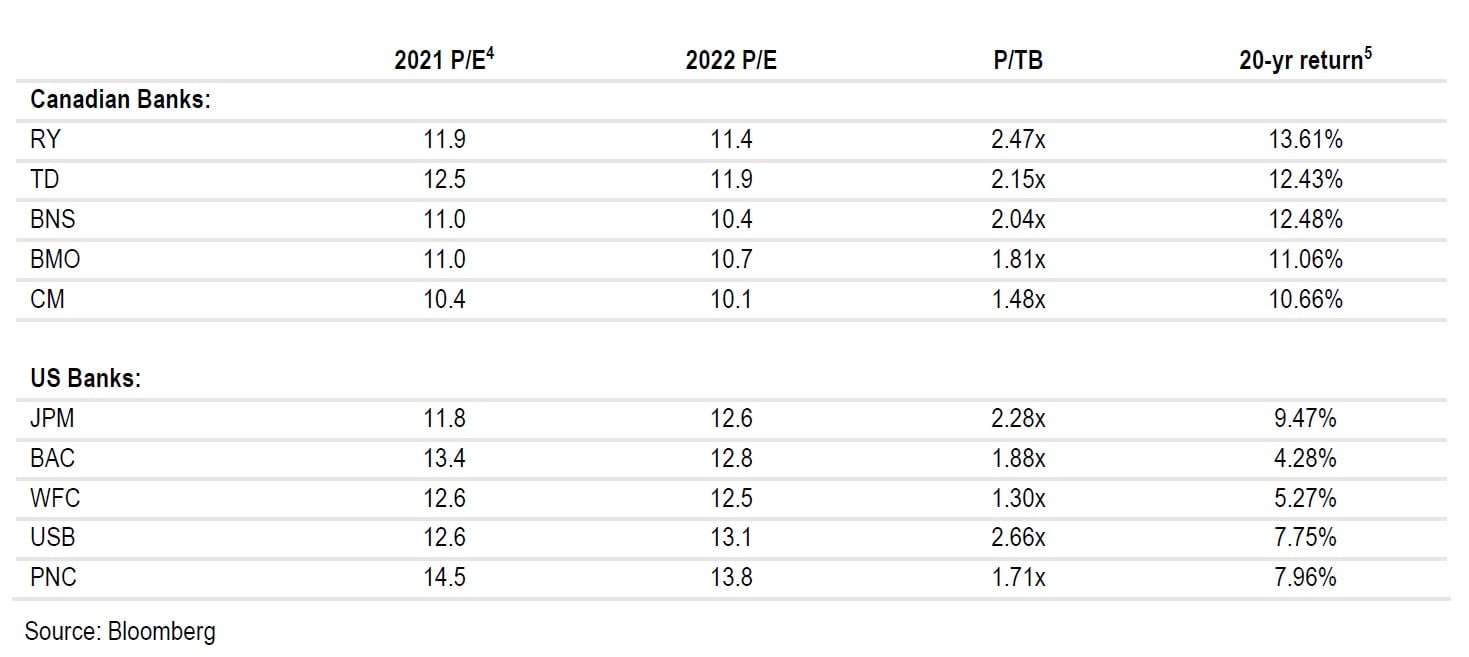

The table below shows the current valuations and 20-year annualized returns of the five largest Canadian banks versus 5 of the top 6 US banks. We excluded Citigroup because its poor performance and returns. As you can see, the Canadian banks generally have lower valuations even though they have all outperformed the US banks.

We own a position in Royal Bank of Canada (“RBC”) and are completing our due diligence on several other Canadian banks. Royal Bank is the #1 bank in Canada. It has a business mix similar to JP Morgan Chase (“JPM”) with strong retail and corporate banking businesses. It also has a significant investment banking and asset management business. From here, we believe Canadian bank stocks will generate attractive returns for shareholders in the medium and long term.

Here is more detail on our investment thesis for Royal Bank of Canada:

1. Bank with consistently high returns – RBC consistently posts Return on Tangible Common Equity (“ROTCE”) in the low 20%. In contrast, JPM has reported ROTCE between 12% and 19% over the last six years. We think this reflects the higher margins of the Canadian banking system.

2. Leading bank in Canada – RBC is the leading bank in Canada. It has the highest returns, the highest market share, and the highest valuation of the five major Canadian banks. We believe other stock market investors will favor RBC when Canadian banks regain favor.

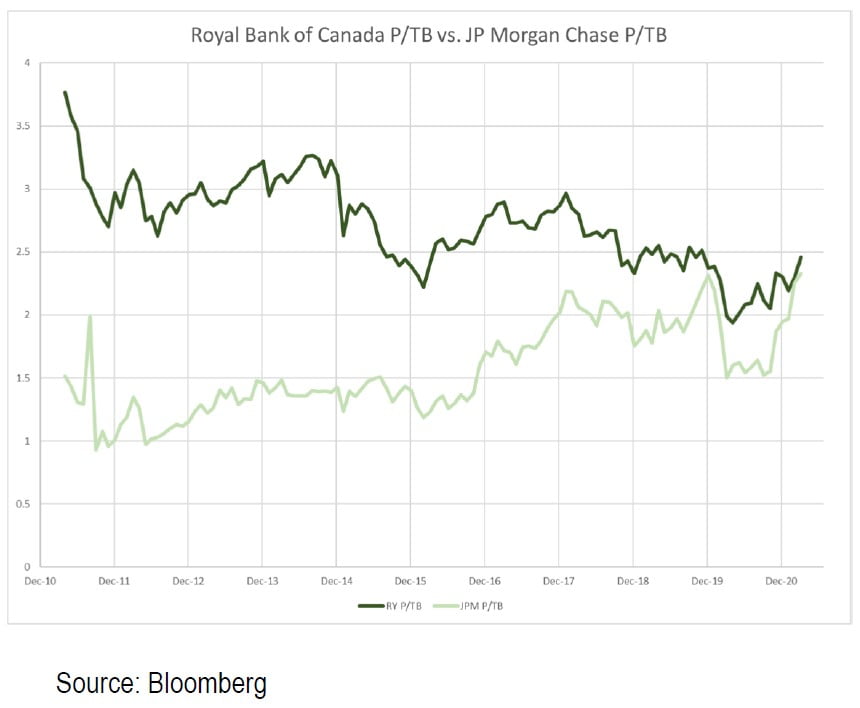

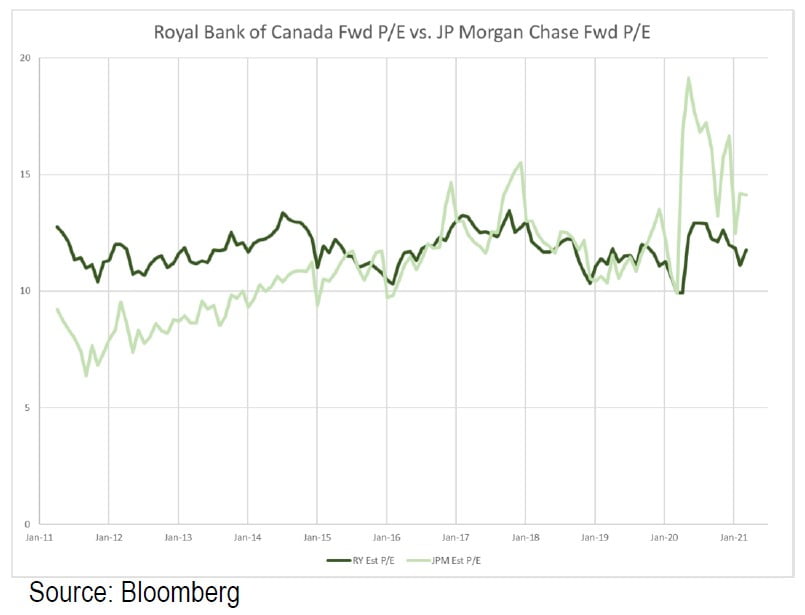

3. Low relative valuation to US Banks – Canadian banks have had premium valuations compared to US banks for a few decades due to their higher and more consistent returns. Over the last 10 years, this valuation premium has almost disappeared. The chart below shows the price-to-tangible book ratio (“P/TB”) of RBC compared to JPM’s. As you can see, in 2011 RBC traded at 3x P/TB while JPM traded at 1x. Now, both banks trade at 2.5x P/TB.

4. Strong growth at City National – RBC’s US Subsidiary, City National Bank, is growing very quickly. RBC purchased City National in 2015. City National was an LA-based bank focused on high-net-worth customers. At the time of the purchase, City National had already expanded and gained traction in San Francisco and New York. Now, City National has branches in Washington, DC, Atlanta, Miami, Dallas, Minneapolis, San Diego, and Las Vegas. City National has a banking strategy similar to that of First Republic and is growing at a comparable rate. We would note that First Republic trades at 26x 2021 estimated earnings.

5. Solid management team – Chief Executive Officer, Dave McKay, has led the bank for the last seven years. He has been at RBC for his entire career and has run several of the business units as he climbed the corporate ladder. Rod Bolger has been Chief Financial Officer for almost five years and has worked at RBC for 10 years. Prior to joining RBC, Bolger worked at Bank of America and Citigroup. We think both men are good bankers and good stewards of shareholder capital.

6. Consistent capital management – RBC has had a consistent policy of reinvesting for organic growth, paying a dividend, and using excess capital to repurchase shares. None of the five major Canadian banks have cut their dividend payouts since World War II. At 3.7%, RBC’s dividend yield is higher than any major US bank.

7. Potential for a stronger Canadian dollar – The Canadian dollar loosely tracks the price of oil. It seems when crude oil is below $60 per barrel, the Canadian dollar trades at 70 cents compared to the US Dollar. When crude oil approaches $100 per barrel, the Canadian dollar trades closer to parity with the US dollar. We do not have a strong view on crude oil prices. Still, we would note that we seem headed toward a strong economic recovery from the pandemic, and crude oil prices generally reflect the level of economic activity.

For the last eight years, we have seen investors shorting Canadian banks due to the housing markets in Toronto and Vancouver. We believe this short thesis is stale and hasn’t come to fruition. We believe different dynamics drive the Canadian housing market than the US housing market in 2008. We do not see the banks engaging in risky lending practices. The substantial problem in the US market in 2008 was due to risky loans with low or no documentation and loans to subprime borrowers. We don’t see evidence of either of these practices in Canada. We admit that the residential property markets in Toronto and Vancouver appear very expensive, but we believe the pricing reflects the strong demand for housing in global cities with land-constrained markets. We think both Toronto and Vancouver will benefit from immigration policies in the US making it difficult for high-quality immigrants to enter. We compare Toronto and Vancouver to New York and San Francisco and see similar pricing. We would point out that both New York and San Francisco fared relatively well during the 2008 US housing crash. Also, we do not see concerning house pricing trends in the rest of Canada.

We do believe there are real risks in the RBC story:

1. Energy Exposure – The Canadian economy is more natural resource dependent than the US economy. Oil and gas production accounts for a significant proportion of the economy. This presents two risks to RBC: 1) direct credit risk to energy companies, and 2) Canadian dollar risk due to the Canadian dollar’s high correlation to the price of oil. As the world moves away from fossil fuels, Canada’s economy will have to transition as well. In the short-term, this is less of a concern due to the economic strength supporting the price of oil.

2. M&A – We would prefer RBC to not make a large acquisition in the US, but we are realistic that they may. We would say their M&A track record is mixed. First, their roll-up of US retail stockbrokers in the 1990s has worked very well. Also, their 2015 acquisition of City National Bank has performed well. However, during the 2000s, RBC bought Centura Bank in North Carolina, Eagle Bancshares in Georgia, and Alabama National BanCorporation. RBC was not able to improve the returns of those three US bank acquisitions and sold the operation to PNC in 2012. RBC lost at least $1 billion over 11 years from these acquisitions. We’re hopeful that RBC’s management team has learned its lesson and won’t try to acquire another generic US bank. We would rather they continue to organically grow the old City National franchise, which focuses on high-net-worth customers in major US cities.

3. Vaccine distribution in Canada – A short-term risk is that vaccine distribution in Canada is going more slowly than in the US. So, the Canadian economy might recover more slowly than the US economy. We believe this risk is small because we think stock market investors will look through this issue. However, we are concerned about further lock-downs in Canada, like the recent second shut-down in Ontario.

Given the large rally in US bank stocks, we are moving out of some US banks and into Canadian banks. We have long admired the banking oligopoly in Canada, but we had stayed away due to the hefty premium that the Canadian banks had over the US banks. That premium is largely gone now. We think the Canadian banks will regain their premium valuation over the US banks. We see parallels between buying the Canadian banks now and our call to buy “Growth banks” like SIVB and WAL in 2019. Growth banks had lost their premium valuation because they were asset-sensitive. They have since regained their premium valuation. We think the same thing will happen for the Canadian banks.

Portfolio Analysis

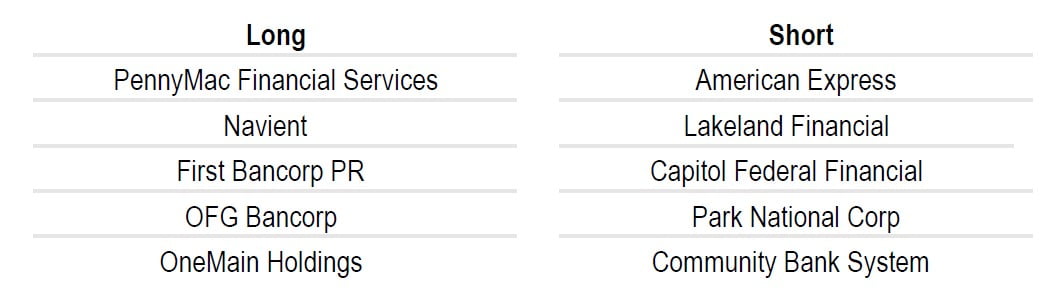

Below are the Fund’s five largest common equity long and short positions. All data is as of March 31st, 2021.

Sub-Sector Weightings

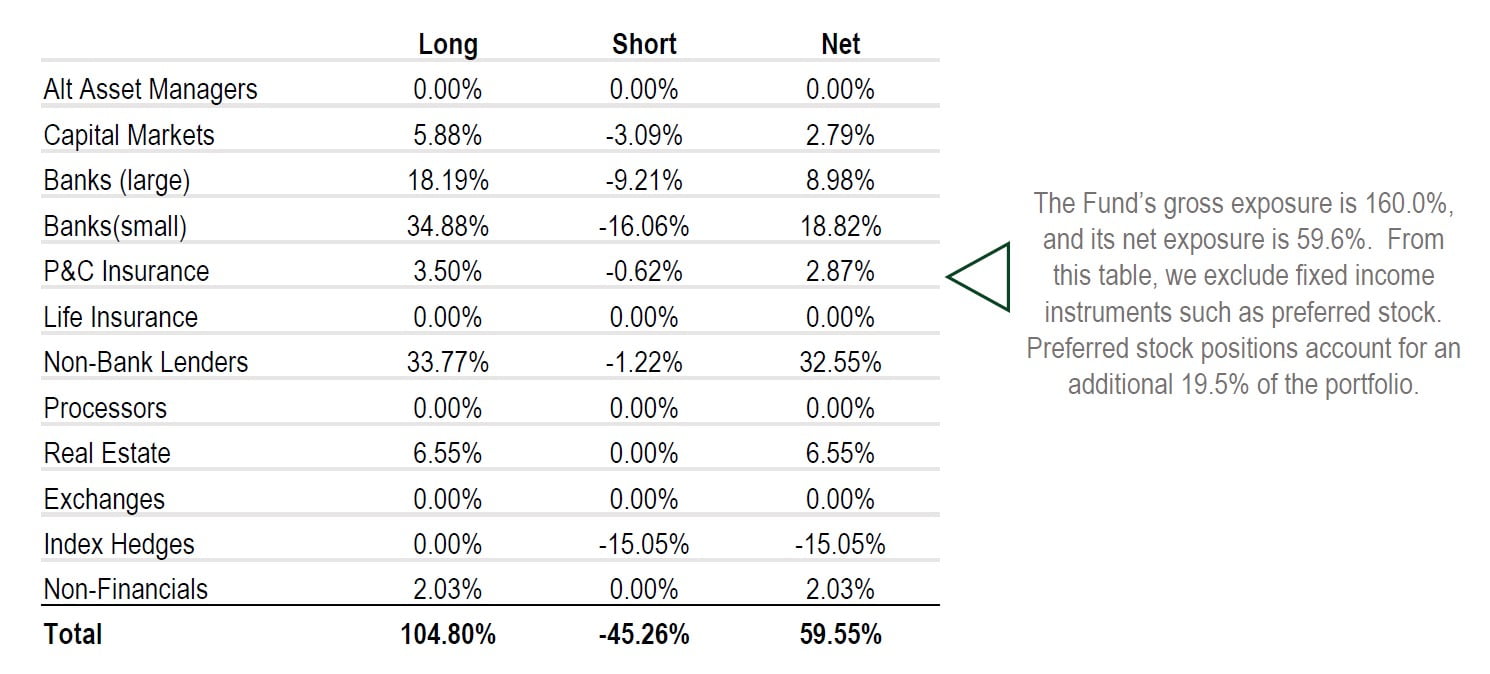

Below is a table showing the Fund’s positioning within the Financials sector as of March 31st:

Conclusion

Thank you for entrusting us with a portion of your wealth. We are grateful for investors like you who believe and trust in our strategy. On a personal level, Derek Pilecki, the Fund’s Portfolio Manager, continues to have more than 80% of his liquid net worth invested in the Fund.

As always, we welcome the opportunity to speak with you and discuss the Fund.

Sincerely,

Gator Capital Management, LLC